📈 Should you buy Microsoft after the decline?

Microsoft is one of the most valuable companies in the world.

A lot of people use Windows or Microsoft Office every single day.

The stock is currently down 25% from its peak.

Does it make Microsoft an interesting investment? Let’s find out.

Microsoft - General Information

👔 Company name: Microsoft Corporation

✍️ ISIN: US5949181045

🔎 Ticker: MSFT

📚 Type: Oligopoly

📈 Stock Price: $391.8

💵 Market cap: $ 2.91 trillion

📊 Average daily volume: $13.6 billion

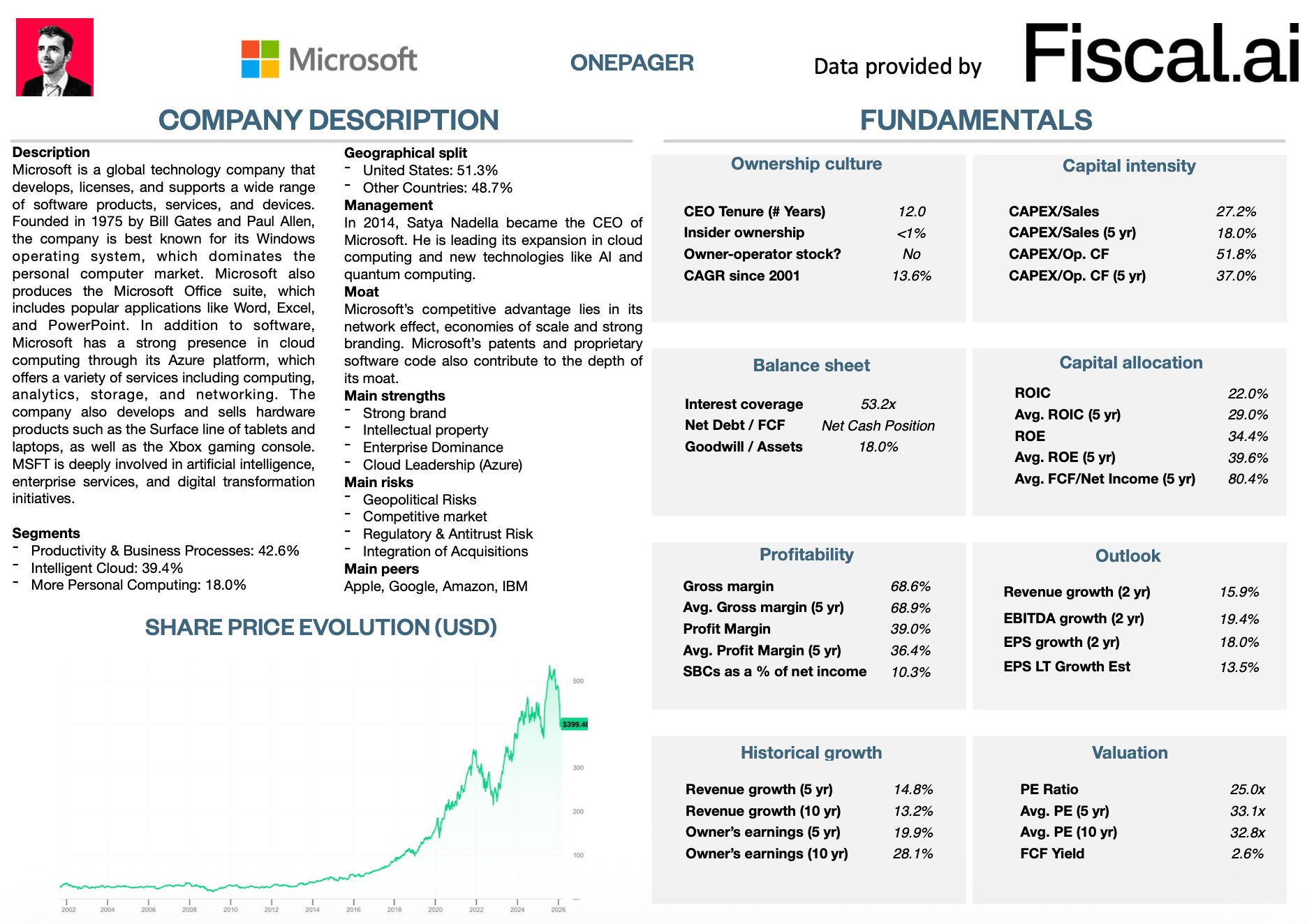

Onepager

Here’s a onepager with the essentials of Microsoft.

You can click on the picture to expand:

15-Step Approach

Let’s use our 15-step approach to analyze the company.

At the end of this article, we’ll give Microsoft a score on each of these 15 metrics.

This results in a Total Quality Score.

1. Do I understand the business model?

Microsoft is a leading technology company that develops, licenses, and supports software products, services, and devices.

Founded in 1975 by Bill Gates and Paul Allen, Microsoft has grown into one of the world’s most well-known and valuable companies.

Gates wanted to build a platform like no other:

“A platform is when the economic value of everybody that uses it, exceeds the value of the company that creates it.” - Bill Gates

Microsoft is active in three main markets:

Productivity and Business Processes (42.6% of total revenue): This includes sales of Microsoft Office software, such as Word and Excel, and subscription services like Microsoft 365. It also covers business tools like LinkedIn and Dynamics 365

Intelligent Cloud (39.4% of total revenue): Microsoft makes money from its Azure cloud services, which provide computing power, storage, and other services to businesses

More Personal Computing (18.0% of total revenue): This segment includes revenue from Windows operating system licenses for PCs, sales of Surface tablets and laptops, and Xbox gaming consoles. It also covers advertising and search revenue from Bing

So next time you’re working on a document or playing a game, remember Microsoft is behind the scenes making it all happen.

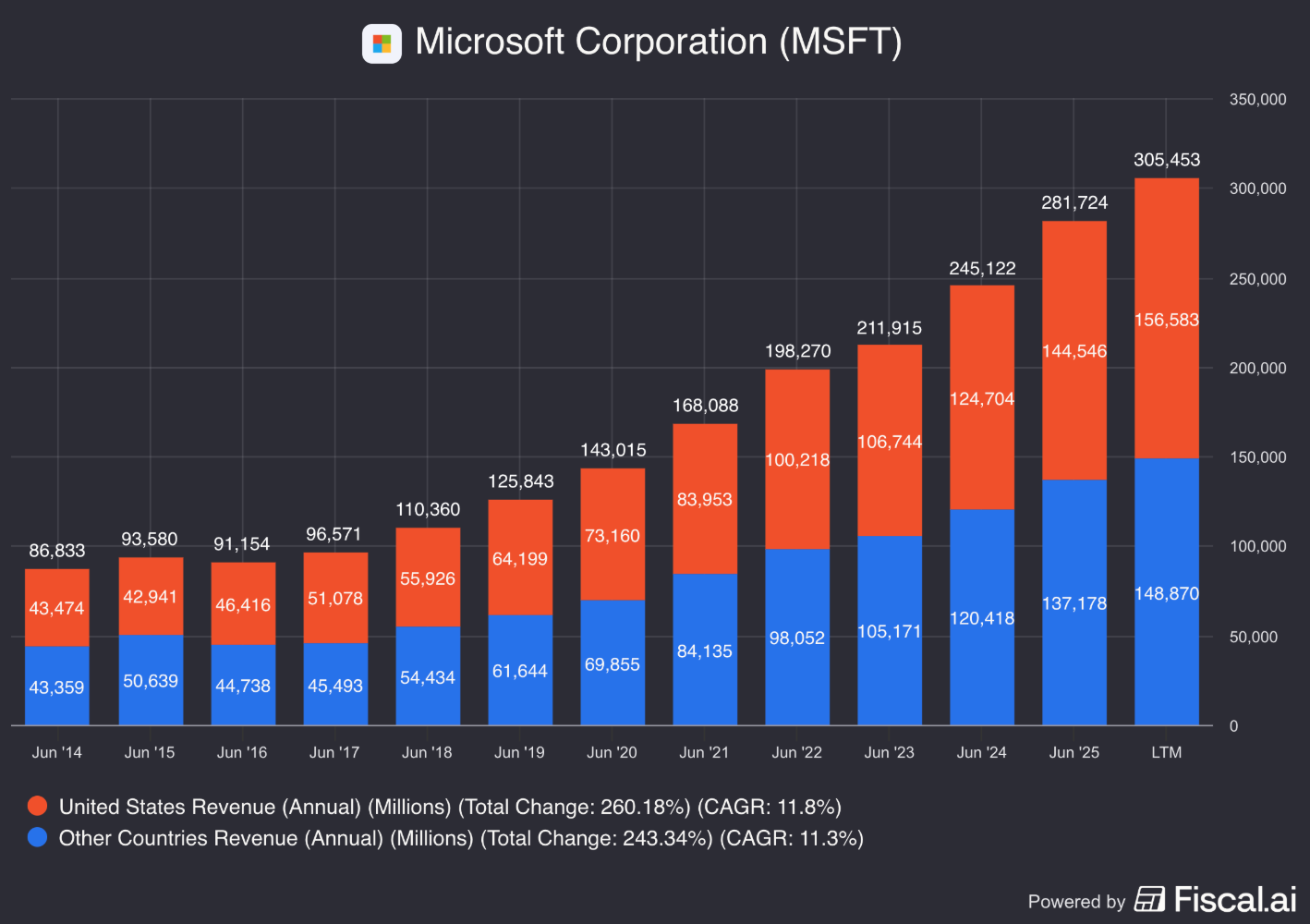

As you can see in the chart below, half of Microsoft’s revenue comes from the US:

Please note that by investing in Microsoft, you are also investing ChatGPT.

Microsoft currently owns 27% of OpenAI.

2. Is management capable?

Satya Nadella is the CEO of Microsoft since 2014.

Nadella joined the company in 1992, leading major projects on building and running cloud computing and development.

It’s great seeing Nadella must own a minimum of 15x his base salary worth of Microsoft stocks.

In 2013, Amy Hood became the CFO. She joined Microsoft in 2002 after finishing her MBA at Harvard University.

Insider ownership is less than 1% (total value: $1.1 billion).

What’s great seeing? Employees would recommend working at Microsoft (high Glassdoor rating):

3. Does the company have a sustainable competitive advantage?

Microsoft is a global leader with a wide moat.

Their competitive advantage is based on high switching costs.

Users and businesses find it costly and difficult to move away from its integrated software and services. This dependency keeps customers loyal to Microsoft.

Microsoft also benefits from other moat sources:

Intellectual property: Microsoft holds numerous patents and copyrights

Brand strength: Microsoft has a well-known brand name and strong reputation

Economies of scale: They produce software and services more efficiently

Network effects: Windows and Office increase in value as more people use it because of compatibility

Barriers to entry: Microsoft’s compliance with global regulations creates high barriers to entry

Companies with a sustainable advantage have these qualities:

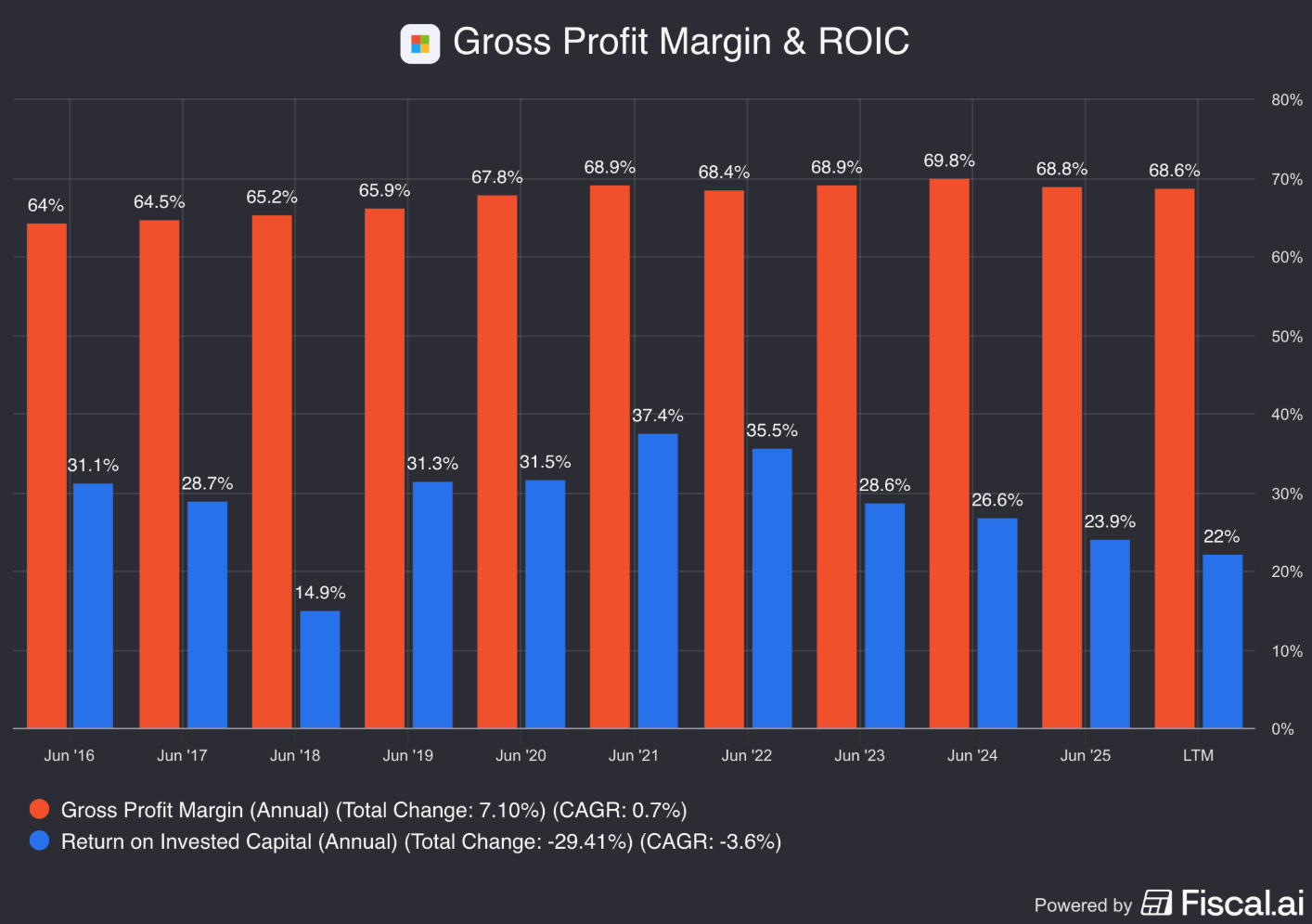

Gross Margin: 68.6% (Gross Margin > 40%? ✅)

Return On Invested Capital (ROIC): 22.0% (ROIC > 15% ✅)

Microsoft is investing heavily in AI.

That’s the main reason why you see a declining ROIC.

We think this number will go up again over time as these investments will yield a return eventually.

4. Is the company active in an attractive end market?

Microsoft is active in attractive end markets for sure.

Here are just a few examples:

Windows is a clear market leader in the Personal Computing Market. They have a 75% market share with Apple as a major competitor

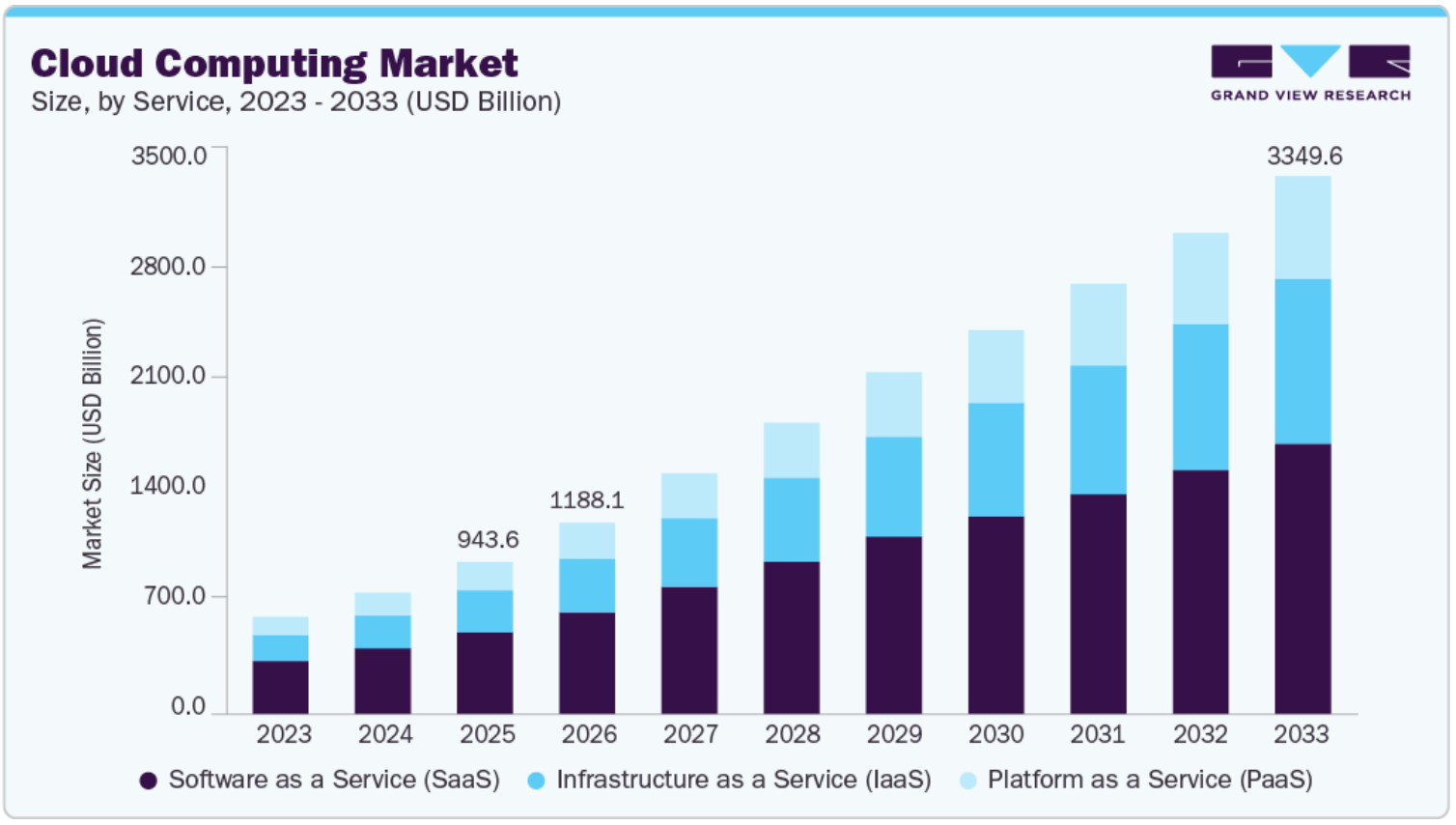

The company’s Cloud Services segment is active in a competitive market. Microsoft has a 20% market share in this segment. This market is expected to grow at a CAGR of 16.0% until 2033. Main competitors are Amazon, Google Cloud, Alibaba Cloud and IBM.

Market leader in the productivity software market (Office, LinkedIn, ..). Google is a major competitor in this segment.

5. What are the main risks for the company?

Here are some of the main risks for Microsoft:

Intense competition: A lot of competition from other Big Tech companies

Data security risks: Microsoft is a prime target for cyberattacks and breaches that could damage its reputation

Rapid advancements in technology (AI): While Microsoft has made major bets on AI through its OpenAI partnership, the pace of innovation means it risks being disrupted

Regulations: Growing scrutiny from regulators across the US and Europe around antitrust, data privacy, and AI governance

High valuation levels (see later)

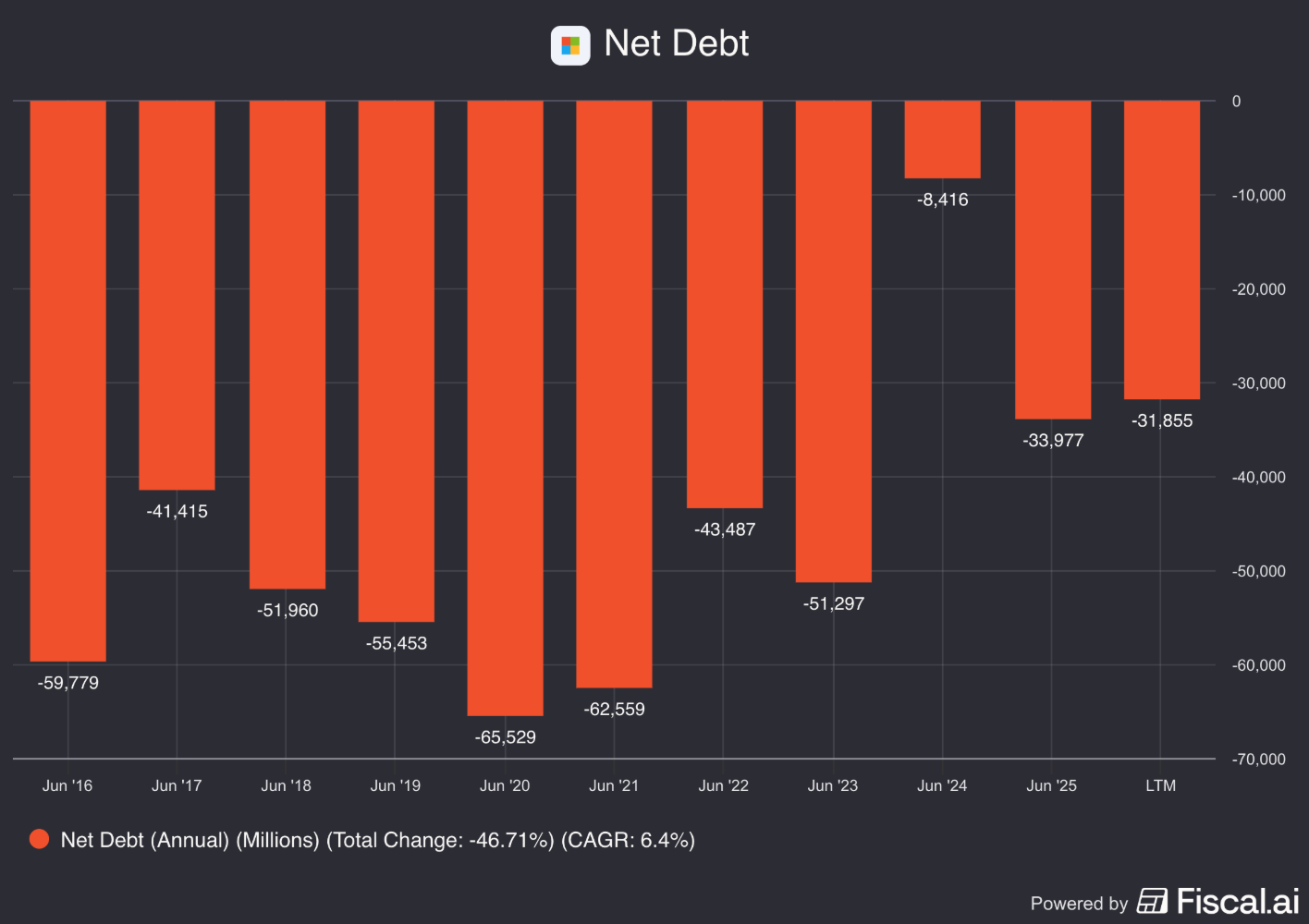

6. Does the company have a healthy balance sheet?

We look at 3 ratios to determine the healthiness of Microsoft’s balance sheet:

Interest Coverage: 53.2x (Interest Coverage > 15x? ✅)

Net Debt/FCF: Net Cash Position (Net Debt/FCF < 4x? ✅)

Goodwill/Assets: 18.0% (Goodwill/assets not too large? < 20% ✅)

Microsoft’s balance sheet looks healthy.

7. Does the company need a lot of capital to operate?

We prefer to invest in companies with CAPEX/Sales lower than 5% and CAPEX/Operating Cash Flow lower than 25%.

Microsoft:

CAPEX/Sales: 27.2% (CAPEX/Sales < 5%? ❌)

CAPEX/Operating Cash Flow: 51.8% (CAPEX/Operating CF? < 25% ❌)

But wait… Microsoft is investing heavily in future growth.

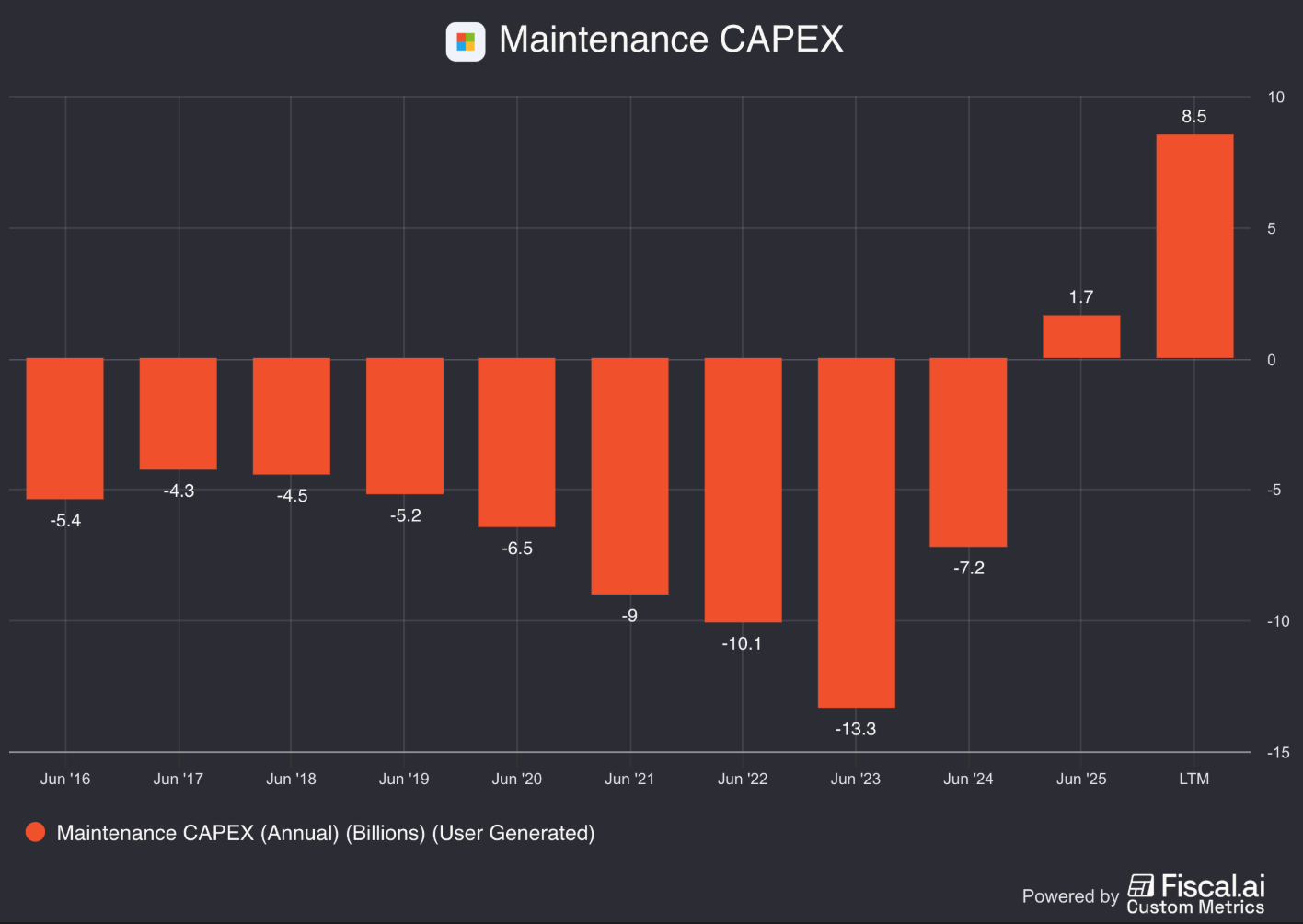

Remember that there is a difference between Maintenance CAPEX and Growth CAPEX.

Maintenance CAPEX: Investments made in existing assets

Growth CAPEX: Investments made in new assets in order to grow

When a company invests a lot in order to grow, its growth CAPEX is very high but these investments might create a lot of value in the long term.

That’s why sometimes (like for Microsoft) it might make sense to only take the company’s Maintenance CAPEX into account.

As a rule of thumb, we state that the company’s maintenance CAPEX is equal to the company’s Depreciation & Amortization.

When we only take Microsoft’s Maintenance CAPEX (without R&D costs) into account, we get the following:

CAPEX/Sales: 2.8% (CAPEX/Sales < 5%? ✅)

CAPEX/Operating Cash Flow: 5.3% (CAPEX/Operating CF? < 25% ✅)

These numbers already look way more attractive.

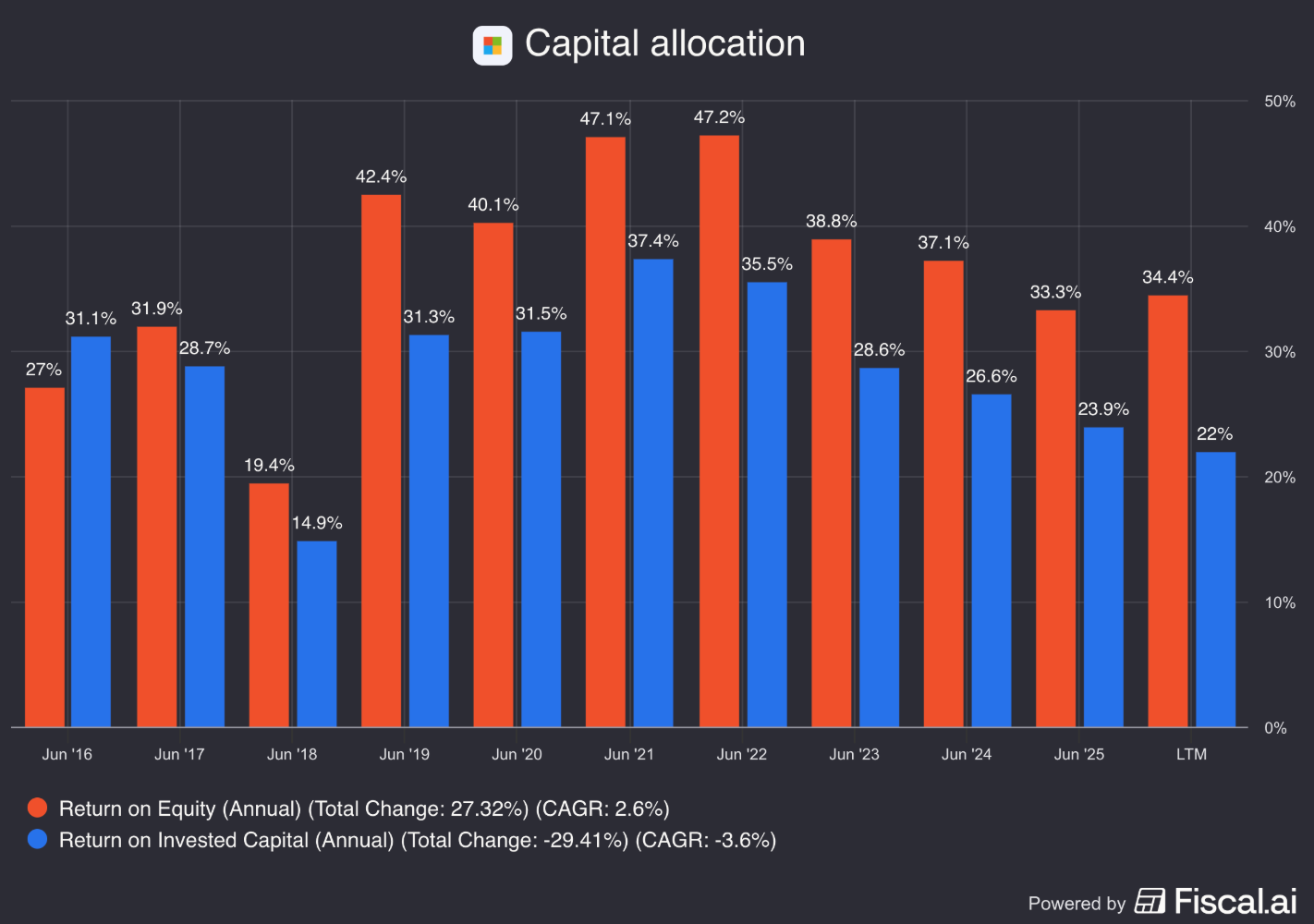

8. Is the company a great capital allocator?

Capital allocation is the most important task of management.

Look for companies that put the money of shareholders to work at attractive rates of return.

Microsoft:

Return On Equity: 34.4% (ROE > 20%? ✅)

Return On Invested Capital: 22.0% (ROIC > 15%? ✅)

These numbers look attractive.

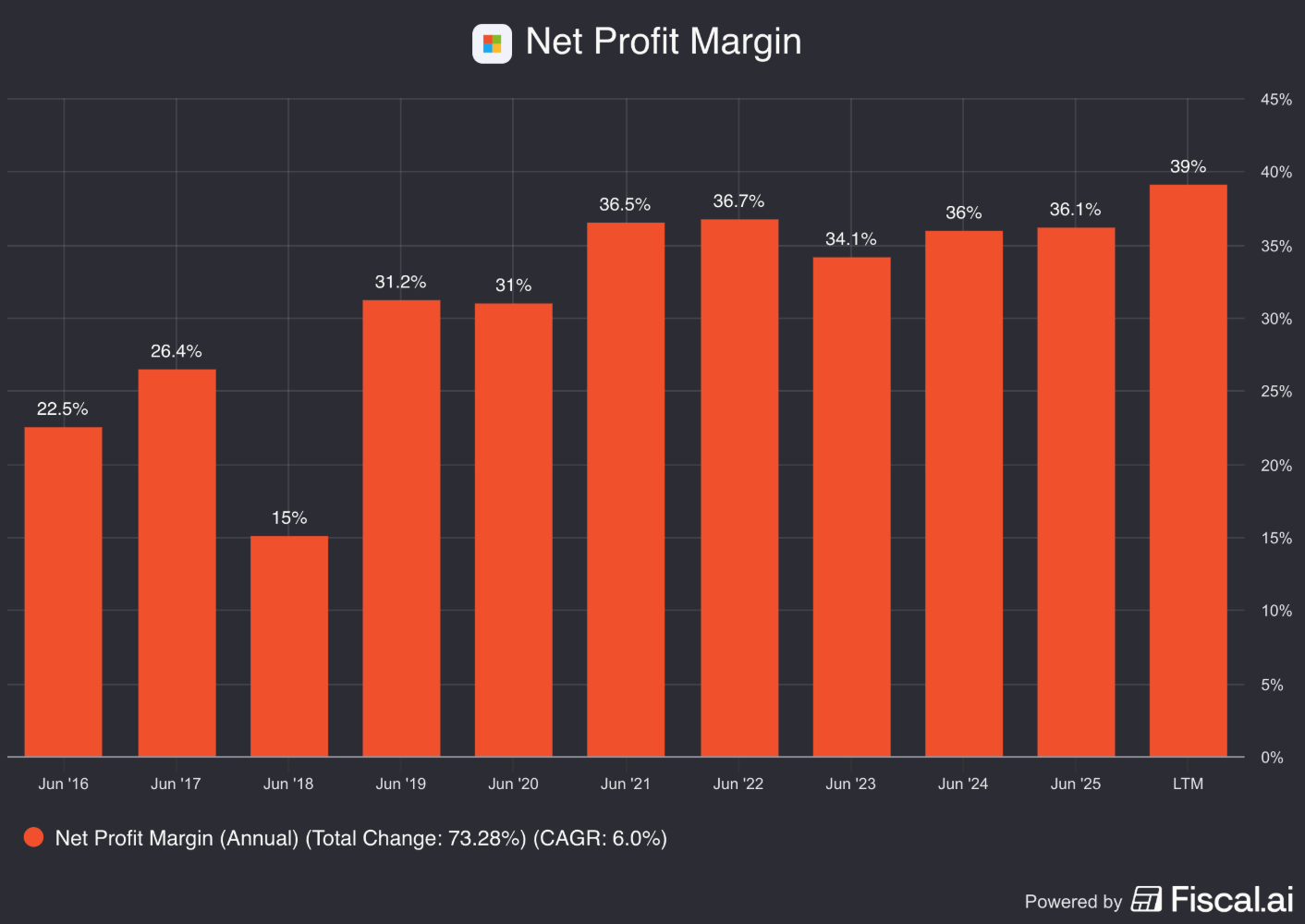

9. How profitable is the company?

The higher the profitability of the company, the better.

Here’s what things look like for Microsoft:

Gross Margin: 68.6% (Gross Margin > 40%? ✅)

Net Profit Margin: 39.0% (Net Profit Margin > 10%? ✅)

Average FCF/Net Income past 5 years: 80.4% (FCF/Net Income > 80%? ✅)

Microsoft’s is a very profitable company.

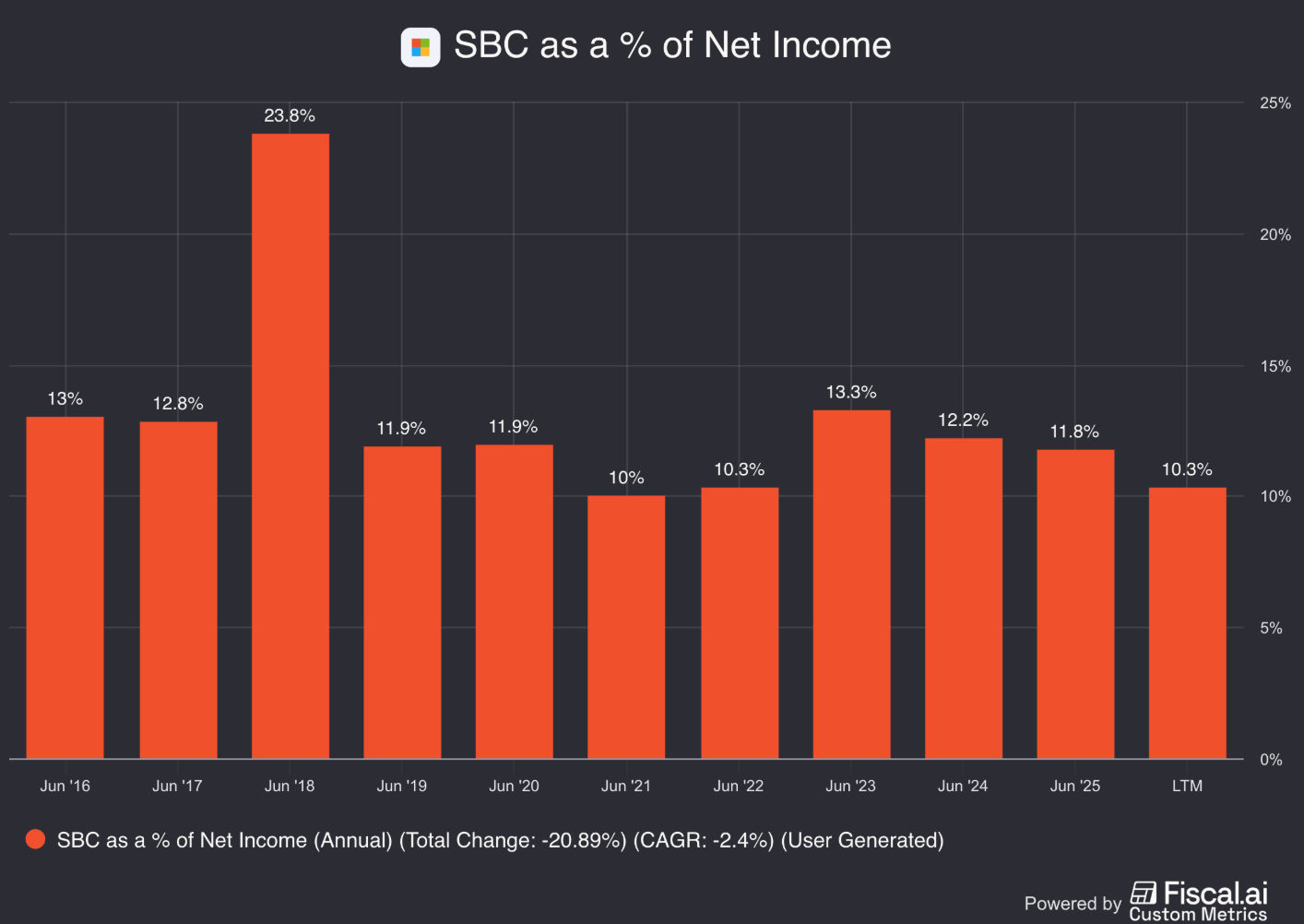

10. Does the company use a lot of Stock-Based Compensation?

Stock-based compensation is a cost for shareholders and should be treated accordingly.

Preferably we want SBCs as a % of Net Income to be lower than 4% and certainly below 10%.

Microsoft:

SBCs as a % of Net Income: 10.3% (SBCs/Net Income < 10%? ❌)

Avg. SBC as a % of Net Income past 5 years: 11.3% (SBCs/Net Income < 10%? ❌)

As you can see, Microsoft uses quite some Stock-Based Compensation.

This is a cost for shareholders like us. We will take this into our valuation models (see later).

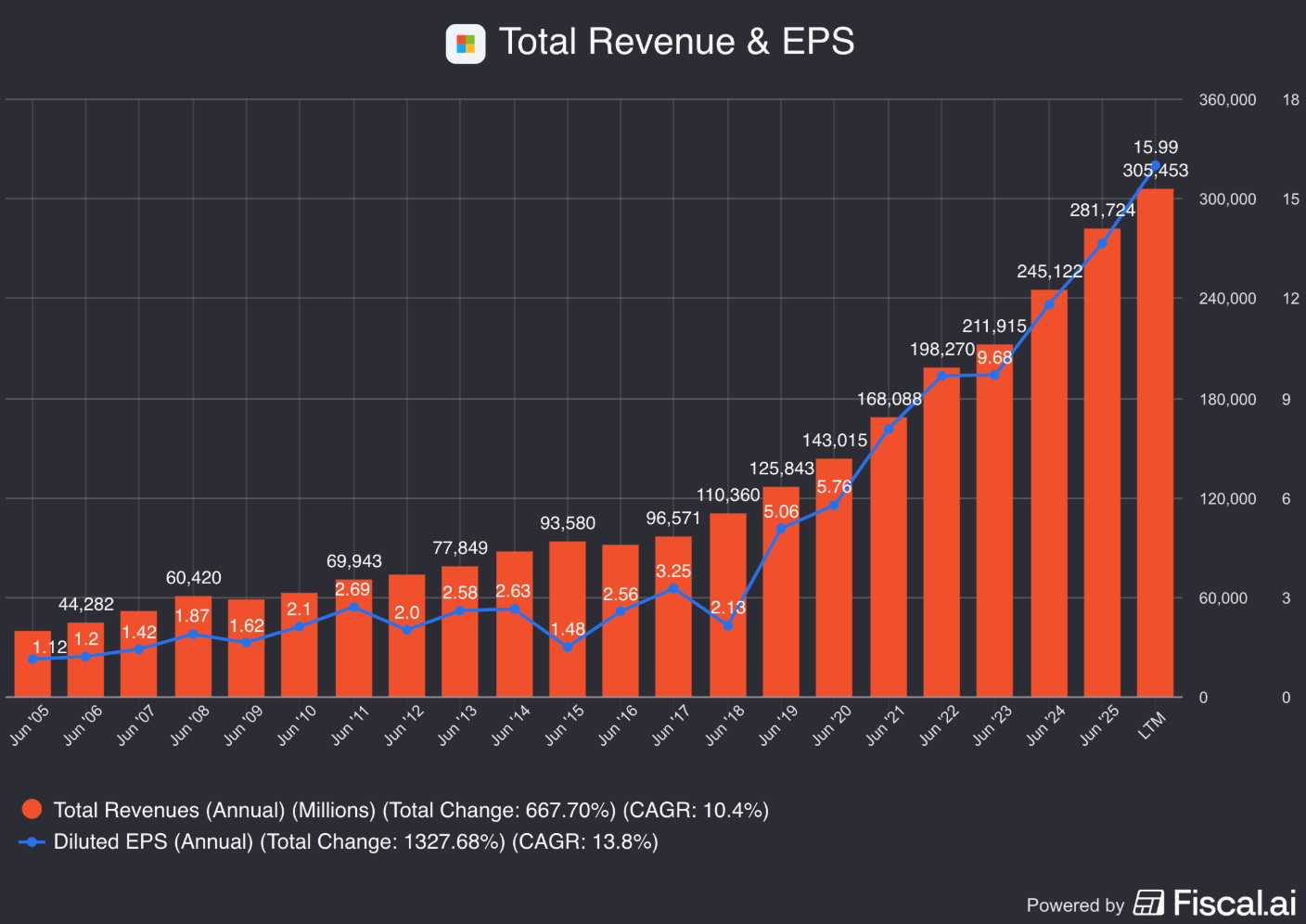

11. Did the company grow at attractive rates in the past?

We look for companies that managed to grow their revenue and EPS by at least 5% and 7% per year respectively.

Microsoft:

Revenue Growth past 5 years (CAGR): 14.8% (Revenue growth > 5%? ✅)

Revenue Growth past 10 years (CAGR): 13.2% (Revenue growth > 5%? ✅)

EPS Growth past 5 years (CAGR): 19.0% (EPS growth > 7%? ✅)

EPS Growth past 10 years (CAGR): 27.2% (EPS growth > 7%? ✅)

These growth figures look attractive.

12. Does the future look bright?

You want to invest in companies that manage to grow at attractive rates as stock prices tend to follow FCF per share growth over time.

Microsoft:

Exp. Revenue Growth next 2 years (CAGR): 15.9% (Revenue growth > 5%? ✅)

Exp. EPS Growth next 2 years (CAGR): 18.0% (EPS growth > 7%? ✅)

EPS Long-Term Growth Estimate: 13.5% (EPS growth > 7%? ✅)

This outlook looks attractive.

13. Does the company trade at a fair valuation level?

Now let’s dive into the valuation.

It’s very important as even the best company in the world can be a horrible investment if you pay too much for it.