📈 Is L'Oréal an interesting stock?

You're worth it

L’Oréal is a French company active in the beauty segment.

They sell cosmetic products for women and men worldwide. Think about skincare, makeup and much more.

But is it an interesting stock? Let’s find out today.

L’Oréal - General Information

👔 Company name: L’Oréal

✍️ ISIN: FR0000120321

🔎 Ticker: OR

📚 Type: Owner-Operator

📈 Stock Price: €367.4

💵 Market cap: €184.8B

📊 Average daily volume: €144.6M

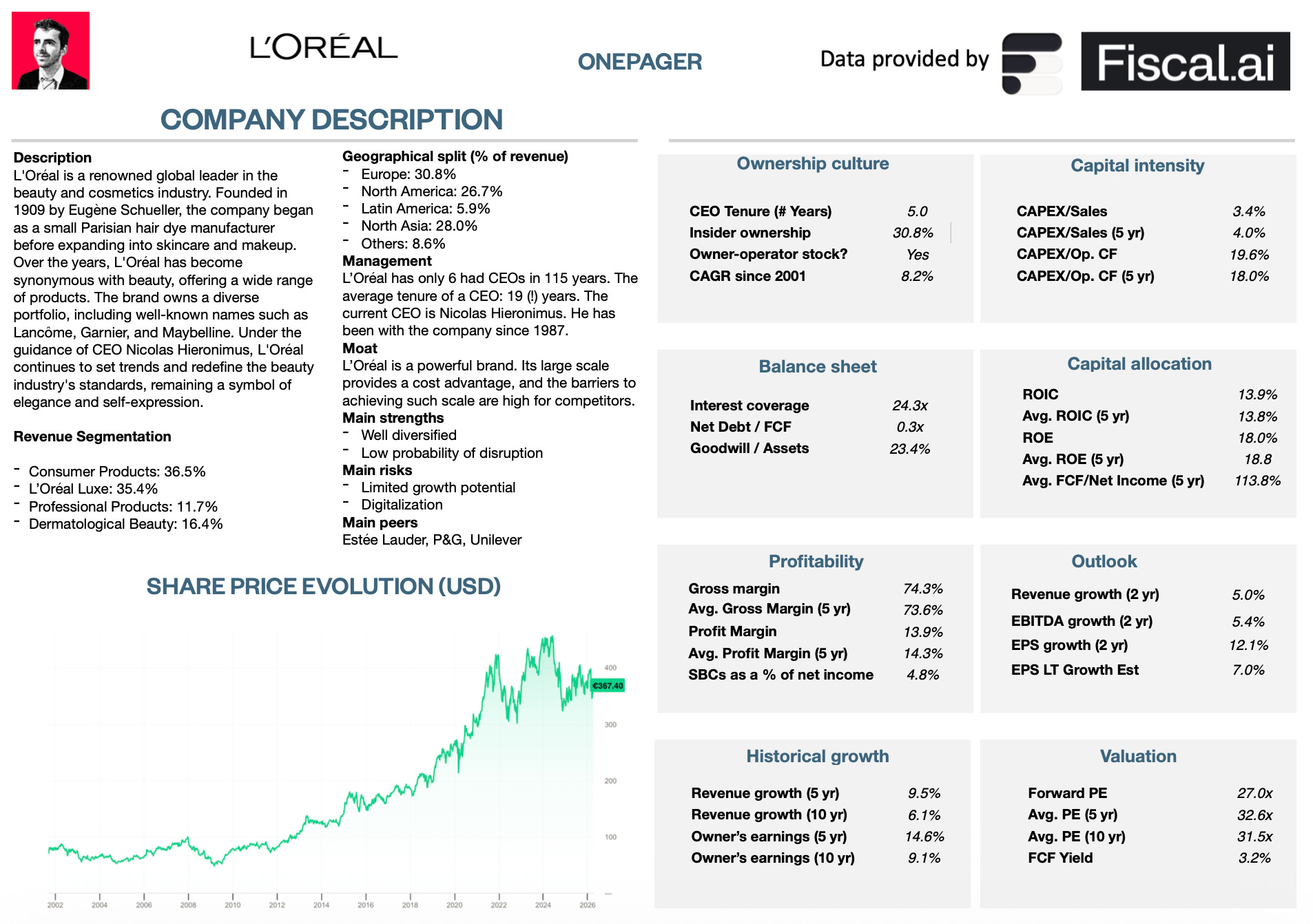

Onepager

Here’s a onepager with the essentials of L’Oréal

15-Step Approach

Now let’s use our 15-step approach to analyze the company.

At the end of this article, we’ll give L’Oréal a score on each of these 15 metrics.

This results in a Total Quality Score.

1. Do I understand the business model?

The company behind your favorite beauty essentials?

Go take a look in your bathroom and you’ll see it’s probably L’Oréal.

They’re all about making us feel good.

L’Oréal sells beauty and confidence with their iconic products.

And they do it through 37 brands in 150 countries.

Here’s a sneak peek at some of their products:

Maybelline New York

Garnier

Lancôme

L’Oréal Paris

L’Oréal is the number 1 beauty company worldwide.

Their market share equals approximately 14.5%.

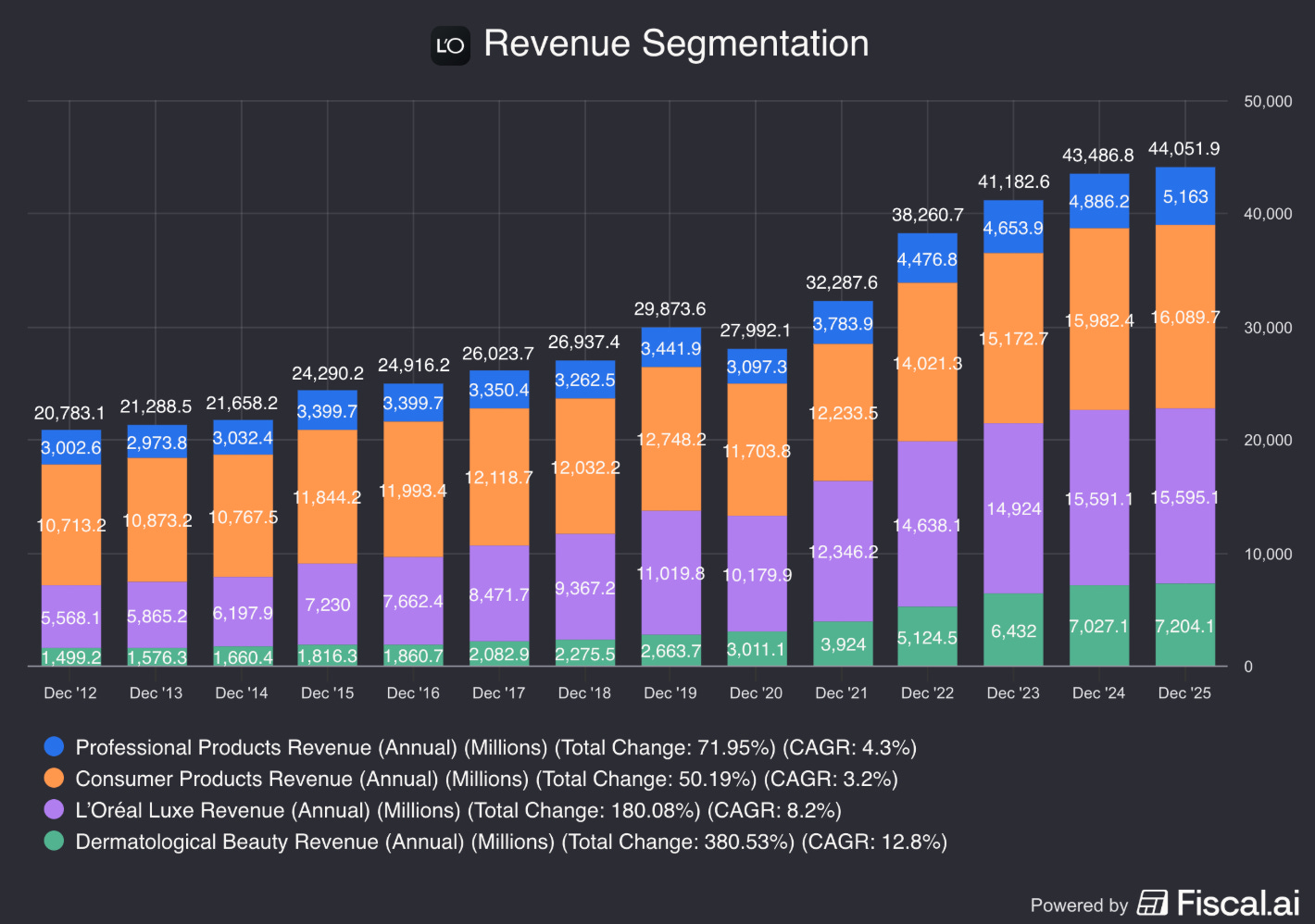

The company is active in four different segments:

Consumer Products (36.5%): You’re likely already familiar with these products. You can find L’Oréal’s consumer products in stores like Sephora or Ulta Beauty

L’Oréal Luxe (35.4%): L’Oréal works with high luxury brands such as Giorgio Armani and Prada through licenses

Professional Products (11.7%): Products directly sold to hairstylists

Dermatological beauty (16.4%): Sells medical-grade skincare products

L’Oréal is very well diversified in all aspects:

2. Is management capable?

Do you know the average tenure of a CEO? It’s 8.1 years.

L’Oréal does it differently.

In its long history of 115 (!) years, they only had 6 CEOs.

That’s 19 years on average per CEO. This is an indication of the stability and strong culture of the business.

The current CEO is Nicolas Hieronimus. He started at L’Oréal in 1987.

Nicolas is a manager who is actively working on the future.

He even has a team researching skin aging in space.

He might have stolen this idea from Leonard Lauder, the son of Estée Lauder, who said the following:

Think in decades, not quarters.

The Frenchman owns €87.2 million worth of shares.

But there’s an even bigger insider. A way bigger one.

It’s Françoise Bettencourt.

She still owns over 29.5% of the business which makes her the second richest woman in the world.

Her estimated net worth is $91.3 billion. She is active on the Board of Directors.

She owns a large share of L’Oréal, inherited from her mother, Liliane Bettencourt, whose father founded the company.

3. Does the company have a sustainable competitive advantage?

“I love a big castle and a big moat with piranhas and crocodiles.” - Warren Buffett

L’Oréal has very strong brands.

People spot their products right away on the store shelves.

However, there’s an important nuance there.

Year after year, L’Oréal spends roughly 32% of its revenue on advertising and promotion expenses.

It makes you wonder what is doing the heavy lifting: the brand or the advertising?

The piranhas are its high barriers to scale.

It’s not so hard to get some local market share but it takes decades to come to the scale that’s relevant to compete with L’Oréal.

And don’t forget the crocodiles. These are L’Oréal’s cost advantages.

Its large scale lets it make products way cheaper than small competitors.

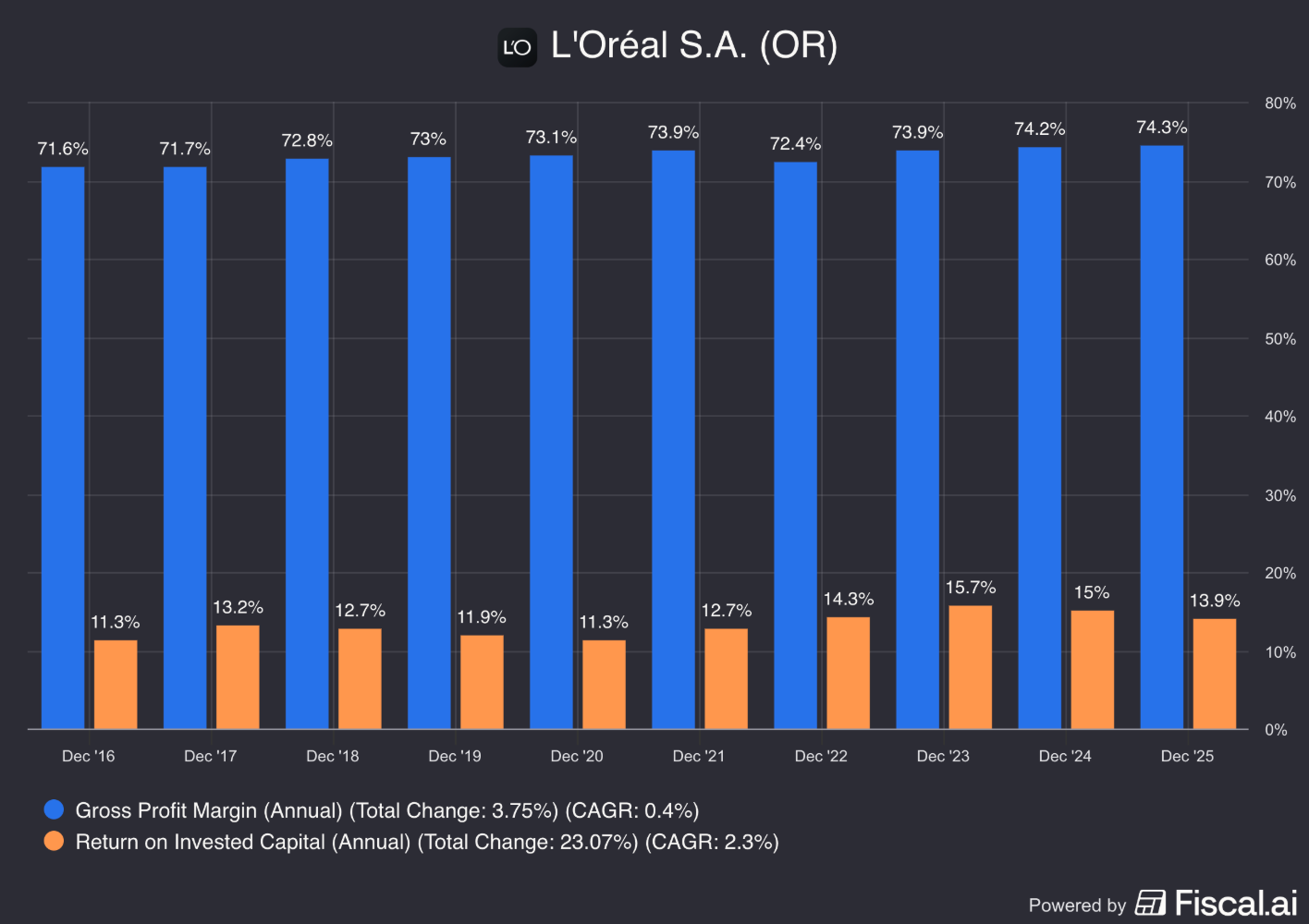

Companies with a sustainable competitive advantage are often characterized by the following:

Gross Margin: 74.3% (Gross Margin > 40%? ✅)

Return On Invested Capital (ROIC) 13.9% (ROIC > 15%? ❌)

The high and increasing Gross Margin might indicate that L’Oréal has pricing power.

4. Is the company attractive in an interesting end market?

Although the beauty market is mature, there are still some interesting trends:

The aging population has an increasing need for beauty products

L’Oréal benefits from a rising middle class in Asia, projecting 600 million potential new customer by 2030

Skin care is a fast growing, global trend

The Global Beauty and Personal Care Product market is projected to grow by 6.7% per year until 2030.

Even though L’Oréal isn’t active in a fast-growing industry, the risk of disruption is pretty low.

A great company stays great for a long time.

L’Oréal is just like that.

If a company keeps doing well with the same products, it’s fair to think it will keep doing well.

"I very frequently get the question: ‘What’s going to change in the next 10 years?’ And I almost never get the question: ‘What’s not going to change in the next 10 years?’ I submit to you that that second question is actually the more important of the two, because you can build a business strategy around the things that are stable in time." - Jeff Bezos5. What are the main risks for the company?

Here are the main risks for L’Oréal:

The law of large numbers: With around $51.7 billion in annual sales, L’Oréal’s size makes rapid growth more challenging. This is a great example of the law of larger numbers at play: the larger a business, the harder it becomes to grow

Intense competition from rivals like Estée Lauder, Procter & Gamble, and Unilever

Rising threat from niche beauty brands gaining market share

Digitalization allows smaller competitors to reach customers online. They don’t have to battle for expensive shelf space anymore

Economic downturns reducing consumer spending on beauty products

6. Does the company have a healthy balance sheet?

We look at three ratios to determine the healthiness of the balance sheet:

Interest coverage: 24.3x (interest coverage > 15x? ✅)

Net Debt/FCF: 0.3x (Net Debt/FCF < 4x? ✅)

Goodwill/Assets: 23.4% (Goodwill to assets < 20%? ❌)

In an ideal world, we would love to see less goodwill.

7. Does the company need a lot of capital to operate?

The less capital a business needs to operate, the better

Here’s what things look like for L’Oréal:

CAPEX/Sales: 3.4% (CAPEX/Sales? < 5%? ✅)

CAPEX/Operating cash flow: 19.6% (CAPEX/Operating CF? < 25%? ✅)

L’Oréal has a capital light business model.

This means that it can take a large part of Free Cash Flow to invest in growth or to distribute to shareholders.

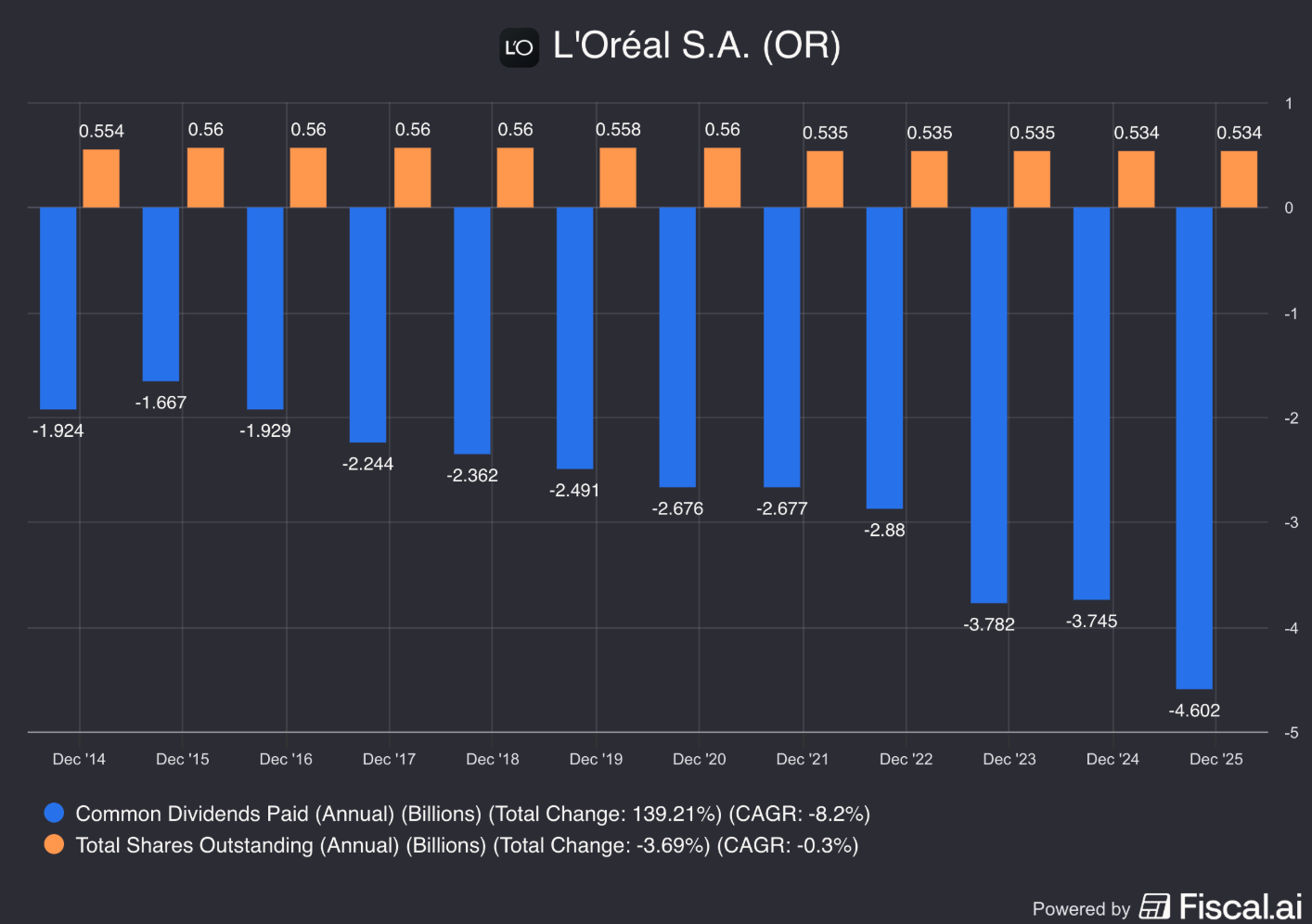

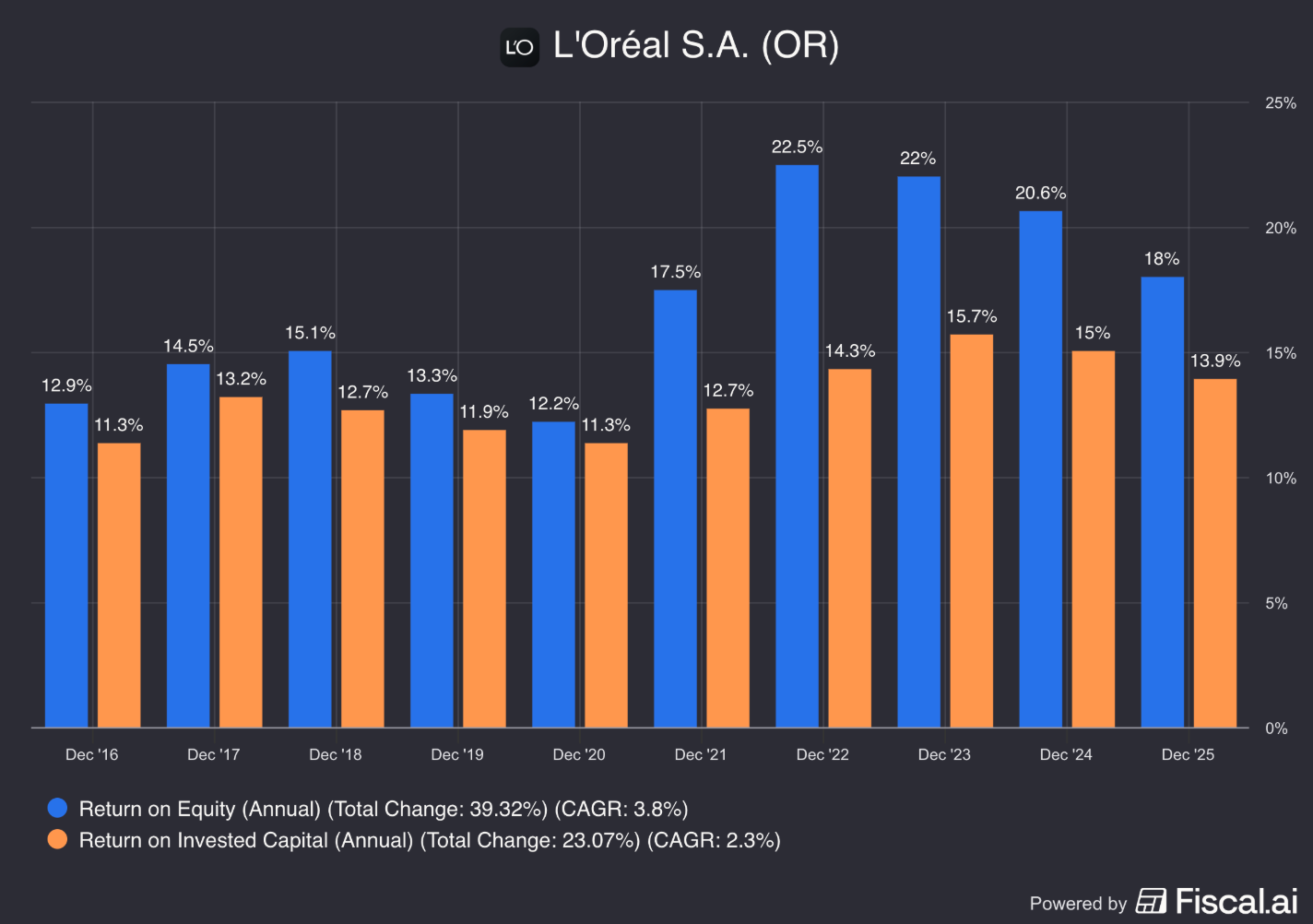

8. Capital allocation

Capital allocation is the most important task of management.

We are looking for businesses that are capable of allocating the resources of shareholders effectively.

L’Oréal:

Return on equity (ROE): 18.0% (ROE > 20%? ❌)

Return on Capital (ROIC): 13.9% (ROIC > 15%? ❌)

Here’s an evolution of L’Oréal’s ROE and ROIC:

In an ideal world, we would prefer these numbers to be a little bit higher.

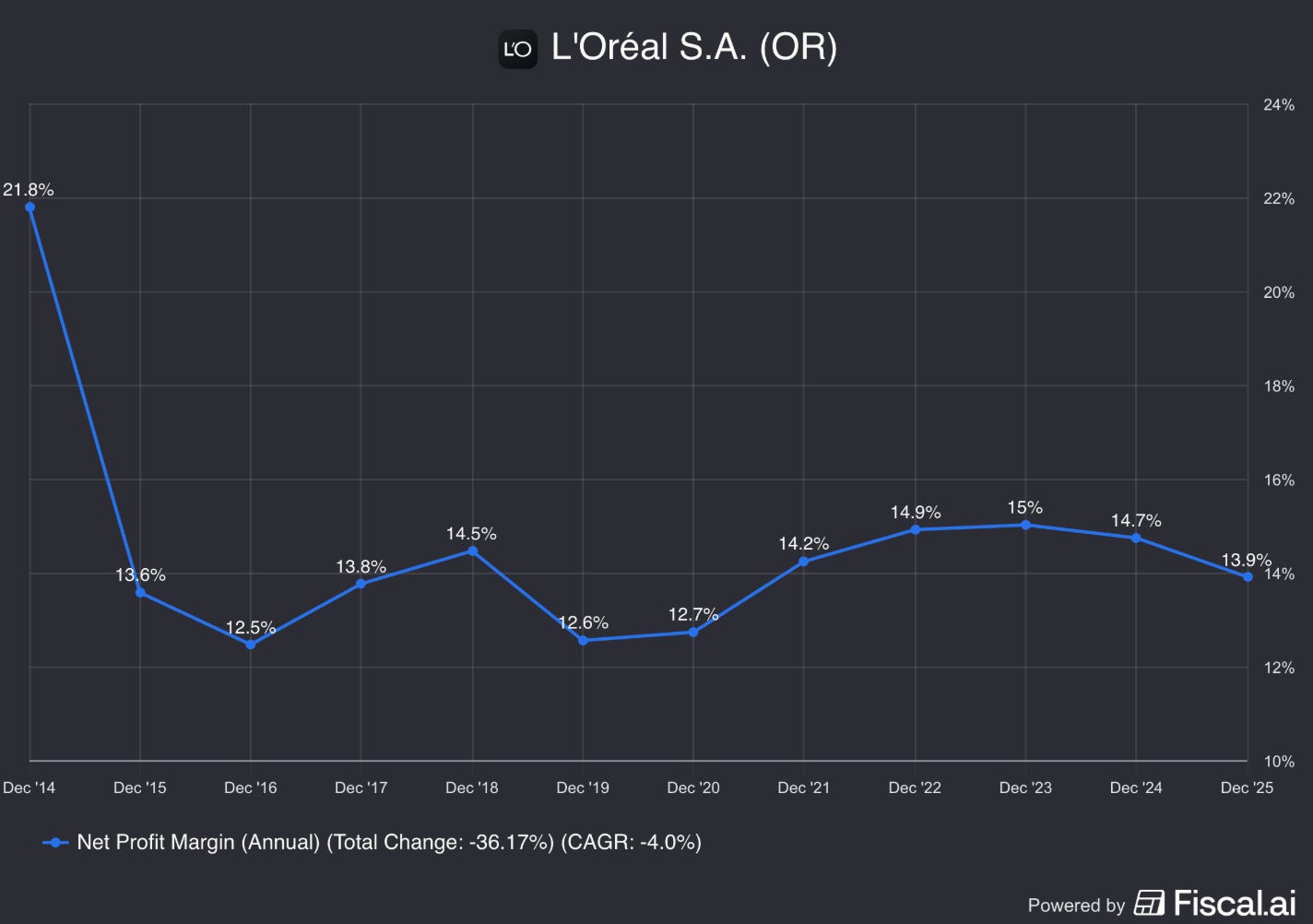

9. How profitable is the company?

The higher the profitability of the business, the better.

Here’s what thing looks like for L’Oréal:

Gross margin: 74.3% (Gross margin > 40%? ✅)

Net Profit Margin: 13.9% (Net Profit Margin > 10%? ✅)

FCF/Net income: 116.9% (FCF/Net income > 80%? ✅)

10. Does the company use a lot of Stock-Based compensation?

Stocks-based compensation is a cost for shareholders and should be treated accordingly.

Preferably, we want SBCs as a % of Net Income to be lower than 10%.

L’Oréal:

SBCs of a % of Net Income: 4.8% (SBSs/Net income < 10%? ✅)

Avg. SBC as a % of Net Income past 5 years: 3.8% (SBCs/Net income < 10%? ✅)

L’Oréal does not use a lot of Stock-Based Compensation.

This is a positive for investors.

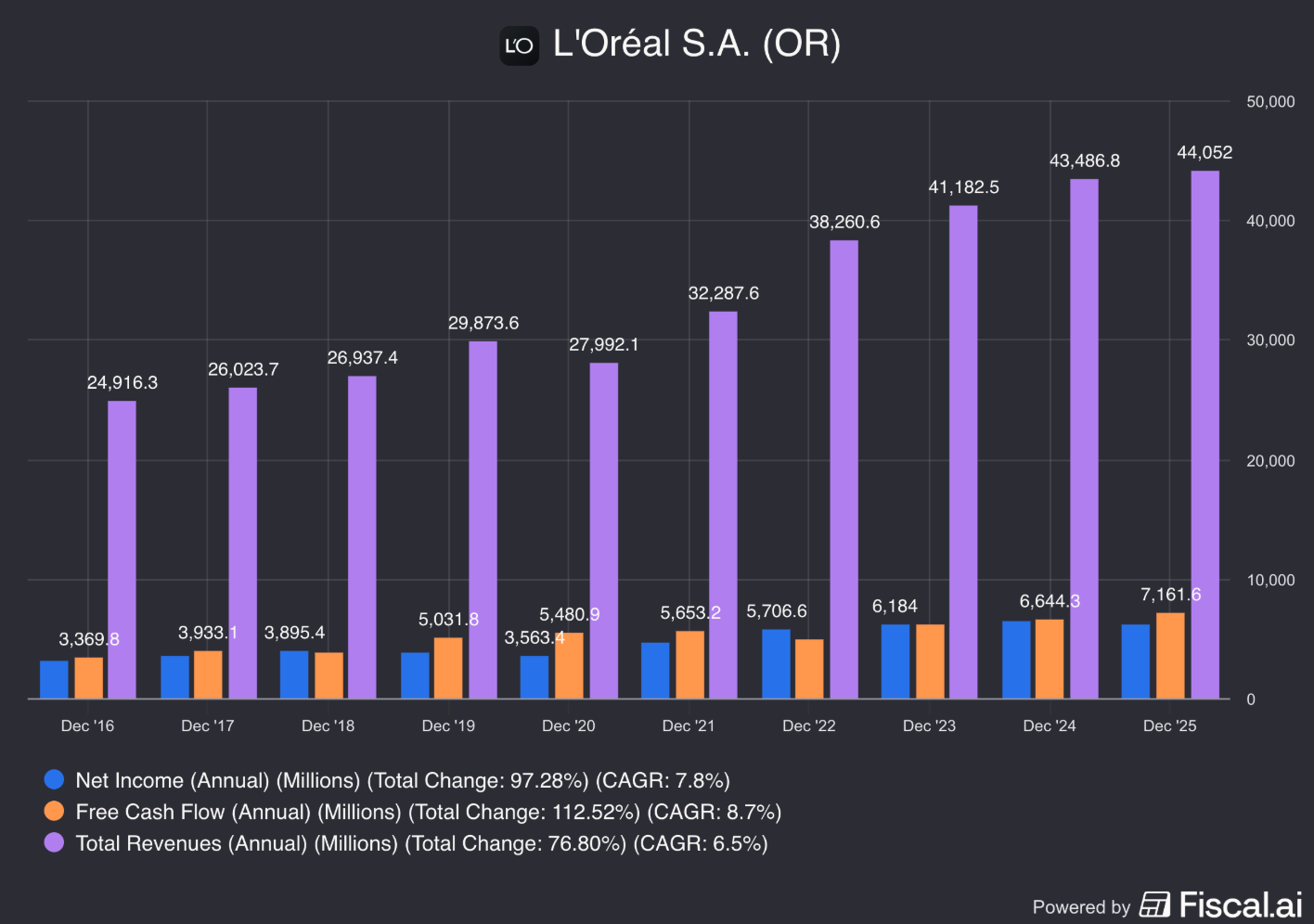

11. Did the company grow at attractive rates in the past?

Let’s look at what the recent history tells us:

Revenue growth past 5 years (CAGR): 9.5% (revenue growth > 5%? ✅)

Revenue growth past 10 years (CAGR): 6.1% (revenue growth > 5%? ✅)

EPS growth past 5 years (CAGR): 12.5% (EPS growth > 7%? ✅)

EPS growth past 10 years (CAGR): 7.1% (EPS growth > 7%? ✅)

The company has grown at attractive rates in the past.

12. Does the future look bright?

Let’s look at what the estimates are:

Exp. Revenue growth next 2 years (CAGR): 5.0% (revenue growth > 5%? ✅)

Exp. EPS growth next 2 years (CAGR): 12.1% (revenue growth > 7%? ✅)

Long-term growth estimate EPS (CAGR): 7.0% (EPS growth > 7%? ✅)

In an ideal world, we would love to see the revenue growth a bit higher.

13. Does the company trade at a fair valuation level?

L’Oréal’s iconic slogan is “Because You’re Worth It.”

Let’s explore what L’Oréal is worth to investors.

We always use three methods to look at the valuation of a company:

A comparison of the Forward PE multiple with its historical average

Earnings Growth Model

Reverse Discounted-Cash Flow

A comparison of the Forward PE multiple with its historical average

The first thing we do is compare the current forward PE with its historical average over the past 10 years.

This is a shortsighted method to give a quick indication.

Today, L’Oréal trades at a forward PE of 27.0x compared to a historical average of 31.5x.

As you can see, the valuation of L’Oréal came down significantly since 2022.

Earnings Growth Model

This model shows you the yearly return you can expect as an investor.

Here are the assumptions I use:

EPS growth: 7.0% per year over the next 10 years

Dividend Yield: 1.7%

Forward PE to decline from 27.0X to 25.0x

Expected yearly return = 7.0% + 1.7% + 0.1((25.0x – 27.0x)/27.0x)) = 8.0%

An expected yearly return of 8.0% is good, but we target a higher expected return in general.

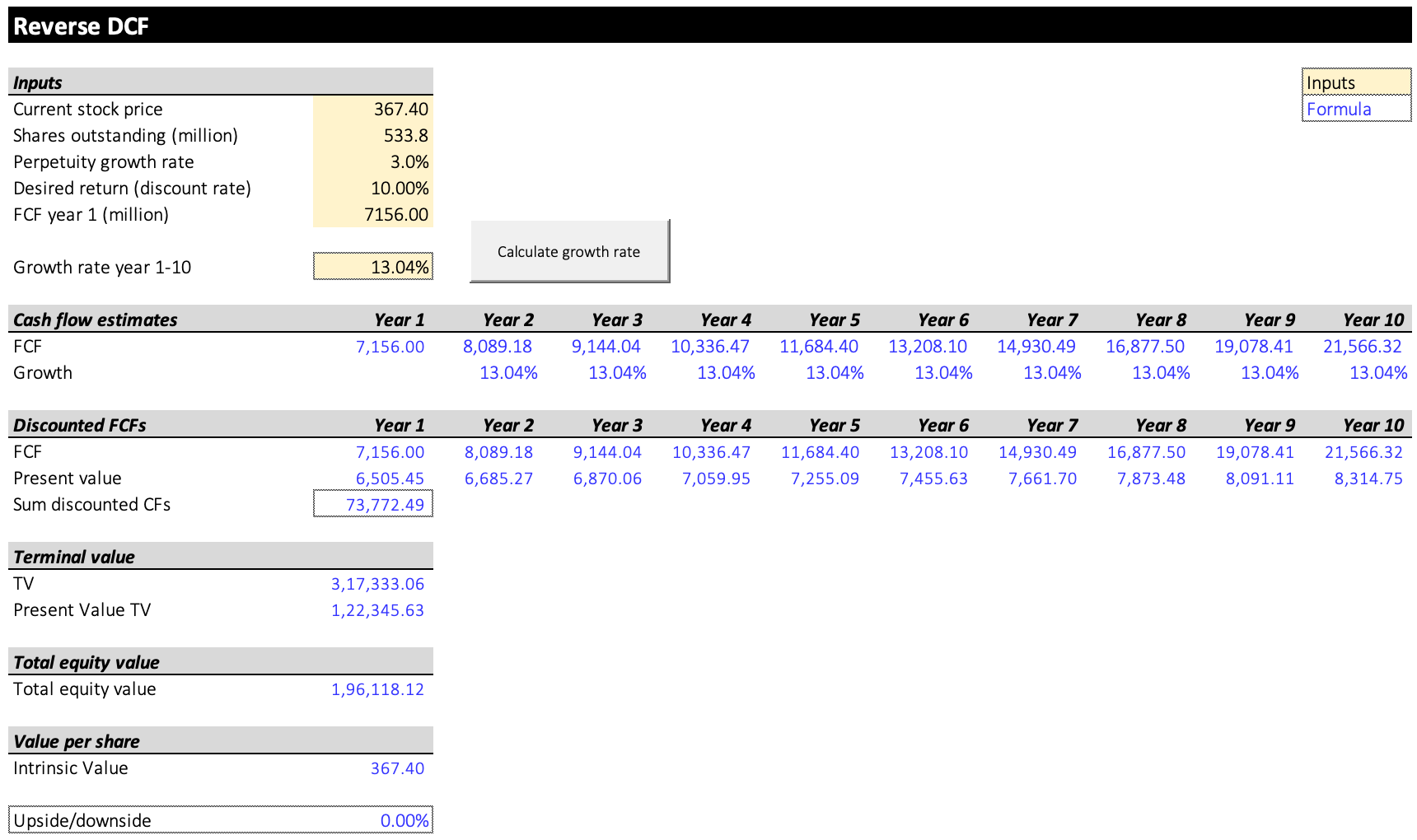

Reverse DCF

Charlie Munger once said that if you want to find a solution to a complex problem, you should invert. Always invert. Turn the problem upside down.

This is exactly what a reverse DCF does.

As an investor, we don’t make assumptions. We simply look at what assumptions the market has made and see whether they are reasonable.

The expected Free Cash Flow of the next 12 equals €7,350.0 million.

We subtract the Stock-Based Compensation (€248.0 million) and add Growth CAPEX (€54.0 million) to arrive at FCF in year 1 of €7,156.0 million.

The reverse DCF indicates that L’Oréal should grow its FCF by 13.0% each year for the coming 10 years.

This valuation seems to quite high.

Over the past 10 years, L’Oréal grew its FCF by 8.7% per year.

L’Oréal:

Forward PE: 27.0x (lower than its 10-year average? < 31.5x? ✅)

Earnings Growth Model: 8.0% (Yearly return? < 10%? ❌)

FCF-Growth Reverse DCF: 13.0% (Realistic growth expectations? ❌)

L’Oréal seems to be trading at rich valuation levels.

14. How did Owner’s Earnings evolve in the past?

Over time, stock prices tend to follow the Owner’s Earnings of the company (EPS growth + Dividend Yield)

That’s why we want to invest in companies that managed to grow their Owner’s Earnings at attractive rates in the past.

Owner’s Earnings = EPS change + dividend yield

L’Oréal:

CAGR Owner’s Earnings (5 years): 14.6% (CAGR Owner’s Earnings > 12%? ✅)

CAGR Owner’s Earnings (10 years): 9.1% (CAGR Owner’s Earnings > 12%? ❌)

15. Did the company create a lot of shareholder value in the past?

We want to invest in companies that managed to compound at attractive rates in the past.

Ideally, the company returned more than 12% per year to shareholders since its IPO.

Here’s what the performance of L’Oréal looks like:

YTD: +0.6%

5-year CAGR: +3.2%

CAGR since 2001: +8.2% (CAGR since 2001 > 12%? ❌)

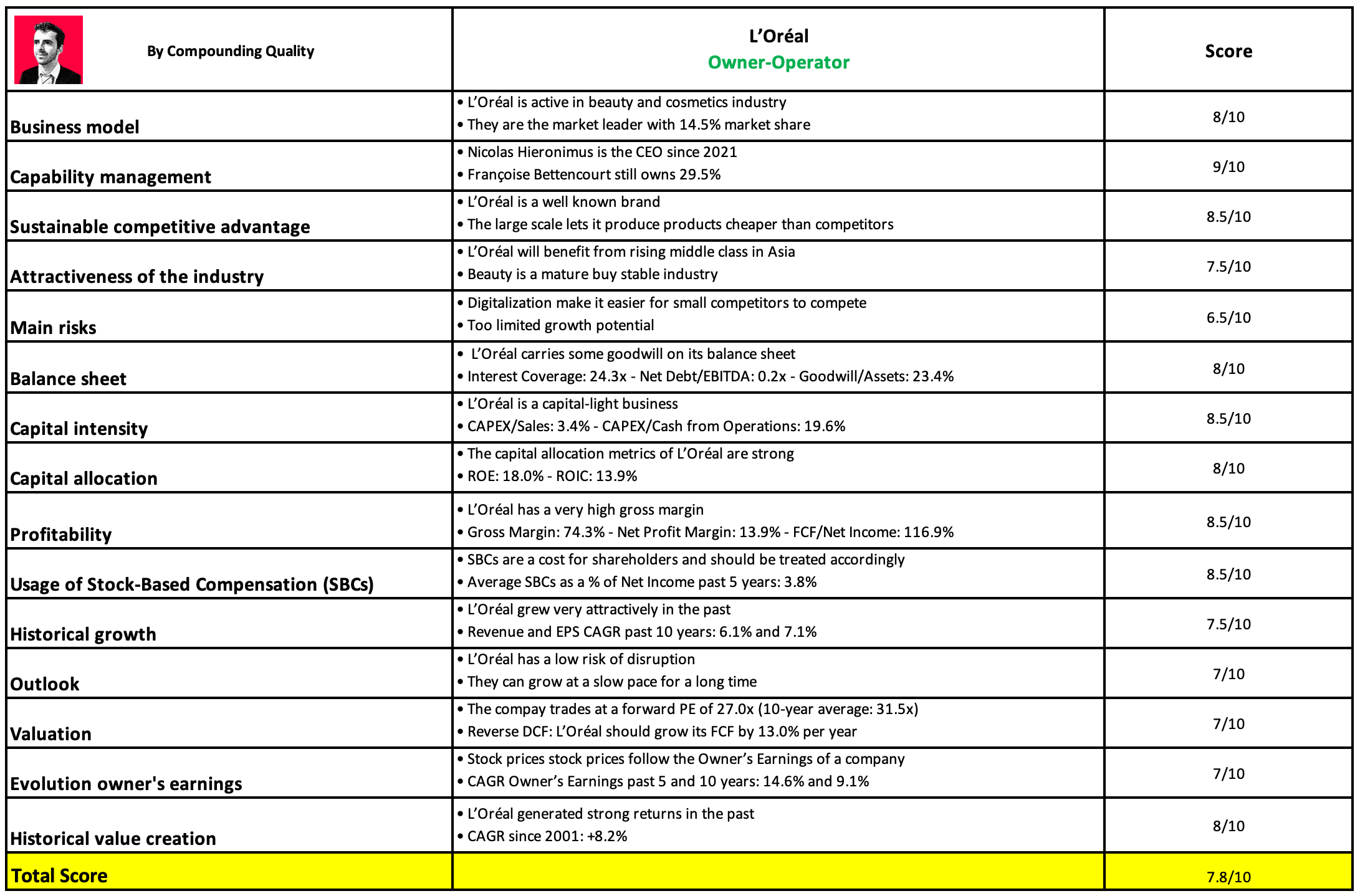

Quality Score

Finally, let’s bring everything together and give the company a Total Quality Score.

As you can see in the table below, L’Oréal gets a Total Quality Score of 7.8/10

The key conclusion?

L’Oréal is a wonderful business but the future growth prospects are too low.

I would love to own L’Oréal at 20x earnings.

This means I would love to buy L’Oréal at a price of €271 (current stock price: €367.4).

There are more attractive companies today if you ask me.

Which ones?

The ones in Our Portfolio!

Partners have 24/7 access to the Portfolio here:

Everything in life compounds

Team Compounding Quality

Book

Order your copy of The Art of Quality Investing here

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

This reads like one of those businesses everyone agrees is excellent, but the debate quietly shifts to what you’re actually paying for that excellence.

The consistency is what stands out. Long CEO tenures, strong margins, global reach. It’s the kind of machine that keeps working regardless of the cycle.

But the tension is clear. When a company gets this large, growth becomes less about expansion and more about defending what’s already built. That’s where expectations start doing most of the heavy lifting.

Feels like a situation where the business quality isn’t really in question. The real question is how much of that quality is already priced in.

What makes L'Oreal interesting from an AI transformation perspective is how far ahead they are versus most luxury and beauty brands. They invested early in personalization, AR try-on, and data infrastructure when most competitors were still debating whether to run pilots.

The real P&L question going forward is whether those investments start compressing customer acquisition costs in premium segments or mostly drive volume in mass market. The brands where AI actually moves gross margin are the ones where the customer relationship is personal enough to act on. L'Oreal sits in both worlds, which makes the financial story more complex than it looks.