🏦 Are we buying KKR?

Hi Partner 👋

Today, you will receive a full investment case of 50 (!) pages about KKR

This is a wonderful company that definitely deserves your attention.

Happy reading!

KKR & Co - General Information

👔 Company name: KKR & Co. Inc.

✍️ ISIN: US48251W1045

🔎 Ticker: KKR

📚 Type: Owner-Operator Stock

📈 Stock Price: $97

💵 Market cap: $87.0 billion

📊 Average daily volume: $595.0 million

Onepager

Here are the basics of KKR (click on the picture to expand)

Three main takeaways

Here are the 3 important takeaways:

🏦 KKR is one of the largest asset managers in the world

♾️ Thanks to its insurance activities, KKR enjoys “permanent capital”

🏆 Excellent track record

🏦 One of the largest asset managers in the world

KKR is one of the world's largest alternative asset managers:

♾️ Permanent Capital Advantage

KKR has $219 billion in permanent capital through Global Atlantic.

Permanent capital is the money from insurance premiums that KKR can invest for decades before it needs to be paid out as claims.

This gives them flexibility to pursue opportunities whenever they arise.

🏆 Excellent Track record

KKR has an excellent track record.

The stock is up +870% (!) since 2010.

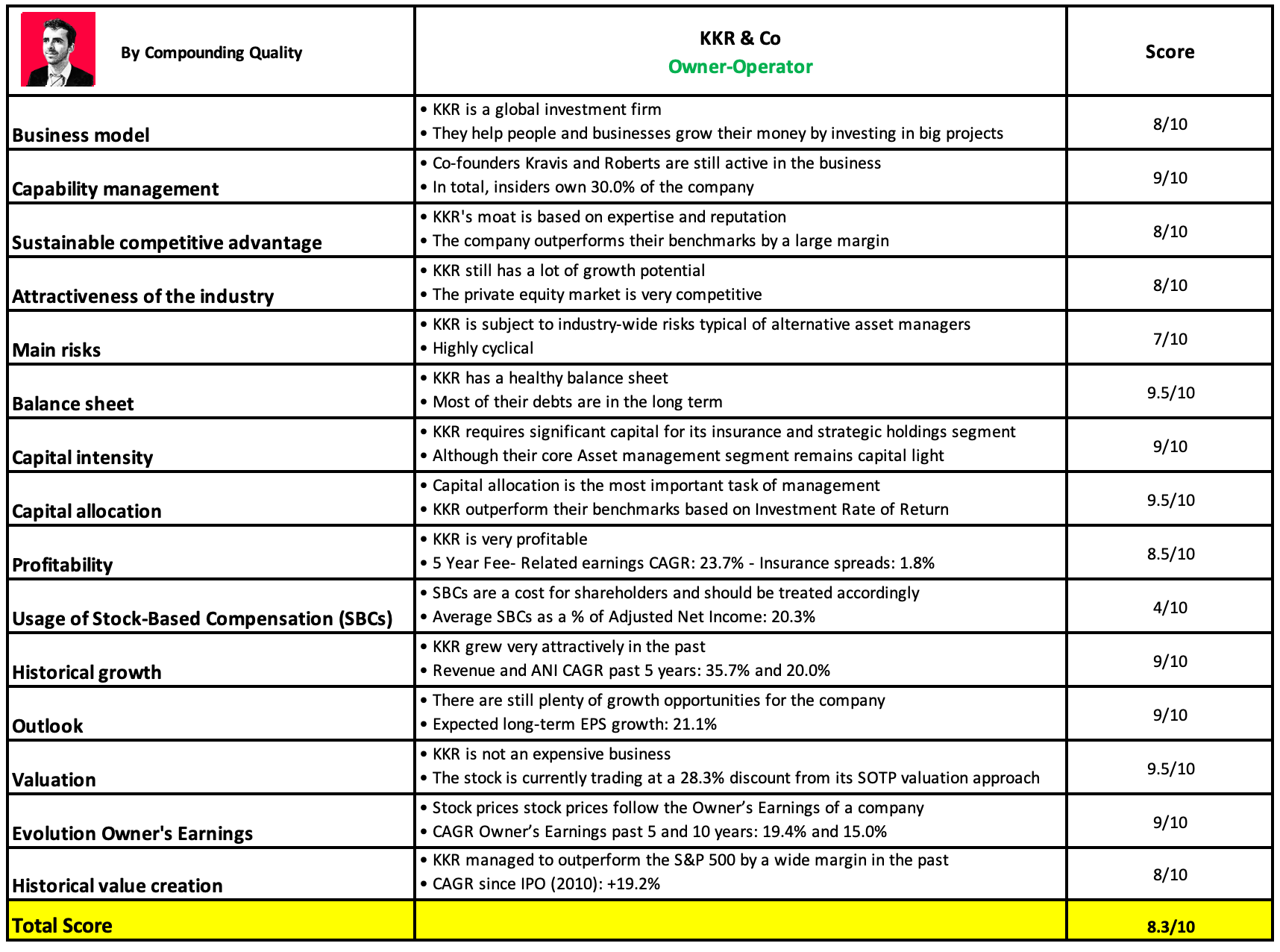

Quality Score

Every company gets a Quality Score based on 15 metrics.

Finally, the company gets a ‘Total Quality Score’ which is calculated by taking the sum of the score of all 15 metrics and dividing it by 15.

As you can see in the table below KKR gets a Total Quality Score of 8.3/10.

Full Investment Case

We wrote a 50-page deep dive about KKR.

You can download it here:

Conclusion investment case

You don’t want to read the entire investment case?

You can just read the conclusion instead.

KKR started as a private equity firm in the 1970s.

Today it manages $744 billion across three businesses:

Asset Management: Earns fee income from managing money

Insurance (through Global Atlantic): Takes in premiums and invests them

Strategic Holdings: Compounds value through their investments and dividends

The three businesses work together supporting the businesses as a whole.

Global Atlantic brings in premiums that need to be invested.

KKR invests that capital into private credit, infrastructure, and real assets.

This means KKR always has capital to deploy, unlike most competitors who raise fixed ten-year funds and return the money. We call this Permanent capital.

At $744 billion in AUM, KKR can do deals that most competitors cannot.

They have been doing this for nearly 50 years, which is why CEOs and pension funds choose KKR over newer entrants.

The markets KKR operates in are growing fast.

Alternative assets, private credit, and insurance are all expanding, and banks pulling back from direct lending after 2008 only accelerated that shift.

KKR was positioned to fill that gap and has been doing so ever since.

The business is still in growth mode.

Revenue, fee earnings, and net income have all compounded at strong double digit rates over the past five years.

On top of this, KKR raised nearly twice as much capital in 2025 as it did in 2023.

The balance sheet is stronger than it looks.

The headline debt figure is mostly non-recourse debt sitting inside separate funds, meaning lenders have no claim on KKR itself.

Direct corporate debt is manageable, cash is healthy, and book value has compounded at a strong rate since 2015.

But the most important risk?

Stock-based compensation

This is very high relative to their net income. But unfortunately this is an industry wide practice.

The leadership is experienced and has skin in the game. Founders Kravis and Roberts are still involved.

Co-CEOs Bae and Nuttall have been at the firm for 30 years each. Insiders own 30% of the company, which is far above the industry norm.

The growth targets are clear. Management wants to double earnings in five years.

The retail K-Series funds more than doubled in AUM in 2025 alone, opening up an entirely new pool of individual investor capital.

The Arctos acquisition adds sports investing and brings KKR closer to $1 trillion in AUM.

On valuation, the stock trades well below its own historical range and below every major peer.

A sum-of-the-parts analysis puts fair value at $133 per share which is significantly above its current market price.

But the real question is…

Are we buying it?

The answer is…