By monthly tradition, you’ll get an update on our Best Buys of the month.

What’s going on in the markets? And what are our favorite stocks?

Let’s get a little bit wiser today.

November 2025

The S&P 500 was flat in November.

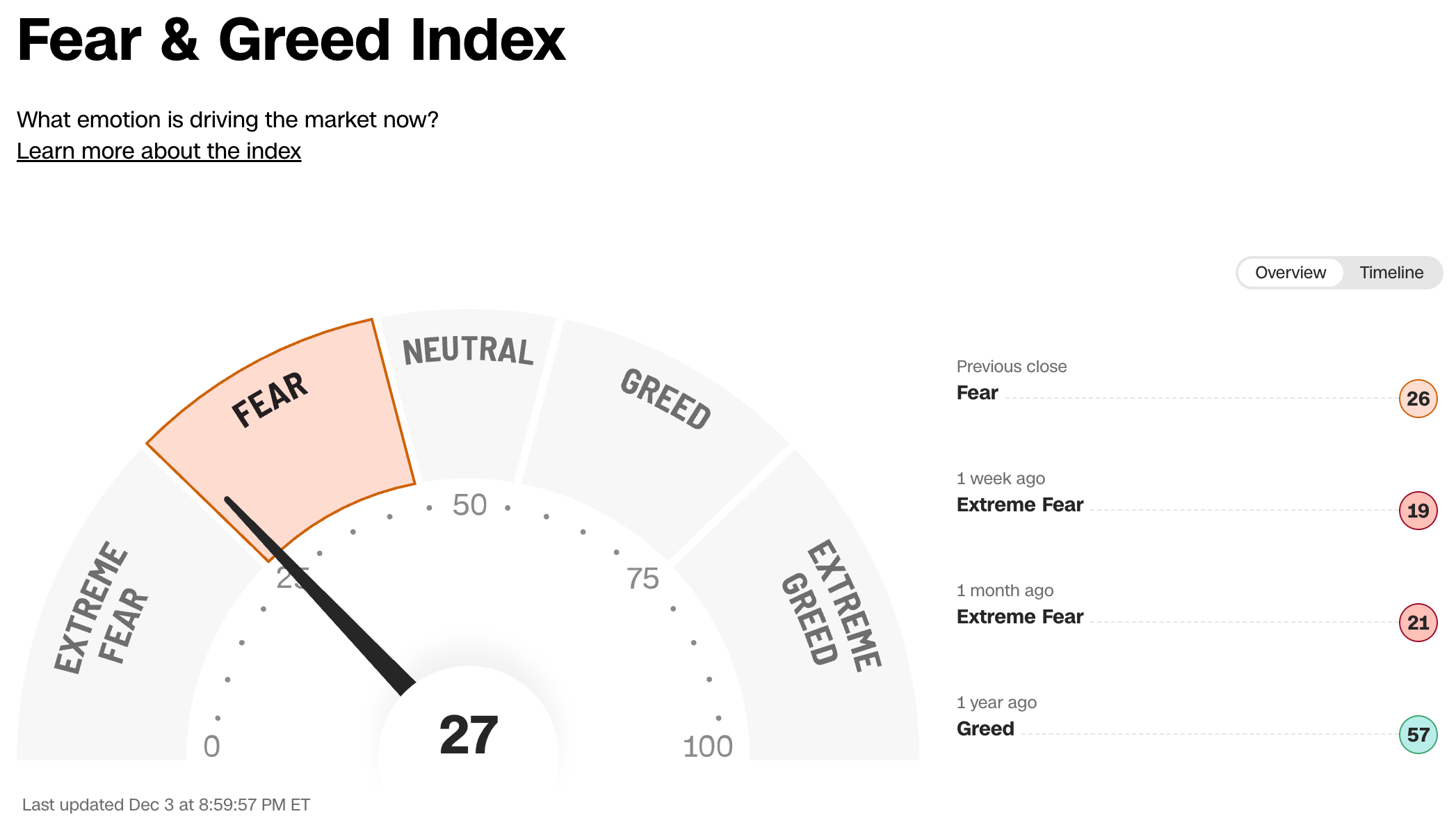

Investors are Fearful today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

Worst performers

The cheaper we can buy great companies, the better.

Here are the worst performers of the past month:

MercadoLibre is an interesting business. The CEO Marcos Galperin recently said the following on X (Twitter):

"MercadoLibre is the only public company in the world (out of +83.000 public companies) to grow more than 22 consecutive quarters in a row at a yearly rate greater than 30%. Currently we have done this for 27 consecutive quarters."

Best performers

Here are the best performers of November:

Games Workshop published great results. The stock trades at an all-time high now:

Spotlight: Paycom Software ($PAYC)

How does Paycom make money?

Paycom is a cloud-based payroll and human capital management (HCM) software provider. They sell their all-in-one software platform to businesses to manage the entire employee lifecycle, from talent acquisition and time tracking to payroll and benefits administration. Recurring revenue from subscriptions and services makes up over 90% of their sales.

Brief introduction

Paycom was one of the first companies to offer web-based HR and payroll tech.

The company was born in 1998.

It has been led by its founder, Chad Richison, since day one.

Paycom’s secret weapon is their focus on employee-driven payroll, primarily through a product called Beti.

This feature puts the responsibility on employees to check and approve their own payroll before it gets paid out.

It results in dramatically reduced administrative errors and manual data entry, which saves the client company time and money.

Another thing we love to see?

Insiders still own 11.6% of the company.

Founder and CEO Chad Richison is the largest shareholder with a stake of 10.7%.

Competitive advantage

Paycom’s key advantage is that all its software runs on one database.

This has lots of advantages when compared to competitor’s systems.

Competitors often piece together different HR modules:

Remove the need for extra databases: It stops the mistakes that happen when you have to move data by hand between systems.

Keeps one clear record for every employee: No confusion or mistakes that happen when different teams have slightly different info.

Provides better data and reporting: Managers can make reports that pull info from everywhere at the same time and show it right away.

Paycom also enjoys high switching costs. Why? Changing payroll systems is expensive and difficult.

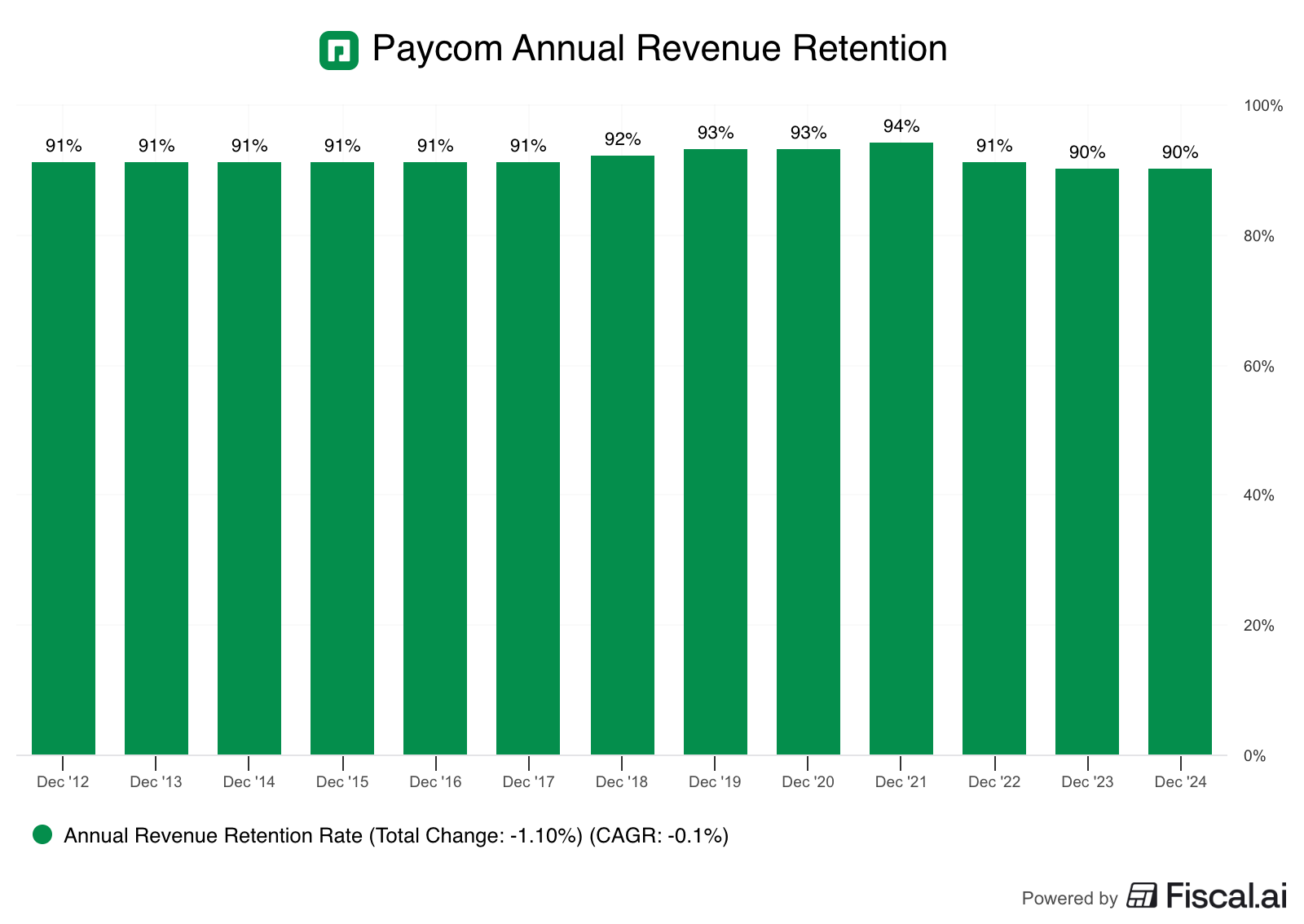

Their annual revenue retention rate is very high (90-91%).

Why is the stock cheap?

Seems like a wonderful company, right?

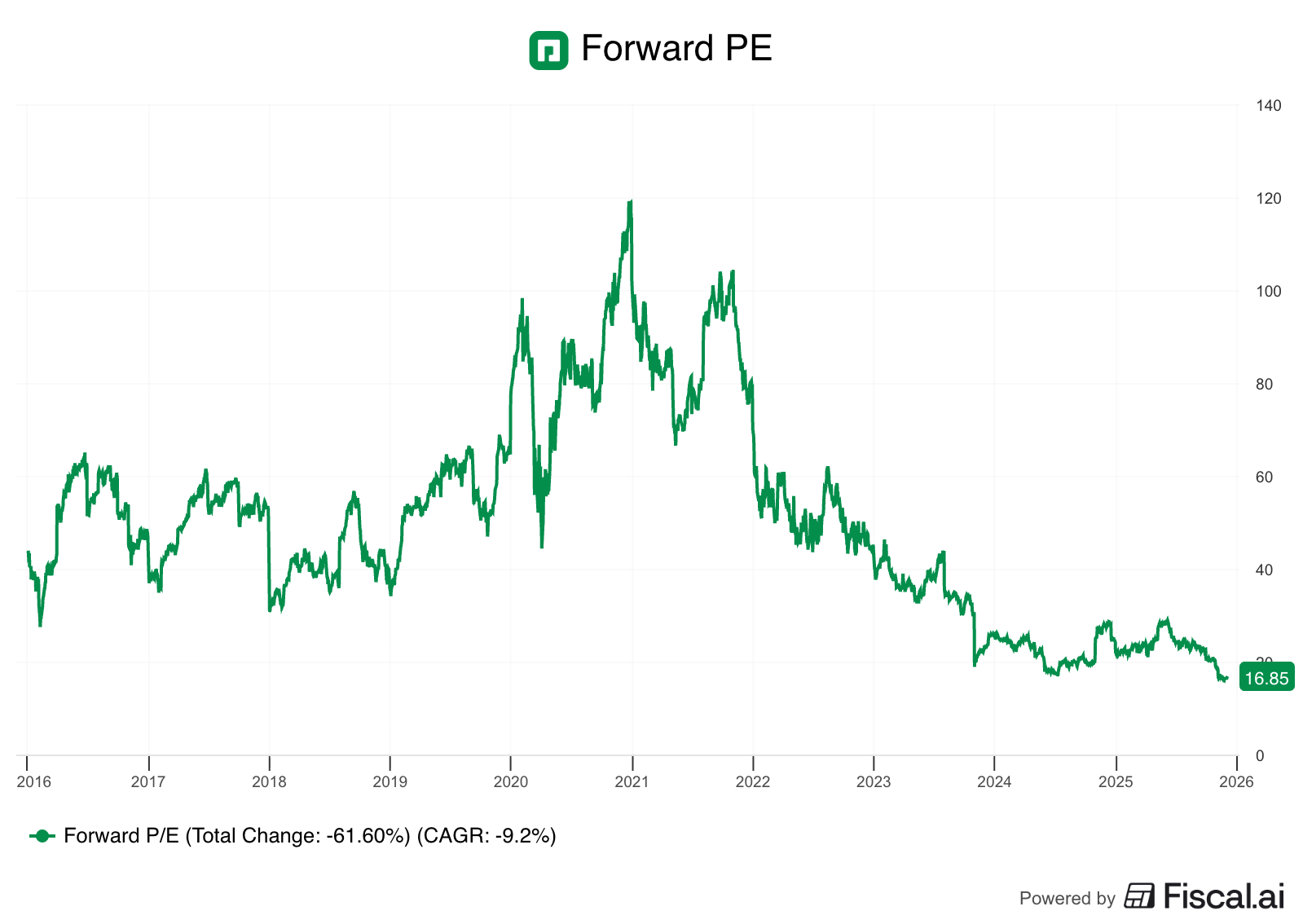

Now, let’s take a look at the price chart. Since 2021, the stock declined over 60%.

The reason?

Paycom was historically valued as a high-growth Software-as-a-Service (SaaS) company.

This resulted in a high valuation multiple. Investors expected very strong growth.

Revenue growth has slowed from 30% to 10% over the past few years.

Part of this decline is actually positive…

… Beti made payroll so efficient that it replaced some of Paycom’s own products.

This results in lower transaction-based revenue but more recurring revenue.

As a result, the P/E ratio for Paycom declined substantially.

I think the market might be overreacting here.

In just 2 months, Paycom repurchased 3% of its outstanding shares (management thinks the stock is undervalued)

Terry Smith (Fundsmith) heavily bought Paycom in the last quarter

Fundamentals

Here’s what the fundamentals look like:

Debt/Equity: 0x (Debt/Equity < 1x? ✅)

ROCE: 35.1% (ROCE > 15%? ✅)

5-Yr Revenue CAGR: 19.7% (5-Yr Revenue CAGR > 7%? ✅)

FCF-Margin: 18.1% (FCF-Margin > 10%? ✅)

P/FCF: 36.7x (P/FCF < 20x? ❌)

Paycom has been investing a lot in data centers to prepare for AI integration.

These investments have now been made.

If we remove the $100 million they spent on data centers from the 2024 CAPEX, Paycom is trading at a P/FCF of around 21x.

That looks much more reasonable if you ask me.

Best Buys December 2025

Now, let’s dive into our five favorite stocks for December 2025.

We only talk about companies that aren’t in Our Portfolio today. Why? We love all companies we own.

Partners have 24/7 access to the Portfolio here.

The 5 examples we talk about in this article can be considered as serious candidates for the Portfolio.

5. Adobe ($ADBE)

How does Adobe make money?

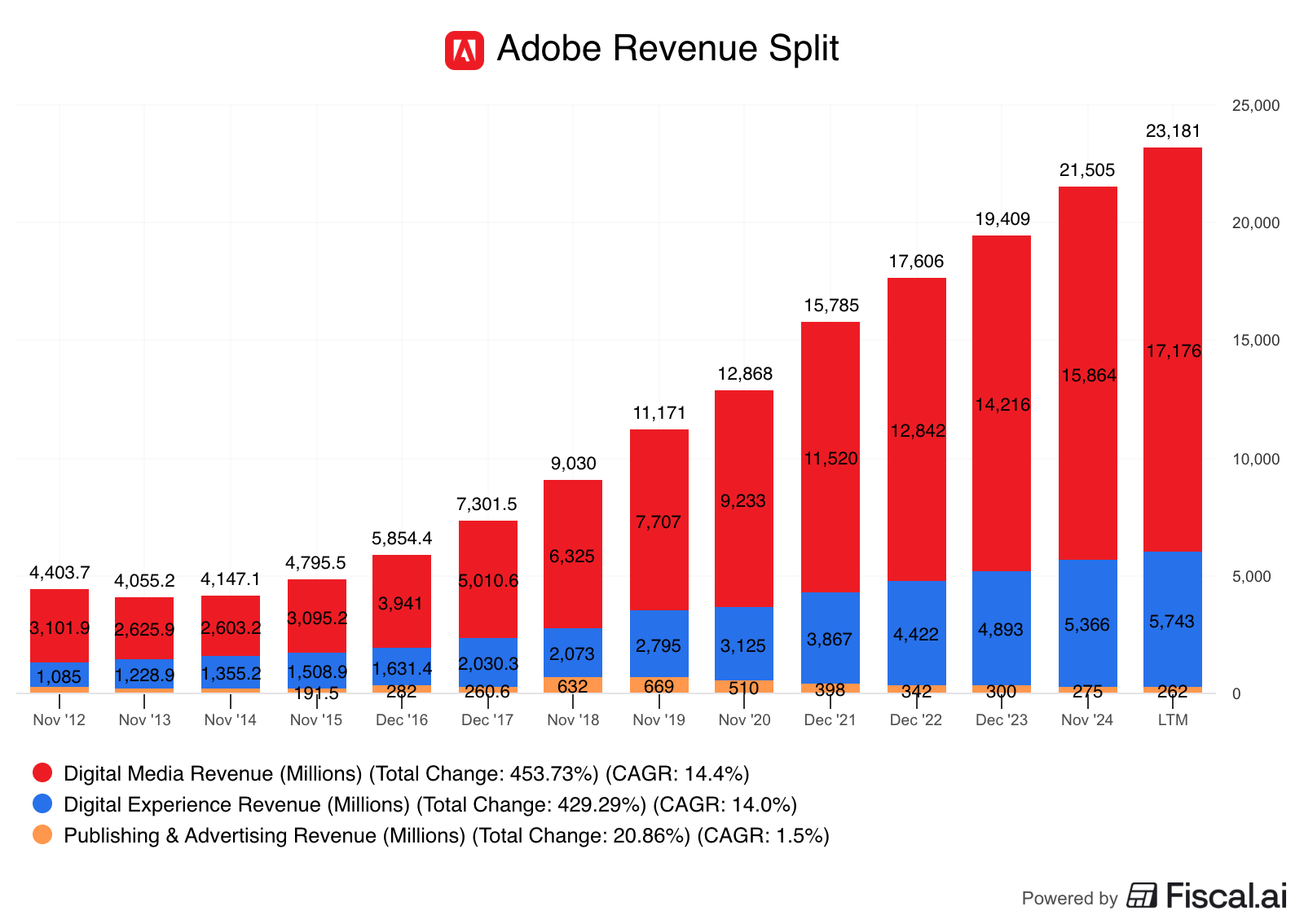

Adobe earns the vast majority of its revenue from subscriptions to its industry-standard creative, document, and experience software platforms. This high-quality recurring revenue model gives Adobe highly predictable cash flows and gross margins consistently above 85%.Adobe’s revenue is primarily divided into three parts:

Digital Media

Digital Experience

Publishing & Advertising

1. Digital Media (74.1% of Revenue)

This is Adobe’s flagship segment.

It is primarily made up of subscription revenue from 2 categories:

Creative Cloud (CC):

Tools for creative professionals, like Photoshop, Illustrator, Premiere Pro, and InDesign, as well as new Generative AI features like Firefly.

Document Cloud (DC):

Tools like Adobe Acrobat and Adobe Sign that enable the creation, editing, security, and digital signing of PDFs and other documents.

2. Digital Experience (24.8% of Revenue)

This fast-growing segment sells large businesses software for managing customer experiences, marketing, and online commerce.

3. Publishing & Advertising (1.1% of Revenue)

This segment is the smallest, containing legacy print, publishing, and some advertising tools.

Its impact on total revenue is negligible.

Management

Shantanu Narayen has been the CEO since 2007.

He has led Adobe’s successful transition from selling boxed software (licenses) to a recurring subscription model (SaaS) in the early 2010s.

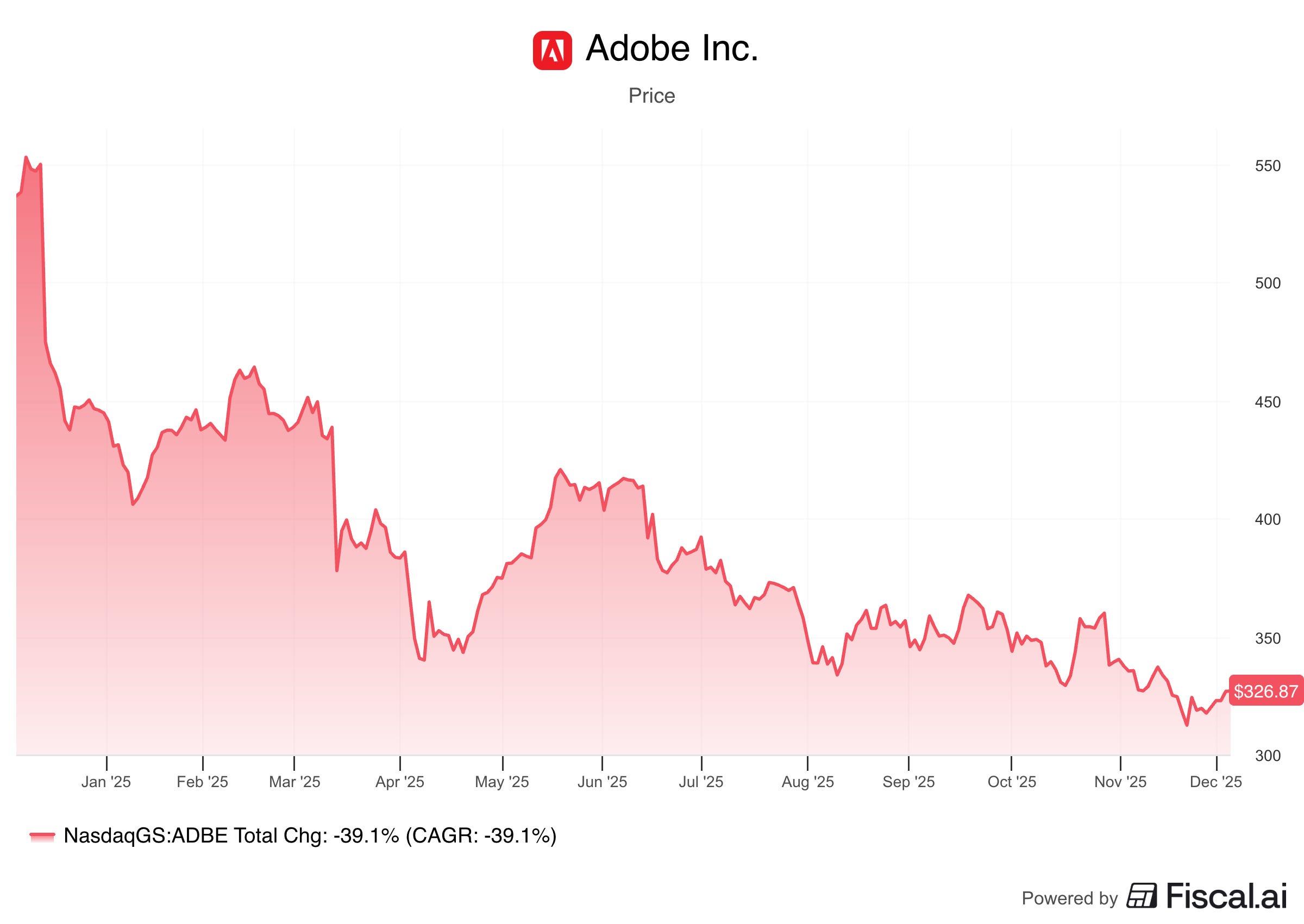

Adobe is a great company with a great history. However…

… Its stock is down more than 35% over the past year.

Investors are scared of new AI competitors.

This fear may underestimate Adobe’s massive competitive strengths:

Switching Costs: Designers and companies are locked in because their entire workflow is built around Adobe’s complex tools (Photoshop, Premiere)

Industry Standard: Adobe created the PDF and the standard file formats for creative work which means that to collaborate, everyone needs to use Adobe products

Adding AI: Adobe is adding its powerful AI, Firefly, right into its existing tools, meaning customers won’t need to switch programs, and Adobe can stay the main software for creative work

To conclude, Adobe is a highly profitable, high ROIC business, surrounded by a lot of fear.

This could be an interesting opportunity for investors who think the fear is overblown and that Adobe’s business foundations will remain strong and durable.

Management thinks the company is too cheap as they are heavily buying back shares.

4. Copart ($CPRT)

How does Copart make money?

Copart makes money by operating a massive global platform for online vehicle auctions, primarily for salvage and total-loss vehicles. It acts as an intermediary, connecting sellers (mainly insurance companies) with a global pool of buyers (dealers, dismantlers, rebuilders).Copart makes money in two ways:

Seller Fees: Charged to insurance companies for storing, marketing, and selling the salvaged vehicle

Buyer Fees: Charged to the winning bidder for the transaction

The secret of their business model is simple: they provide the system that helps the insurance world handle damaged cars and other salvage.

Copart manages the entire value chain:

Towing and Storage: Retrieving the damaged vehicle and storing it in one of their 250 global junkyards.

Digital Listing: Creating a listing with photos and vehicle details on their proprietary online auction platform.

Auction and Sale: Facilitating the live, online auction process to sell the vehicle to the highest bidder globally.

This gives Copart a strong two-sided network effect.

Remember that network effects are one of the strongest moats a company can have.

As they have many yards and lots of insurance partners more buyers join the platform

More buyers attract more sellers

More sellers attract even more buyers

It becomes a loop that keeps growing

![What is a two-sided marketplace? [Definition + examples] | Zapier](https://substackcdn.com/image/fetch/$s_!10Tg!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F25ec583d-f3cc-4991-ad05-4d2dc838e093_1400x788.png "What is a two-sided marketplace? [Definition + examples] | Zapier")

In addition to being a strong business, Copart has strong leadership.

The company was founded in 1982 by Willis Johnson, who was later joined by current CEO Jayson Adair.

When Johnson bought his first junkyard, he used all his savings and even lost his house, ending up living in a trailer between the wrecked cars.

Johnson and Adair are known as disciplined and obsessed operators.

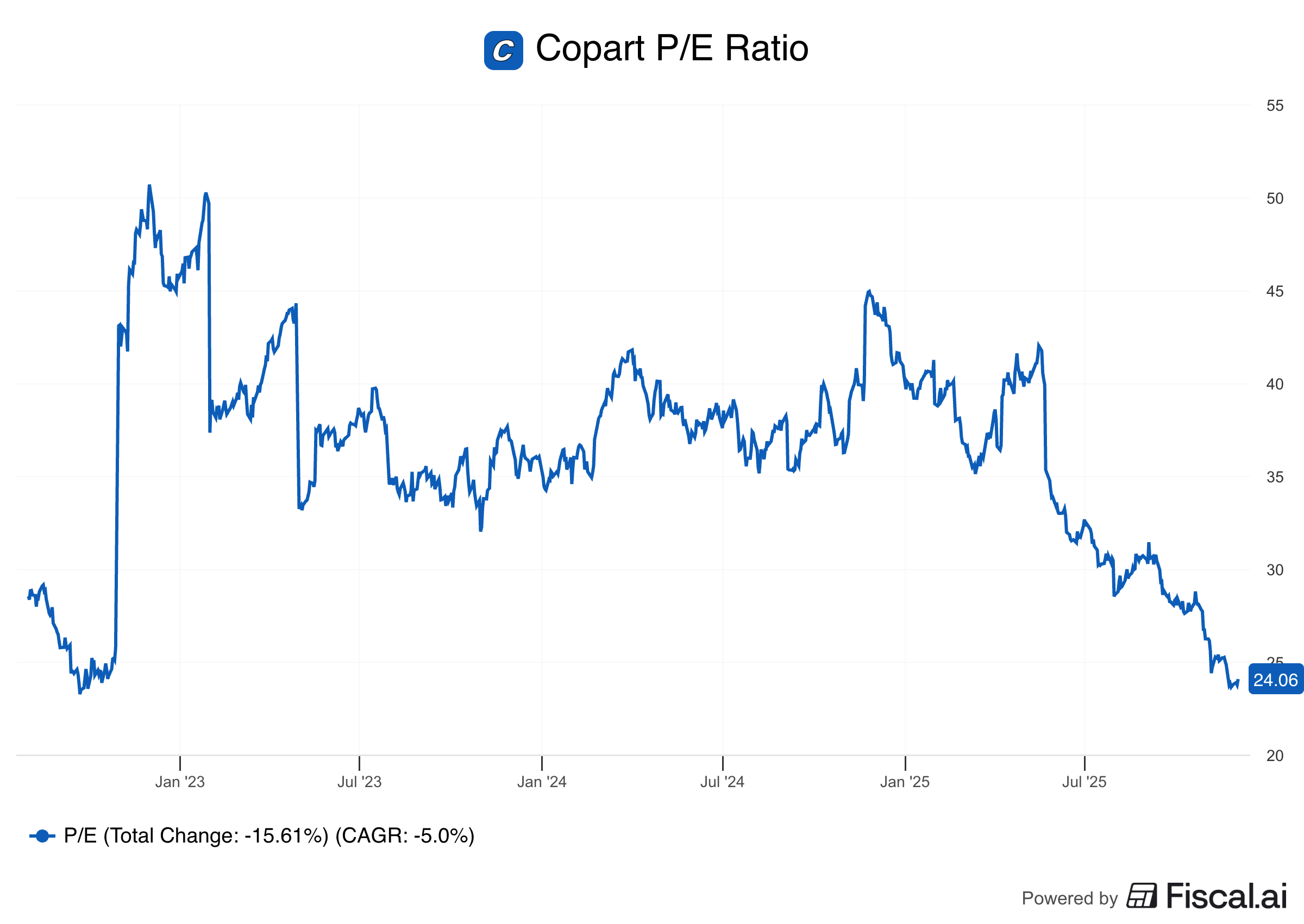

Copart is a an amazing business, but it looked expensive for a long time.

It’s finally starting to come down to more reasonable valuation levels.

As a result, we get interested as long-term quality investors:

Now let’s dive into the top 3.