Portfolio Update: July 2026

Hi Partner 👋

I hope you are having an amazing summer.

Let’s dive into Our Portfolio Update today.

What’s going on in the markets today? And how are our stocks doing?

Chasing Momentum

Investors seem to continue to be focused on the short term and chasing momentum.

Remember when the Magnificent 7 were the most exciting stocks in the market?

Investors have already moved on.

Bill Ackman says the market is distracted by momentum and hype.

He sees companies like Microsoft and Meta as old-fashioned.

The market is distracted by big IPOs.

Here are just a few examples:

SpaceX

OpenAI

Anthropic

Stripe

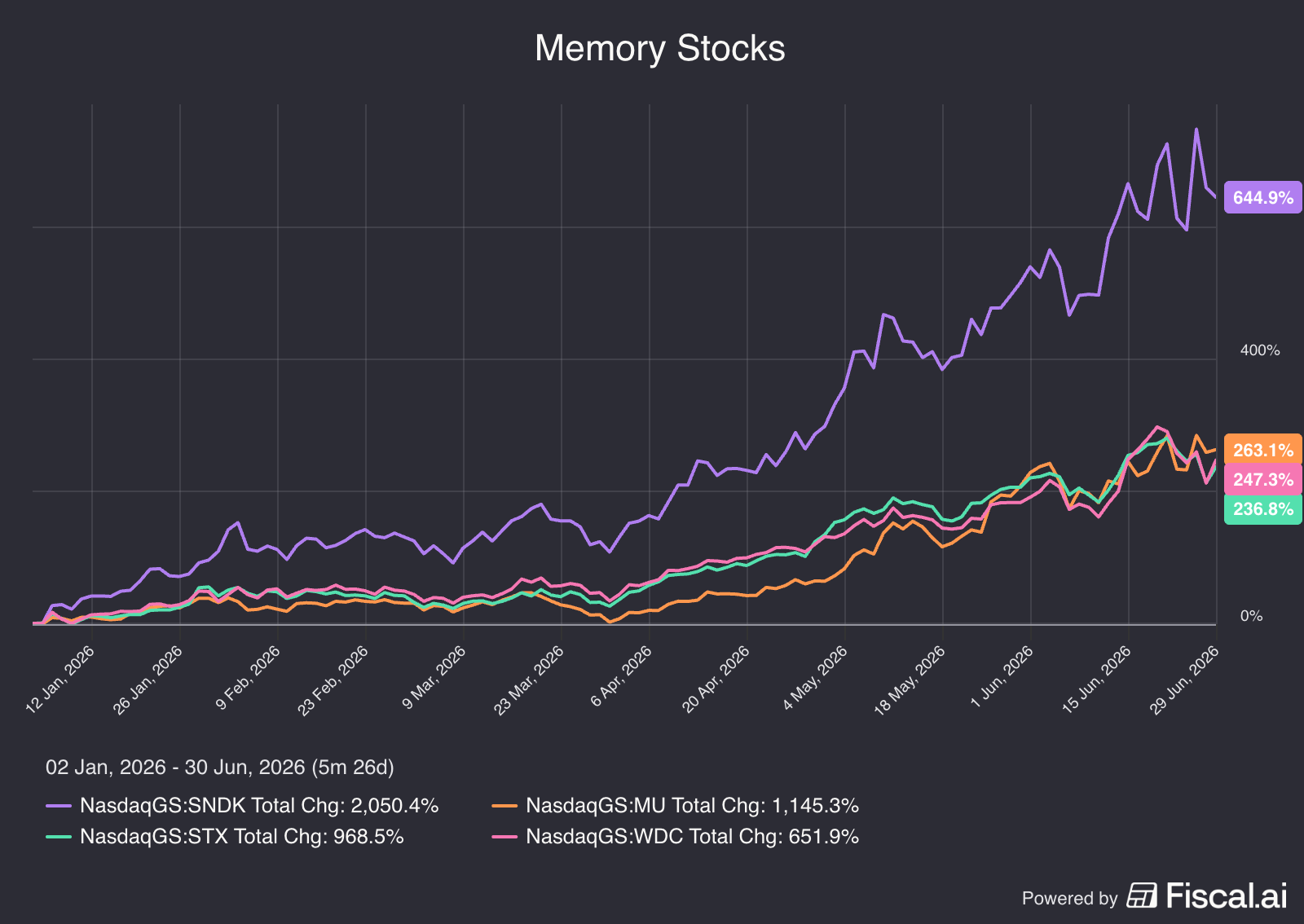

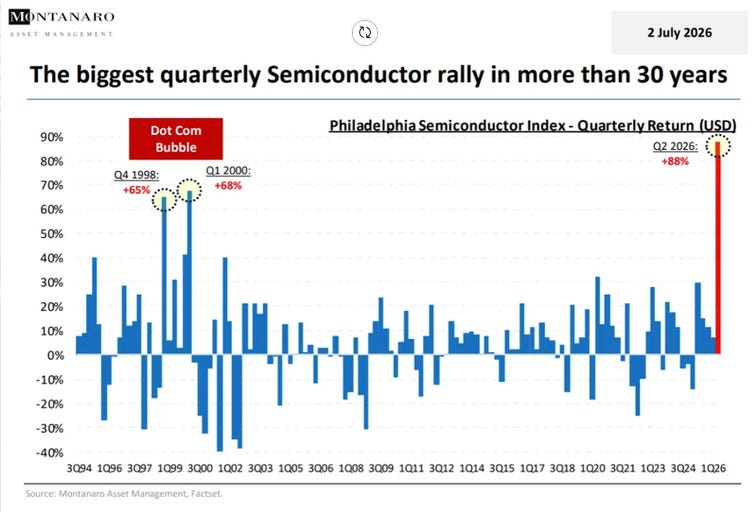

Besides IPOs, the market focuses on memory stocks (manufacturers of semiconductor memory chips):

Micron

Western Digital

Sandisk

They are all up +200 to +700% this year.

Just take a look at this chart shared by my good friend Sebastian:

A different kind of problem

Companies like SpaceX and OpenAI are having a different problem compared to memory companies right now:

Companies like OpenAI, SpaceX, and Anthropic lose money every single month.

Memory companies like Micron and SanDisk are currently making too much money.

I know it sounds strange to say a company can make too much profit.

Why might that actually be a problem?

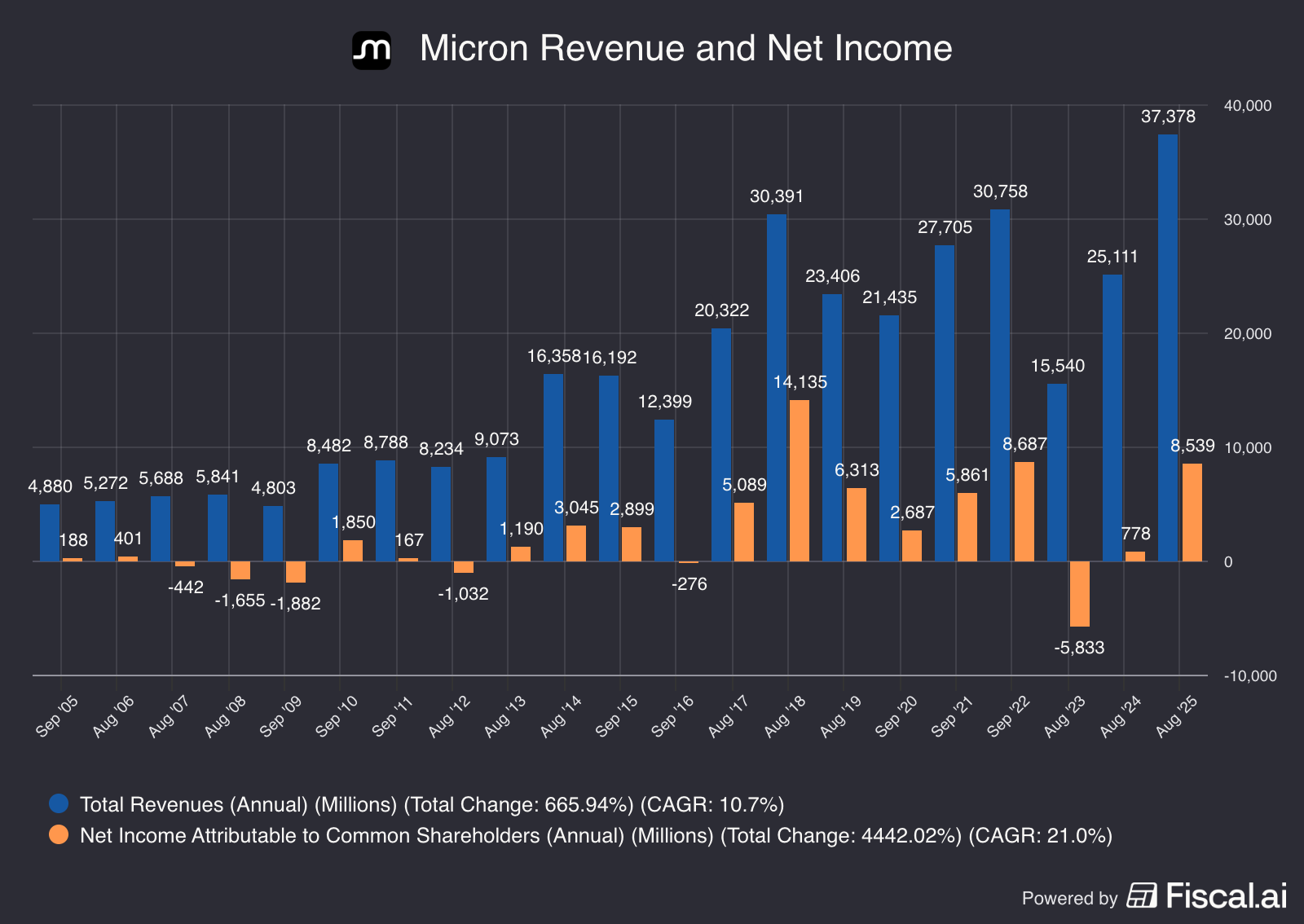

Historically, memory has been a very cyclical business.

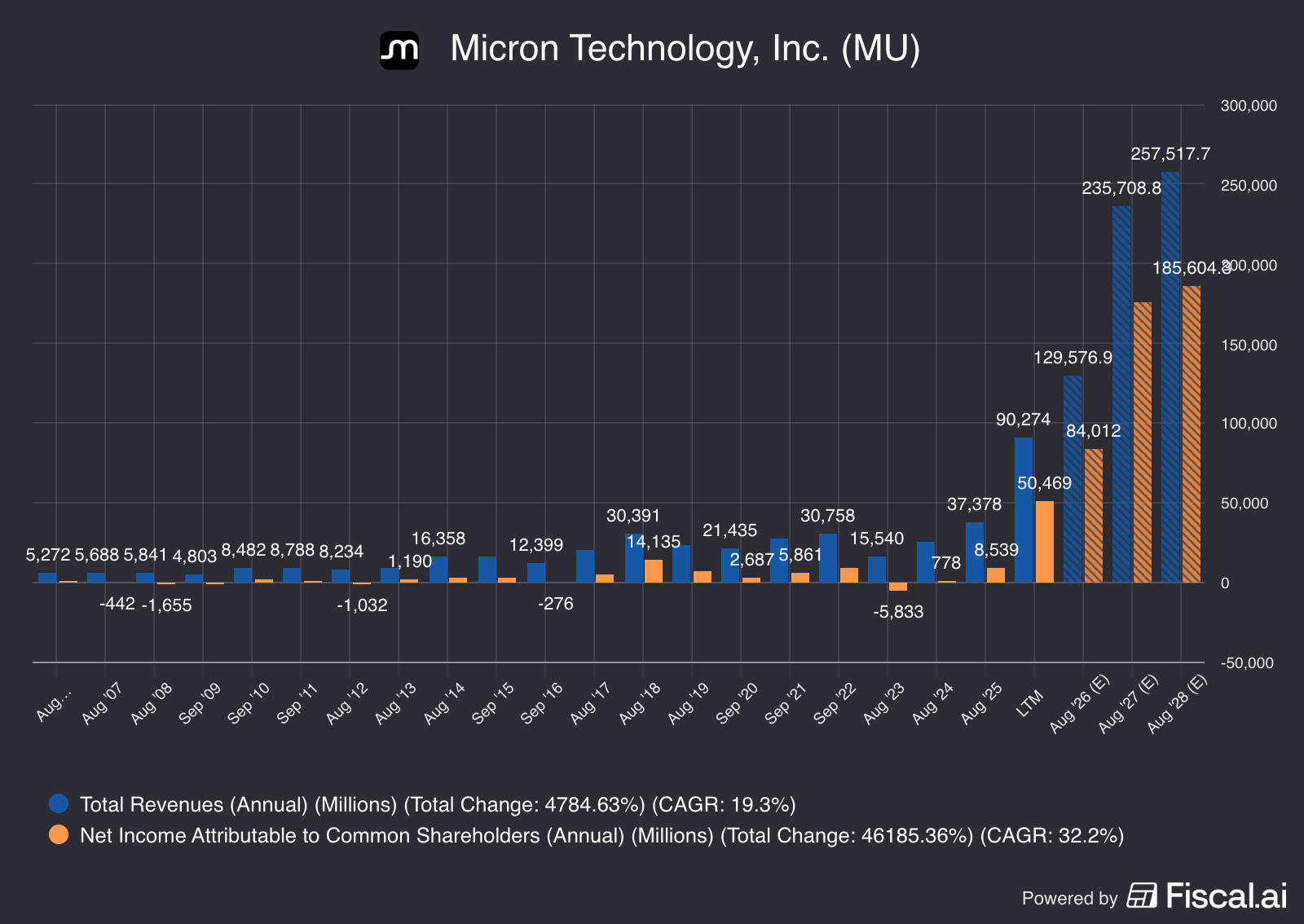

Just look at Micron’s revenue and net income:

Periods of high revenue and profits are almost always followed by periods of low revenue and profits.

Why?

Because memory is a commodity business.

These companies don’t have any pricing power.

Their profits are completely driven by supply and demand.

Can you imagine a company like Coca-Cola or Moody’s losing money because their customers demanded lower prices?

I can’t.

But that’s exactly what happened to Micron in 2023 and 2024.

Sumit Sadana, CEO of Micron, said that a couple of customers were aggressively pushing for lower prices.

“We told a couple of the customers who were being very aggressive with pricing at that time that this is not constructive. A lot of the industry investments got shut down in 2023 because of really poor pricing and really poor margins.”

The losses (and low demand for memory) stopped Micron from building new factories.

Now that AI is pushing memory demand up and supply is low, prices are sky high.

In the past, this caused competition and lower prices.

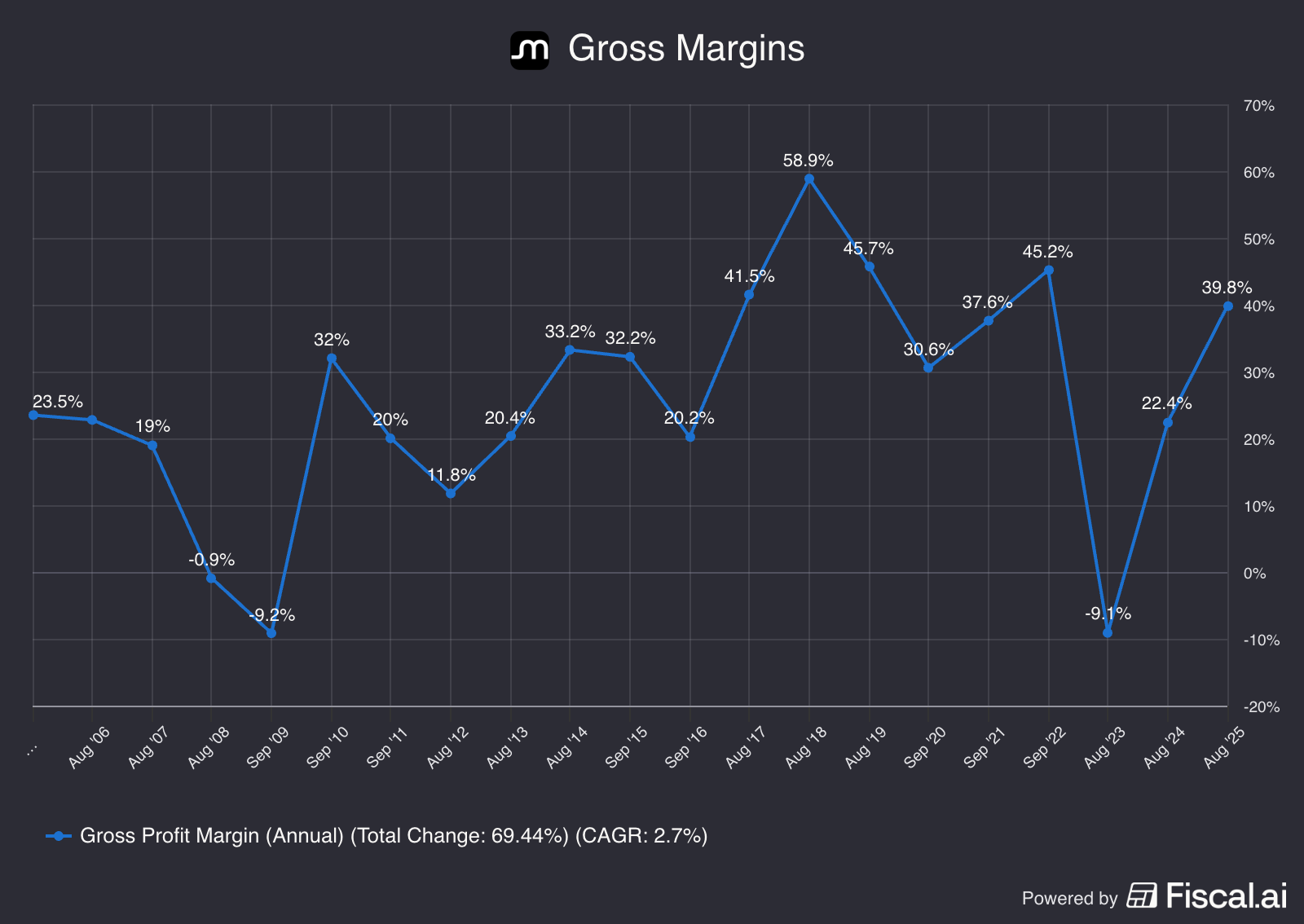

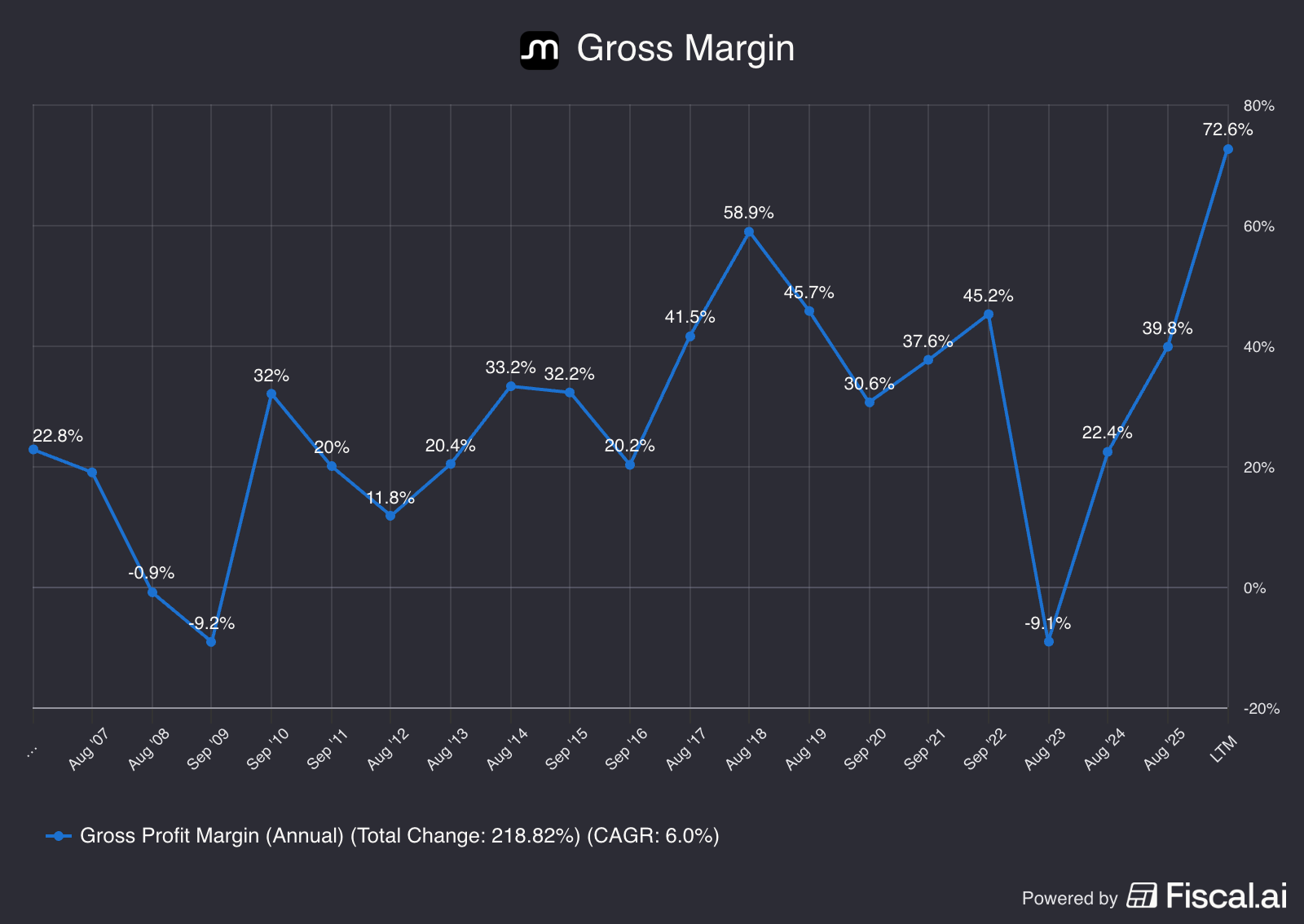

Look at the Gross Margins for Micron in 2018, they were much higher than normal.

But they came back down.

And Micron’s stock went down the year thereafter:

Today their margins are even higher than in 2018.

Micron’s elevated profits will probably last for a while, but here’s what Jeremy Grantham says:

“Mean reversion is kind of shorthand for history matters… If you make abnormal profits, you will receive competition. If you make obscene profits, you’ll get ferocious competition.”

Here’s the chart of Micron’s Revenue and Net Income from 2006 to 2028:

The market is clearly not expecting any mean reversion or increased competition.

Maybe this time really is different.

But that’s not a bet that I want to make.

And I don’t think you should do either.

Let’s now dive in and see how our businesses are performing.

Our Portfolio

Fundamentally, our businesses are doing great.

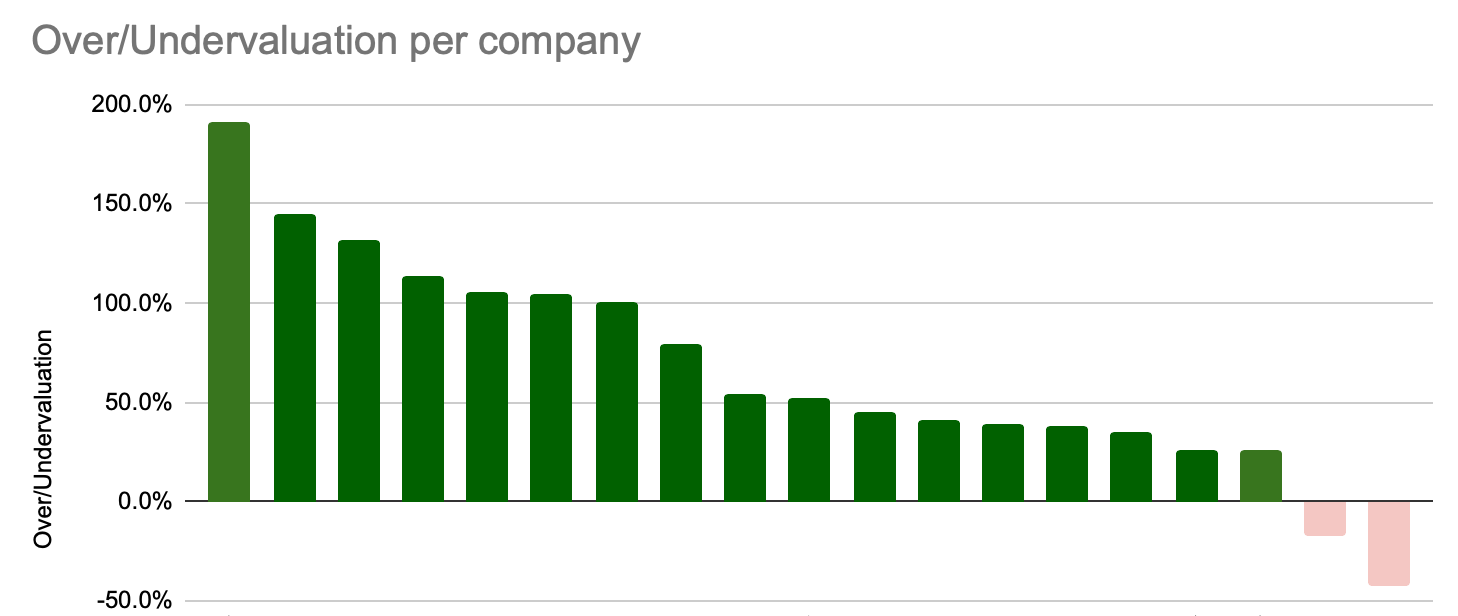

Our companies are healthier than the ones in the S&P 500.

And our companies are 15% (!) cheaper than the S&P 500.

The S&P 500 continues to look very expensive.

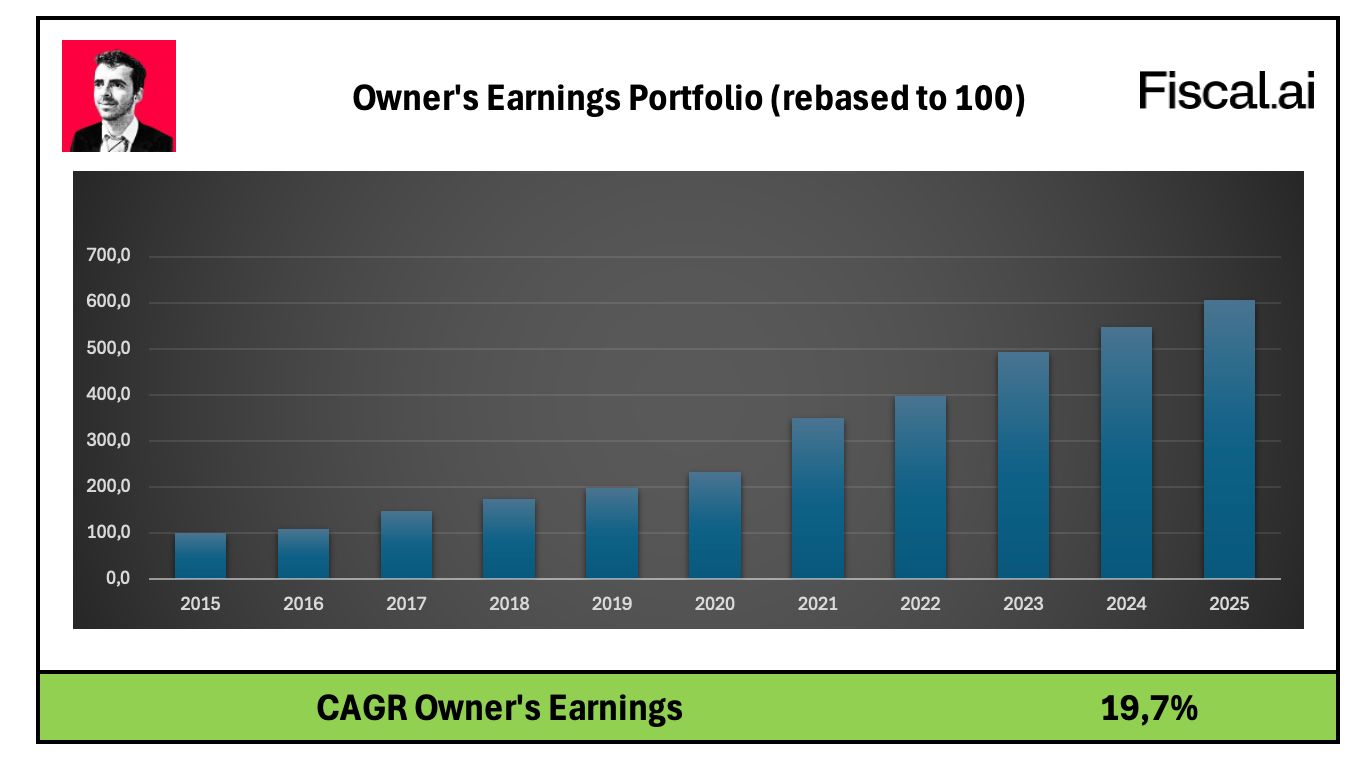

The intrinsic value of our companies has grown by nearly 20% (!) per year.

Almost every company we own remains undervalued right now.

That means it’s a great time to buy a lot of the companies in Our Portfolio.

I feel very confident that Our Companies will be fine.

Why?

Because we own companies with durable competitive advantages.

In the short run, the prices can diverge a lot from the businesses fundamentals.

But in the long run, the business fundamentals will determine Our Results.

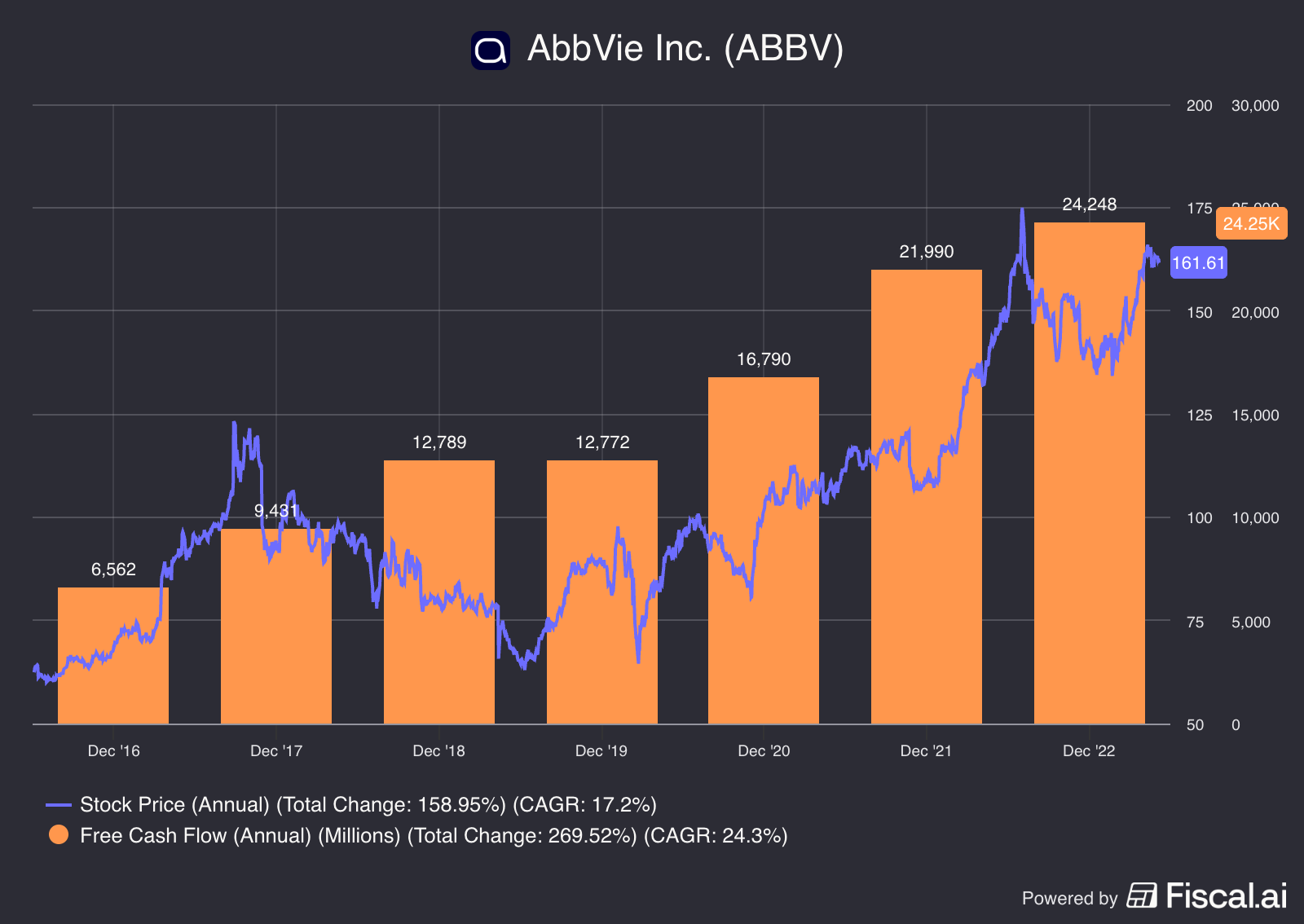

Just look at AbbVie (for clarity, we don’t own this company).

The price declined all through 2018 because of fear over some of its drugs losing patent protection.

In the meantime the Free Cash Flow kept increasing.

And over the next few years, the stock caught up and more than doubled.

Our Fundamentals

Here’s the situation for our companies right now:

Expected Revenue Growth Rate (next 2 years): +6.8%

Forward P/E Ratio: 17.1x

Do you know what it would take to give us a 10% return per year going forward?

Grow Owner’s Earnings at the same rate at Revenue (6.8%, very conservative)

And re-rate to just 20x Earnings

In other words, the expectations for our businesses are very low right now.

I think Mr. Market is underestimating Our Companies.

But he may be starting to catch on…

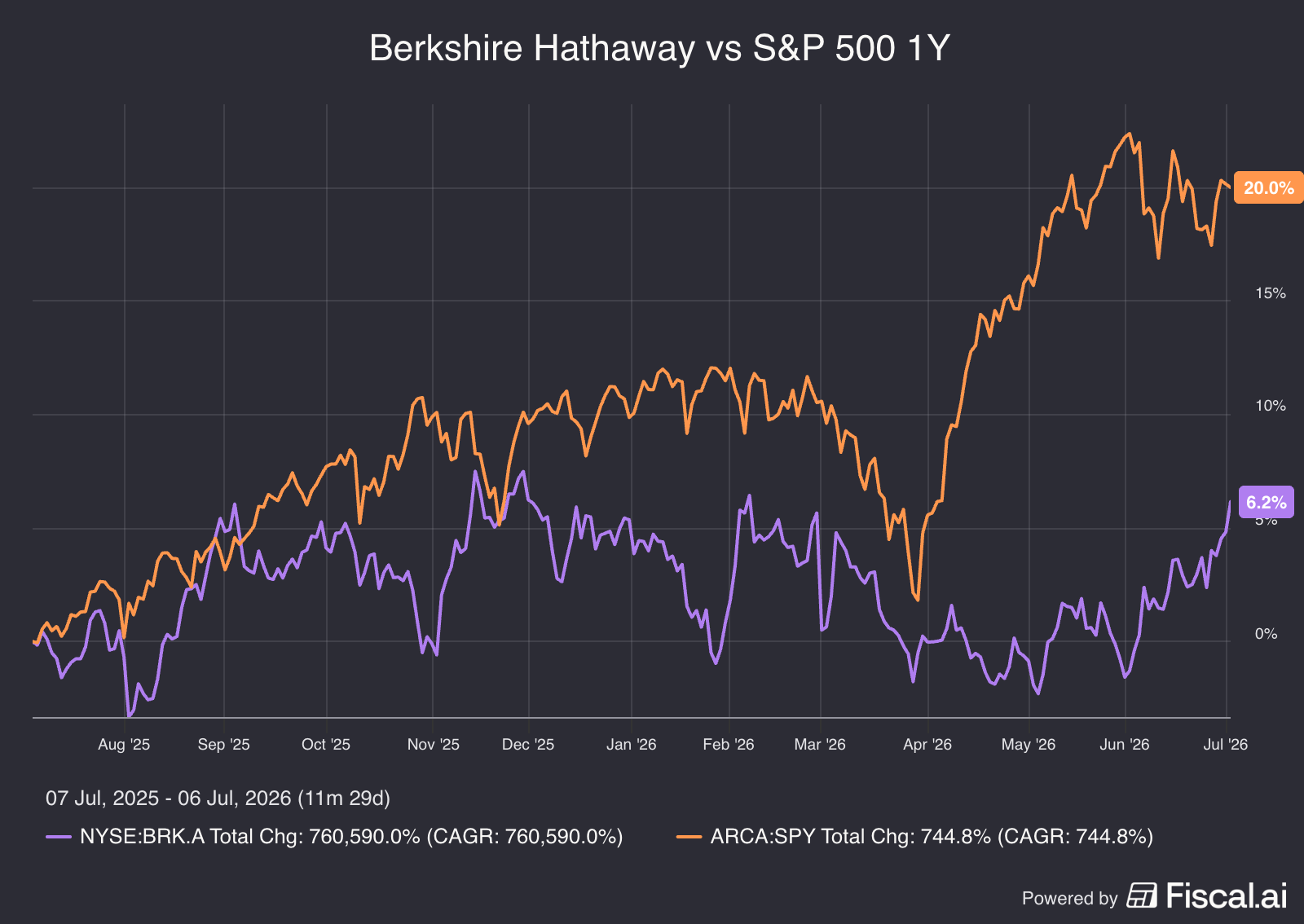

During speculative market runs like this one, boring, high-quality companies like Berkshire Hathaway often outperform in the years that follow.

Here’s how Berkshire has performed compared to the S&P 500 over the past year:

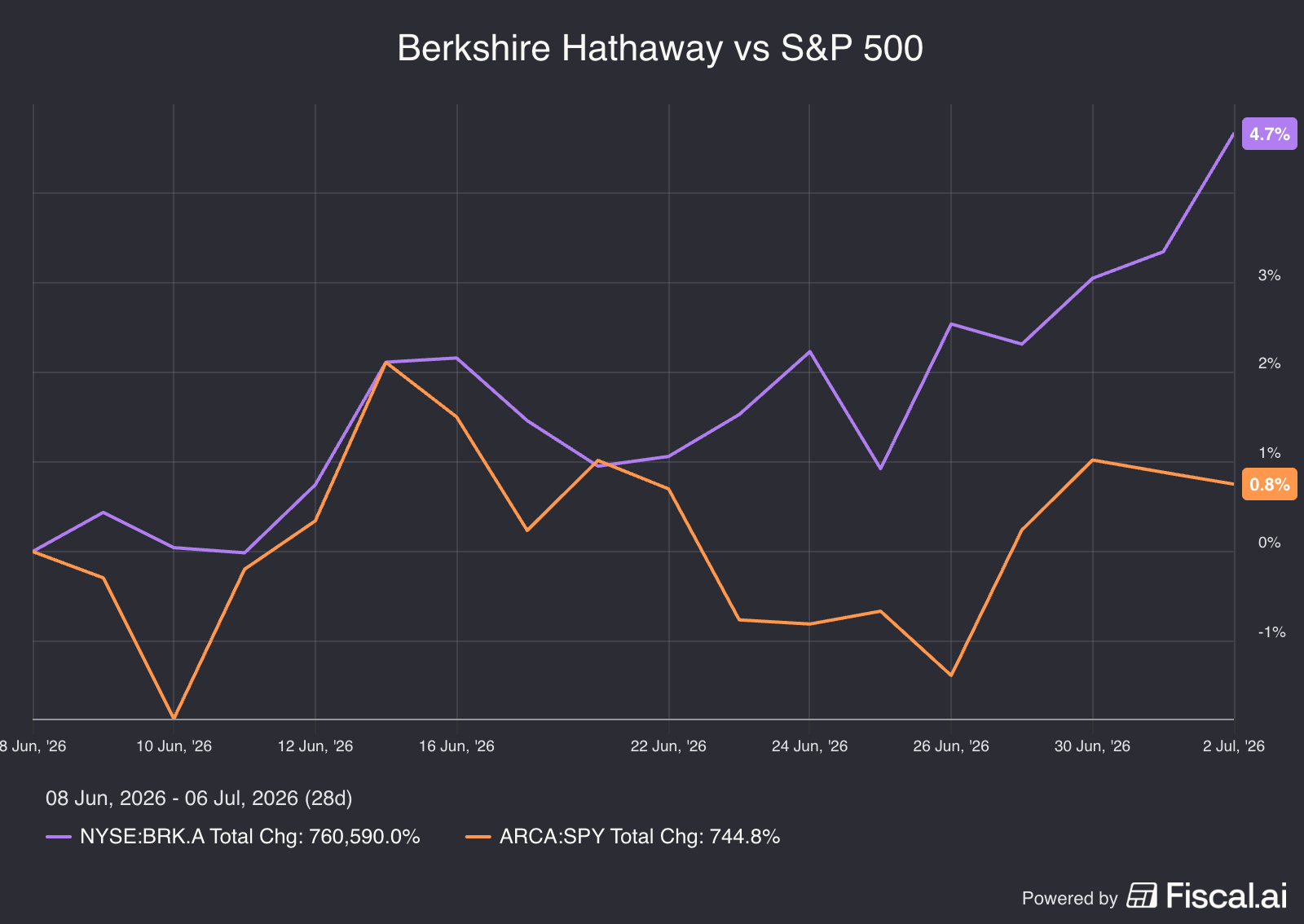

But if we look at the past month, it looks like we might be starting to see a rotation back into quality.

Let’s look at a few of our businesses and see what makes them so special.