By monthly tradition, you’ll get an update on our Best Buys of the month.

What’s going on in the markets? And what are our favorite stocks?

Let’s get a little bit wiser today.

February 2026

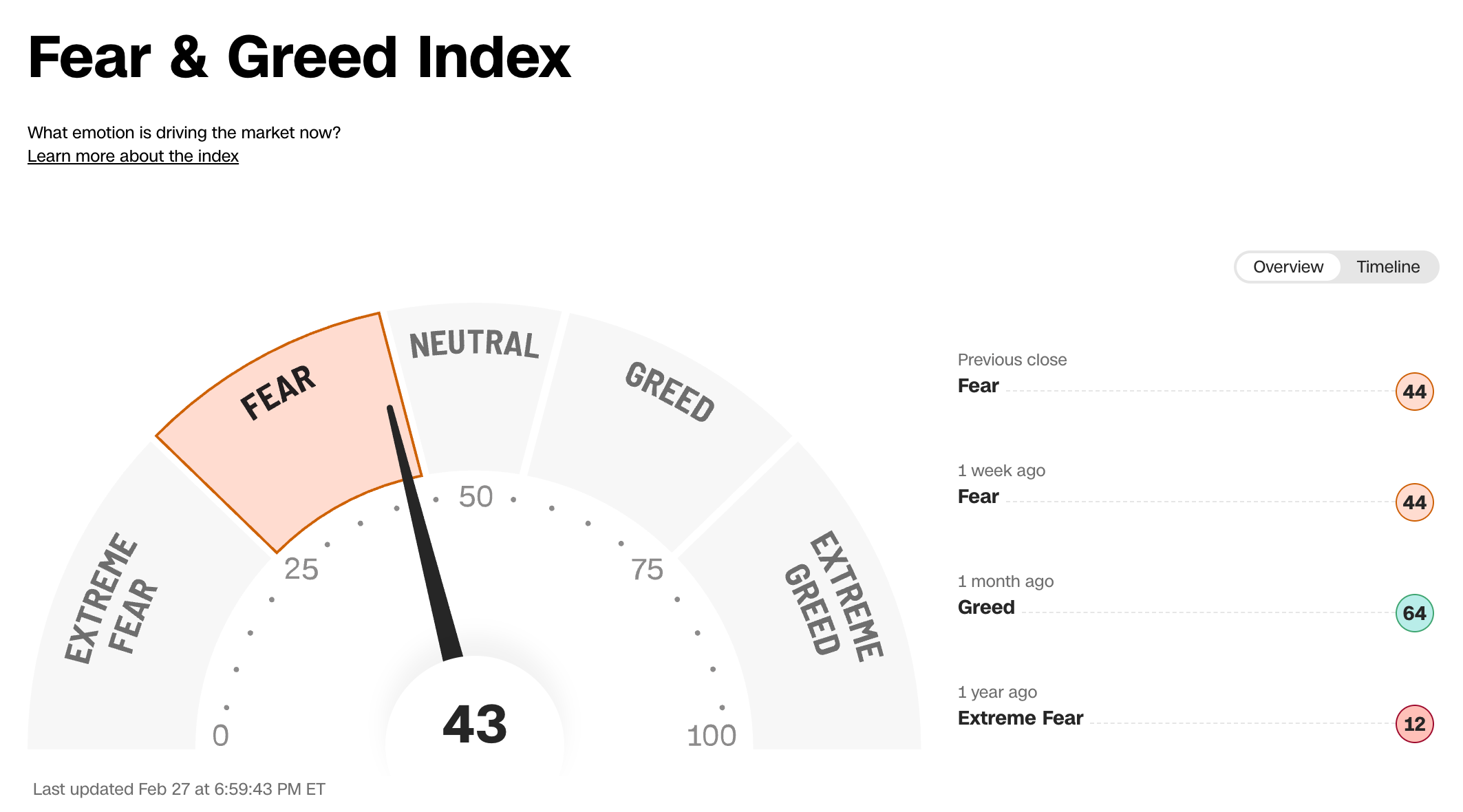

The S&P 500 declined by -1.4% in February

Investors are Fearful today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

Worst performers

The cheaper we can buy great companies, the better.

Here are the worst performers of the past month:

A company like KKR starts to become more and more interesting if you ask me.

Best performers

These stocks did well over the past month:

Spotlight: Fair Isaac Corporation ($FICO)

How does the company make money?

FICO licenses its proprietary scoring algorithm to major credit bureaus (Equifax, Experian, and TransUnion).

The company provides software to banks that helps them make and automate decisions.

Why does it deserve to be in the spotlight?

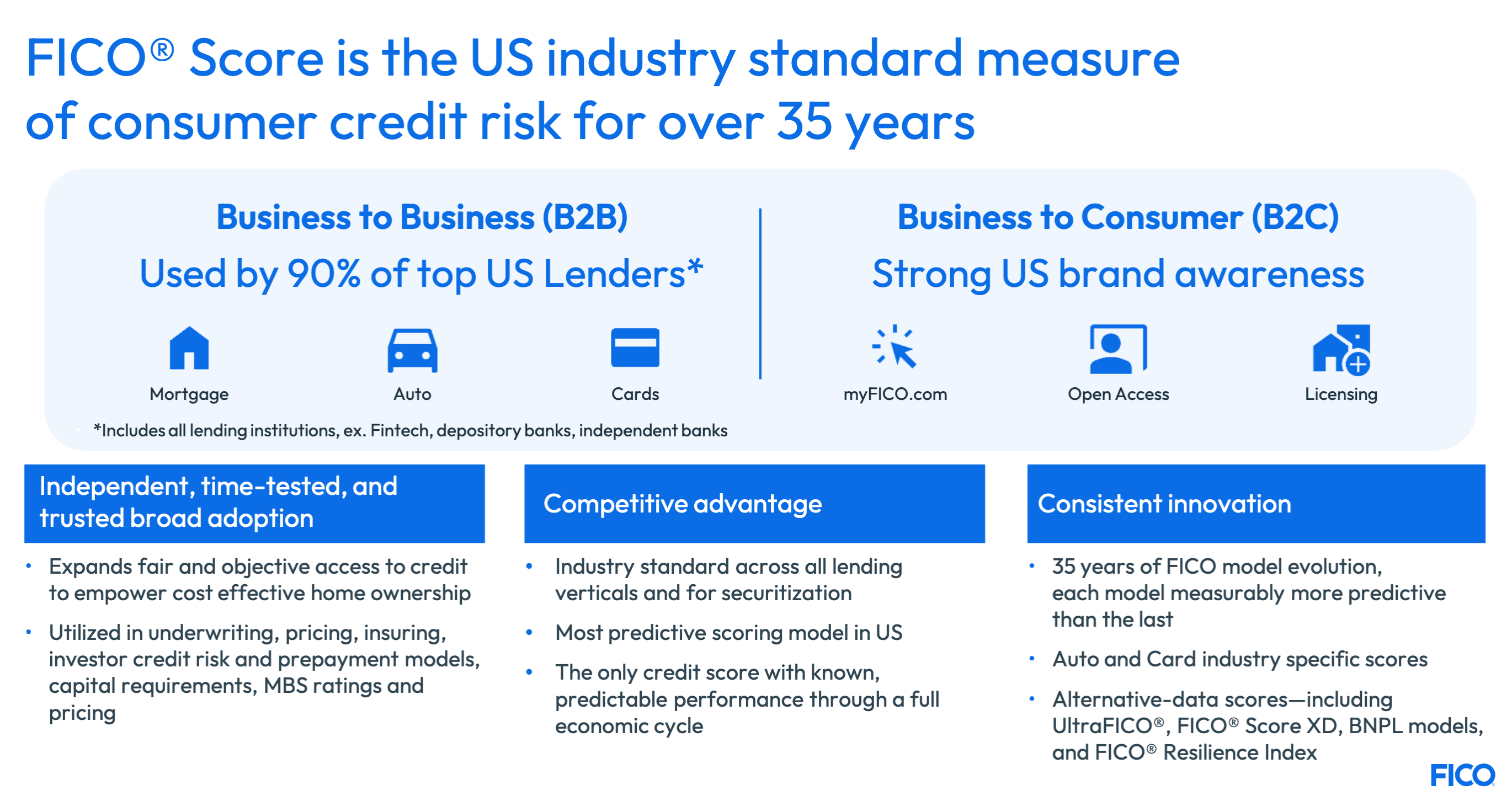

FICO is a data and analytics company.

They are a tollbridge on the American credit system.

If you’ve ever checked your credit score, you’ve interacted with FICO.

Fair Isaac licenses its proprietary FICO Score to lenders.

Every time someone applies for a mortgage, credit card, or auto loan… FICO is being paid a small fee.

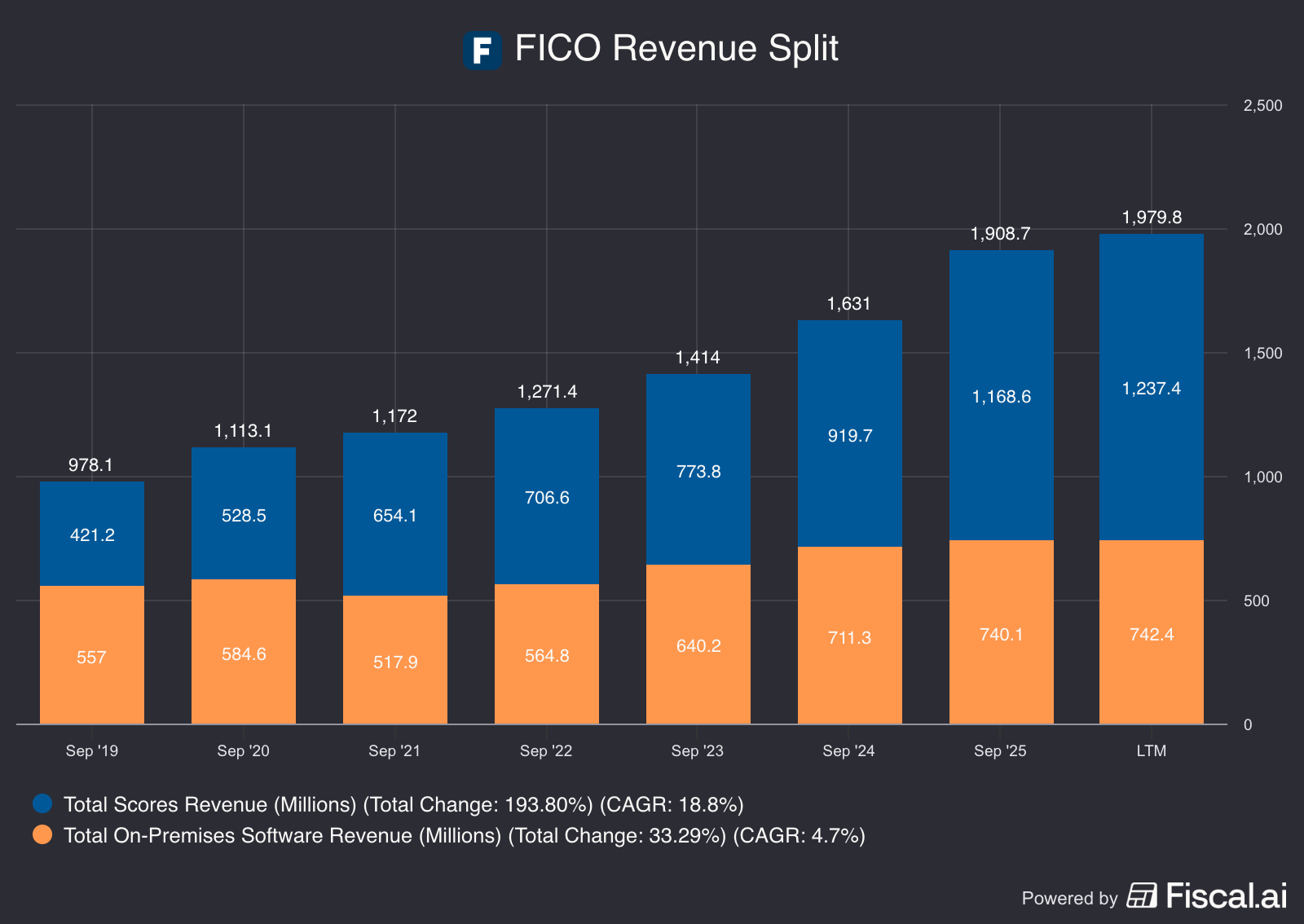

Most of Fair Isaac’s revenue comes from its credit score business:

The other piece of FICO’s business is the decision management software it provides to banks.

This is deeply integrated and critical to their day to day operations.

It helps automate high-volume decisions, like fraud detection and account transitions, giving it very high switching costs.

Fear of AI Disruption

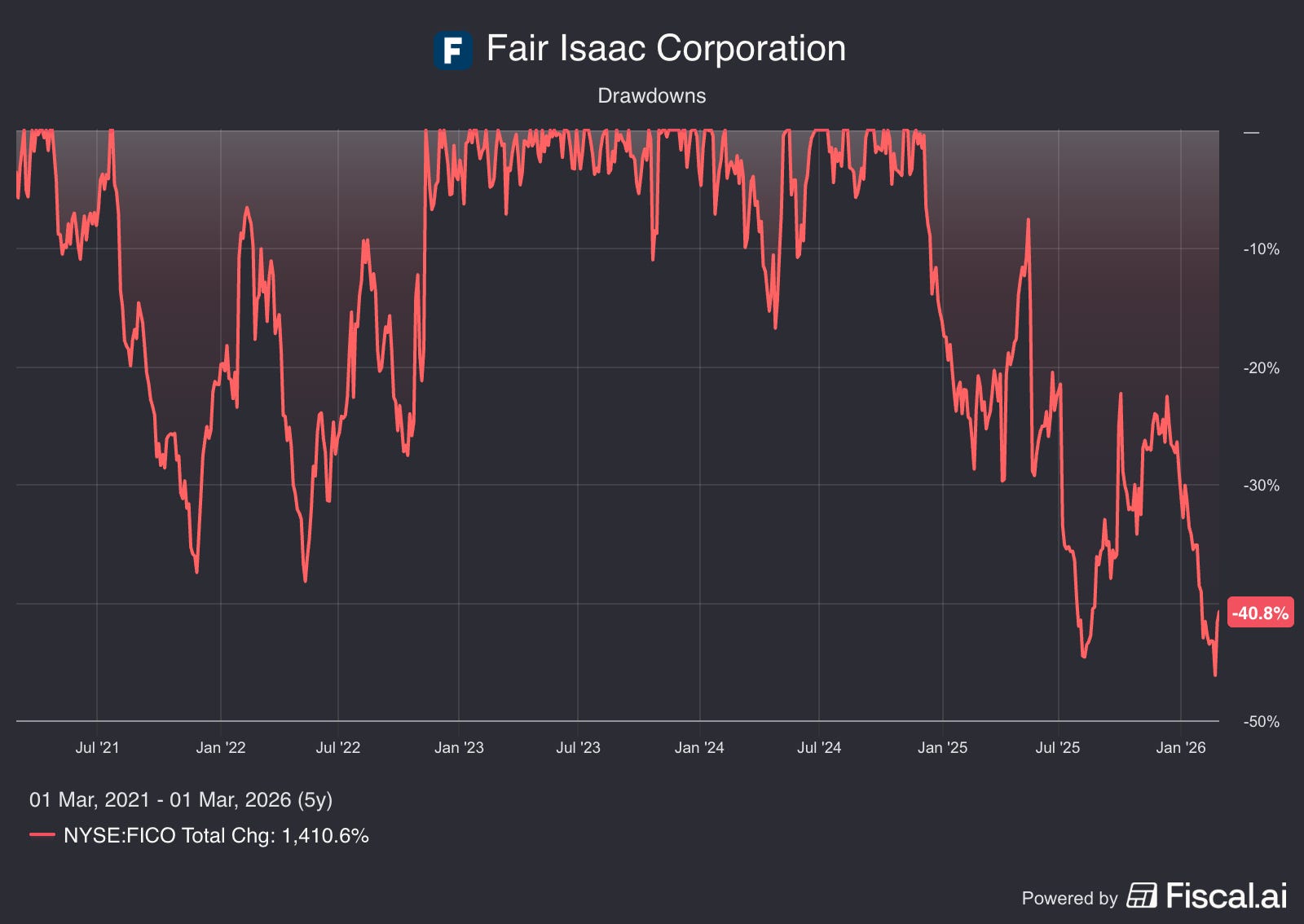

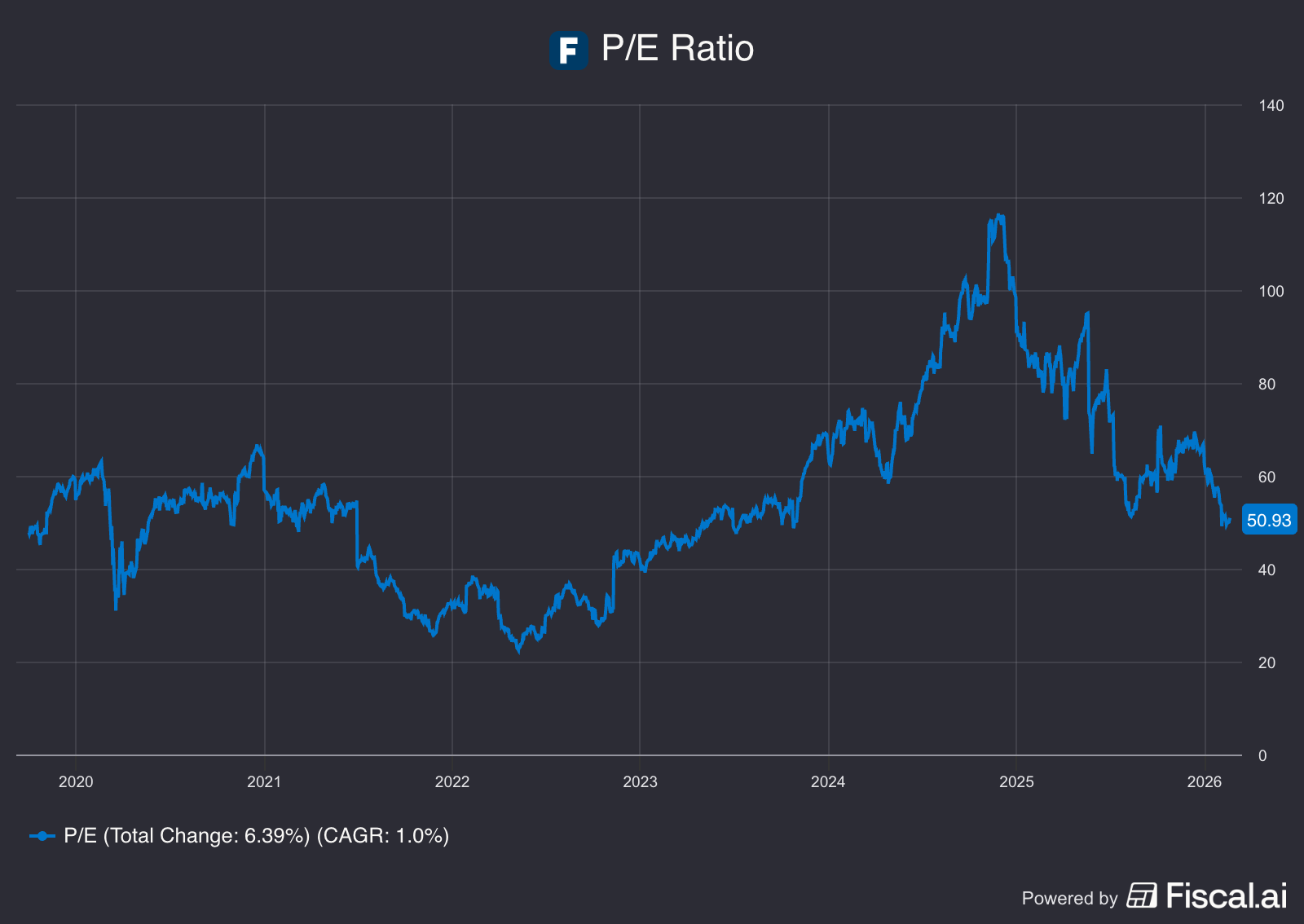

The stock has recently declined from its highs of over $2,200 to around $1,400.

Why?

Investors are panicking…

… They believe Generative AI is about to wipe out traditional credit scoring for good.

In the most pessimistic scenario of the market, lenders will grab AI tools and 'vibe-code' their own credit scores from scratch.

That’s a ridiculous thing if you think about it for a second.

FICO’s Moat

The fear for Artificial Intelligence is short-term noise if you ask me.

FICO’s moat isn’t just it’s credit score algorithm.

It’s the network effect and regulatory integration.

90% of top U.S. lenders use FICO.

The system is hard-coded into the global financial infrastructure.

ROIC remains exceptionally high (often above 50%).

The recent -30% drop in the share price does make it look interesting.

But it’s coming down from very expensive levels, trading at a P/E of >100x in 2024.

Based on the expected EPS of 2028, FICO now trades at a Forward PE of 21.6x.

This is still not very cheap.

Because of this, I think there are more attractively priced Quality businesses elsewhere.

Best Buys March 2026

Only the best of the best is good enough for us.

We focus on companies with:

A wide moat

High ROIC

Consistent Free Cash Flow

Let’s dive into our five favorite buys for the month.

5. Pool Corporation ($POOL)

How does Pool Corporation make money?

Pool Corporation makes money by distributing swimming pool supplies, equipment, and outdoor living products. It is the largest wholesale distributor of pool-related products in the world.

Is it an interesting company?

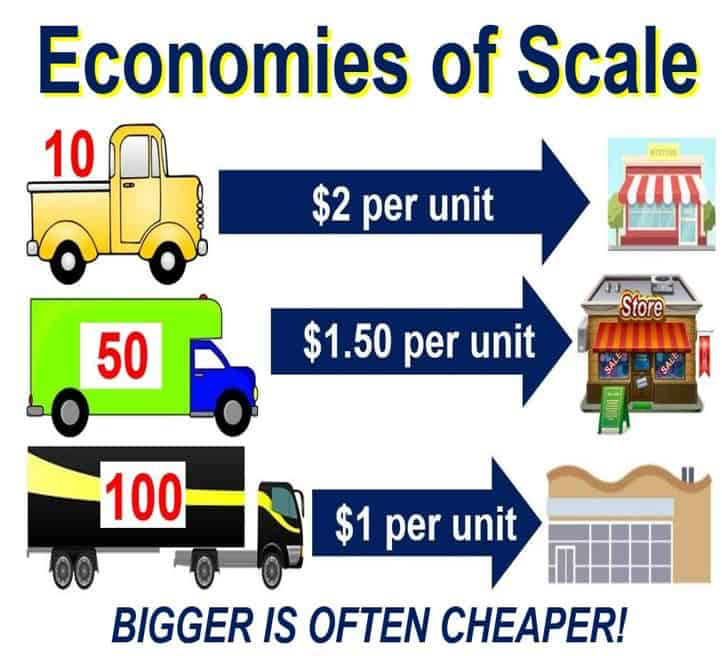

Pool Corp enjoys a lot of Economies of Scale.

They serve 125,000 customers.

The larger they get, the cheaper they can buy and distribute their products.

AI isn’t the problem for Pool Corporation right now.

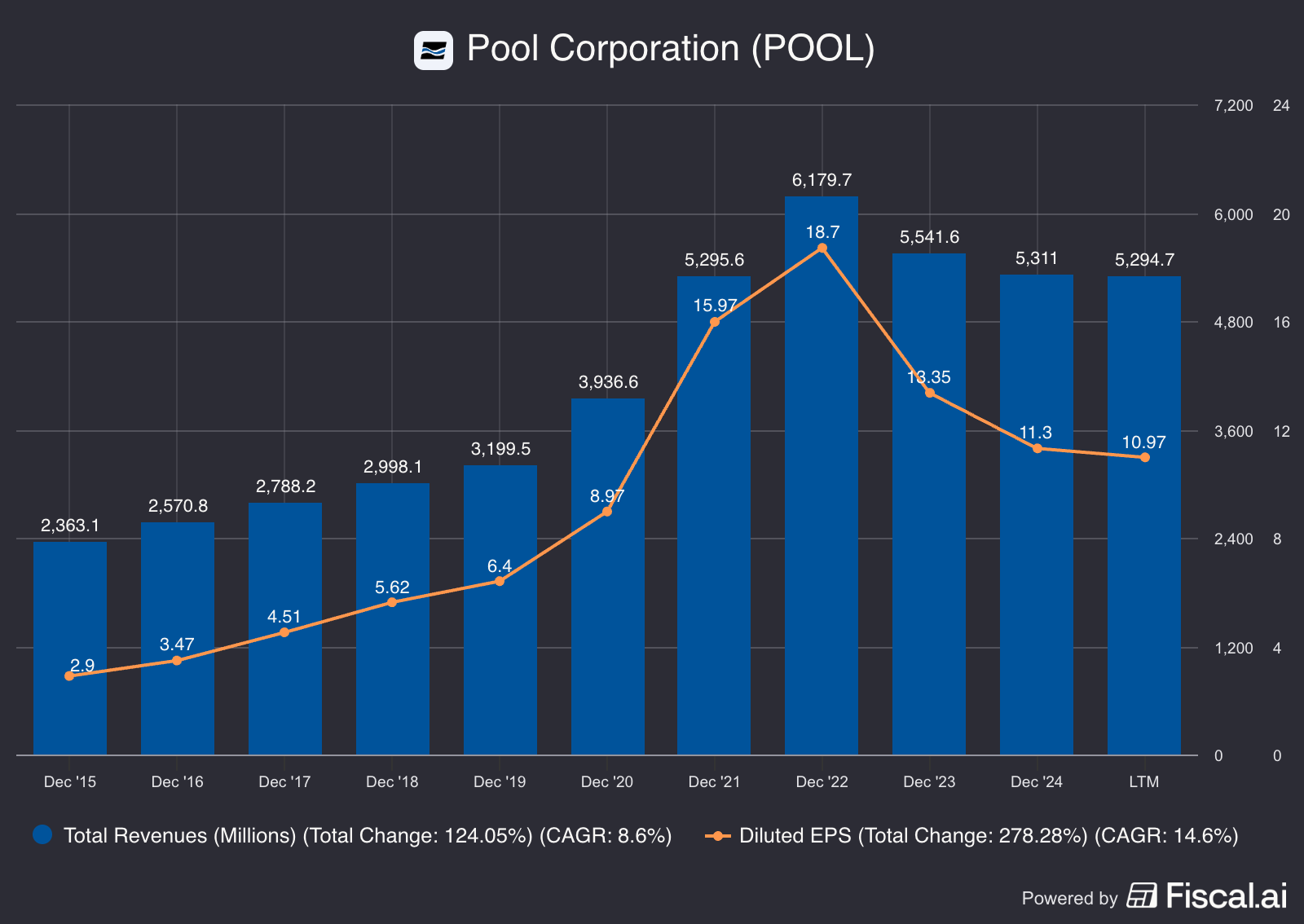

Making too much money during the COVID-19 pandemic is.

Stuck at home with government money in their bank accounts, people across the country made one decision: build a pool.

Demand surged and peaked in 2022. Since then, Pool Corporation struggled to keep growing.

The good news for Pool Corp?

All the new pools installed during the demand spike will need chemicals and maintenance products for the next few decades.

Pool Corporation benefits a lot from these recurring sales.

Short term investors are seeing the earnings decline as permanent.

That’s why Pool is trading at an attractive valuation today.

Buying a business with recurring sales and a strong moat like Pool during a cyclical bottom is often a great investment for a long-term investor.

4. Adyen ($ADYEN)

How does Adyen make money?

Adyen is a global payment technology platform that enables merchants to accept and process payments across channels and geographies through a single integrated system. The company makes money by charging transaction fees on processed payment volume.

Is it an interesting company?

Adyen is a single-platform global payments processor for clients like:

Uber

Netflix

Starbucks

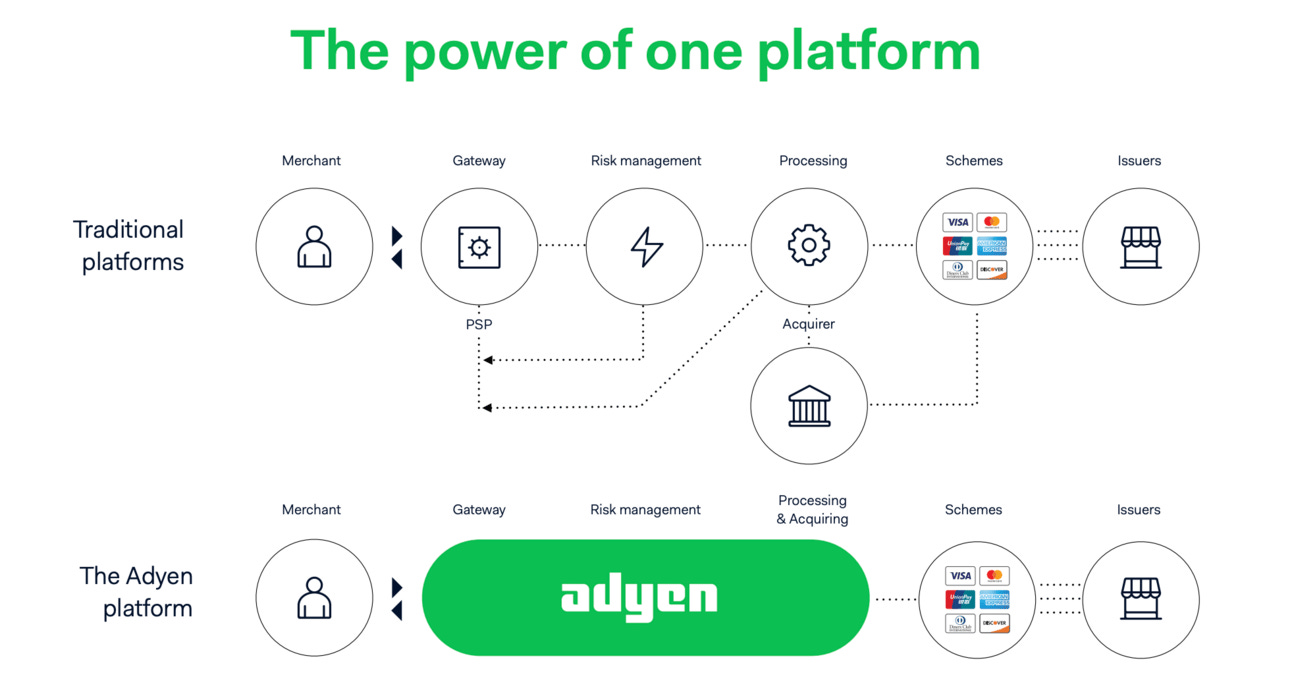

The company has a clear competitive advantage.

Most competitors use a patchwork of old systems.

Adyen built theirs from scratch.

This leads to Technical Excellence and higher authorization rates for merchants.

The image shows how much simpler Adyen is compared to traditional payments platforms:

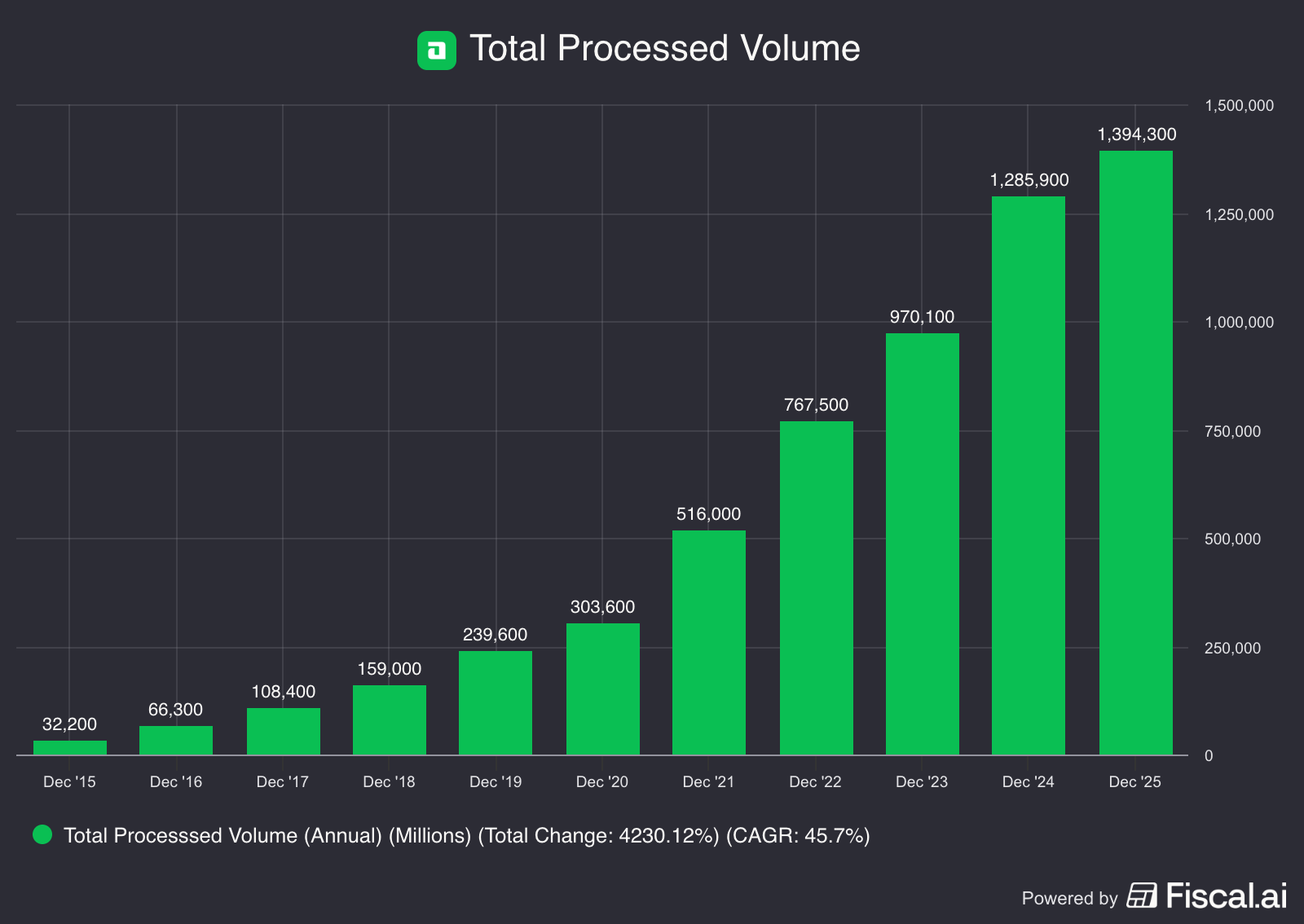

Every single year, more and more payments go through Adyen:

Adyen is a true compounding machine.

They’re able to reinvest at attractive rates, maintain high margins, and generate a lot of cash.

ROIC: 10.0%

Net Margin: 44.7%

FCF/Net Income: 173.7%

In the past, they’ve grown by over 30% per year:

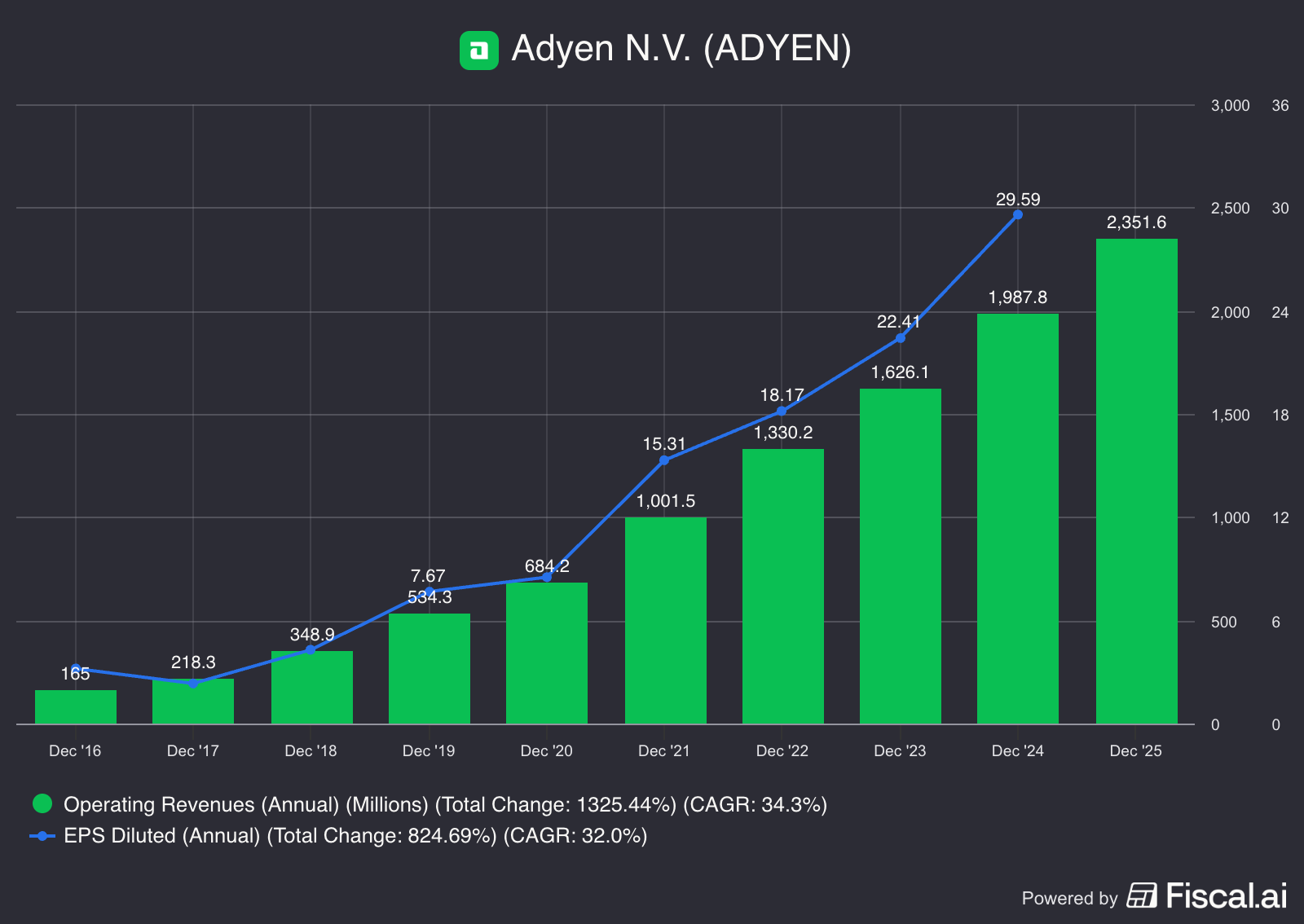

But the stock fell nearly 40% at one point because H2 2025 volume growth was ‘only’ 12%.

Investors who were used to 30% growth panicked and sold.

But guess what? There’s a very good reason for the slowdown.

Adyen is choosing Quality over Volume.

They are walking away from low-margin transactions to focus on more profitable enterprise partnerships.

They are also expanding into Embedded Finance (issuing cards) which grew 8x last year.

This kind of long-term thinking and investment in the business shouldn’t be a surprise.

What makes it even better? Adyen is still run by it’s co-founder, Pieter Willem van der Does. He owns 3% of the company.

Now let’s dive into the top 3.