Best Buys: May 2026

By monthly tradition, you’ll get an update on our Best Buys of the month.

What’s going on in the markets? And what are our favorite stocks?

Let’s get a little bit wiser today.

April 2026

The S&P 500 rose by 9.7% in April.

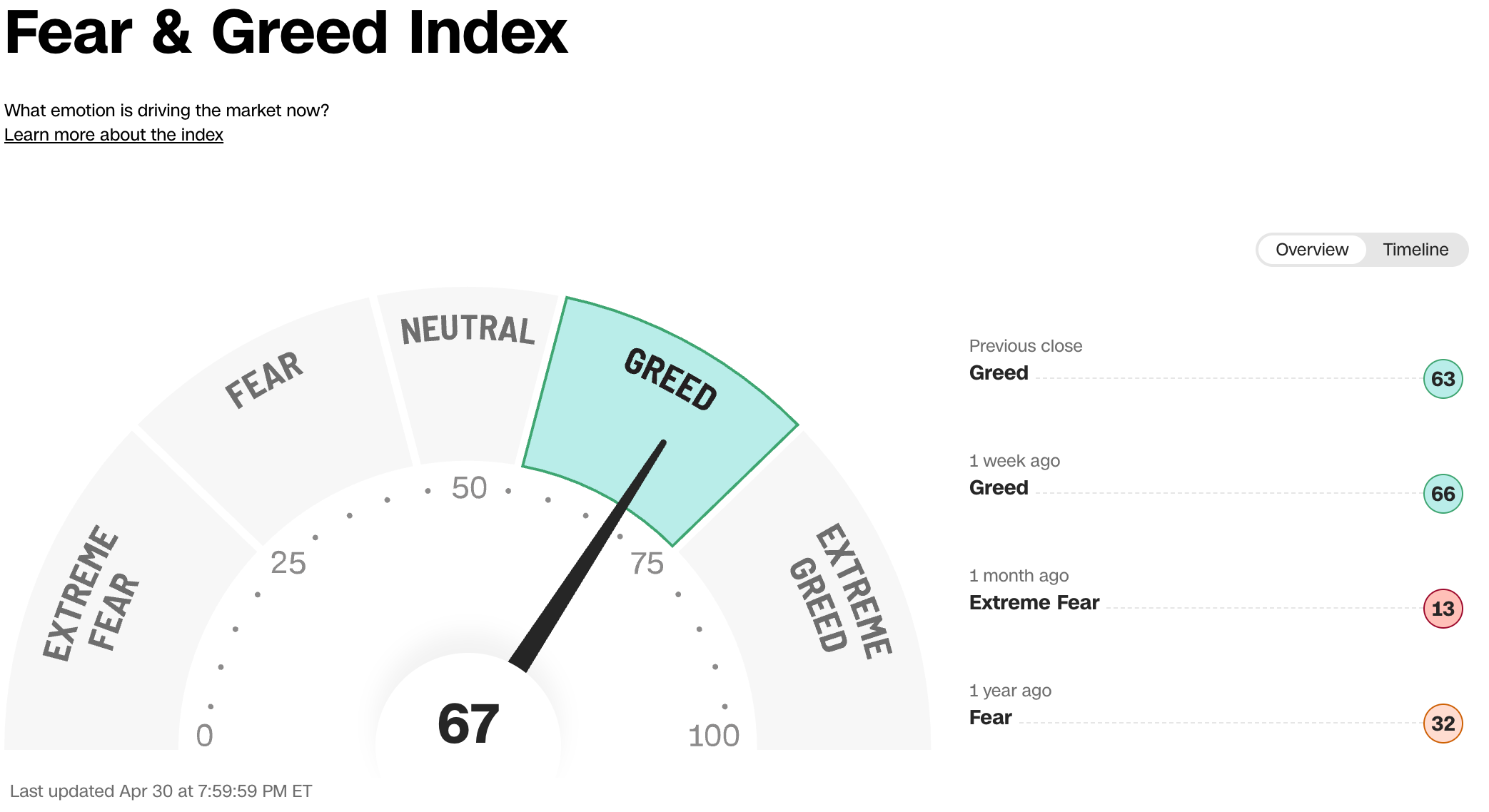

Investors are greedy today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

Worst performers

The cheaper we can buy great companies, the better.

Here are the worst performers of the past month:

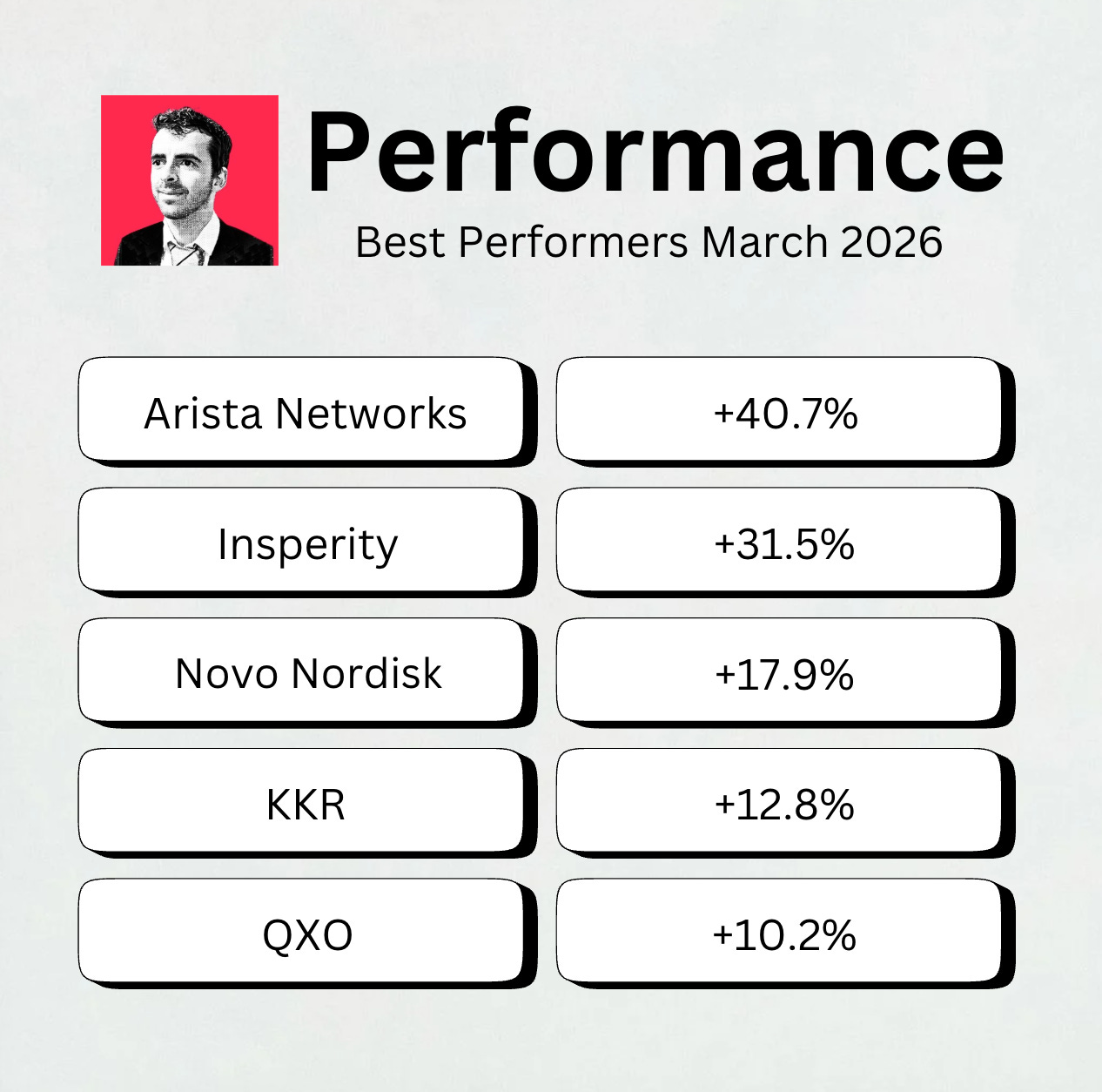

Best performers

These stocks did well over the past month:

🏗️ Spotlight: QXO, Inc. ($QXO)

How Does The Company Make Money?

QXO is a distributor of building products.

They act as the middleman between manufacturers and contractors.

The company is a serial acquirer. They recently acquired TopBuild.

As a result, they are now a clear market leader:

#1 in insulation

#2 in roofing

#1 in waterproofing

#1 or #2 in the lumber and building materials sector

Why does it deserve to be in the spotlight?

We can’t talk about QXO without talking about its founder.

Brad Jacobs is widely considered one of the most successful serial consolidators in business history.

He founded eight separate billion-dollar companies and wrote two must read books:

How to make a few billion dollars

How to make a few extra billion dollars

(Watch out. If you’re reading these books in public, people look at you strangely. I speak from personal experience)

His strategy is a three-step formula.

He used it over and over to build dominant companies in different industries.

Identify a Fragmented, Analog Industry: Jacobs looks for large markets with thousands of small, local players using outdated technology.

Buy the Anchors: He raises massive amounts of capital upfront to buy the biggest and most important players in the industry. This gives him immediate scale and purchasing power that no local competitor can match.

Use Tech to Become Efficient: Once he owns the companies, he puts teams into place to get rid of inefficient processes and replace them with high-tech solutions. At XPO, he used AI to optimize truck routes, at QXO, he is using it to centralize pricing and inventory across 1,150+ locations.

The track record of Brad Jacobs is phenomenal:

United Waste Systems (1989): Sold it for $2.5 billion

United Rentals (1997): Built the world’s largest equipment rental company from scratch

XPO Logistics (2011): Grew revenue from $175 million to $15 billion

QXO is his latest project.

He is applying his successful playbook to the $800 billion fragmented building products industry.

In the past 12 months alone, QXO has spent over $30 billion on acquisitions.

The TopBuild Acquisition

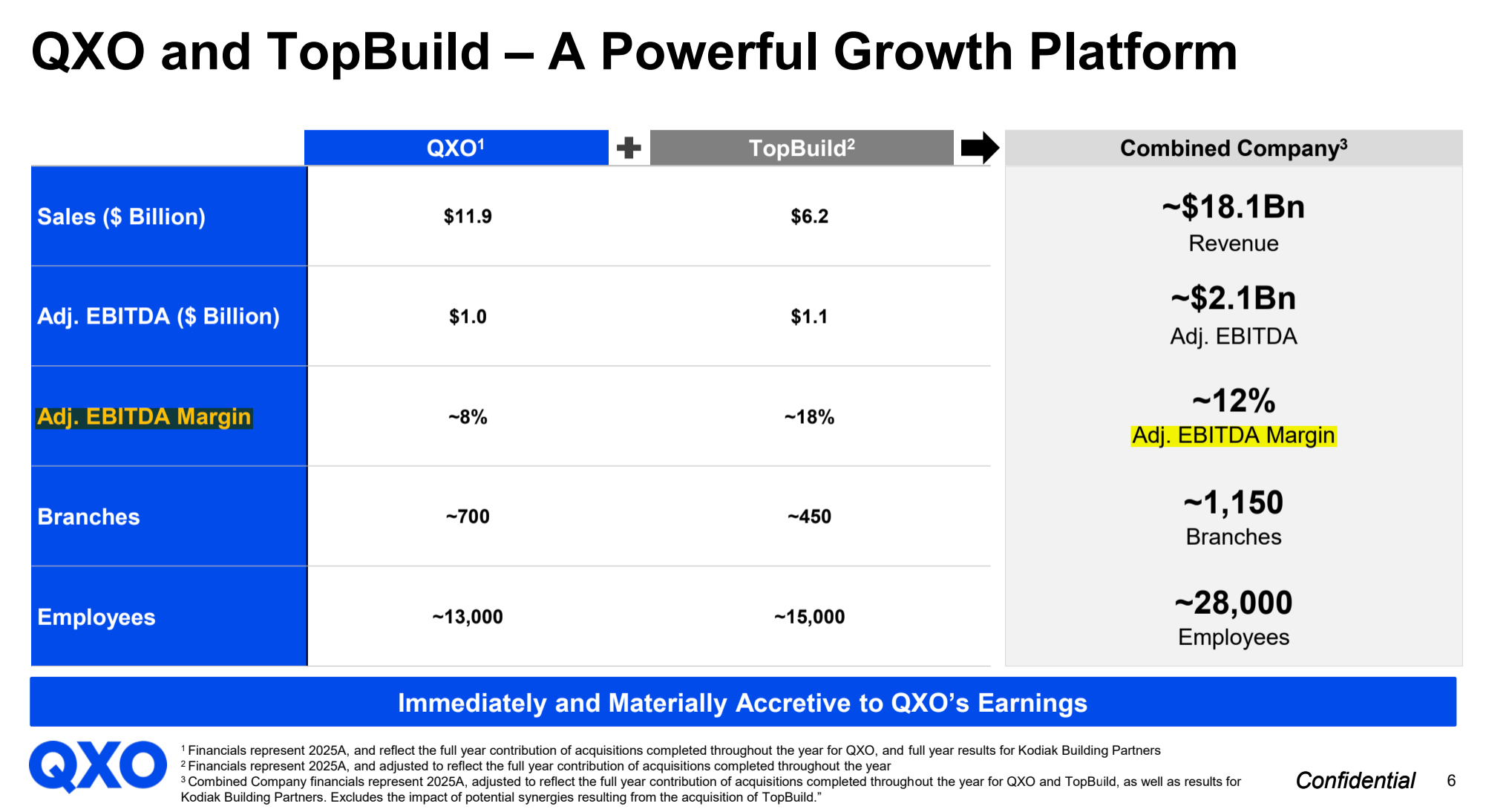

The biggest catalyst for QXO is the $17 billion acquisition of TopBuild (BLD).

The acquisition was announced in April 2026.

TopBuild is the largest distributor and installer of insulation and related building products in North America

I know the company well as I used to follow it when I was involved in the daily management of a Climate Fund.

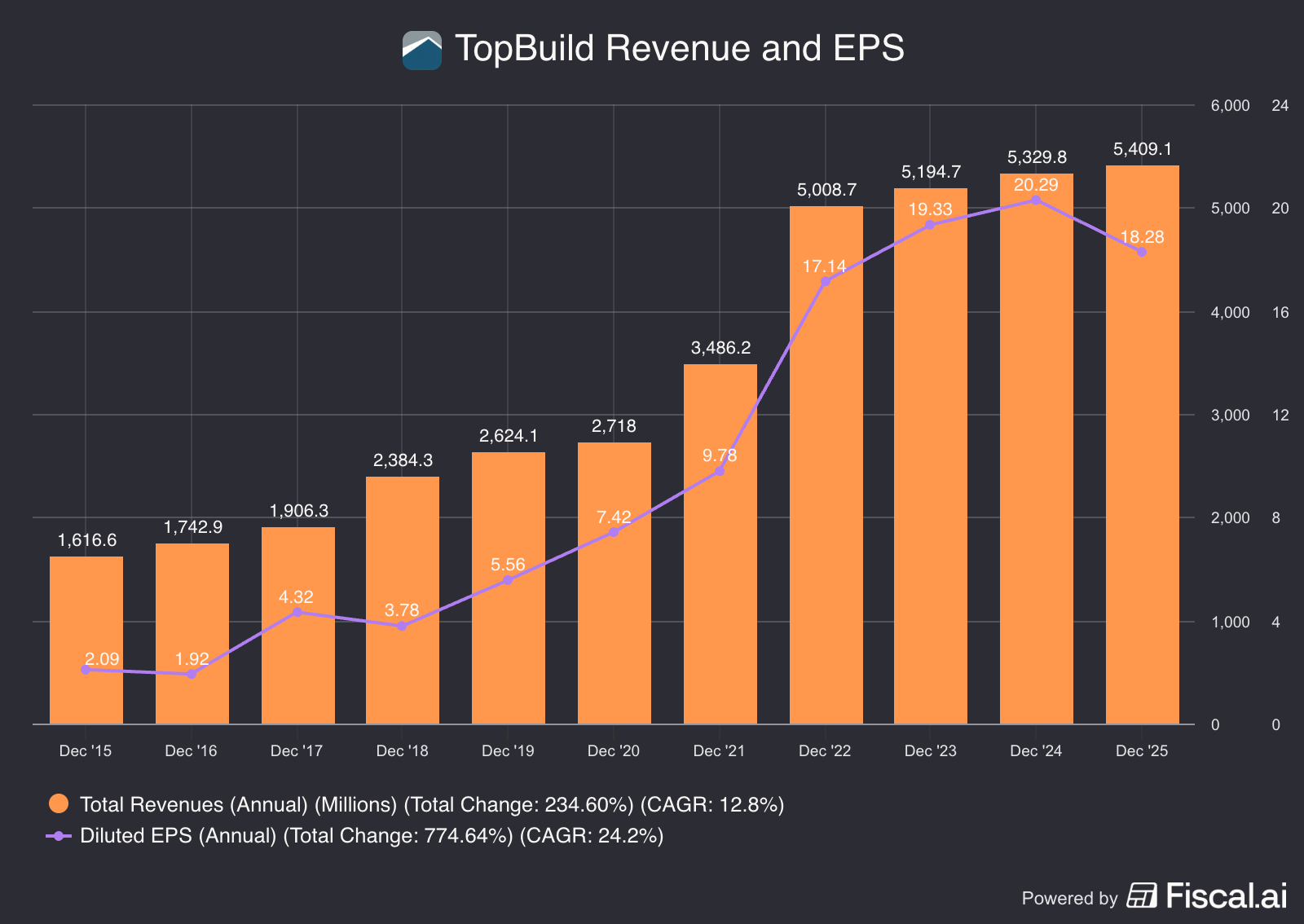

The stock is up +444% since 2020.

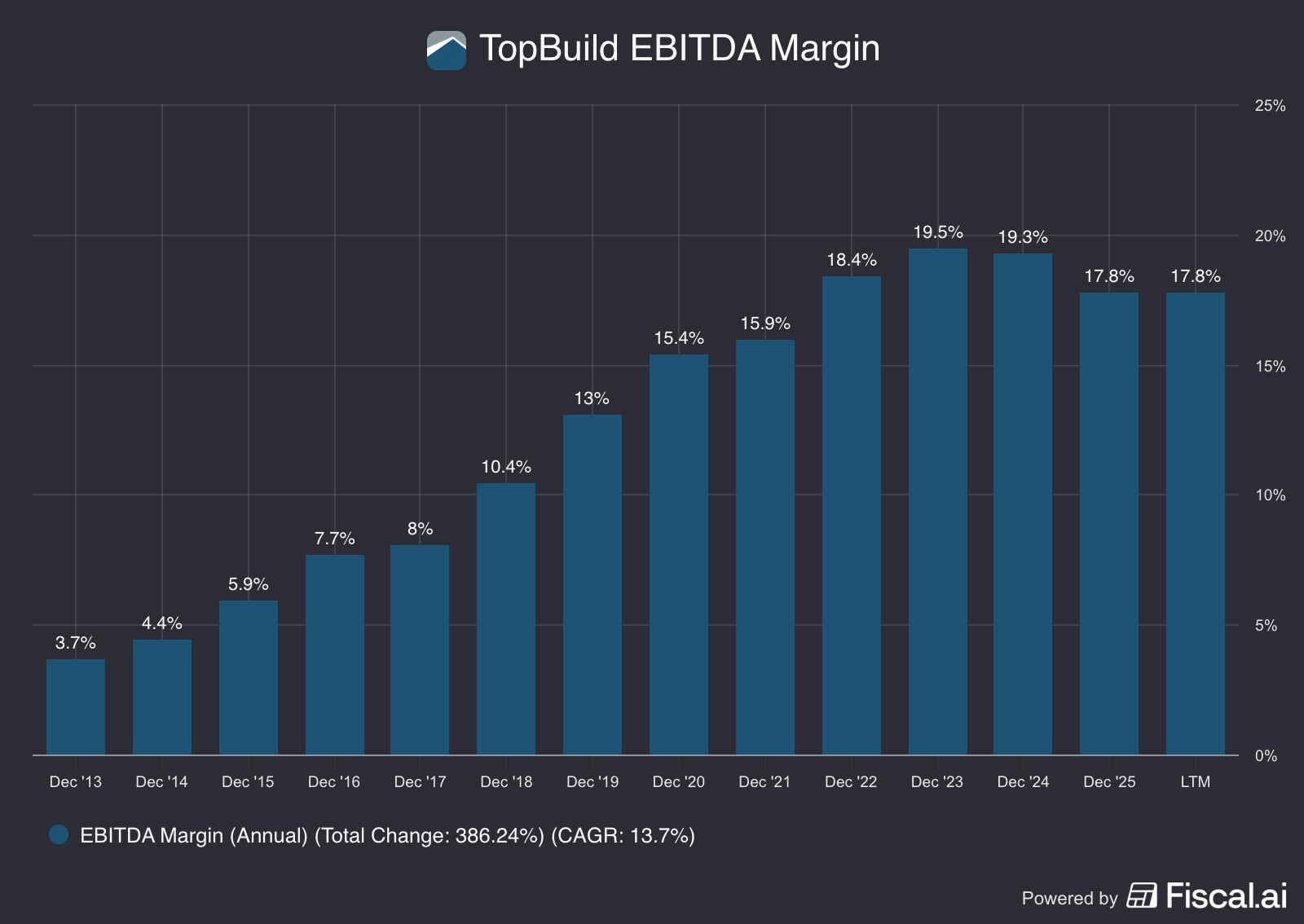

It’s Revenue and EPS grew very attractively too:

Why this deal matters:

Market Leadership: It makes QXO the #2 largest building products distributor in North America

Scale: The merger adds $6.2 billion in annual revenue and over 400 locations

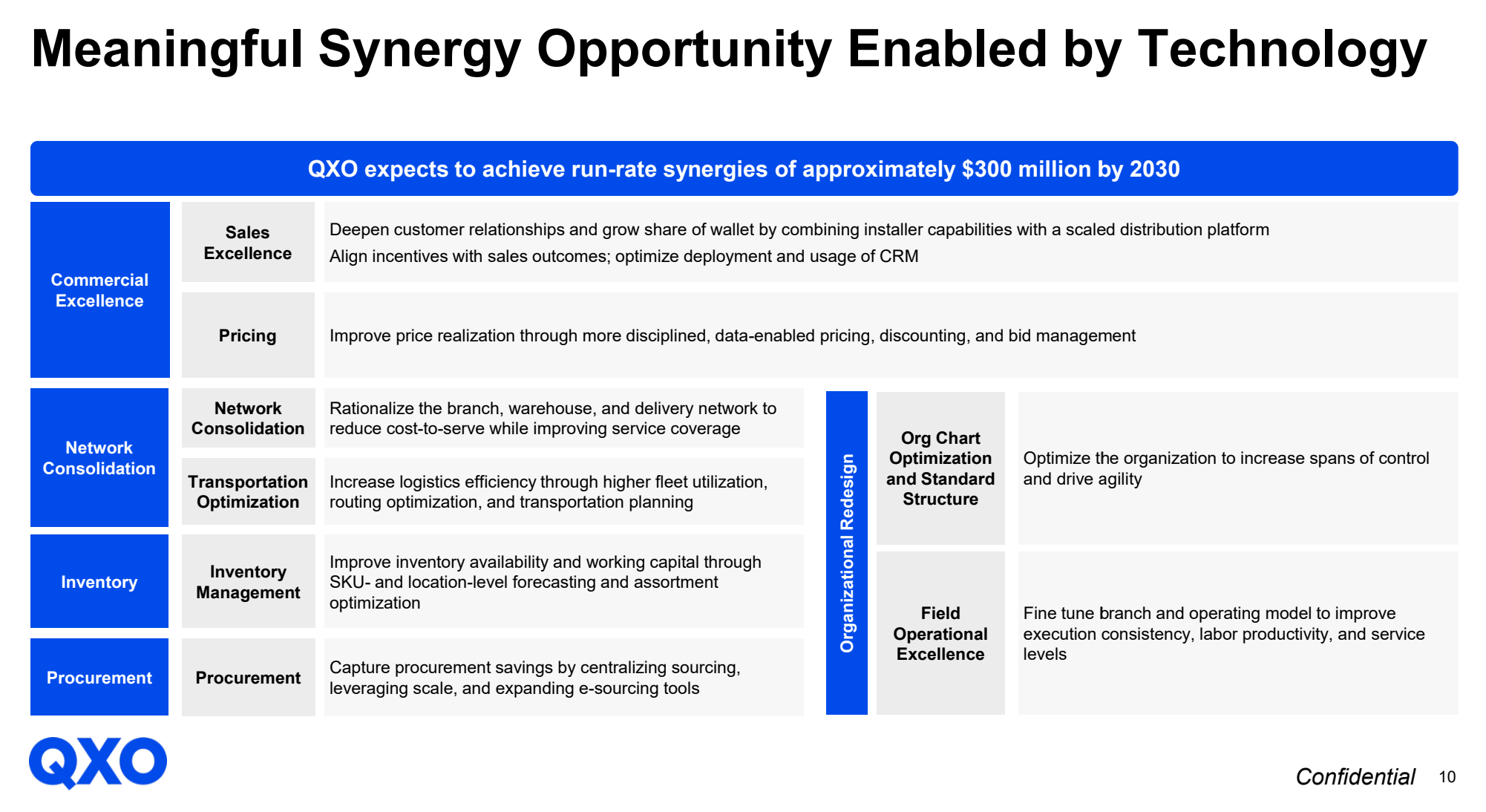

Cost Savings: Management expects to realize $300 million in annual synergies by 2030 through scaled procurement and logistics

Another important thing about TopBuild?

It has a much higher margin than QXO.

Before this acquisition, QXO had an Adjusted EBITDA margin of around 8%.

TopBuild has margins closer to 18%.

QXO estimates that the combined company will have EBITDA margins of around 12%.

QXO is now the #1 or #2 player in almost every category it touches.

Brad Jacobs added another $6.2 billion in revenue with this acquisition.

On top of that, he bought market dominance and a wider moat.

We love businesses that sell essential products with high switching costs led by world-class management.

Best Buys April 2026

Let’s dive into our five favorite buys for the month.

Please note that the companies in Our Portfolio are not mentioned here.

We love all companies in Our Portfolio right now.

5. Fair Isaac Corporation ($FICO)

How does Fair Isaac make money?

FICO licenses their proprietary credit scoring algorithm to major credit bureaus (Equifax, Experian, and TransUnion).

FICO’s is down over 55% (!) from its peak:

What happened?

In April, the The Federal Housing Finance Agency (FHFA) announced they are officially moving forward with VantageScore 4.0.

It will be used as an alternative to FICO for mortgage underwriting.

Why this drop can be a long-term opportunity (and not a disaster):

Even if lenders add VantageScore, they’ll still pull FICO alongside it. In lending, more data beats different data

Regulations and internal risk models are deeply tied to FICO. Switching to VantageScore means a multi-year infrastructure overhaul most banks won’t risk

FICO’s price hikes are negligible on a $500K mortgage. Lenders care about predictive accuracy, and FICO 10T is still the gold standard

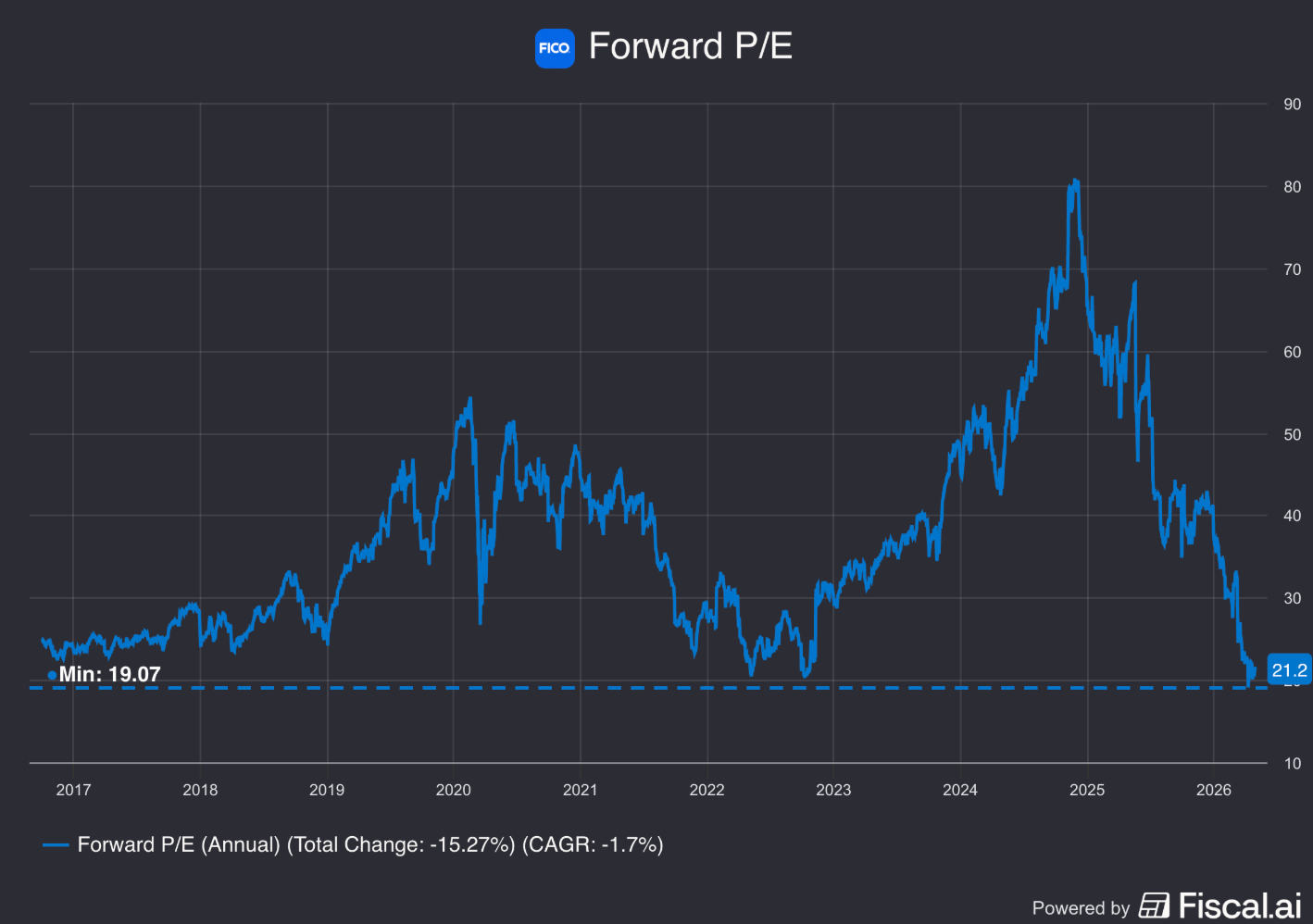

FICO is now very close to the lowest Forward P/E we’ve seen in a decade.

Earlier this week, FICO reported great results.

It seems like the investment thesis is not broken after all.

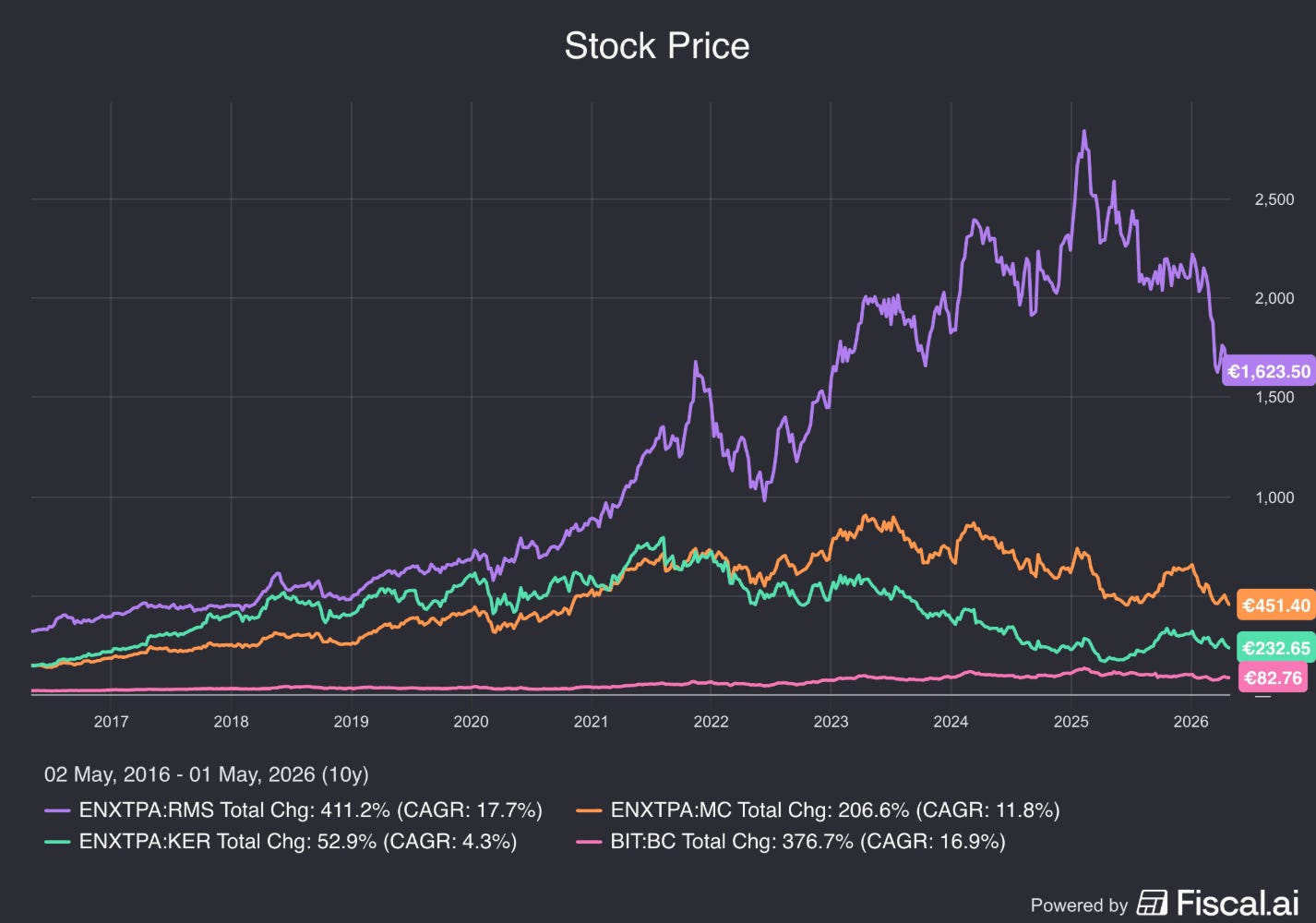

4. Hermès ($RMS)

How does Hermès make money?

Hermès is the king of luxury. They are known for their Birkin and Kelly bags.

The French company uses scarcity as a marketing tool.

They intentionally limit their supply to sell at very high prices.

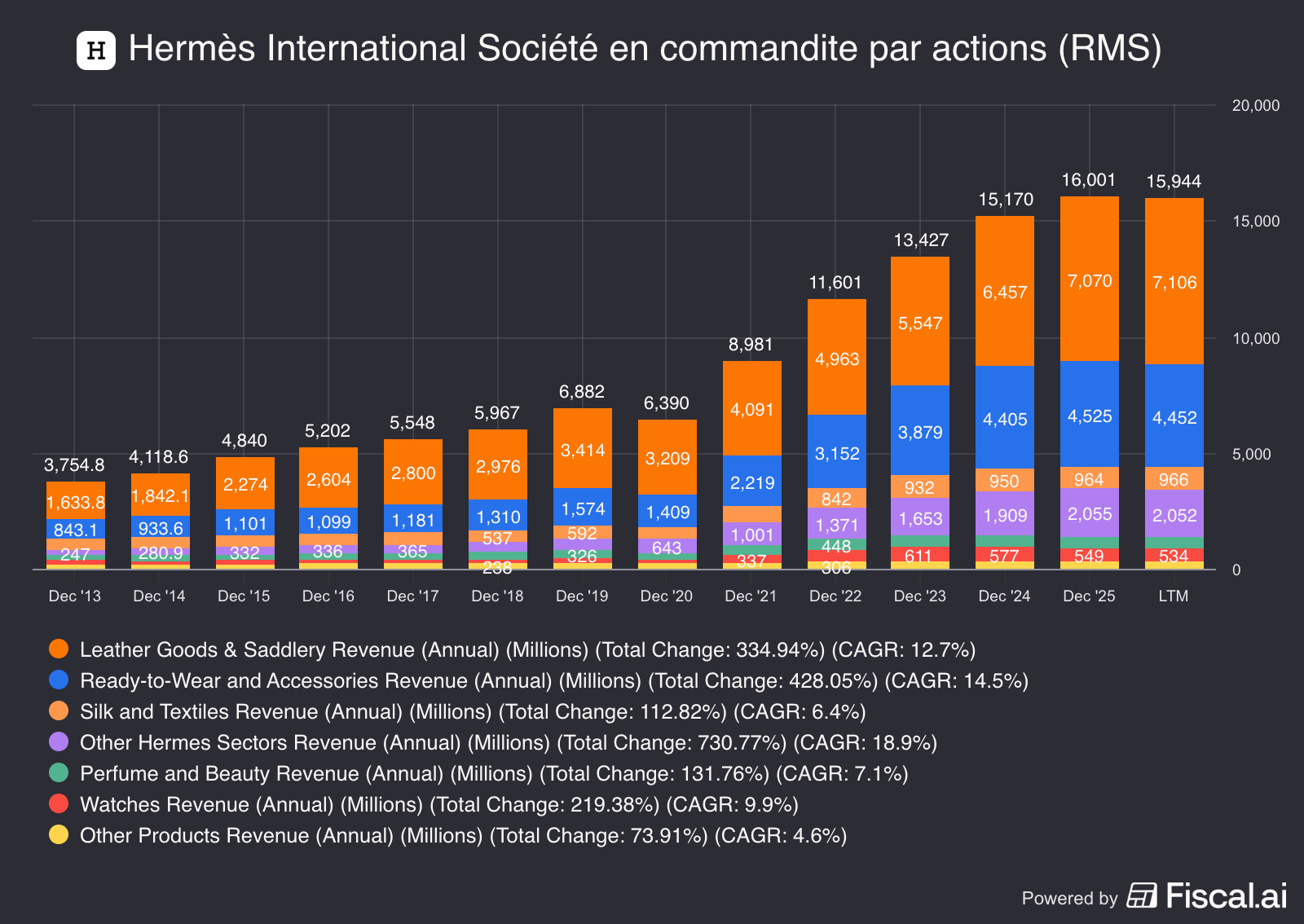

Hermès operates in three main segments:

Leather Goods and Saddlery (~43% of revenue): This is the biggest segment and includes the iconic Birkin and Kelly bags

Ready-to-wear and Accessories (~28%): High-end clothing and footwear

Other (Silk, Watches, Perfume, etc. ~ 29%): Complementary luxury items

The financial performance is amazing.

In 2025, Hermès grew its revenue to €16 billion (up 9% at constant rates) with an operating margin of 41%.

Why does it deserve to be in the spotlight?

Hermès is the ultimate Veblen Good.

This means that as the price goes up, the demand increases because the prestige grows.

You cannot simply walk into a store and buy a Birkin bag. Hermès makes you put your name on a waitlist

Hermès owns its supply chain, from the tanneries to the workshops. This lets them completely control quality in a way competitors can’t.

Hermès caters to the ultra-wealthy. During downturns, their spending tends to hold up better than most consumers. That’s why Hermès is often the last luxury brand to feel a slowdown and the first to recover.

Now let’s dive into the top 3.