Can Arista Networks win the AI-race?

Not-So-Deep-Dive

Every time you use AI or the cloud, huge amounts of data move in the background.

Arista Networks helps power the infrastructure that makes all of this possible.

Let’s dive into this rapidly growing high-quality company with exposure to AI.

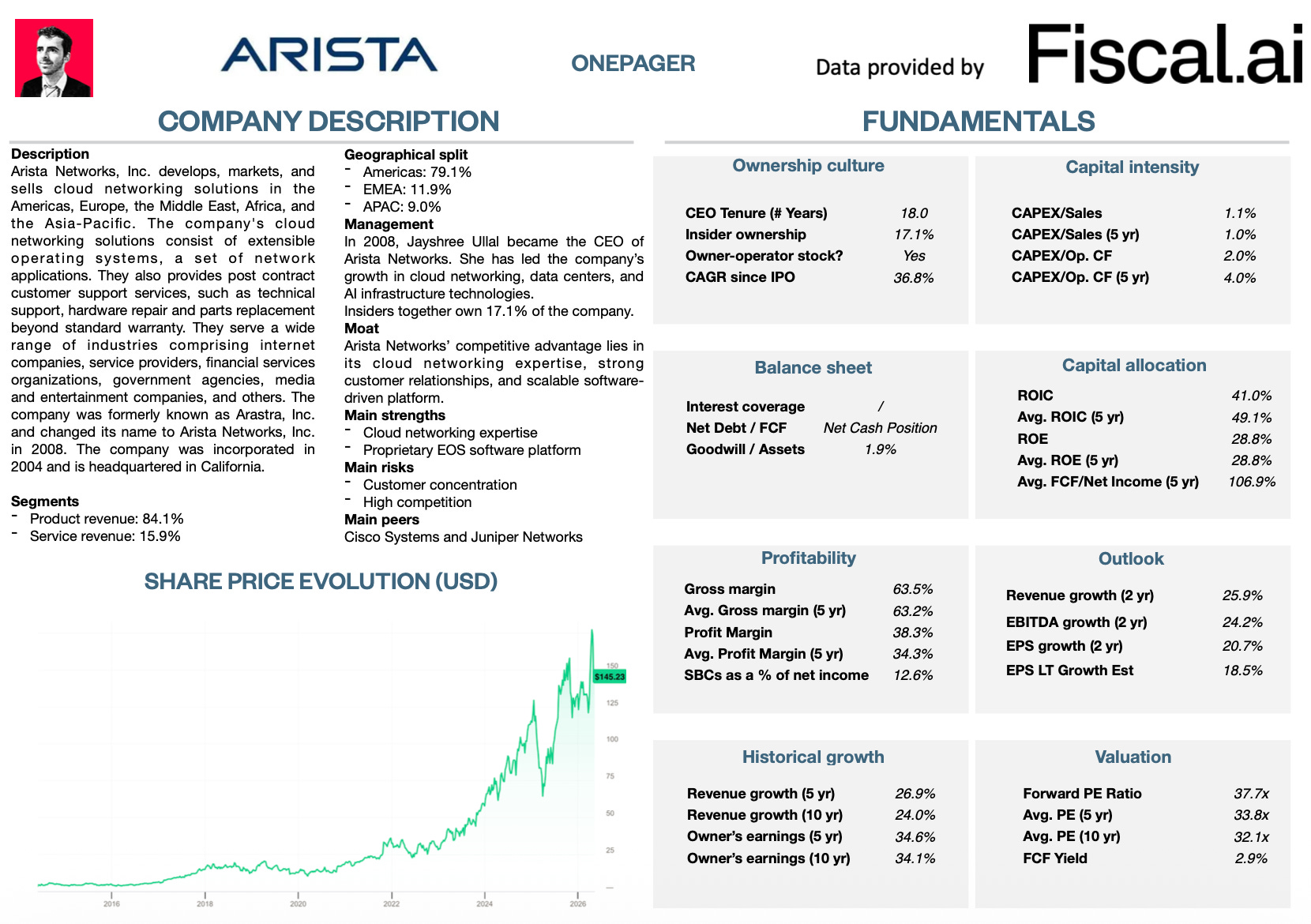

Arista Networks - General Information

👔 Company name: Arista Networks

✍️ ISIN: US0404132054

🔎 Ticker: ANET

📚 Type: Owner-Operator Stock

📈 Stock Price: $145.9

💵 Market cap: $179.9 billion

📊 Average daily volume: $1.2 billion

Onepager

Here’s a onepager with the essentials of Arista Networks:

15-Step Approach

Now let’s use our 15-step approach to analyze the company.

At the end of this article, we’ll give Arista Networks a score on each of these 15 metrics. This results in a Total Quality Score.

1. Do I understand the business model?

AI and the cloud are everywhere.

They shape our entire digital world.

And guess what? Arista Networks plays a key role in making it all happen.

Think of Arista as a pick-and-shovel business in the booming AI industry.

During the gold rush, the people who got rich weren’t the gold diggers... but the ones selling the shovels.

That’s exactly what Arista does. They deliver the technology that connects computers and servers.

Their advanced networking solutions move data at lightning speed. It’s the backbone every AI system and cloud network needs to run.

Who buys from Arista? The biggest names you know.

Microsoft, Meta, Google, Oracle,…

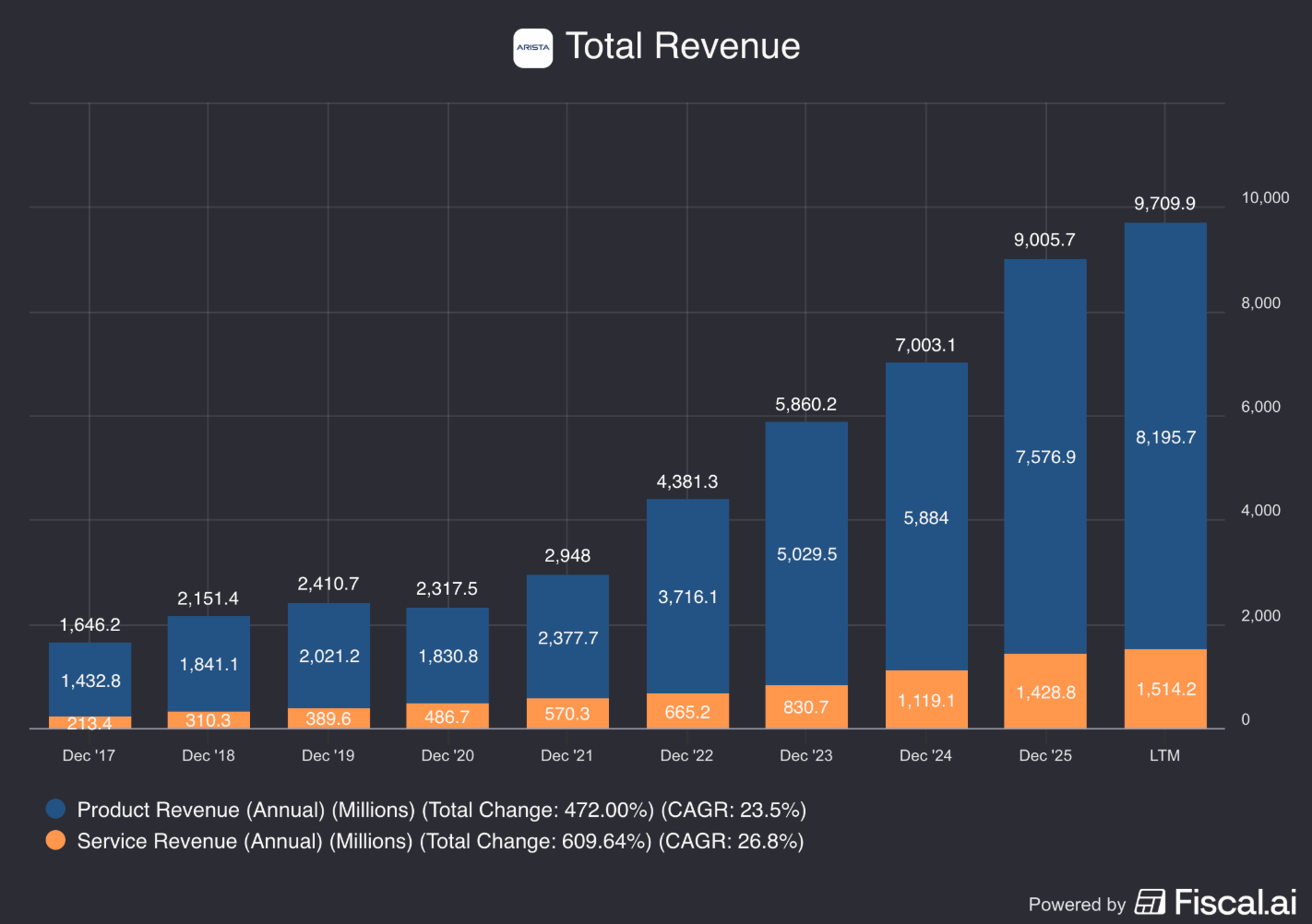

Arista makes money in two ways:

Selling Products (84.1% of sales): Most of the money comes from selling hardware like switches and routers. They also add powerful software called EOS and CloudVision.

Selling Services (15.9% of sales): Arista offers maintenance contracts and premium support to companies that depend on their gear every single day.

2. Is management capable?

Jayshree V. Ullal has led Arista Networks as CEO since 2008, playing a major role in building the company into a leader in cloud networking.

Before joining Arista, she held senior executive positions at Cisco.

Under her leadership, Arista went public in 2014 and has grown into one of the most respected networking companies in the industry.

Ullal is also one of the most prominent women in technology. She owns 2.2% of the company (worth $4.8 billion).

All insiders together own 17.1% of Arista.

Co-founder Andreas Bechtolsheim is the largest shareholder with an estimated 14.6% stake.

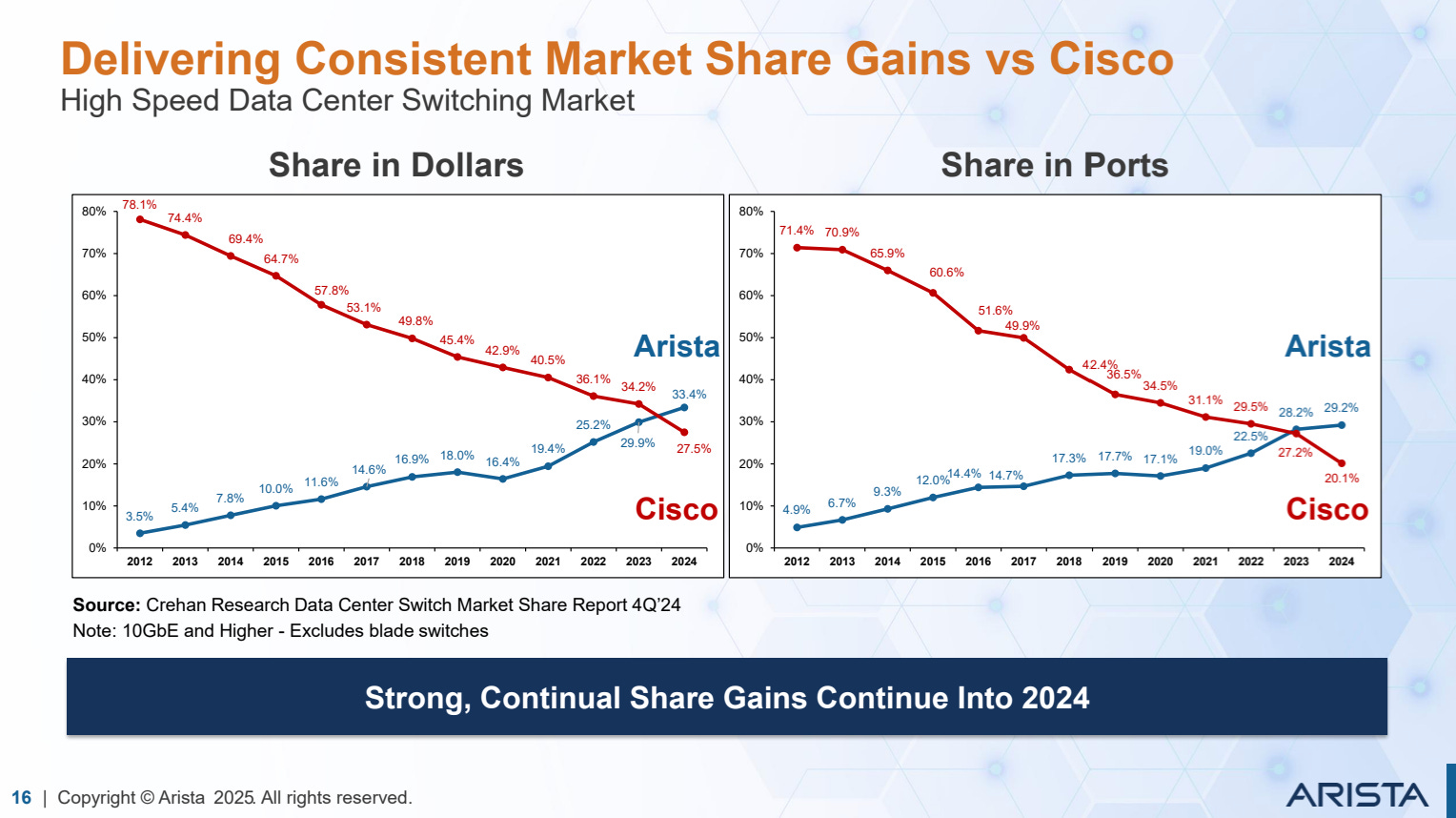

3. Does the company have a sustainable competitive advantage?

Arista Networks has a sustainable competitive advantage based on switching costs, efficient scale, and intangible assets.

Cisco is Arista’s main competitor.

Arista outperforms Cisco with simpler, more reliable software that make updates and automation easier.

Once a customer starts using Arista’s products, they almost never switch.

Although Arista and Nvidia collaborate closely, they’re also becoming competitors.

Arista connects Nvidia GPUs via Ethernet, while Nvidia promotes its own expensive InfiniBand. As AI grows, Arista’s affordable solution becomes more attractive.

Today, Arista is smaller than Cisco and Nvidia but rapidly gaining market share thanks to its scalable, cloud-focused solutions.

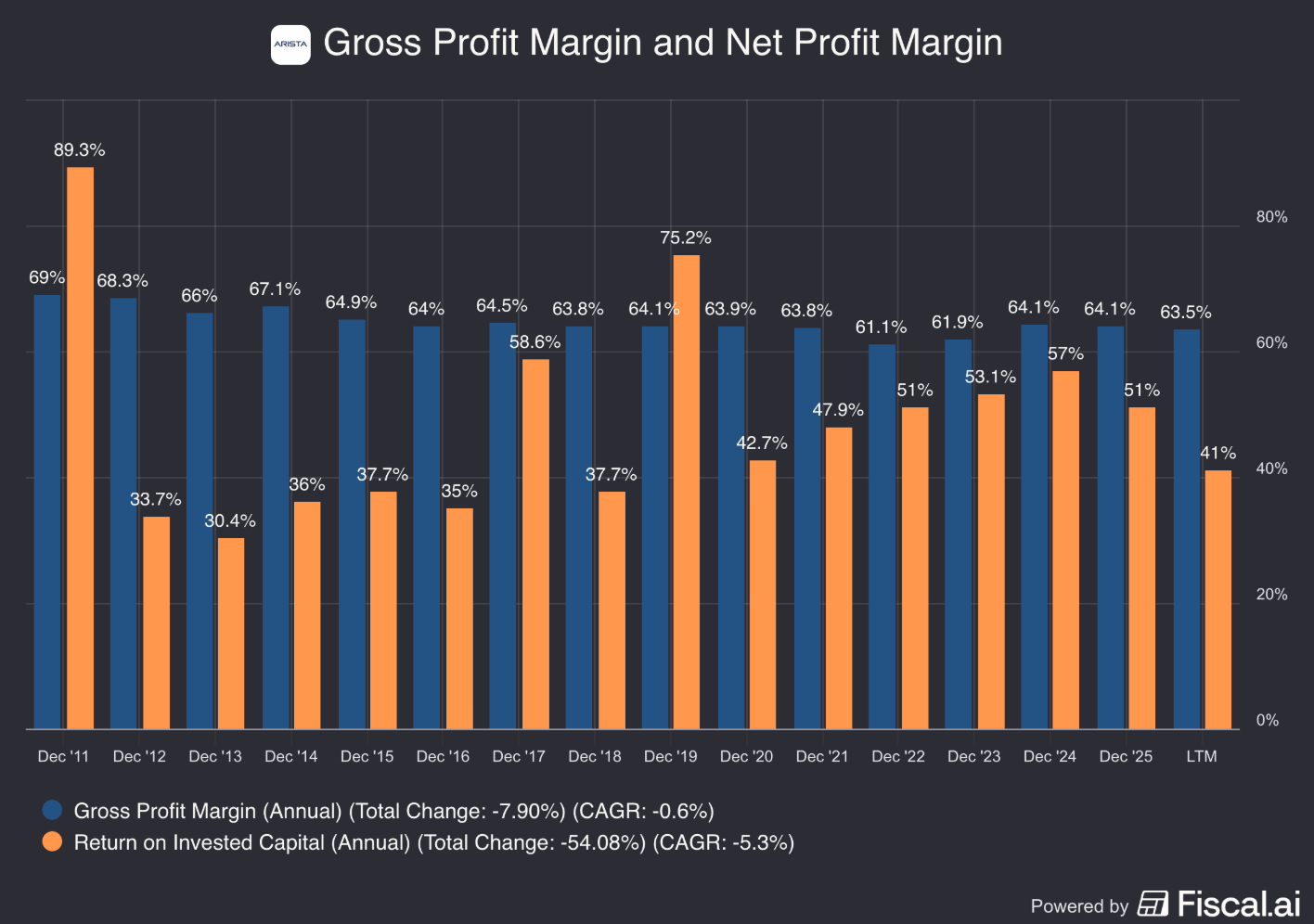

Companies with a sustainable competitive advantage are often characterized by high Gross Margins and a high ROIC.

This is certainly the case for Arista Networks:

Gross Margin: 63.5% (Gross Margin > 40% ✅)

ROIC: 41.0% (ROIC > 15% ✅)

4. Is the company active in an attractive end market?

Yes, Arista Networks operates in a growing market driven by AI infrastructure, cloud computing, and the rising demand for high-performance networking.

Today, nearly 60% of the world’s business data is stored in the cloud, and that percentage continues to increase.

At the same time, major customers such as Microsoft, Meta Platforms, and Google are investing billions into AI infrastructure.

This creates a strong tailwind for Arista’s products and services.

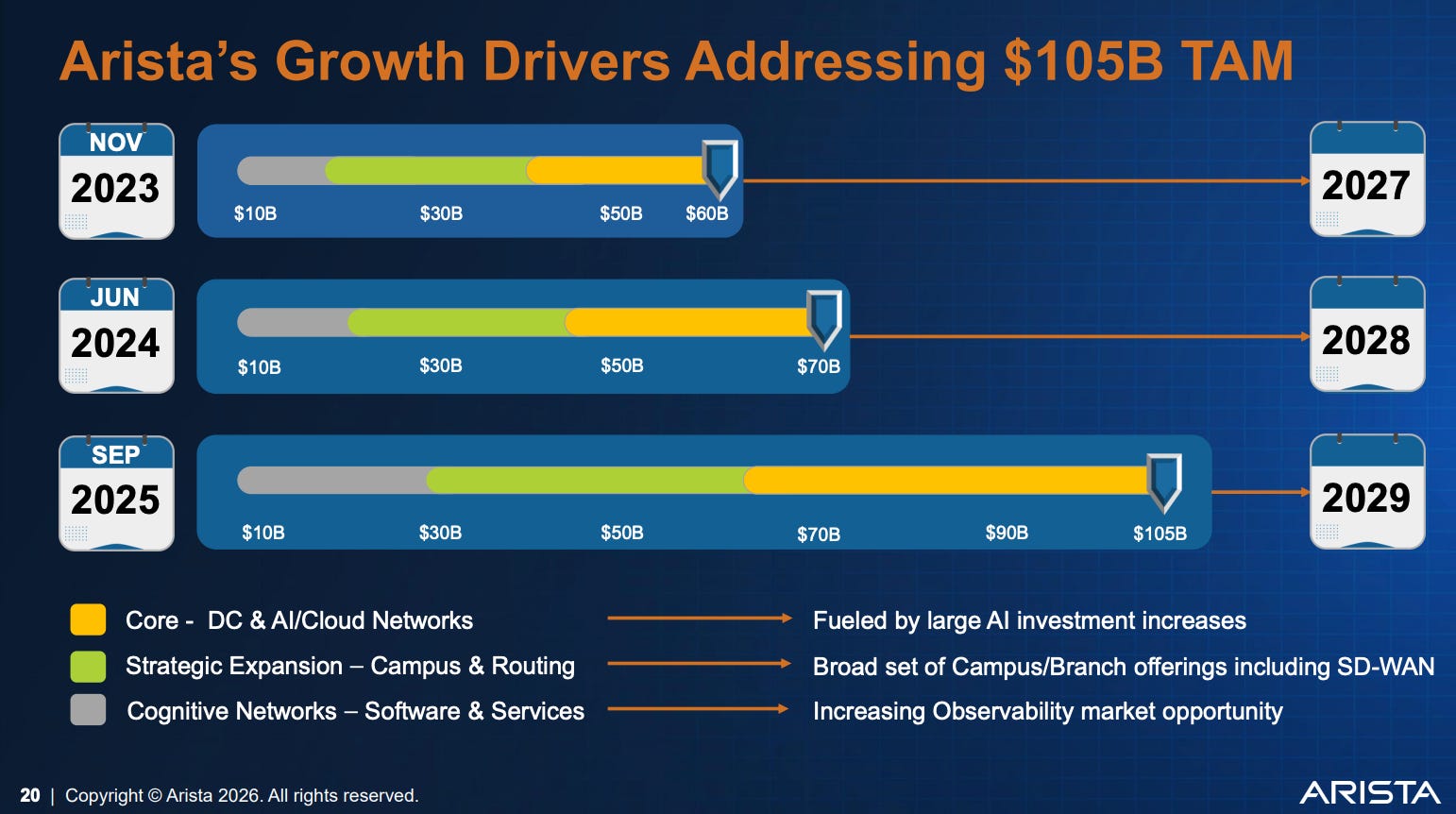

Management estimates Arista’s Total Addressable Market (TAM) could reach $105 billion by 2029, highlighting the company’s significant long-term growth potential.

Arista’s opportunity is mainly divided into three segments:

Core (Data Center & Cloud Networks): The company’s main business, providing networking solutions for hyperscalers, cloud providers, and large-scale data centers

Cognitive Adjacency (Campus & Routing): Arista helps large enterprises connect and manage internal systems, offices, and networks more efficiently

Cognitive Network (Software & Services): Arista’s fastest-growing segment, focused on software and cloud-based tools that automate, optimize, and secure networks using AI-driven capabilities

5. What are the main risks for the company?

No matter how attractive Arista Networks may seem, it is not without risks.

In my view, these are the biggest risks:

Customer concentration: 35% of the revenue comes from two companies, Microsoft and Meta, making Arista vulnerable to changes in their spending

Competitive and technological disruption: Although Arista is gaining market share, innovations and cheaper alternatives could threaten its position

Long lead times: Arista holds extra inventory due to long lead times, but if demand falls, excess inventory can be costly

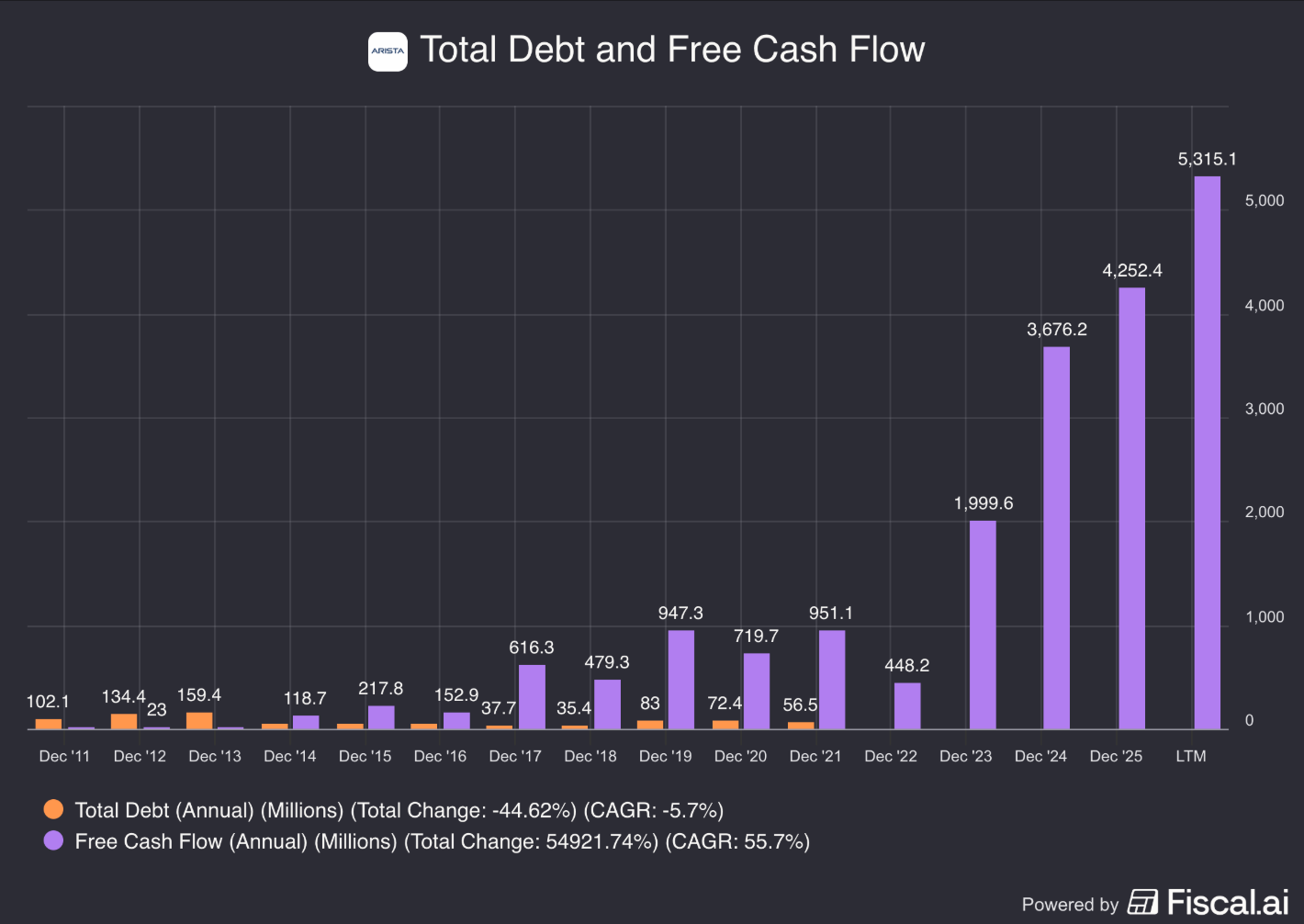

6. Does the company have a healthy balance sheet?

We look at three ratios to determine the healthiness of the balance sheet:

Interest Coverage: Arista Networks has no Interest Coverage Ratio because it has almost no debt to repay (Interest Coverage > 15x ✅)

Net debt/FCF: Net Cash Position (Net debt/FCF < 4x ✅)

Goodwill/Assets: 1.9% (Goodwill to assets? < 20% ✅)

Arista has a very strong financial position.

7. Does the company need a lot of capital to operate?

The less capital a business needs to operate, the better.

Here’s what things look like for Arista Networks:

CAPEX/Revenue: 1.1% (CAPEX/Revenue < 5%? ✅)

CAPEX/Operating Cash Flow: 2.0% (CAPEX/Operating Cash Flow? < 25% ✅)

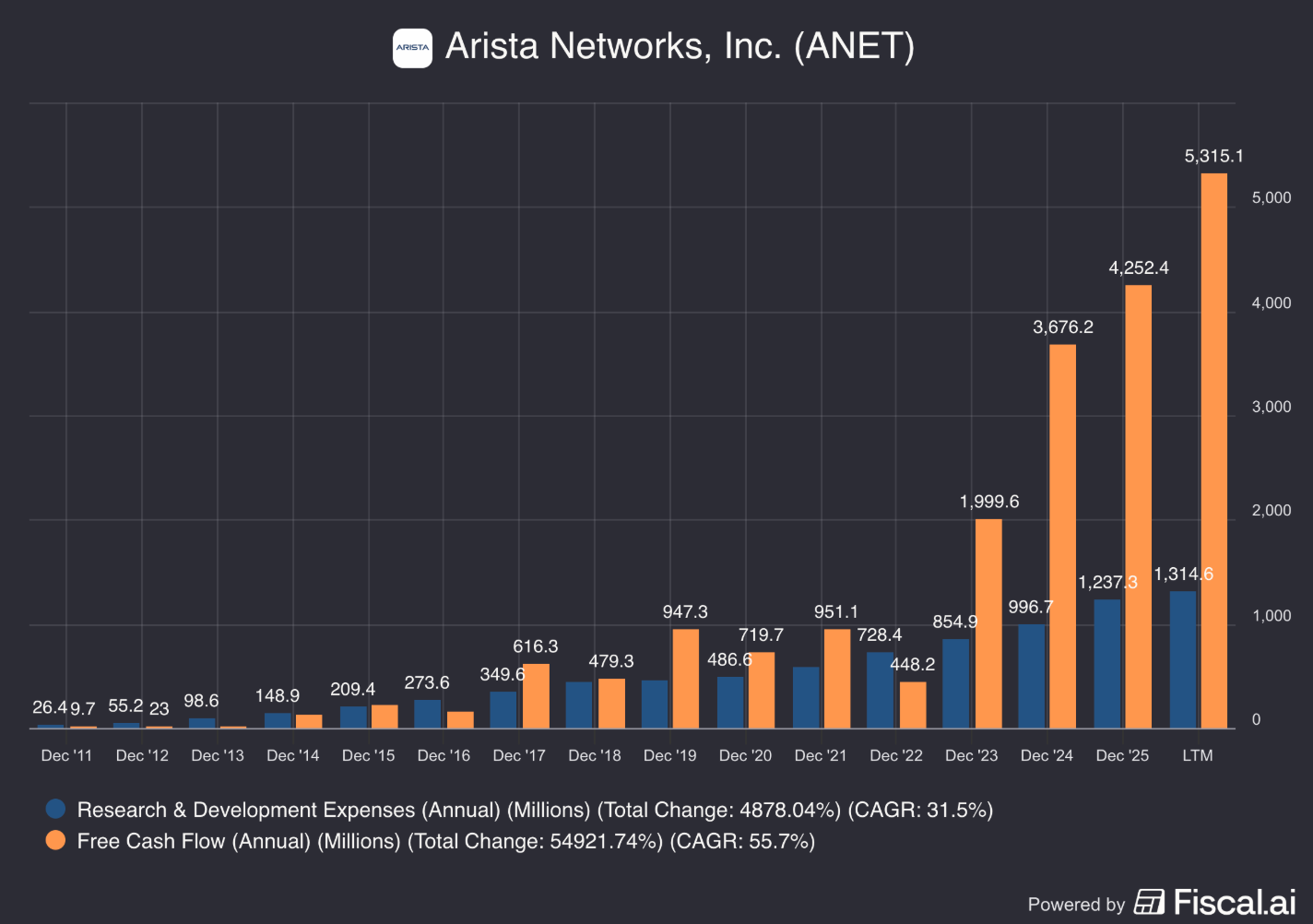

As Arista spends little on factories or equipment, its CAPEX is very low.

R&D spending is a better indicator of how capital-intensive the business truly is.

R&D/Revenue: 13.5% (R&D/Revenue = 10%-20%? ✅)

R&D/Operating Cash Flow: 24.2% (R&D/Operating Cash Flow = 25%-50%? ✅)

Arista is a capital-light company that grows through innovation.

8. Is the company a great capital allocator?

Capital allocation is the most important task of management.

Look for companies that put the money of shareholders to work at an attractive rate of return.

Arista Networks:

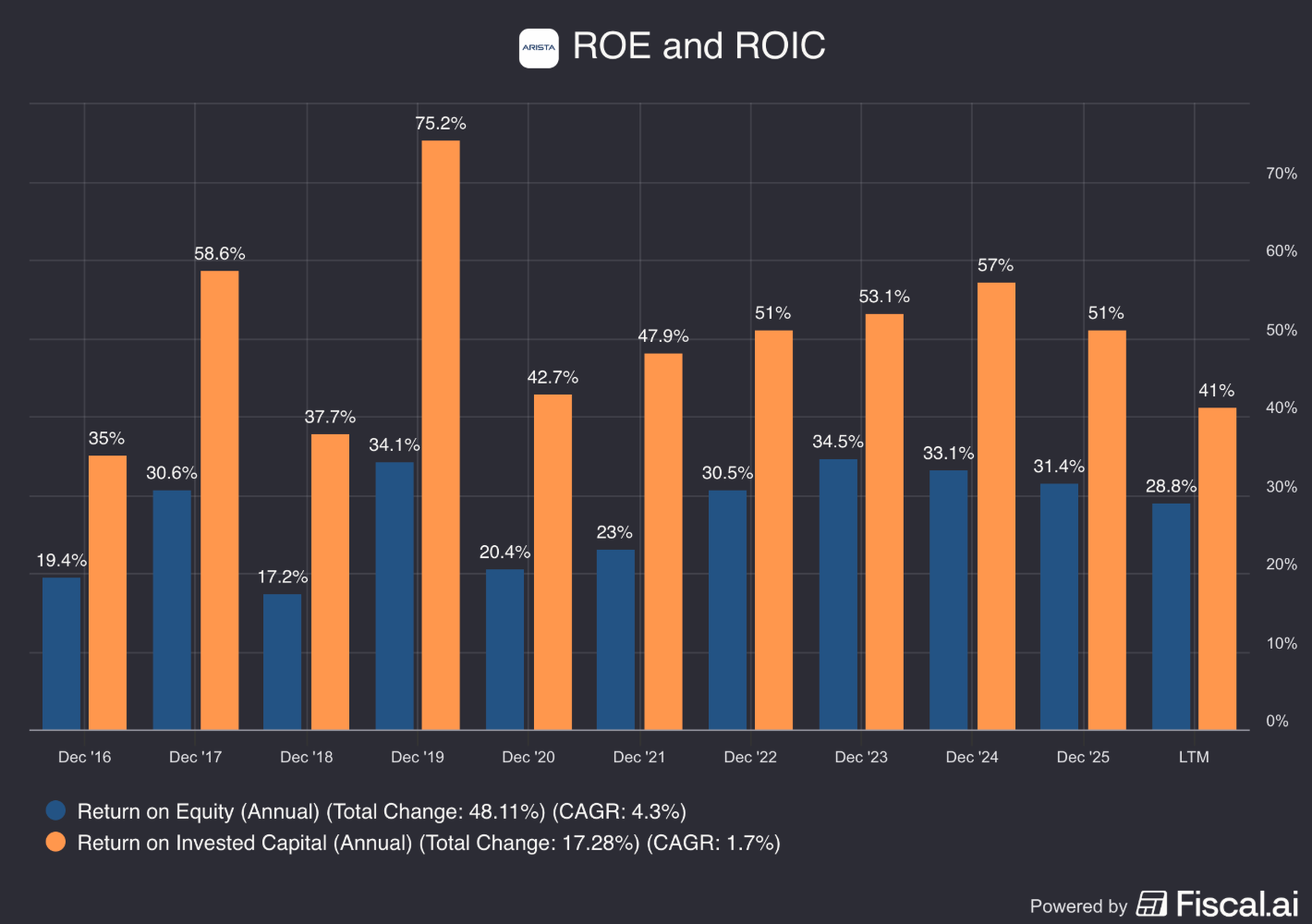

The 5Y avg. ROE (Return On Equity): 28.8% (ROE > 20%? ✅)

The 5Y avg. ROIC (Return On Invested Capital): 49.1%, (ROIC > 15%? ✅ )

These numbers look very attractive.

9. How profitable is the company?

The higher the profitability of the business, the better.

Arista Networks:

Gross Margin: 63.5% (Gross Margin > 40%? ✅)

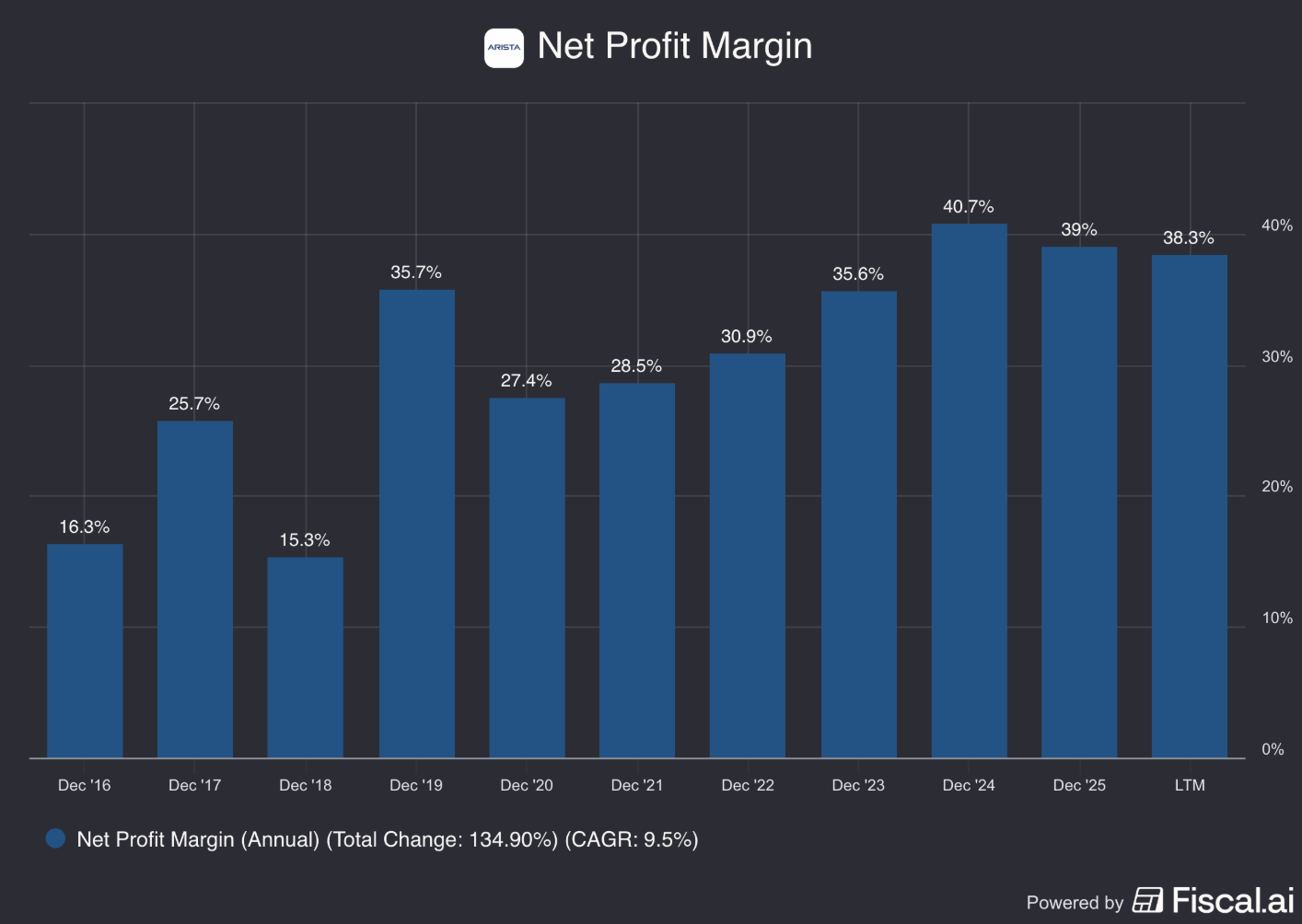

Net Profit Margin: 38.3% (Net Profit Margin > 10%? ✅)

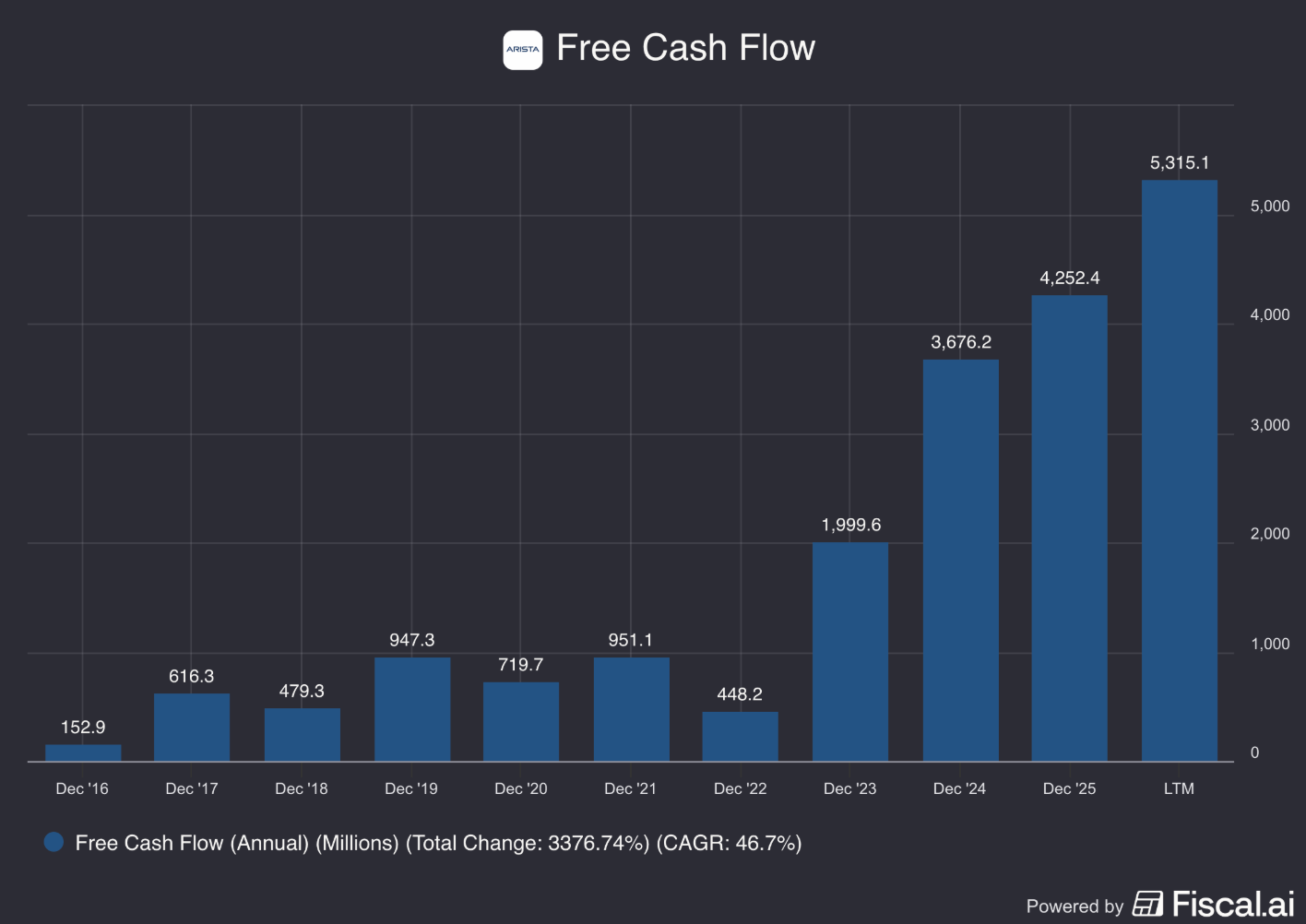

FCF/Net Income: 142.9% (FCF/Net income > 80%? ✅)

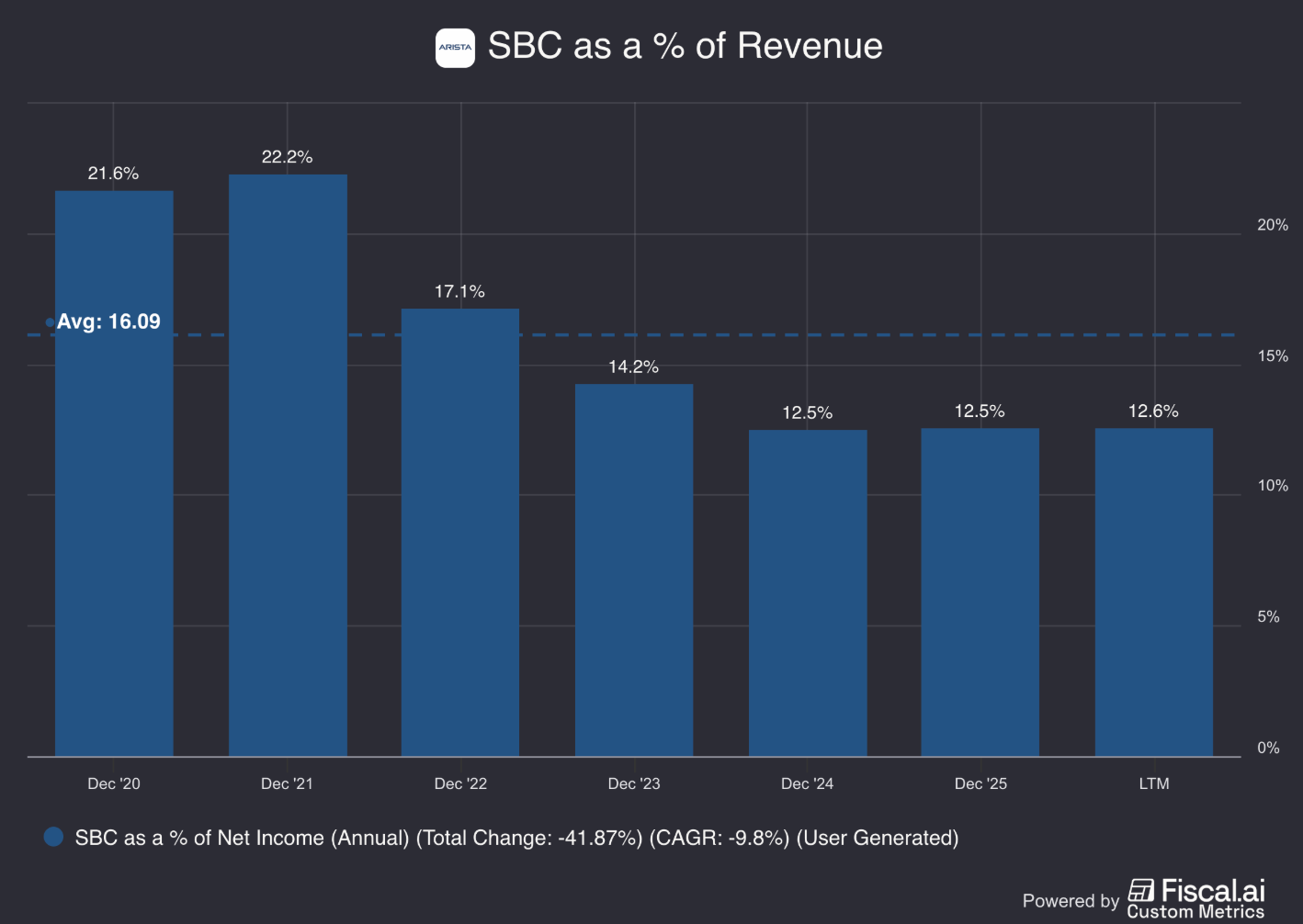

10. Does the company use a lot of Stock-Based Compensation?

Stocks-based compensation is a cost for shareholders and should be treated accordingly.

Preferably, we want SBCs as a % of Net Income to be lower than 10%.

SBCs as a % of Net Income: 12.6% (SBCs/Net income < 10%? ❌)

Avg. SBC as a % of Net Income past 5 years: 16.1% (SBCs/Net income < 10%? ❌)

Arista Networks uses quite some Stock-Based Compensation.

This is a red flag.

We will take this into account in our valuation section later.

11. Did the company grow at attractive rates in the past?

We look for companies that managed to grow their revenue and EPS by at least 5% and 7% per year respectively.

Arista Networks:

Revenue growth past 5 years (CAGR): 26.9% (Revenue growth > 5%? ✅)

Revenue growth past 10 years (CAGR): 24.0% (Revenue growth > 5%? ✅)

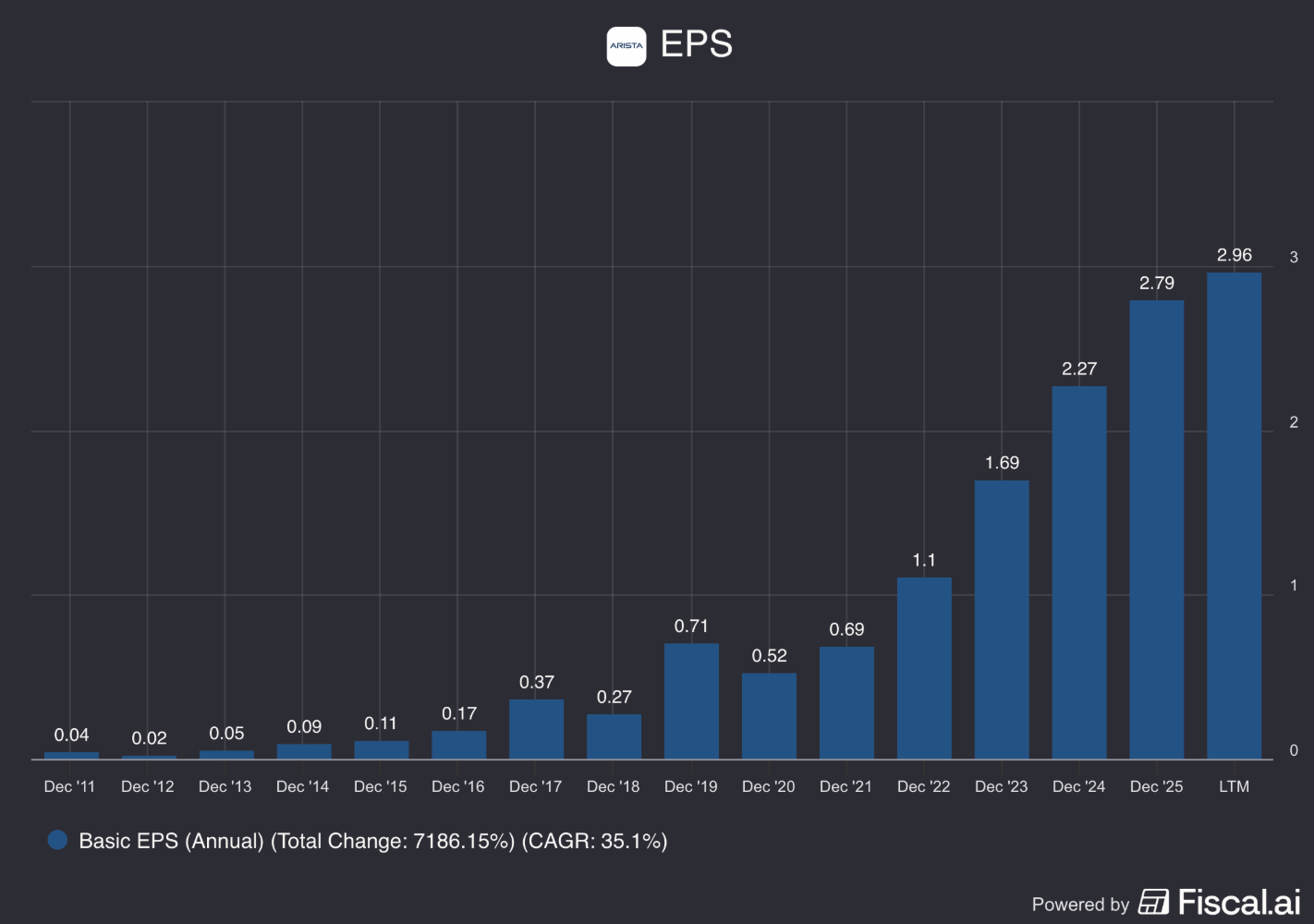

EPS growth past 5 years (CAGR): 34.6% (EPS growth > 7%? ✅)

EPS growth past 10 years (CAGR): 34.1% (EPS growth > 7%? ✅)

Arista Networks has grown at exceptional rates in the past, especially since its FCF growth has also been remarkable.

FCF-growth past 5 years (CAGR): 46.4% (FCF growth > 7%? ✅)

FCF-growth past 10 years (CAGR): 46.7% (FCF growth > 7%? ✅)

12. Does the future look bright?

We want to invest in companies with attractive growth.

Let’s look at what the estimates are for Arista Networks:

Exp. Revenue growth next 2 years (CAGR): 25.9% (Revenue growth > 5%? ✅)

Exp. EPS growth next 2 years (CAGR): 20.7% (EPS growth > 7%? ✅)

Long-term growth estimate EPS (CAGR): 18.5% (EPS growth > 7%? ✅)

This outlook looks very attractive.

But remember that making long-term predictions is very difficult, and analysts are often too optimistic.

13. Does the company trade at a fair valuation level?

We always use three methods to look at the valuation of a company:

A comparison of the Forward PE multiple with its historical average

Earnings Growth Model

Reverse Discounted-Cash Flow

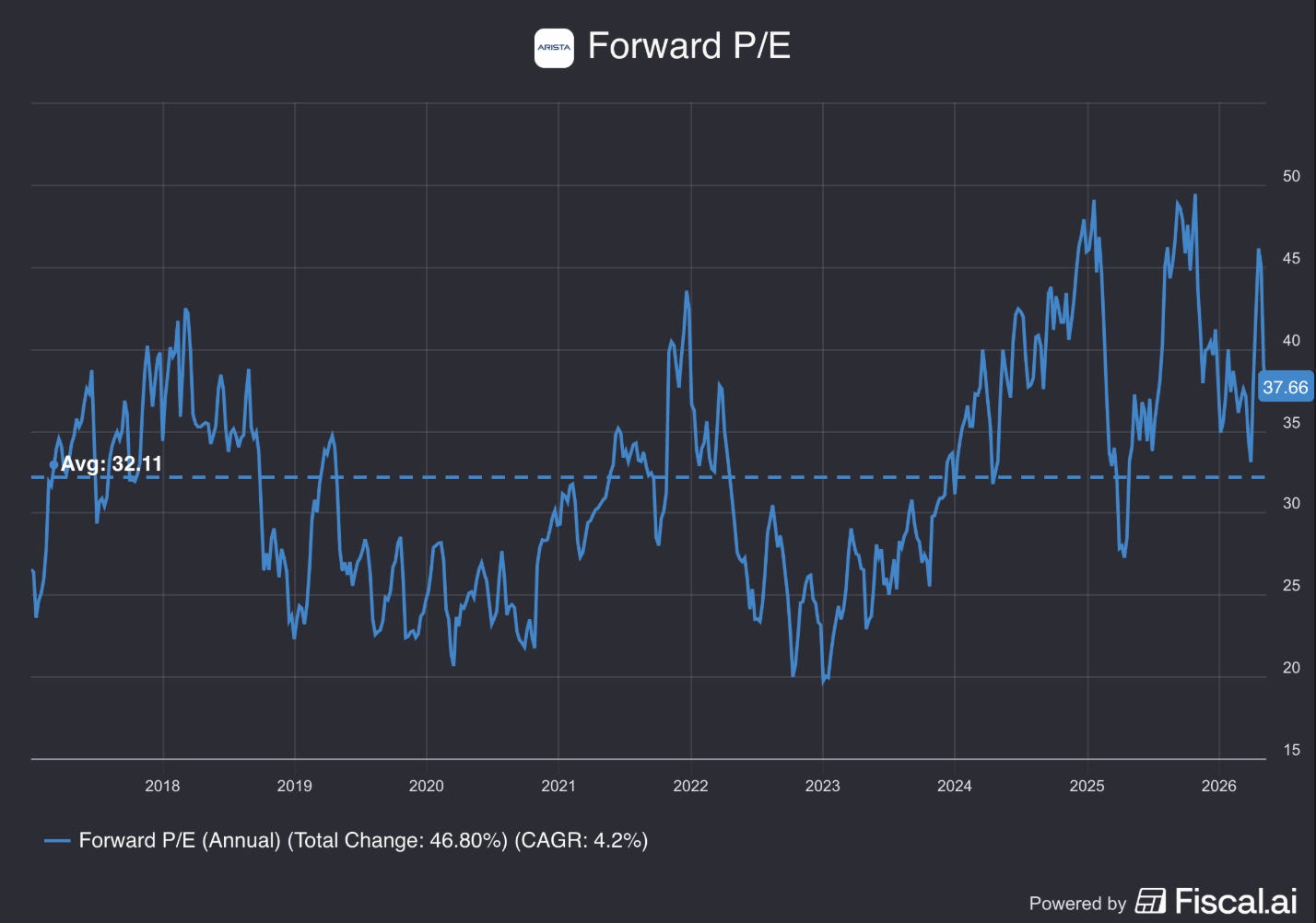

A comparison of the Forward PE multiple with its historical average.

The first thing we do is compare the current forward PE with its historical average over the past 10 years.

This is a shortsighted method, but it already gives a quick indication.

Today, Arista Networks trades at a forward PE of 37.7x compared to the historical average of 32.1x over the past ten years.

Earnings Growth Model

This model shows you the yearly return you can expect as an investor.

In theory, it’s easy to calculate your expected return:

Expected return = EPS growth + Dividend Yield +/- Multiple Expansion (Contraction)

Here are the assumptions I use:

EPS growth: 12.5% per year over the next 10 years

Dividend Yield: 0.0%

Forward PE to decline from 37.7X to 32.0x

Expected yearly return = 12.5% + 0% - 0.1* ((32.0-37.7)/37.7) = 11.0%

Based on these calculations, the expected return is 11.0% per year.

This looks very good.

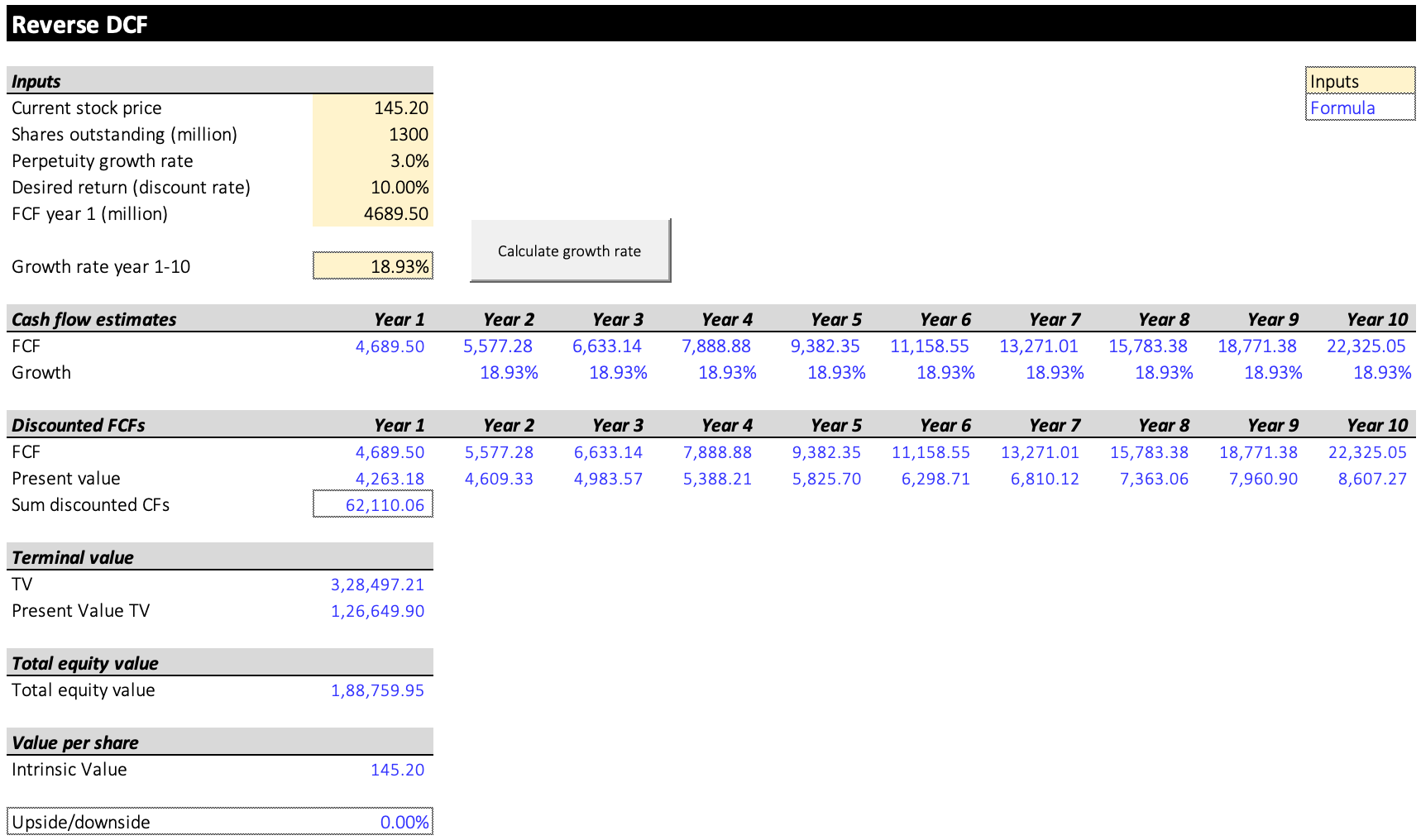

Reverse DCF

Charlie Munger once said that if you want to find a solution to a complex problem, you should invert. Always invert. Turn the problem upside down.

This is exactly what a reverse DCF does. As an investor, we don’t make assumptions. We simply look at what assumptions the market has made and see whether they are reasonable.

You try to determine for yourself whether these expectations are realistic or not.

You can learn more about a reverse DCF here: Reverse DCF 101.

The expected Free Cash Flow of Arista Networks over the next 12 months equals $5,130.0 million.

We subtract the Stock-Based Compensation ($467.0 million) and add the Growth CAPEX ($26.5 million).

Growth CAPEX is calculated by subtracting Depreciation & Amortization from total CAPEX, helping to separate investment spending from maintenance costs.

This brings the FCF in year 1 to $4,689.5 million

The reverse DCF indicates that Arista should grow its FCF by 18.9% each year for the coming 10 years to achieve an annual return of 10% for shareholders.

Although Arista Networks grew Free Cash Flow at a 46.7% CAGR over the past decade, it’s uncertain if this growth rate can be sustained.

Forward PE: 37.7x (lower than its 10-year average? < 32.1x? ❌)

Earnings Growth Model: 11.0% (Yearly return > 10%? ✅)

FCF-Growth Reverse DCF: 18.9% (Realistic growth expectations?❓)

14. How did the Owner’s Earnings of the company evolve in the past?

Over time, stock prices tend to follow the Owner’s Earnings (EPS Growth + Dividend Yield) of the company.

That’s why we want to invest in companies that managed to grow their Owner’s Earnings at attractive rates in the past.

This is certainly the case for Arista:

CAGR Owner’s Earnings (5 years): 34.6% (CAGR Owner’s Earnings > 12%? ✅)

CAGR Owner’s Earnings (10 years): 34.1% (CAGR Owner’s Earnings > 12%? ✅ )

15. Did the company create a lot of shareholder value in the past?

We want to invest in companies that managed to compound at attractive rates in the past.

Ideally, the company returned more than 12% per year to shareholders since its IPO.

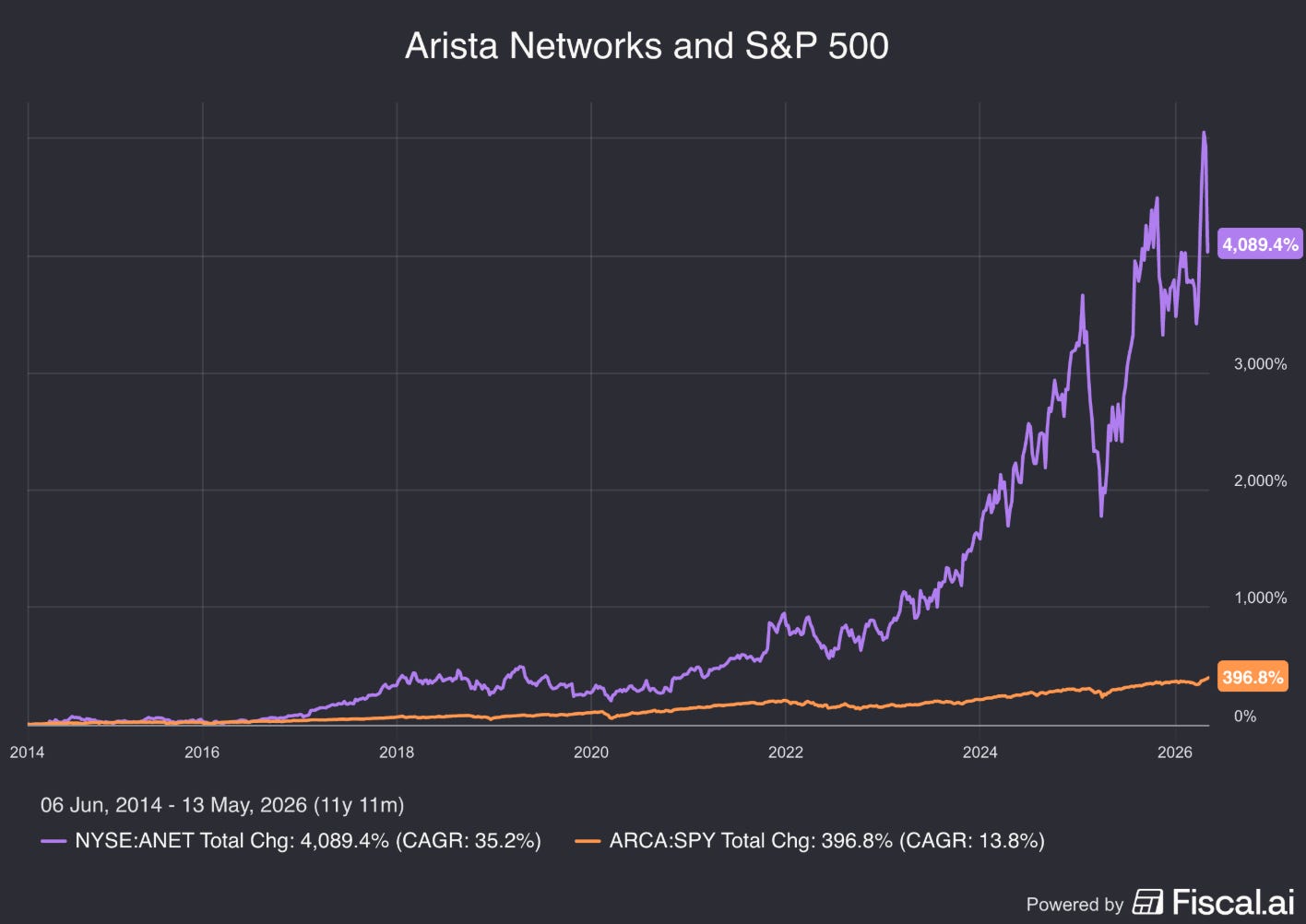

Here’s what the performance of Arista Networks looks like:

YTD: +5.3%

5-year CAGR: 48.6%

CAGR since IPO (2014): 36.7% (CAGR > 12% ✅)

Arista Networks has created significant shareholder value in the past.

Now let’s dive into the conclusion.

Should you buy Arista Networks?