Best Buys: June 2026

By monthly tradition, you’ll get an update on our Best Buys of the month.

What’s going on in the markets? And what are our favorite stocks?

Let’s get a little bit wiser today.

![100+] June Aesthetic Wallpapers | Wallpapers.com](https://substackcdn.com/image/fetch/$s_!Xy_c!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F21a496e1-10eb-4ccf-bfb8-f3e69a35af2a_1920x1080.jpeg "100+] June Aesthetic Wallpapers | Wallpapers.com")

May 2026

The S&P 500 rose +5.0% in May.

However, the start of June was more rough: -2.4%.

To give an example, the Nasdaq was down 4.4% this week while some ‘boring quality stocks’ did really well:

Brown & Brown: +4.8%

Ameriprise Financial: +2.2%

Medpace: +2.2%

I expect more and more moves like this to happen going forward.

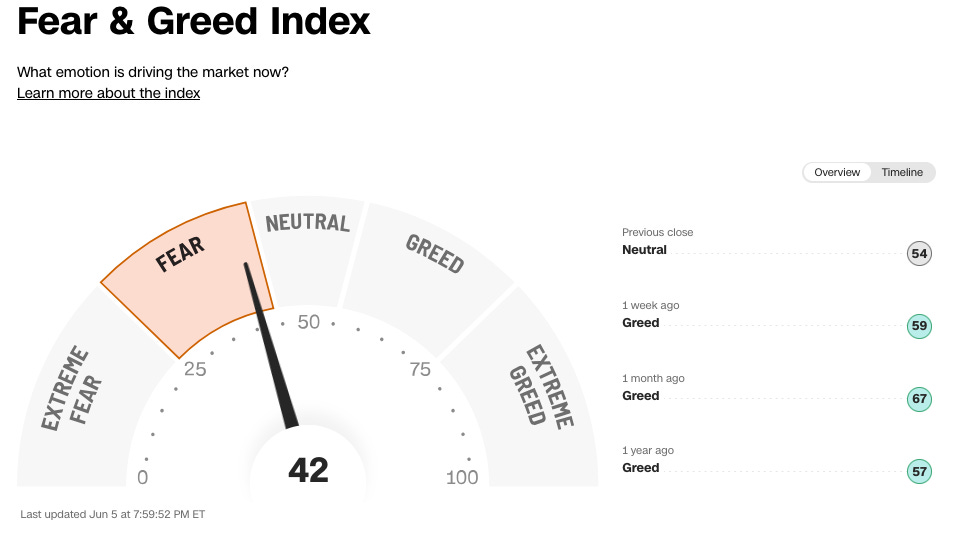

Investors are ‘Fearful’ today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

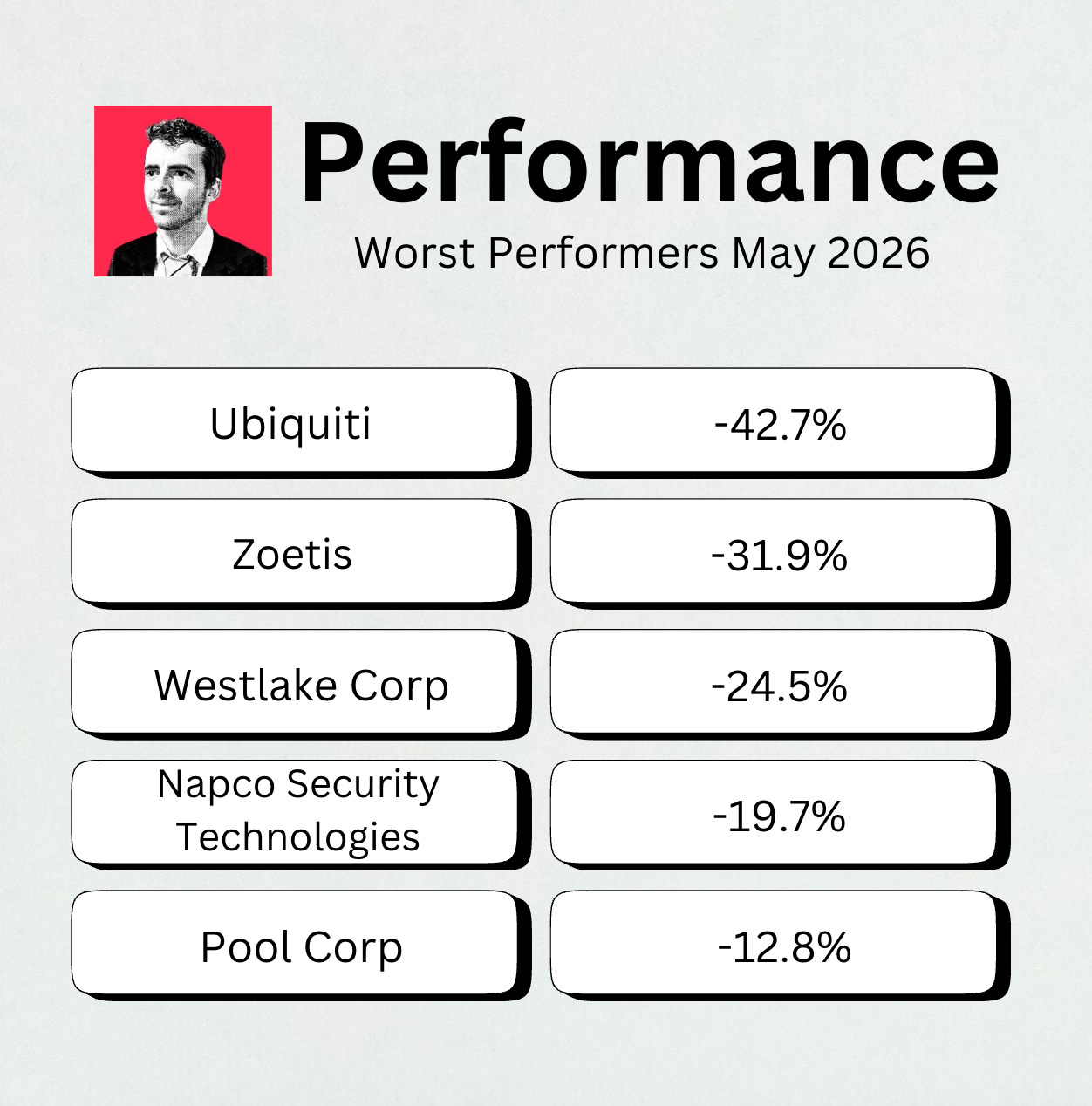

Worst performers

The cheaper we can buy great companies, the better.

Here are the worst performers of the past month:

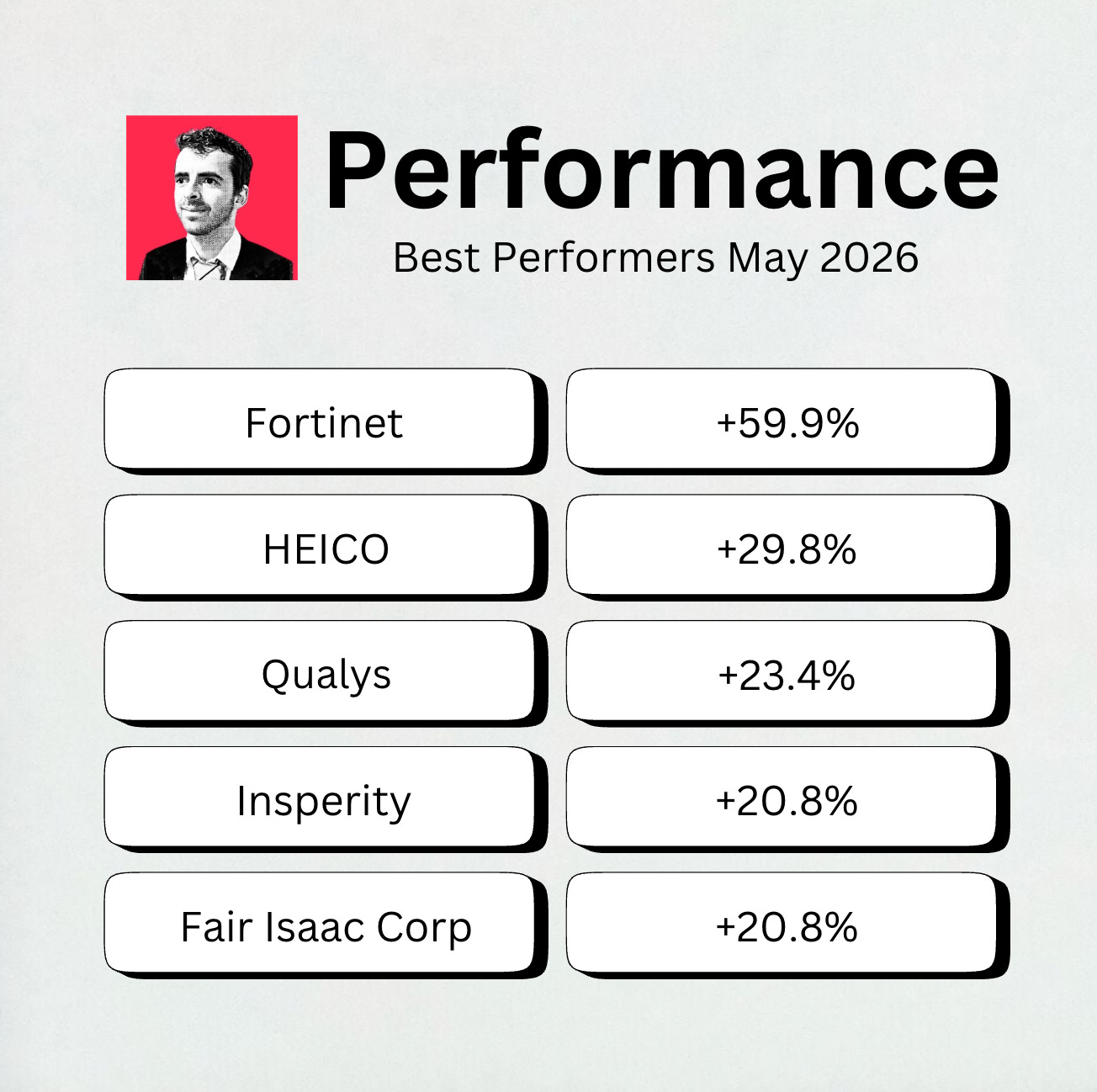

Best performers

These stocks did well over the past month:

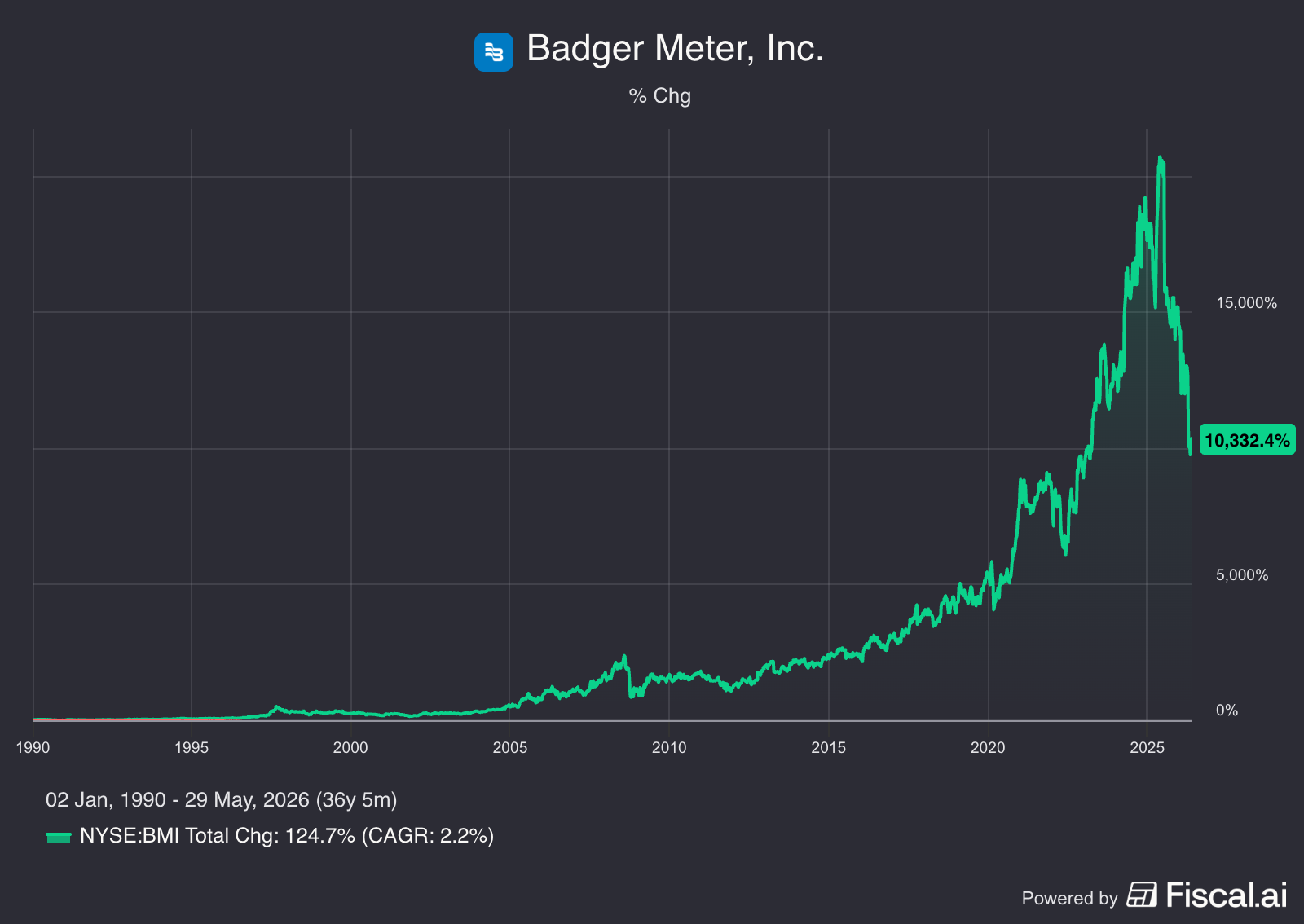

💧 Spotlight: Badger Meter, Inc. ($BMI)

How Does The Company Make Money?

Badger Meter provides the technology to measure and control whatever moves through a pipe.

They’ve managed to transform from a simple mechanical meter manufacturer into a high-tech water management solutions provider.

As a result, they are now a clear market leader:

Over 90% revenue share in the U.S. market

The market leader in smart water systems for cities

One complete system: their own smart meters plus their ORION and BEACON software, all working together

Why does it deserve to be in the spotlight?

We can’t talk about Badger Meter without talking about its durability.

The business is 120 (!) years old.

Since its IPO in 1971, the stock has compounded at 12.2% every year.

Its dominant market position comes from 3 things:

Vertical Integration: They make their own meters, sensors, and software. Because they control every piece, they can fix problems fast and bring out new ideas quicker.

High Switching Costs: Water companies sign long contracts. Once Badger Meter’s systems are installed, switching to someone else costs a lot of money and is a huge hassle.

Recurring Revenue Mix: Money keeps coming in every year. They earn steady, easy-to-predict cash from software subscriptions, monitoring services, and water-company relationships that last for decades.

The track record of Badger Meter’s capital allocation is phenomenal:

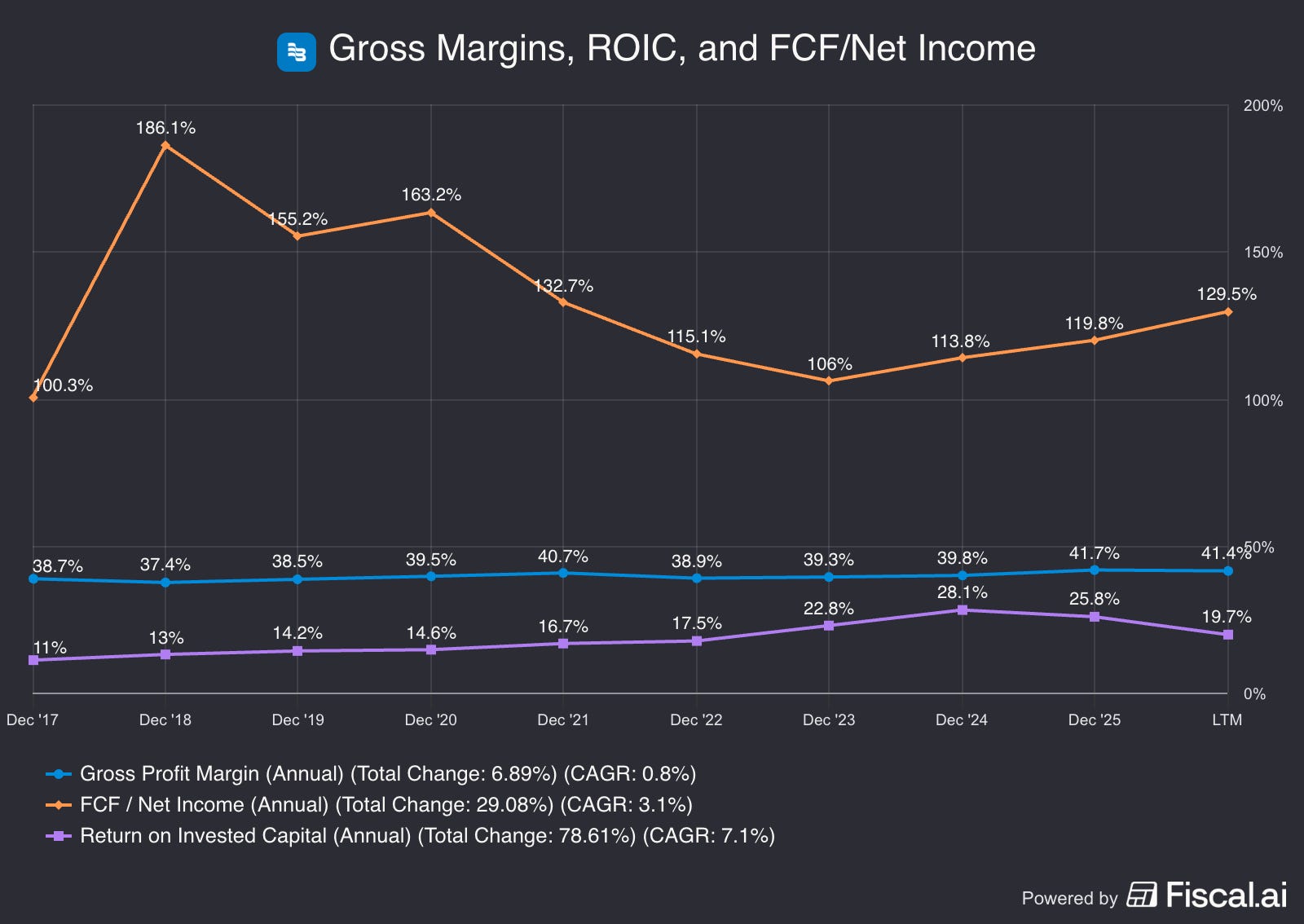

Gross Margin: 41.4% (> 40%? ✅)

ROIC: 25.8% (> 15%? ✅)

Free Cash Flow Conversion: Consistently over 125% of Net Income in the past 5 years (> 80%? ✅)

The global smart water market is set to hit $37.4 billion by 2031, growing more than 12% per year.

A large acquisition

Badger Meter bought SmartCover Systems in 2025.

This was their biggest acquisition ever.

It significantly grew its software segment.

SmartCover sells hardware plus software.

It lets you watch wastewater and stormwater systems in real time.

Why this deal matters:

Expanded Moat: It pushes Badger Meter deeper into the high-growth wastewater monitoring segment.

Recurring Revenue: It heavily expands their higher-margin software and recurring revenue base.

Market Leadership: It cements them as the go-to smart water platform for municipalities.

They’re continuing to add to this portfolio with the recent acquisition of UDlive in the UK.

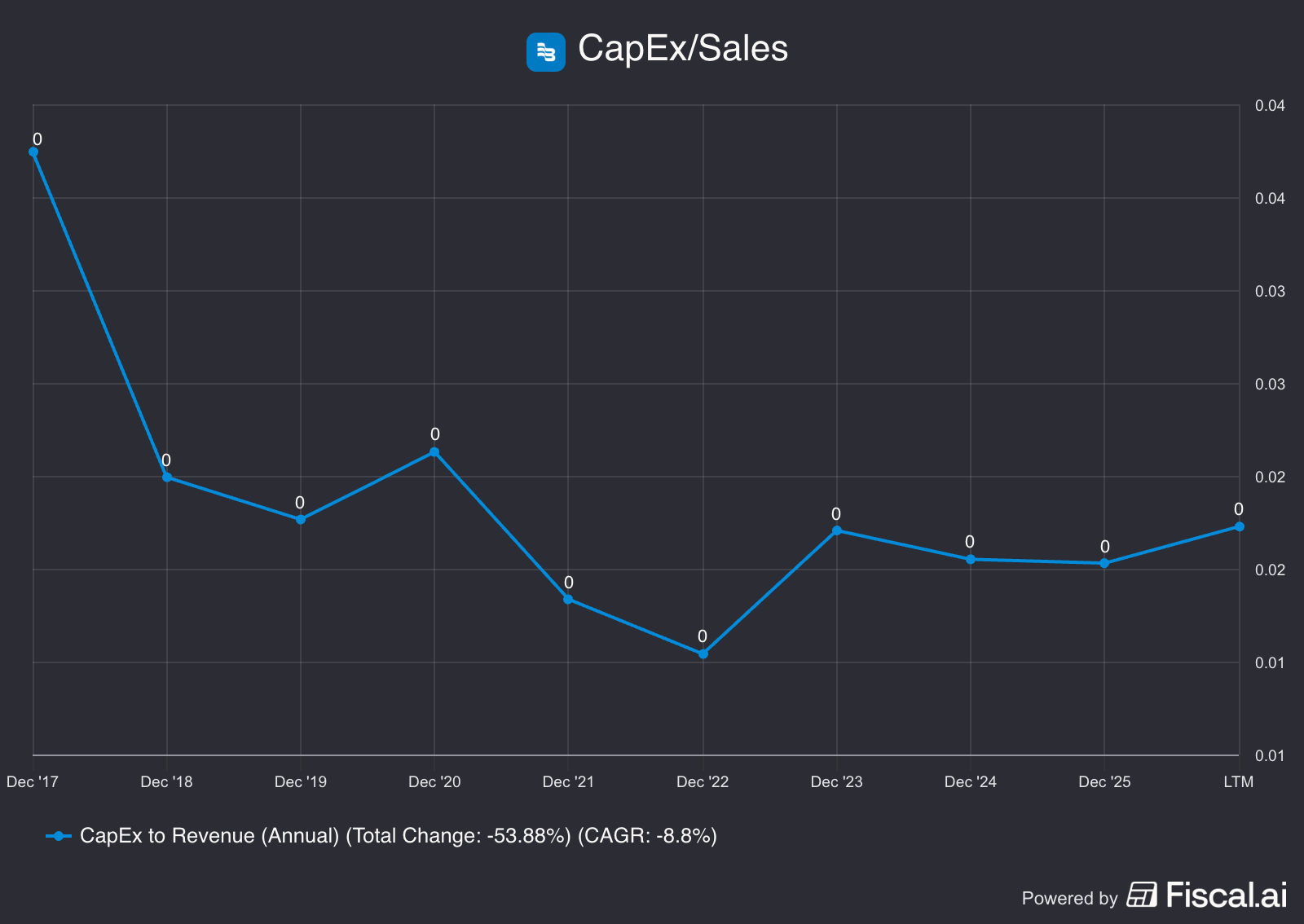

You might think that a company that manufactures meters for utility companies would be a capital intensive business.

But that’s not the case for Badger Meter.

They carry no debt and their CAPEX is consistently below 2% of sales.

They don’t need much money to run the business.

This means they can pour their huge free cash flows into deals like SmartCover and keep growing.

We love businesses that:

Sell must-have products

Are hard to walk away from

And have strong management at the top.

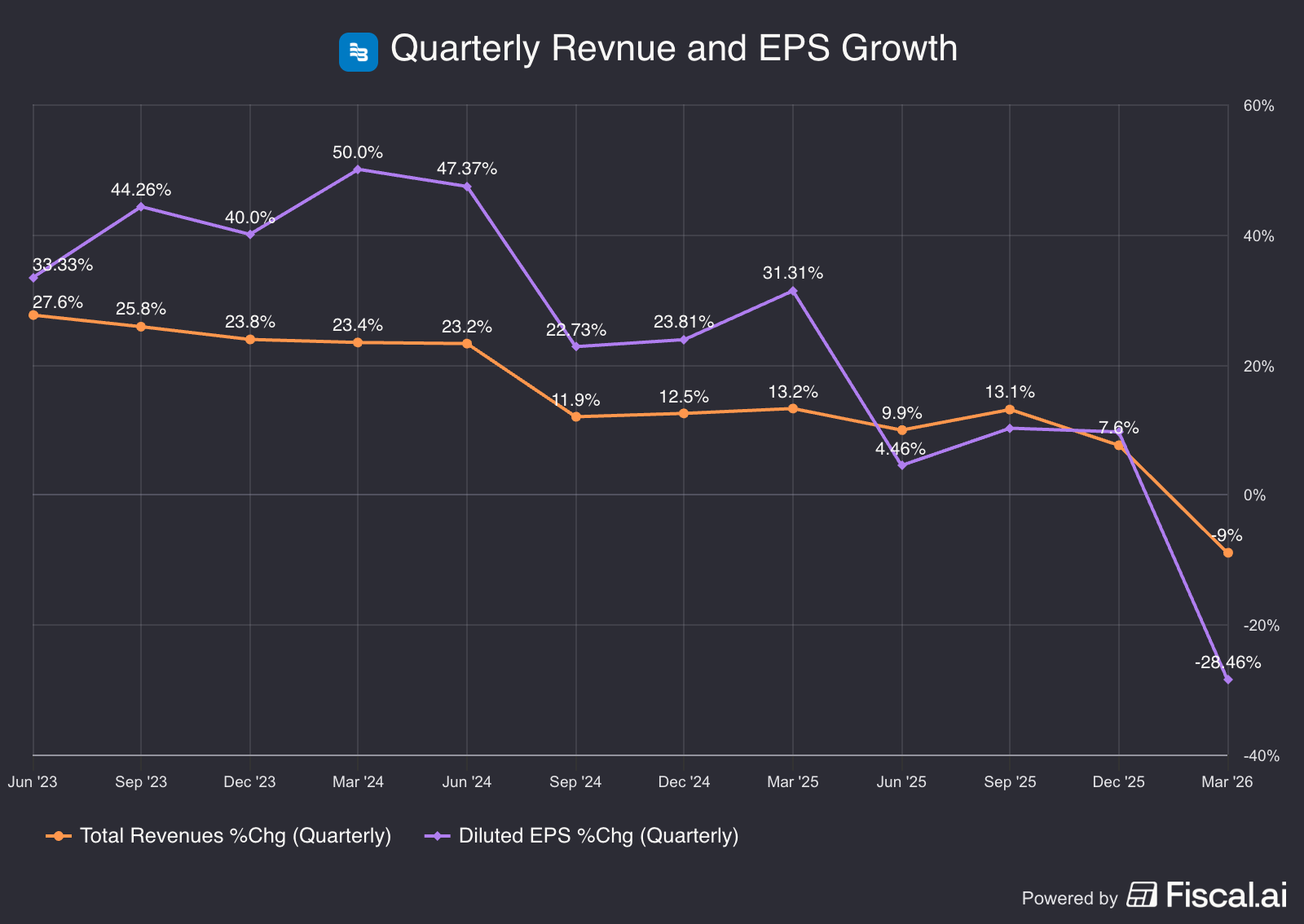

But Badger Meter is going through some macro troubles lately.

They saw revenue and EPS drop in the most recent quarter:

Management blamed it mostly on two things:

Customers working through extra stock they'd built up

Cities holding off on spending for a while.

If these issues are temporary, Badger Meter could be an interesting stock for long-term investors.

Best Buys June 2026

Let’s dive into our five favorite buys for the month.

Please note that the companies in Our Portfolio are not mentioned here.

We love all companies in Our Portfolio right now.

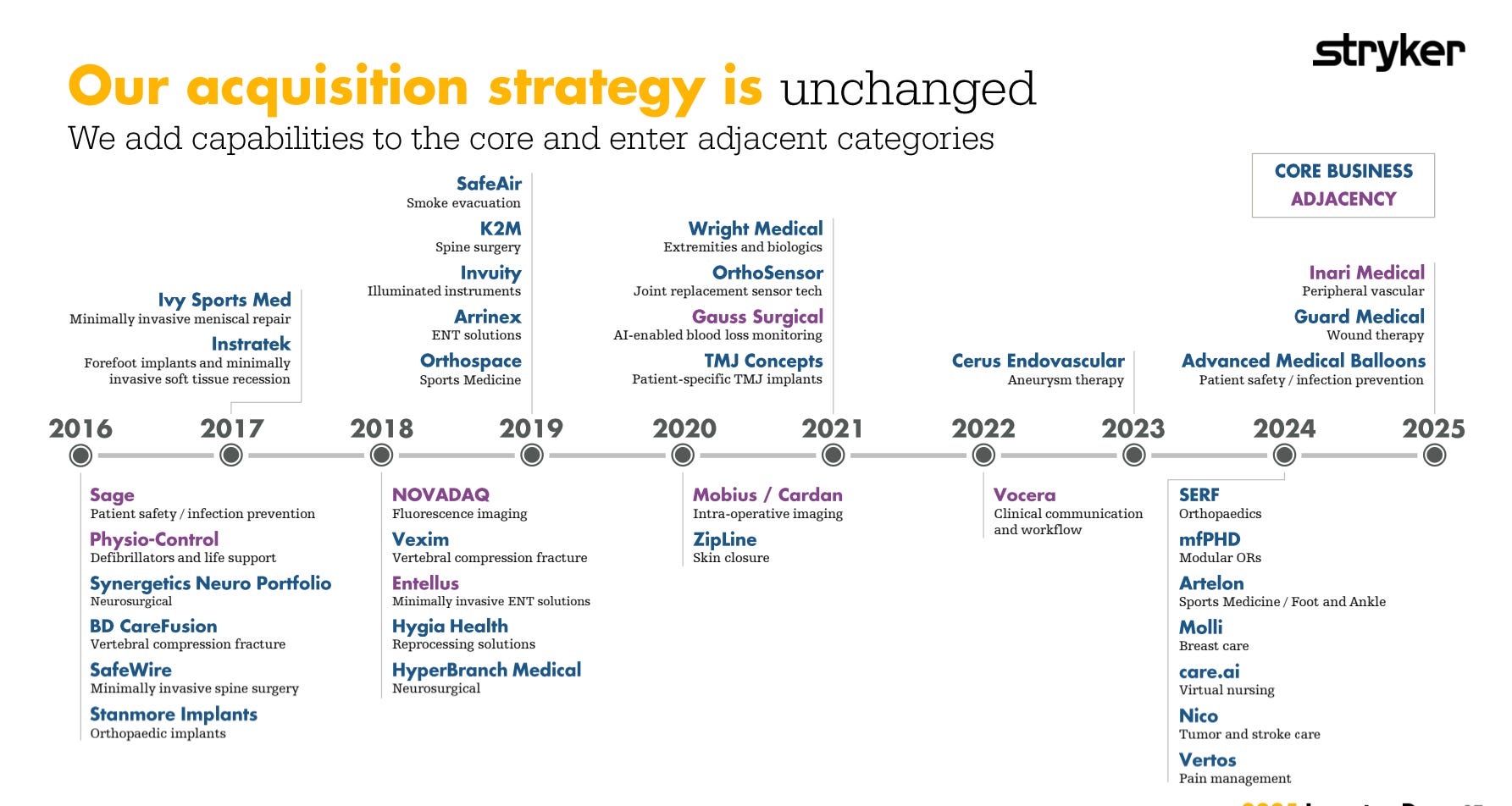

5. Stryker ($SYK)

How does the company make money?

Stryker manufacturers and sells surgical equipment, neurovascular products, and orthopedic implants (like artificial hips and knees) to hospitals worldwide.

Why Stryker is a Best Buy?

The aging global population provides a massive tailwind for Stryker:

Its Mako Robotic-Arm Assisted Surgery system is another really interesting part of the business.:

It operates on a brilliant razor-and-blade model:

High Switching Costs: Once a hospital invests over a million dollars in a Mako robot and trains its surgeons to use it, they rarely switch to a competitor.

Recurring Cash Flow: Stryker doesn’t just make money selling the robot, they make recurring revenue on the software, service contracts, and the specialized consumables required for every single surgery.

Stryker is a proven compounding machine that grows both organically and through acquisitions.

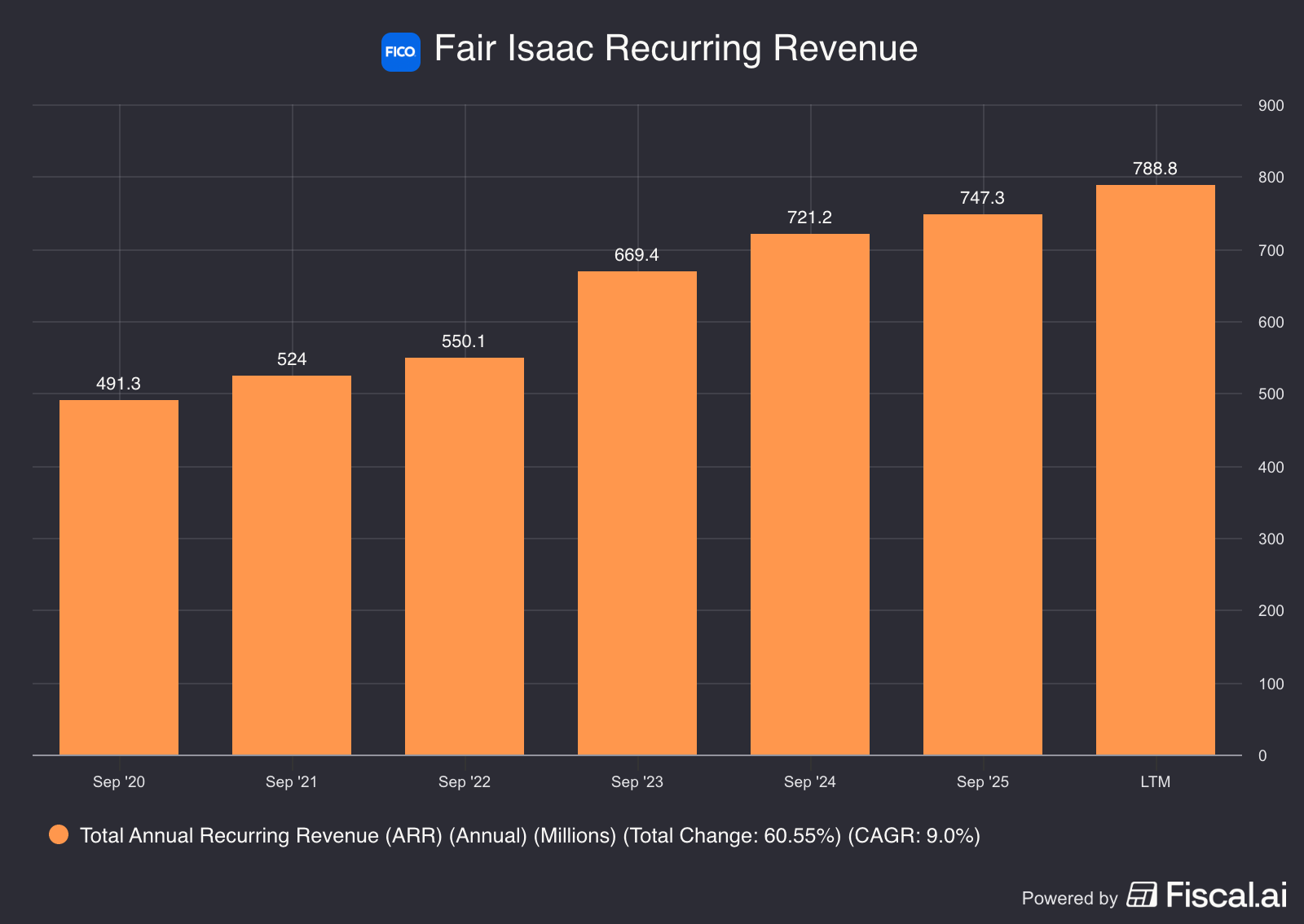

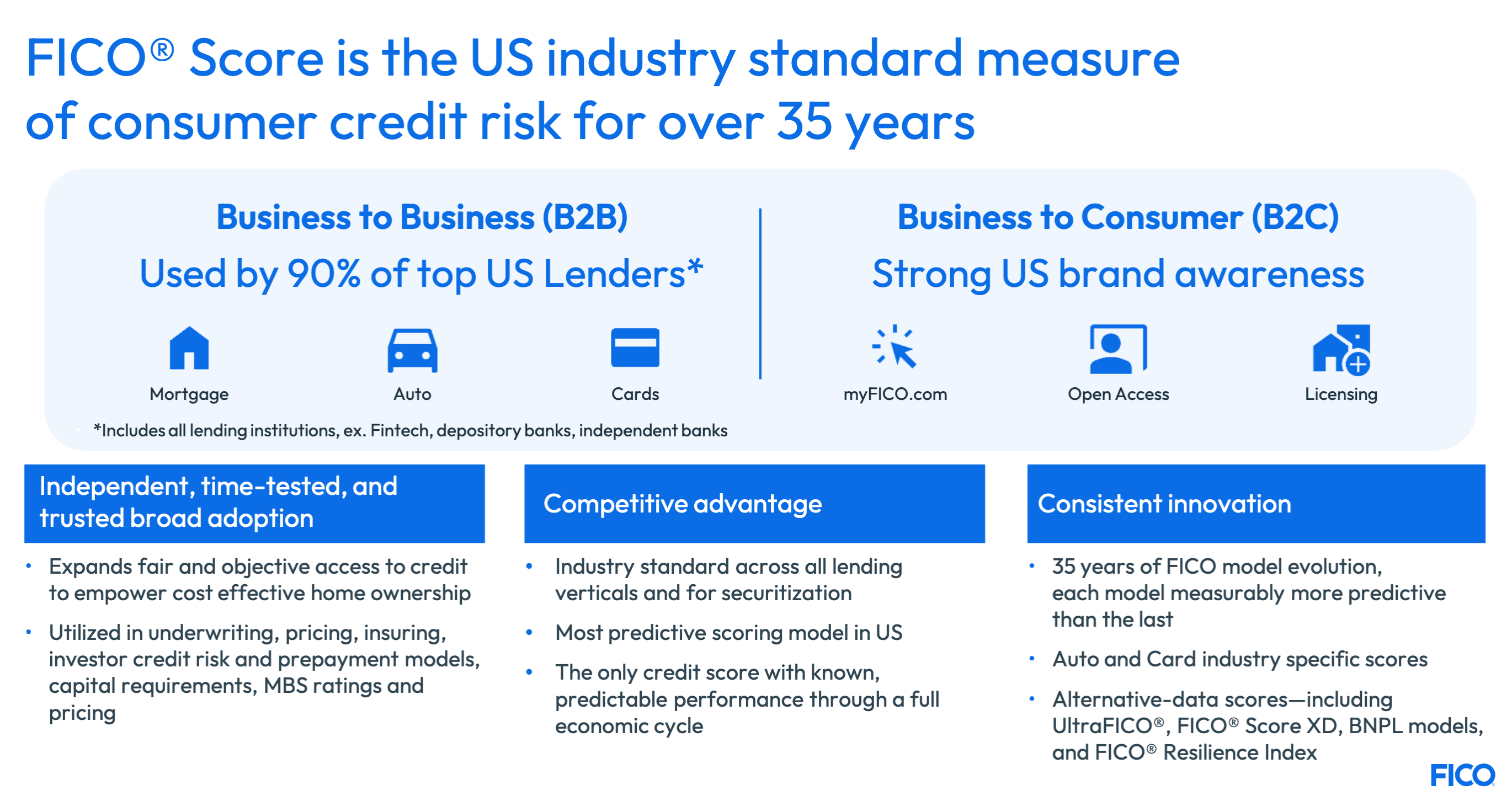

4. Fair Isaac Corporation ($FICO)

How does FICO make money?

FICO is most famous for licensing its proprietary credit scoring algorithm to major credit bureaus (Equifax, Experian, and TransUnion).

They also have a B2B software segment that helps global banks make complex lending and fraud decisions.

Why FICO is a Best Buy?

Fair Isaac is down more than 30% this year.

Why?

A U.S. government housing agency (the FHFA) is now allowing a rival product, VantageScore 4.0, to be used for approving mortgages.

The market is very fearful that this will have a big impact on FICO’s business.

I don’t think that will be the case.

More data is always better: Even if lenders start using VantageScore, they’ll still check the FICO score too to make sure they get it right.

Switching Costs: Bank rules and their own risk systems are built around FICO scores. Changing that means years of rebuilding everything from the ground up

Recurring Revenue: The B2B software platform generates recurring revenue with high retention rates.

FICO scores are still the absolute standard when it comes to measuring consumer credit risk.

The current drawdown in stock price is a chance to buy FICO near the lowest valuation we’ve seen in the past decade.

Now let’s dive in the top 3.