ETF Portfolio Update: An S&P 500 Alternative From Omaha

Do you own an S&P 500 ETF?

You must realize that you are way less diversified than you might think.

Let’s talk about an interesting S&P 500 alternative I heard about at Warren Buffett’s AGM.

The S&P 500

The S&P 500 is the most popular index in the world.

It’s also incredibly popular with passive investors.

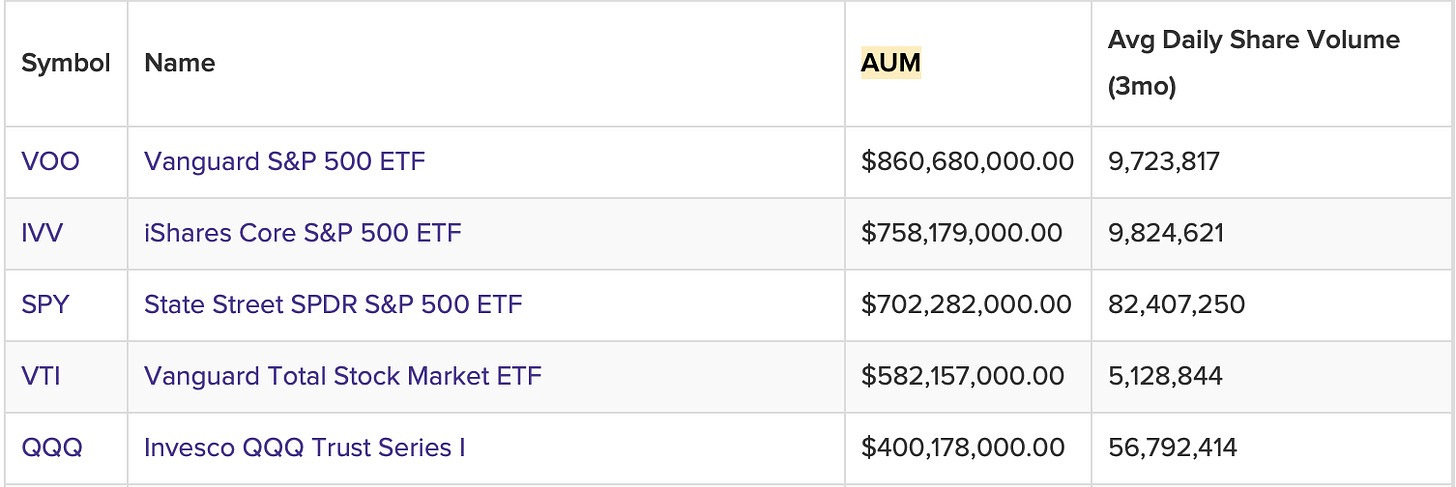

The three largest ETFs in the world all track the S&P 500:

Together, they have more than $2 Trillion (!) in assets.

But when I was in Omaha last weekend, some concerns kept coming up again and again.

The S&P 500 Is Expensive

The price you pay matters.

“The price you pay for an investment determines its risk. The lower the price, the lower the risk and the higher the potential return.” - Seth Klarman, Margin of Safety

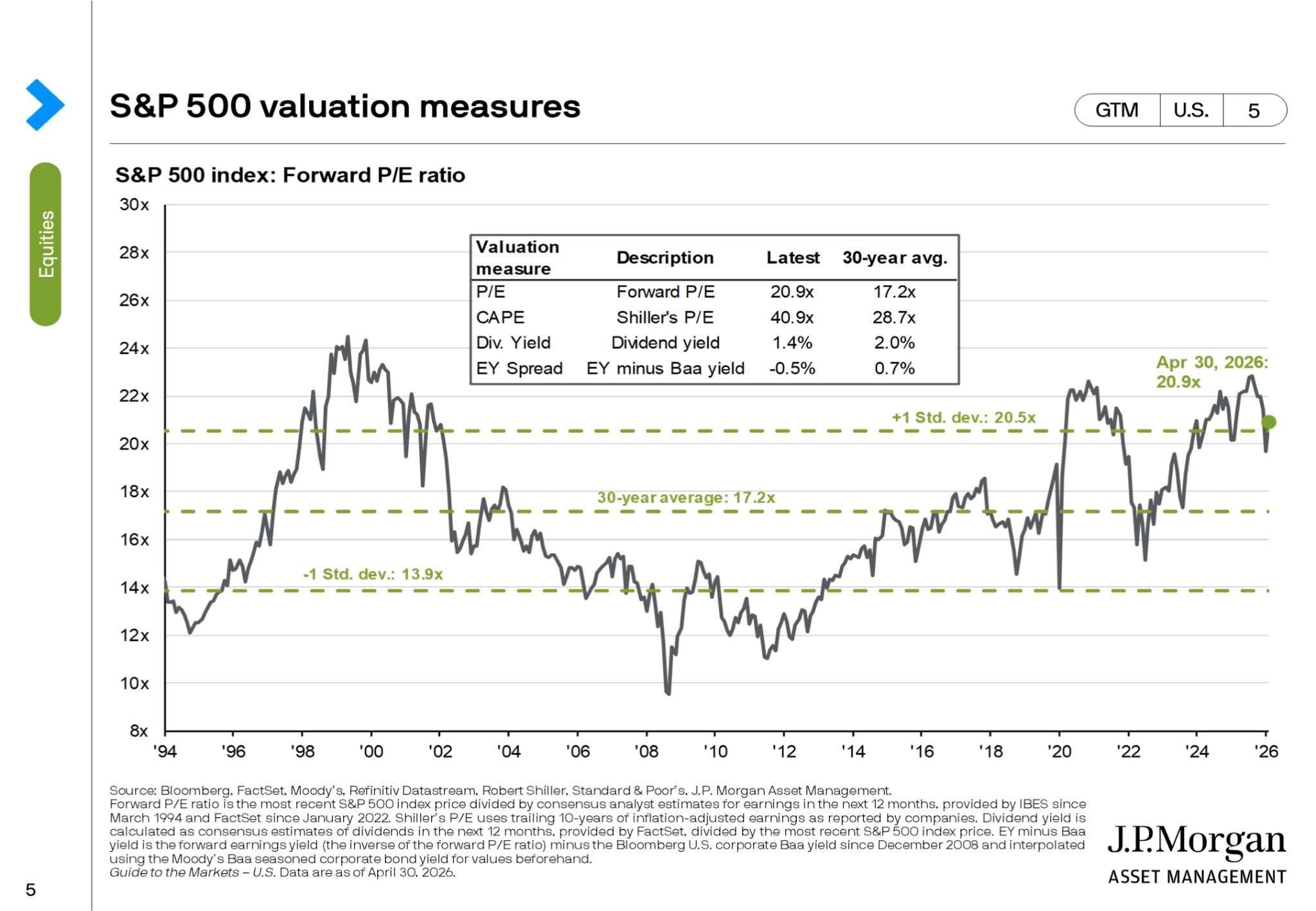

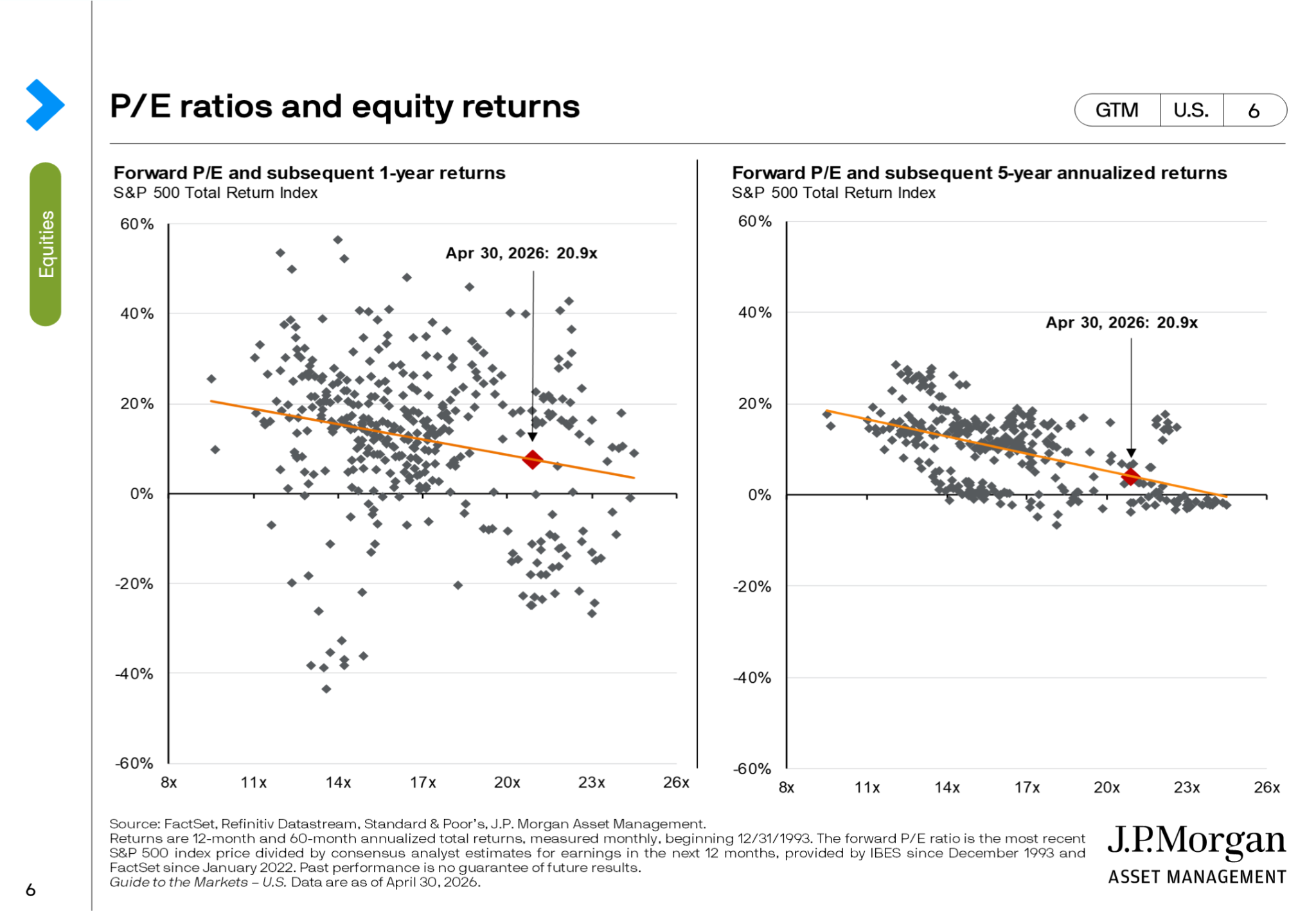

The S&P 500 index looks expensive today.

The Shiller P/E Ratio, also called the CAPE Ratio, compares a stock’s current price to its average inflation-adjusted earnings over the past 10 years.

Using 10 years of earnings helps smooth out short-term market ups and downs that can distort regular one-year P/E ratios.

Right now, it’s over 40.

It approaches the valuation we saw before the 2000s dot com crash.

The S&P 500 doesn’t look like much of a bargain on a Forward P/E basis either.

The S&P 500 Is Concentrated

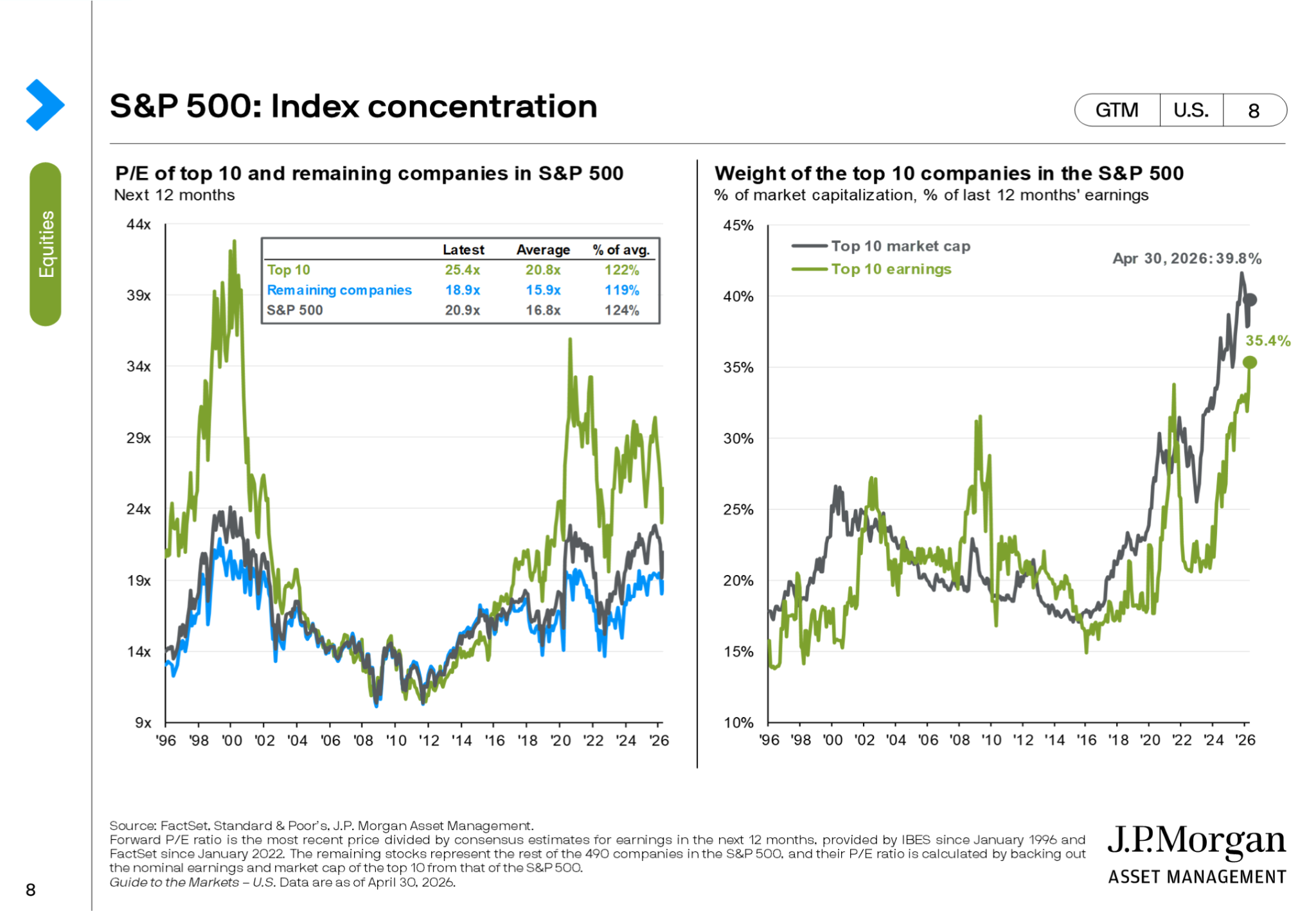

Another concern that came up over and over is the concentration in the S&P 500 index.

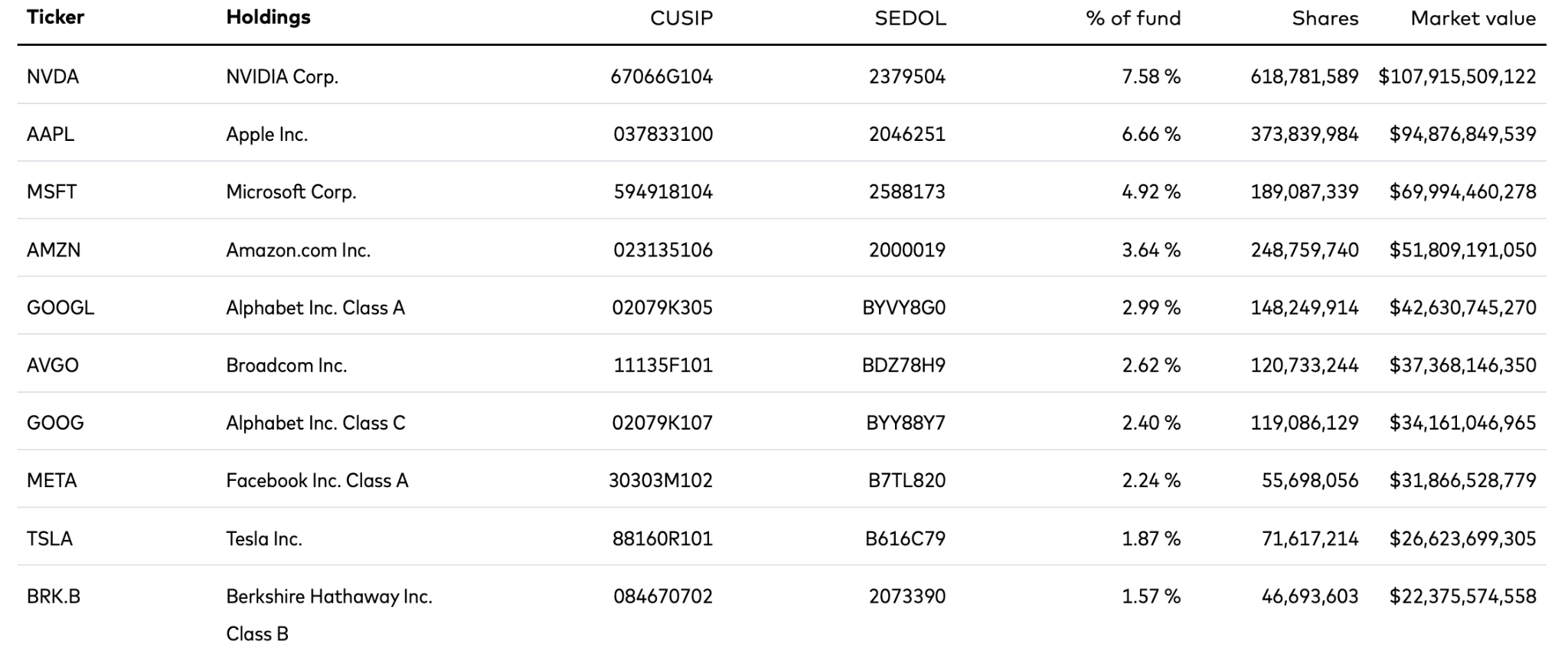

Because it is weighted by market cap, the top 10 companies make up nearly 40% of the index.

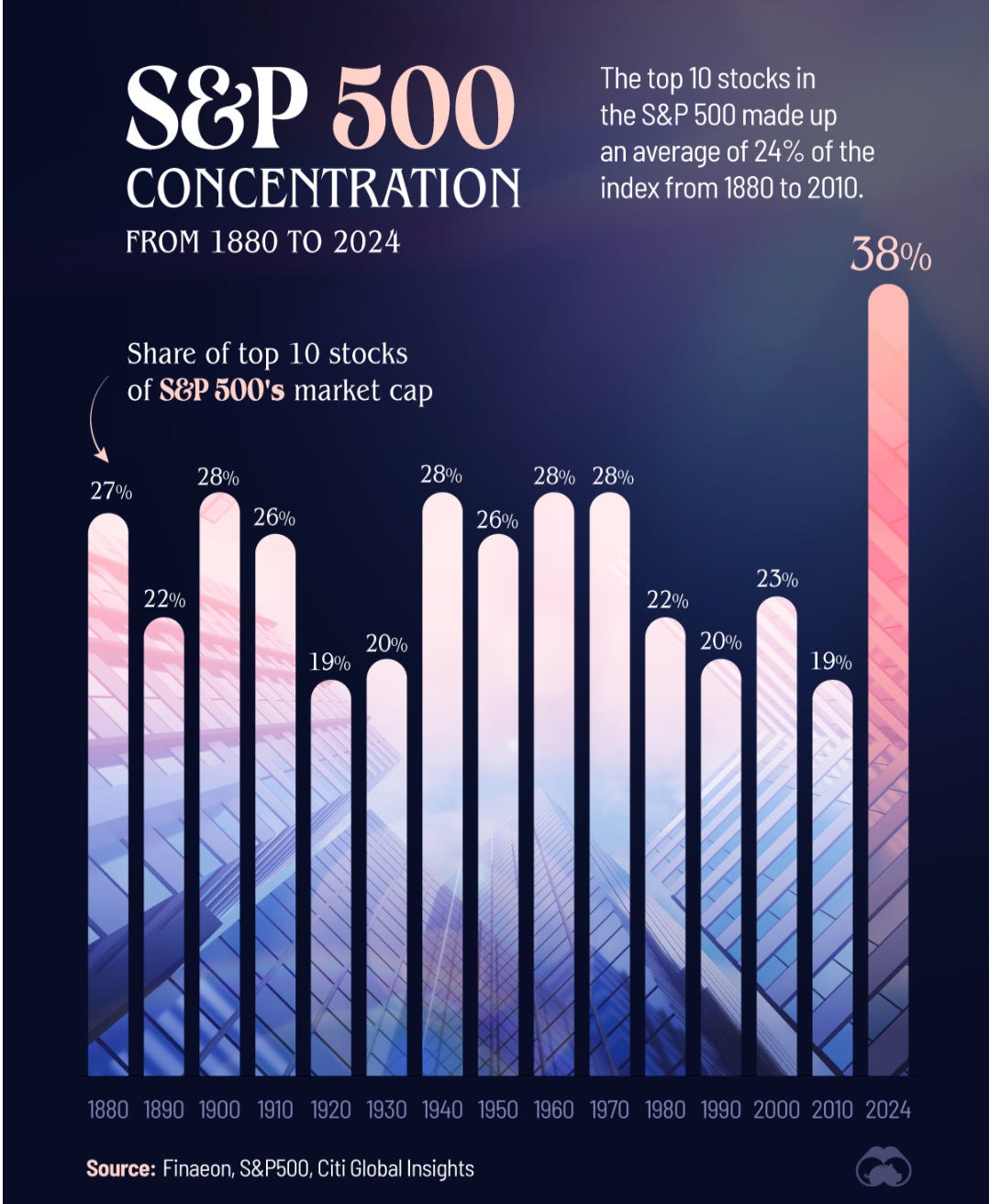

Over the past 140 years, the average concentration for the top 10 stocks was 24%.

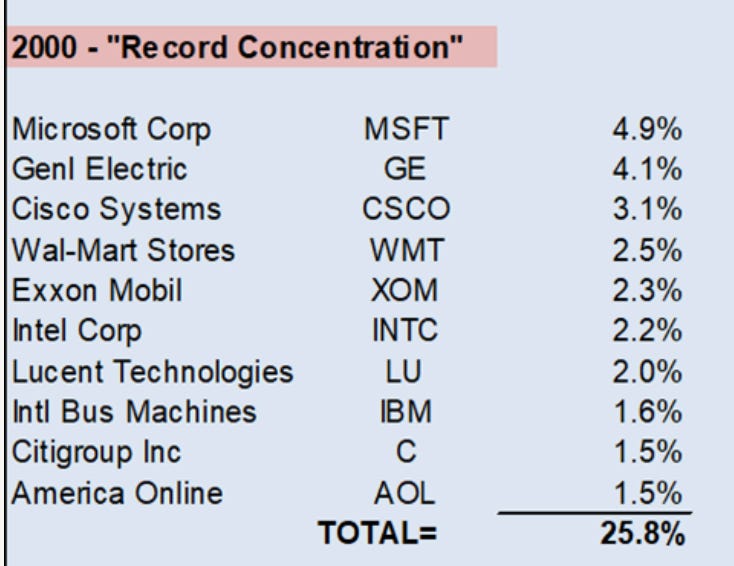

The index concentration has (almost) never been higher:

But in Omaha, Christopher Bloomstran pointed out something interesting.

In the past, even when the index was concentrated, the companies were usually not all tied to the same trend or idea.

For example, the “Nifty Fifty” stocks of the 1960s made the index more concentrated, but the companies operated in different industries.

They included names like IBM, Coca‑Cola, Xerox, and Polaroid.

Even in 2000, not all the companies were internet companies:

Companies like Walmart, Exxon Mobil, and Citigroup had nothing to do with the internet boom.

Today’s top 10 stocks are much more connected to the same trend.

8 of the 10 are now related to Artificial Intelligence.

The math behind AI spending is not very encouraging.

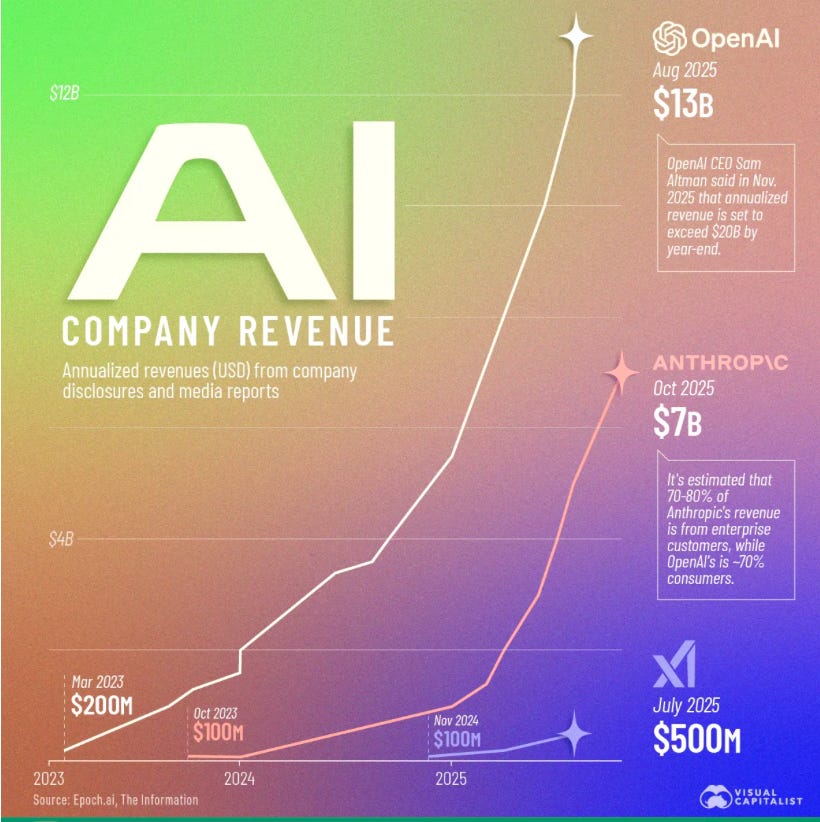

The hyperscalers are expected to spend $700 billion on AI infrastructure in 2026 alone.

To earn a 10% return, they would need to generate $70 billion in profit from that investment.

AI revenue is growing quickly, but it still is very early in the journey.

All AI-related revenue was estimated at only about $40 billion in 2025.

If AI businesses earn a 10% profit margin, they would need $700 billion in revenue to generate a 10% return on that spending.

This raises an interesting question…

Why Do Investors Buy The Index?

The S&P 500 does have some really attractive features that make it such a popular investment.

Diversification: you get a piece of 500 of the best companies in the world

Low costs: most index funds cost less than 0.5% to own

It lets winners run, and losers drop out: Peter Lynch’s idea of watering the flowers and cutting the weeds happens automatically

It’s performed well over the long-term

These are great reasons to invest in the S&P 500, but as you have just seen, the index isn’t as diversified as it once was.

And as every disclaimer says, past performance is not a guarantee of future results.

Based on valuation alone, the future returns of the S&P 500 look much lower than they have been in recent years.

When you combine high valuations with the difficult math behind earning strong returns on AI spending, future returns start to look even less attractive.

It would be ideal to get the benefits of the S&P 500 at a lower price and with less concentration in AI-related companies.

Interestingly, several investors in Omaha presented ideas for exactly that kind of investment.

The S&P 500 Alternative

Investing in Berkshire Hathaway could be a very interesting alternative to the S&P 500.

Here are a few reasons why:

Diversification

Low cost

Let your winners run

Amazing returns

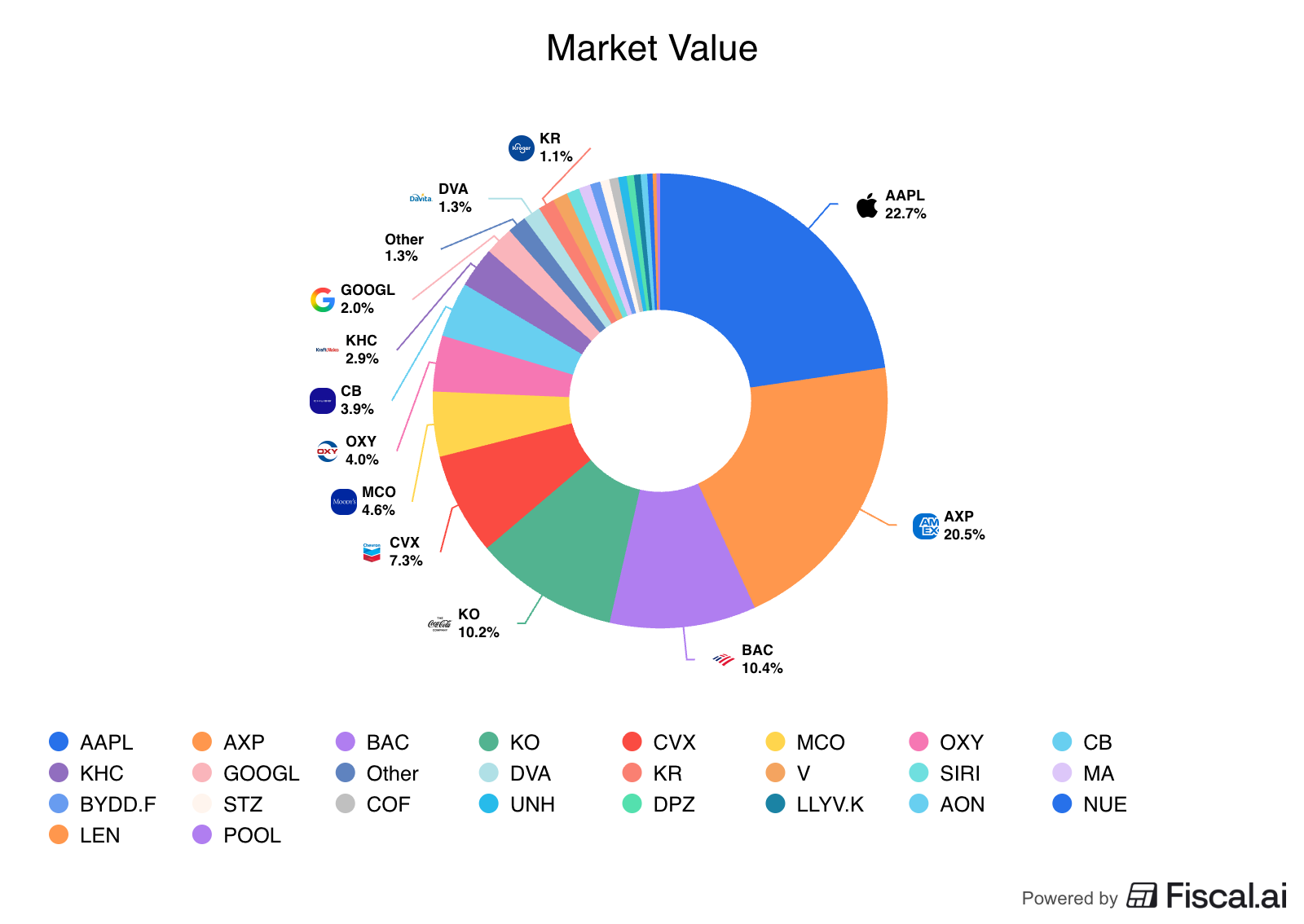

Diversification

Berkshire Hathaway gives you ownership in 26 public companies through its stock portfolio.

It also includes more than 60 private companies that are fully owned by Berkshire.

Those include names like:

BNSF Railroad

Dairy Queen

Clayton Homes

GEICO

NetJets

Duracell

Fruit of the Loom

…

On top of that, they also have the massive insurance operation as well as Berkshire Hathaway Energy.

I would say that Berkshire Hathaway is very well diversified.

Low Cost

This one is easy …

While the fees to own an S&P 500 ETF are very low, there are no management fees to own Berkshire Hathaway stock.

Let Your Winners Run

Warren Buffett has said many times that his favorite holding period is forever.

When Berkshire Hathaway buys something it does so with the intent of holding on for the long term.

Warren Buffett started buying Coca-Cola in 1988.

See’s Candies was bought in 1972.

Both companies have performed exceptionally well for Berkshire Hathaway.

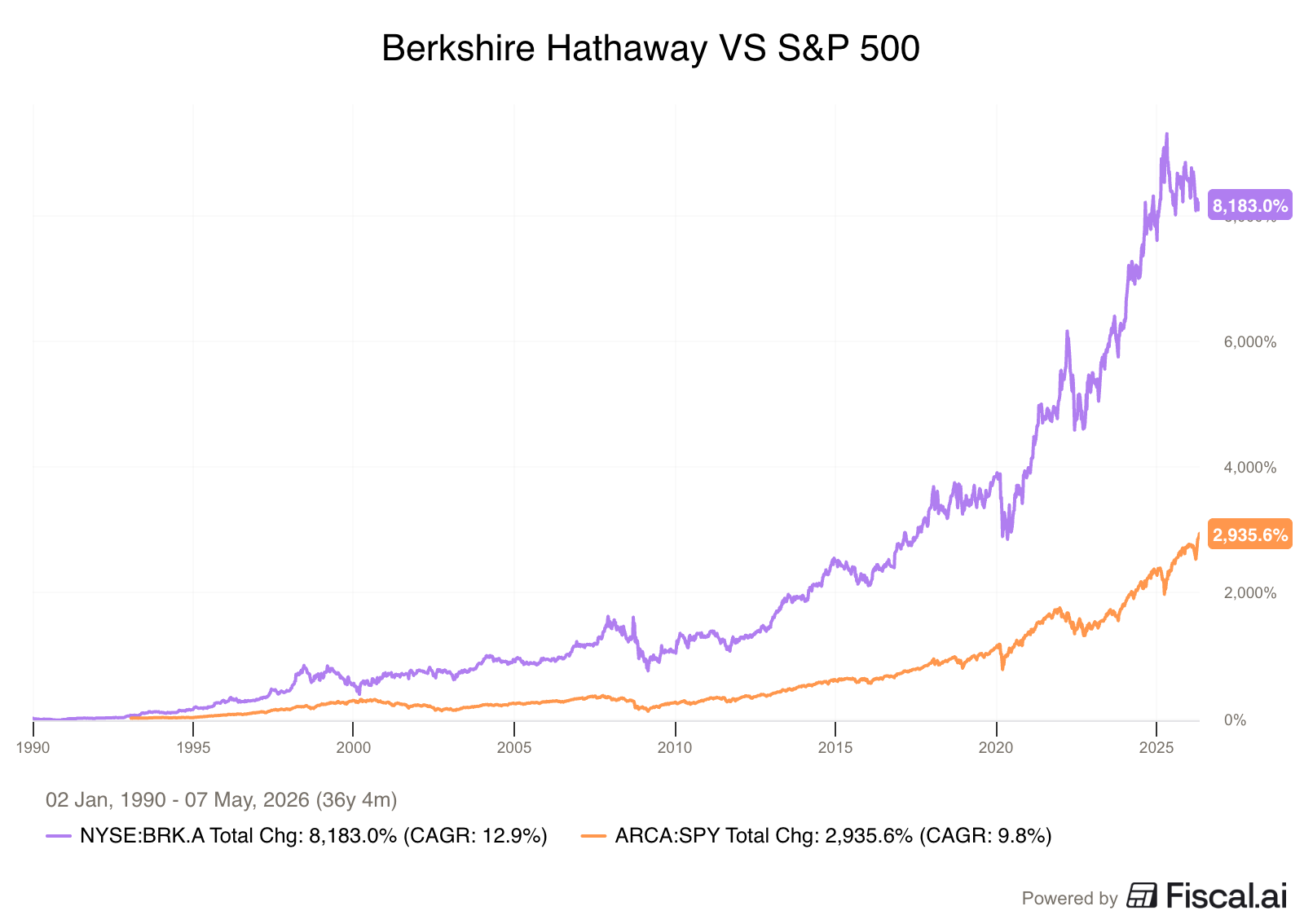

Past Performance

Another easy one.

Over the long-term, Berkshire Hathaway has performed significantly better than the S&P 500.

When you buy Berkshire Hathaway, you get a diversified bet on the American economy.

They have performed really well and have a lot of cash on the sidelines to deploy when the market crashes.

In addition, it’s not one big bet on AI.

They own a lot of companies that are hard for AI to disrupt.

Think about their railroad companies, energy, Clayton Homes, …

You get Greg Abel allocating capital for you.

The man Warren Buffett picked himself.

Berkshire is also available at a much more reasonable valuation than the S&P 500.

We know that Greg Abel thinks Berkshire Hathaway is undervalued, as he started buying back the stock.

Christopher Bloomstran estimates Berkshire Hathaway B shares to be worth between $560 and $580 in his most recent letter (current stock price: $475).

Berkshire has more than $300 billion in cash to deploy when attractive opportunities arise.

If you want a diversified U.S. investment that isn’t tied to big tech and AI, Berkshire Hathaway is an interesting idea.

ETF Portfolio Update: April 2026

Our ETF Portfolio is a great mix of ETFs that should be able to outperform in the long term.

We use multiple factors that tend to do well:

👑 Quality: Only invest in companies that have already won

📏 Size: The smaller the better

🚀 Multifactor: Quality, size, value & momentum

🌏 Emerging Markets: Small exposure to Emerging Markets

Let’s now dive into the ETF Portfolio itself.

You have 24/7 access to the ETF Portfolio here: