📈 Should you invest in Tesla today?

Tesla is the most valuable car company in the world.

But it’s way more than a car company. Elon Musk is working on many other things. Think about robotaxis and robots.

Does this make it an interesting investment? Let’s find out today.

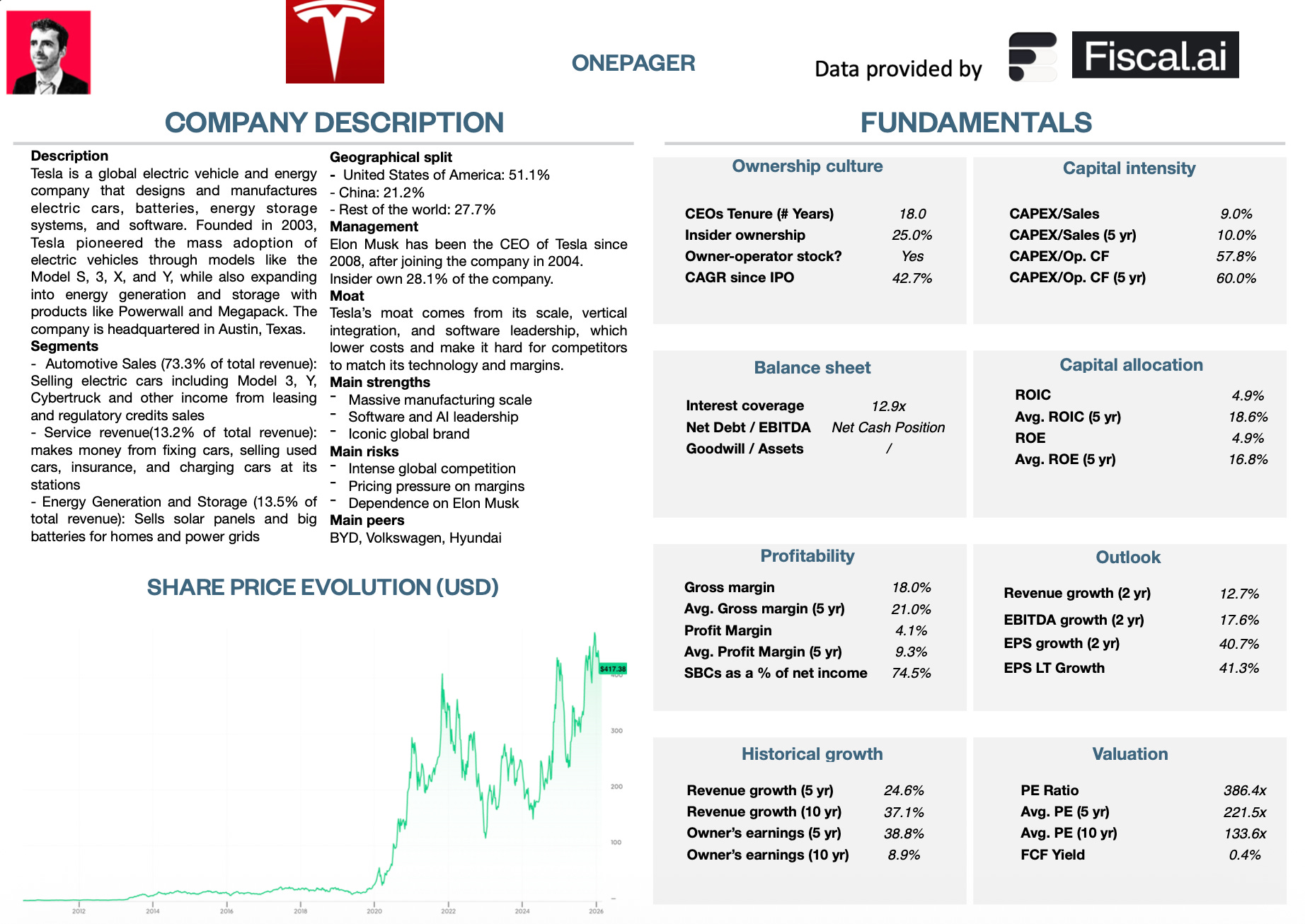

Tesla,Inc. - General Information

👔 Company name: Tesla, Inc.

✍️ ISIN: US88160R1014

🔎 Ticker: TSLA

📚 Type: Owner-Operator

📈 Stock Price: $417.3

💵 Market cap: $1.3 trillion

📊 Average daily volume: $27.9 billion

Onepager

Here’s a onepager with the essentials of Tesla.

(Click on the picture to expand)

15-Step Approach

Now let’s use our 15-step approach to analyze the company.

At the end of this article, we’ll give Tesla a score on each of these 15 metrics.

This results in a Total Quality Score.

1. Do I understand the business model?

"I’d rather be optimistic and wrong than pessimistic and right.” — Elon MuskThis is the mindset that made Tesla the most valuable car company in the world.

In 2003, two engineers decided to build an electric car that people actually wanted to drive.

But they had a problem… They didn’t have any money.

Elon Musk solved that problem.

He joined in 2004, betting his entire fortune on the idea.

He turned out to be right, and today, he is the richest person on earth.

Tesla has become much more than a car company. It’s now working on building robots and autonomous vehicles.

On top of that, it’s also an energy giant.

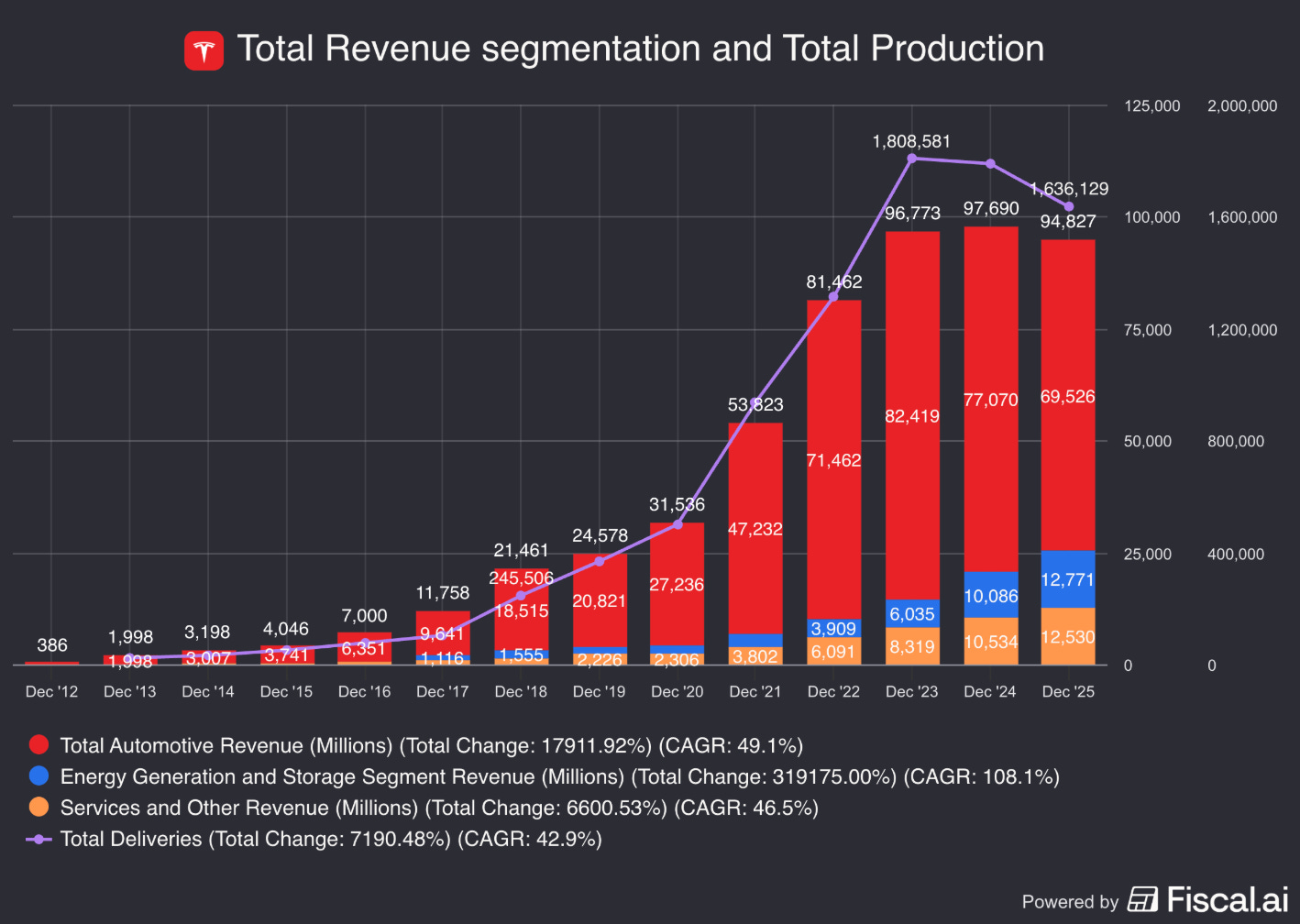

Tesla makes money in three ways:

Automotive Sales (73.3% of sales): Selling electric cars and its Cybertruck

Energy Generation and Storage (13.5% of sales): Solar panels and batteries (Megapacks) sold to store power for cities and data centers

This is the fastest growing segment of Tesla

Services (13.2% of sales): Recurring cash from fixing cars, charging stations, and software subscriptions (like Self-Driving)

Tesla has intentionally slowed down production to upgrade their factories and prepare for the next big wave: Robotaxis and AI robots.

2. Is management capable?

Elon Musk is the face of Tesla, but he didn’t start the company.

He joined as an early investor in 2004 and stepped in as CEO in 2008 to save Tesla from bankruptcy.

Critics often worry that Musk is spread too thin with Tesla, SpaceX, X (Twitter), and xAI.

However, his personal wealth is tied directly to Tesla’s success:

Musk owns approximately 24.9% of Tesla.

That stake makes up over 48% of his $849 billion net worth (as of Feb 2026).

The other thing that helps ease this concern?

Musk doesn’t run the day-to-day operations himself.

While Elon handles the big vision and the headlines, Tom Zhu (Senior VP of Automotive) is the one actually running the factories.

Tom is the leader on the ground who makes sure things are running smoothly.

3. Does the company have a sustainable competitive advantage?

“The factory is the machine that builds the machine.” — Elon MuskMaking cars is incredibly difficult.

It costs billions of dollars to build factories, and if you don’t sell enough cars, you go bankrupt.

Tesla has three things working in its favor:

Low Production Costs: Unlike traditional manufacturers, Tesla stamps out many of its parts in one piece, making them faster and cheaper to build

Sticky Ecosystem: Like Apple, once you start using their software and chargers, you never want to switch brands

Data Advantage: Every day, millions of Teslas record hours of real-world driving footage. This trains their computers to become better drivers

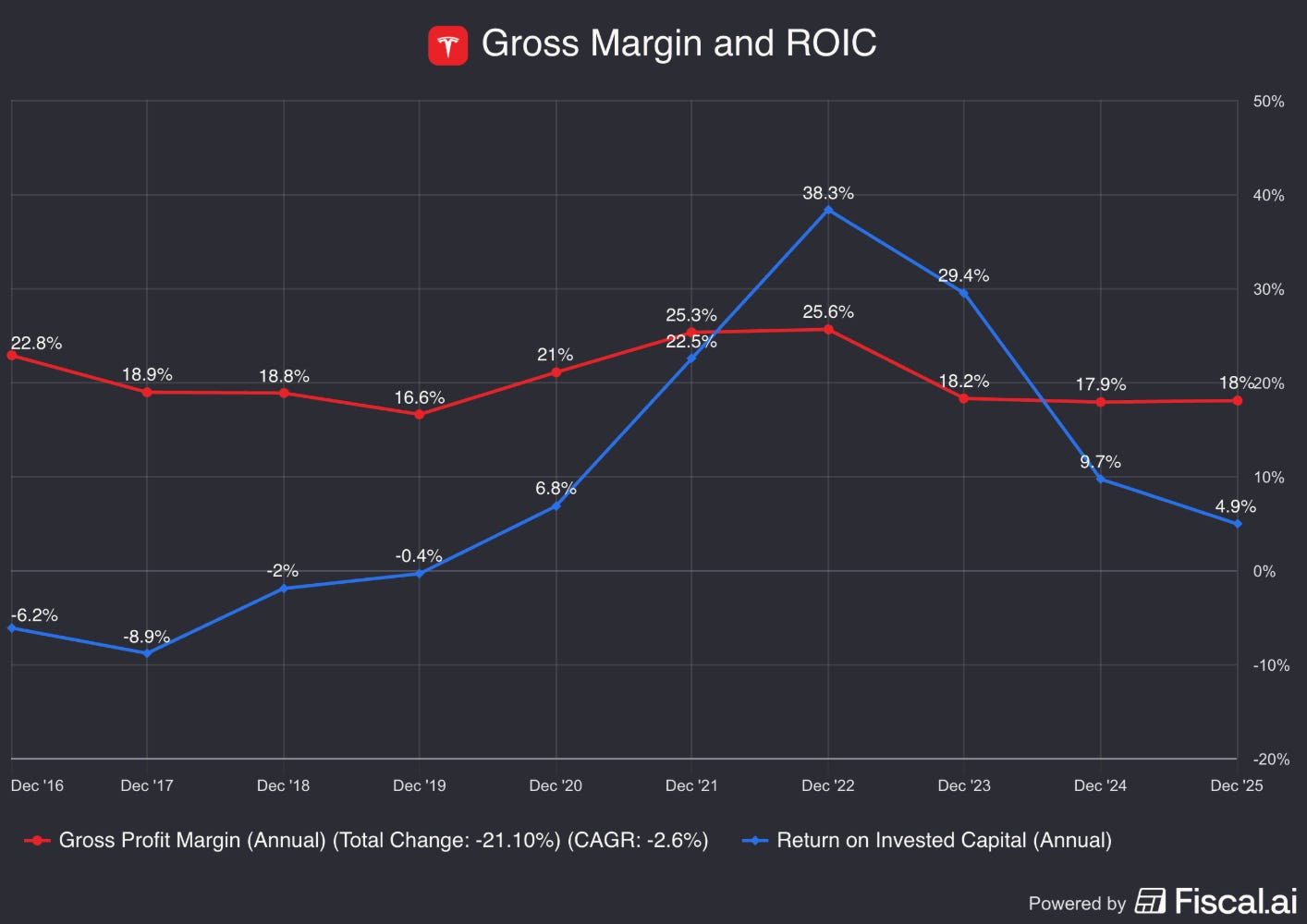

Companies with a sustainable competitive advantage are often characterized by the following:

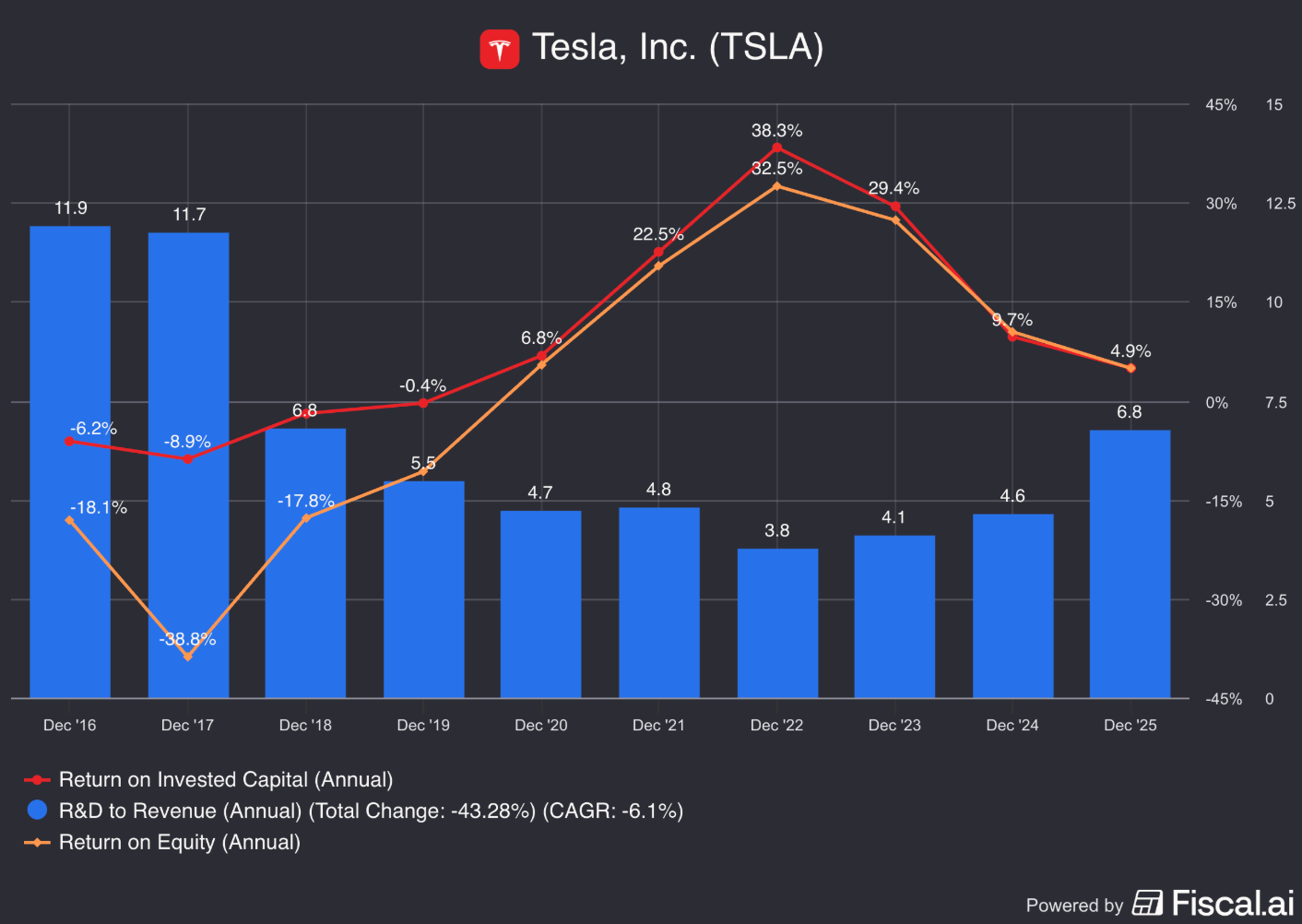

Gross Margin: 18.0% (Gross Margin > 40%? ❌)

Return On Invested Capital (ROIC): 4.9% (ROIC > 15%? ❌)

These numbers don’t look good, but they don’t tell the entire story.

Tesla is building the technology of the future. It requires massive upfront investment before the profits arrive.

As more people adopt Tesla’s technology, two things happen:

Costs Drop: Manufacturing becomes cheaper as they build more units (economies of scale).

Profits Rise: Once the expensive research and development is done, every new car or robot sold has much higher margins

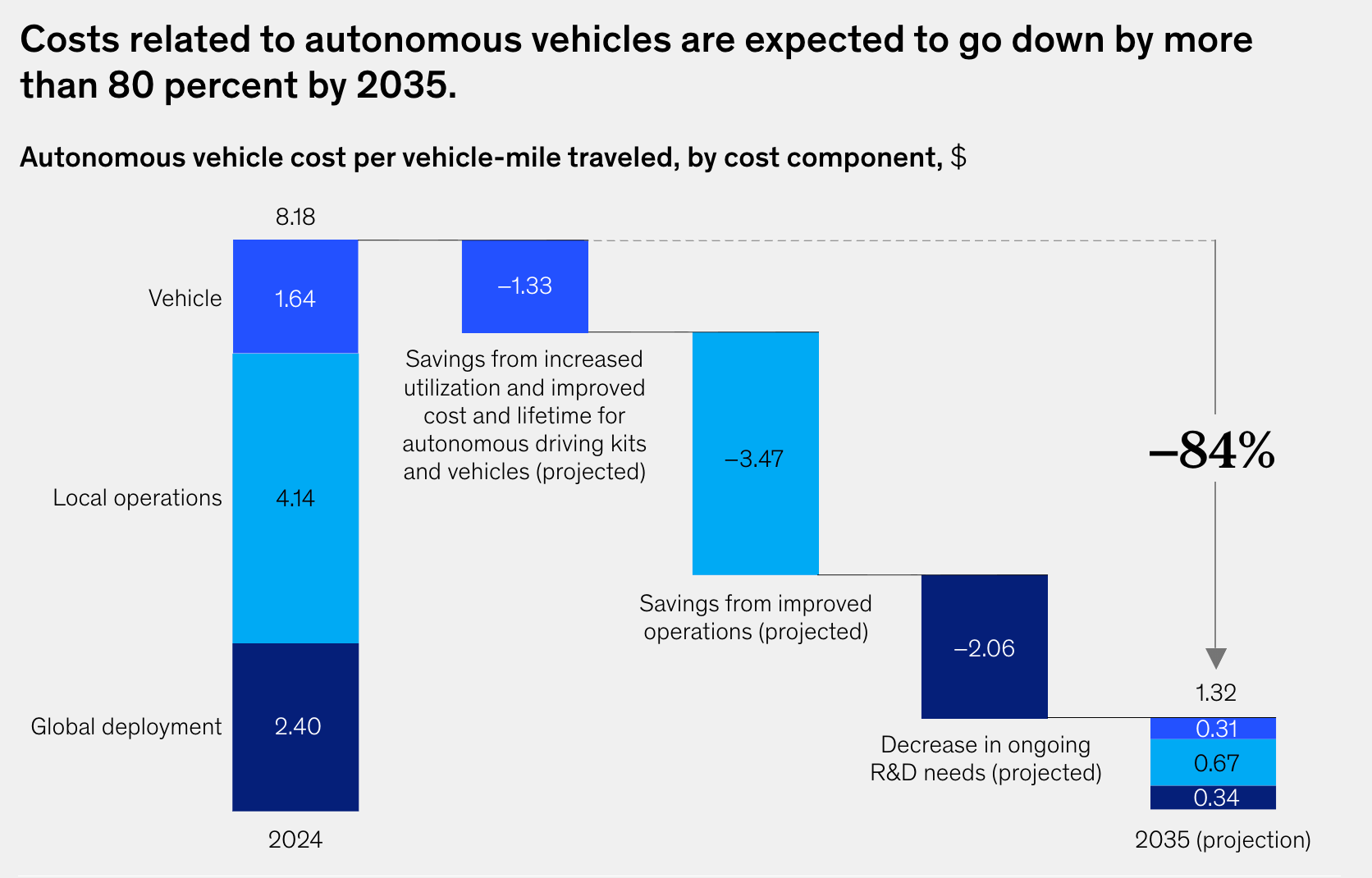

The global consulting firm McKinsey supports this idea, with costs of autonomous vehicles like Tesla’s expected to drop by 80% over the next decade.

4. Is the company active in an attractive end market?

Tesla operates in multiple attractive end markets.

Electric Cars

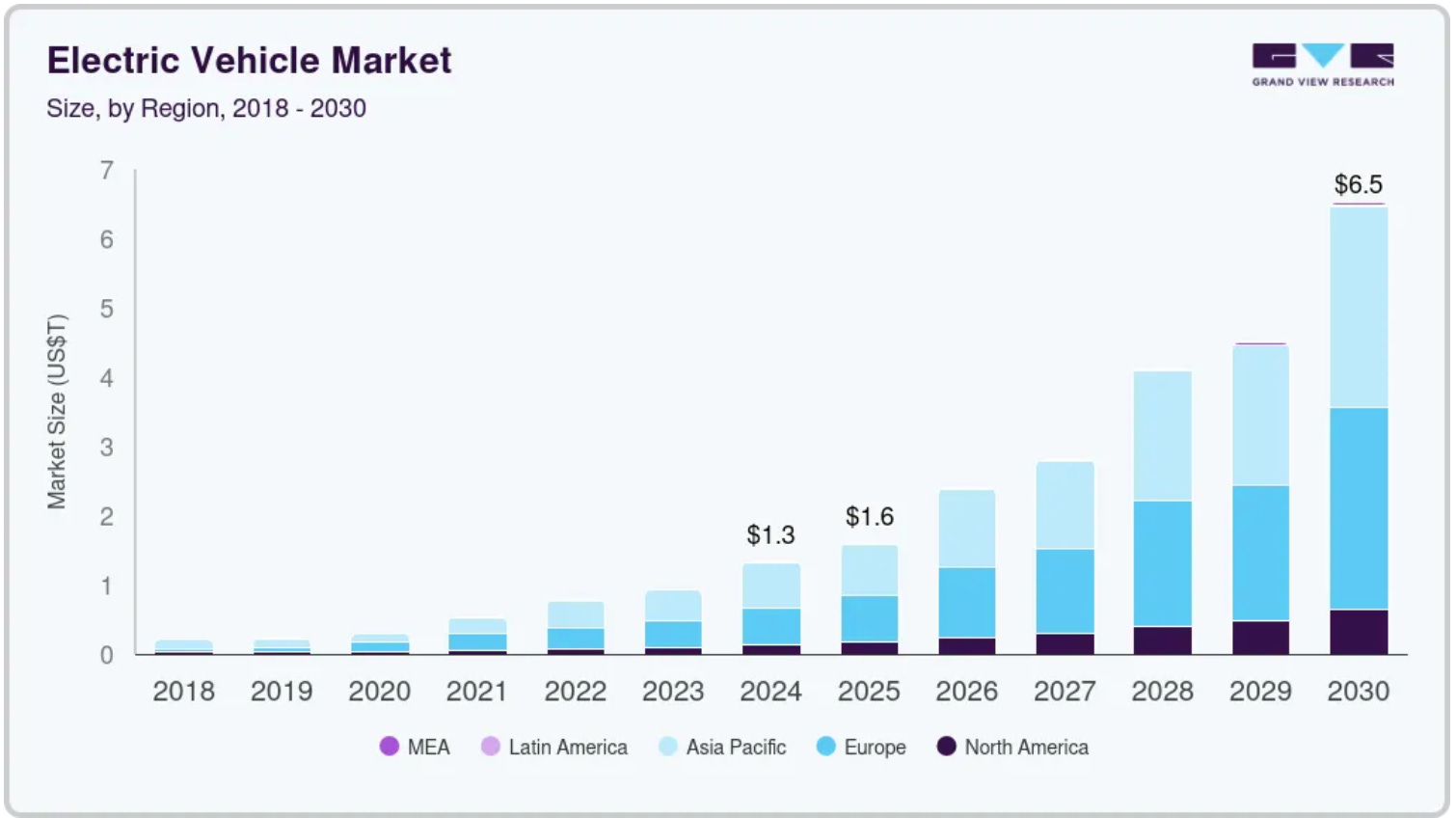

The global electric vehicle market is projected to reach over $6 trillion by 2030 growing at a 32% CAGR.

Energy Storage

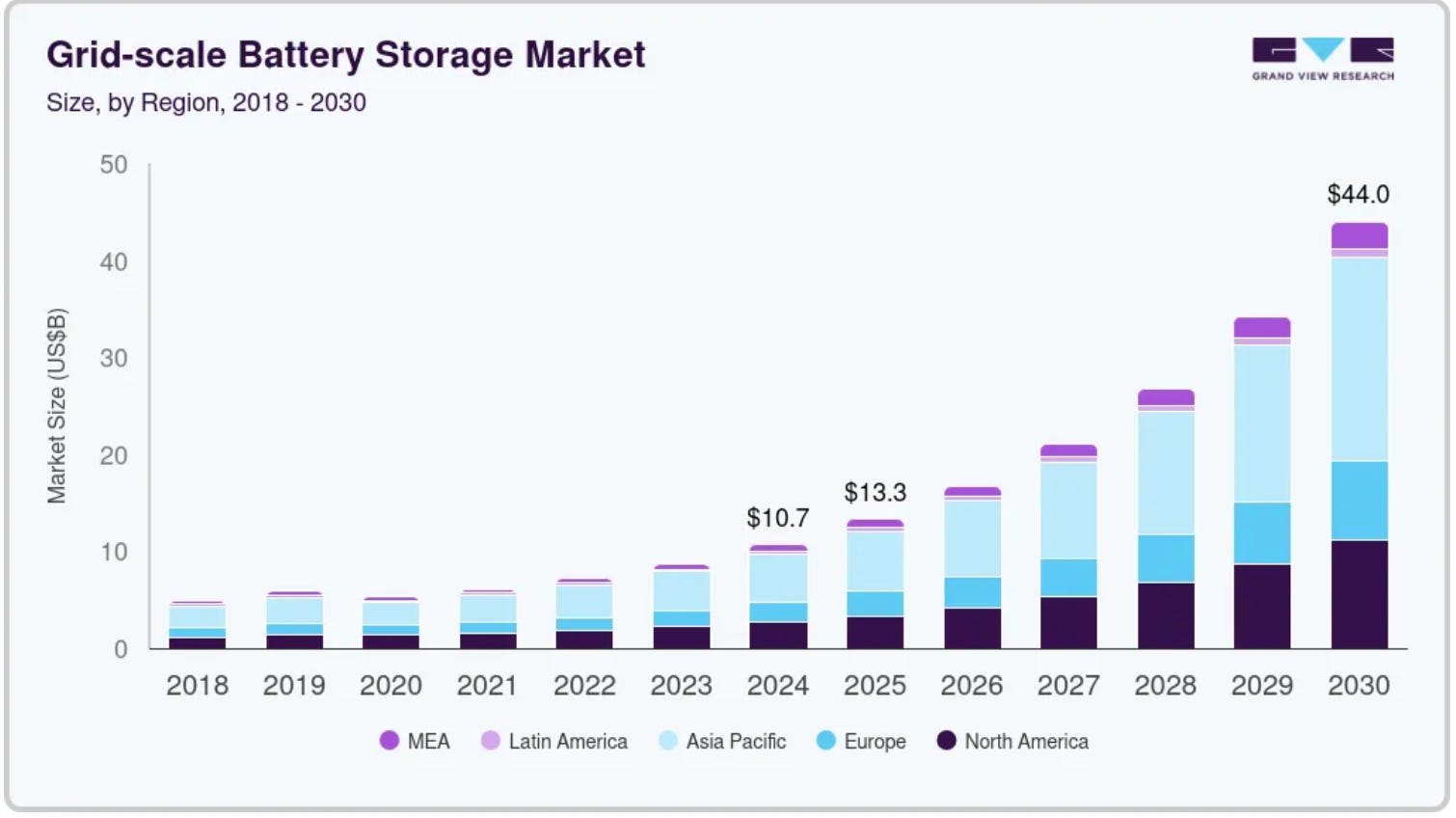

The grid-scale battery market is expected to grow at a 27% CAGR until 2030.

Robotaxis (AI)

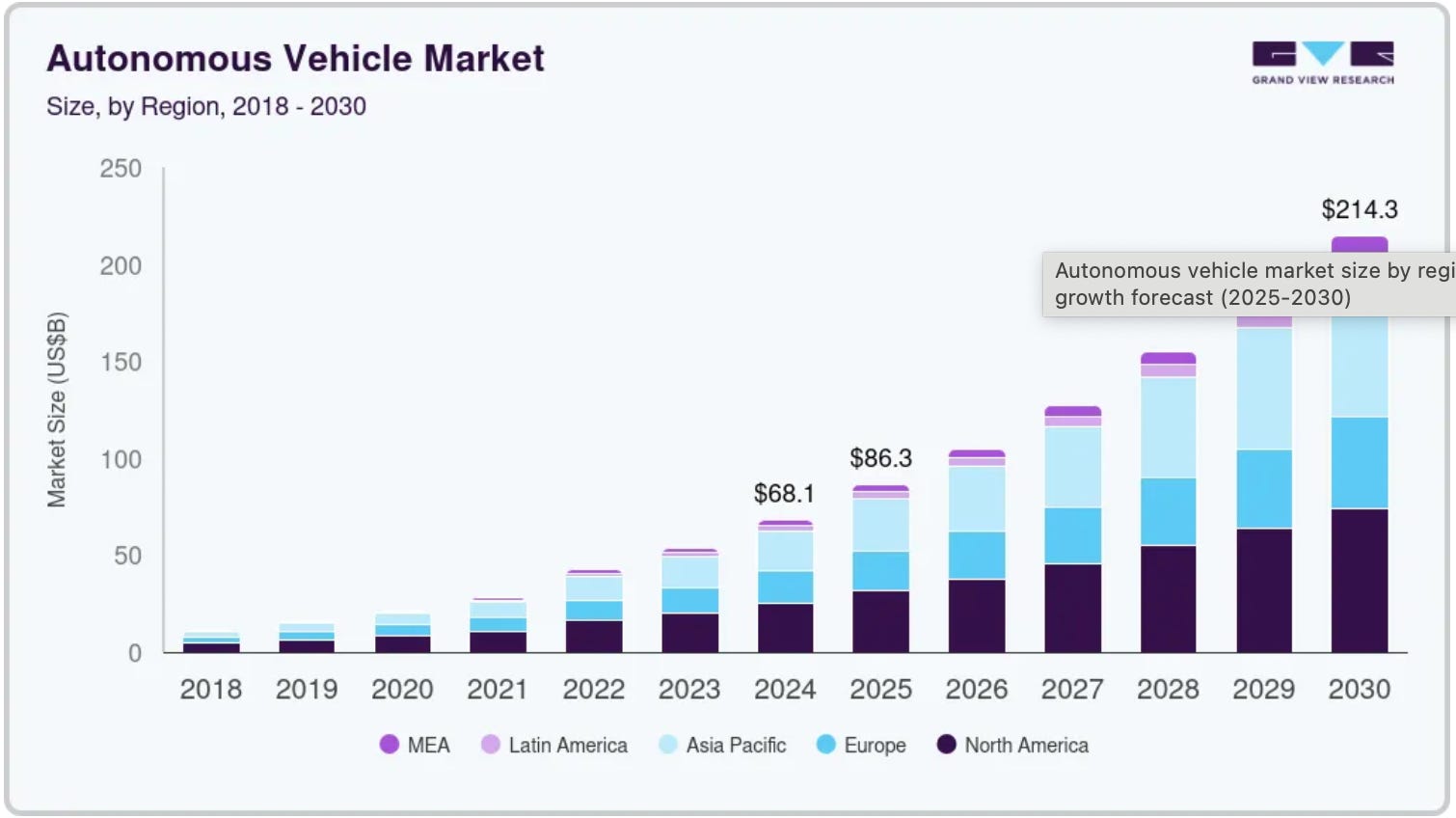

The global autonomous vehicle market is projected to reach over $214 billion by 2030 growing at a 19.9% CAGR.

Tesla benefits from a strong growth trend in all three markets.

But the business also faces a lot of intense competition in each:

BYD (China): They sell more electric cars than anyone else in the world and make their own batteries at a very cheap price

CATL: They supply Tesla with batteries, but they also supply everyone else, giving competitors the same great technology

Waymo (Google): The leader in Robotaxis, with driverless cars already picking up passengers in cities like Phoenix and San Francisco

5. What are the main risks for the company?

Here are the key risks for Tesla:

Intense competition: Tesla faces competition from BYD, Xiaomi, Waymo, and legacy automakers

Regulatory hurdles: Governments are investigating Full Self-Driving safety and trade wars threaten the Shanghai factory

Product Delays: Tesla has a history of delaying new products (Cybertruck, Roadster, Robotaxi), which can frustrate investors relying on future growth

Economic sensitivity: Cars are expensive purchases. High interest rates significantly reduce demand for vehicles

Elon Musk: He’s a genius and a wildcard. His tweets move the stock, his politics alienate buyers, and he runs 5 companies at once, bringing a lot of unpredictability

Rich valuation level: We’ll talk about this later

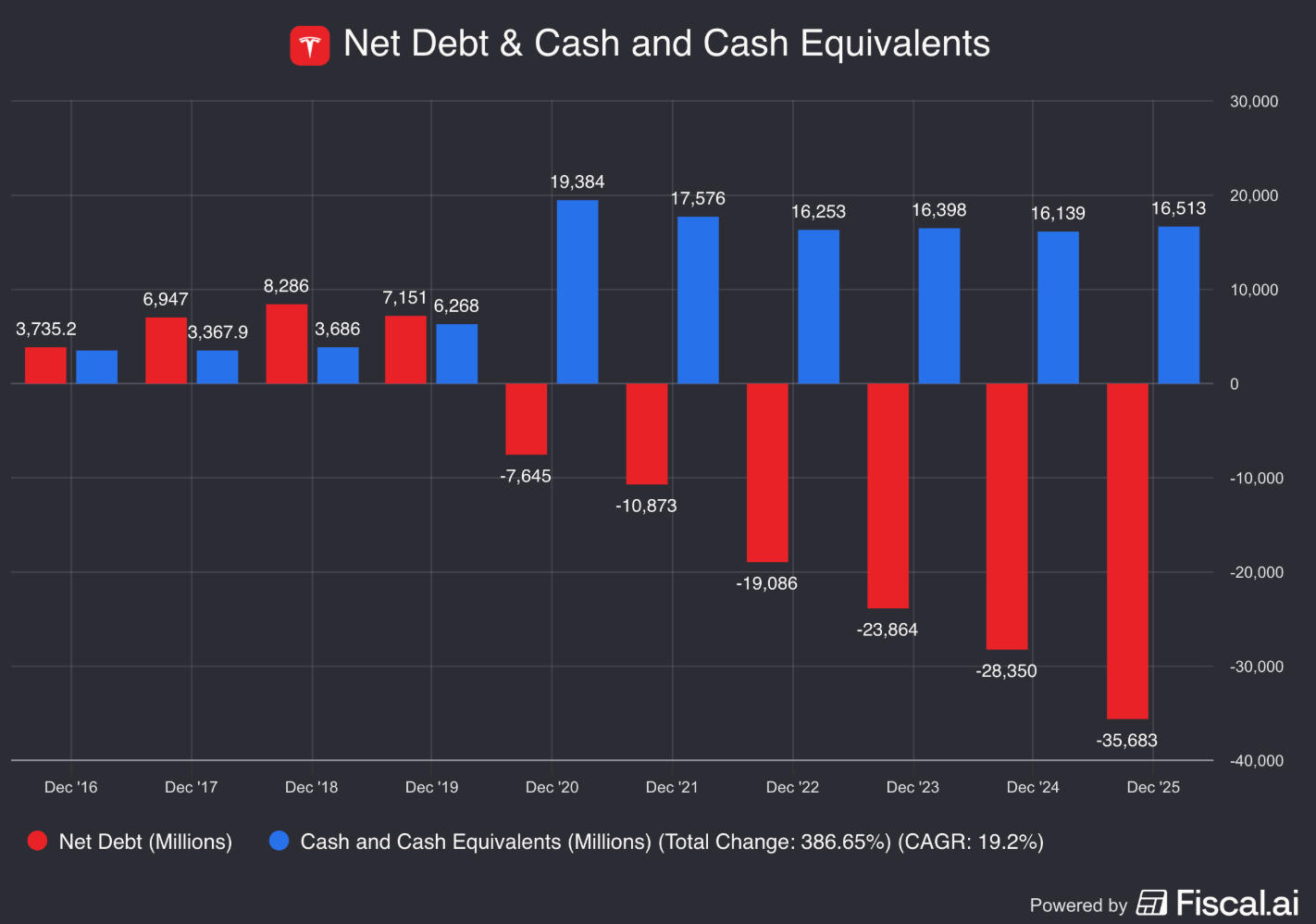

6. Does the company have a healthy balance sheet?

We look at three ratios to determine the healthiness of Tesla’s balance sheet:

Interest Coverage: 12.9x (Interest Coverage > 15x? ❌)

Net Debt/FCF: Net Cash Position (Net Debt/FCF < 4x? ✅)

Tesla has a very healthy balance sheet.

7. Does the company need a lot of capital to operate?

We prefer companies that don’t need a lot of capital to operate.

Here’s how Tesla looks:

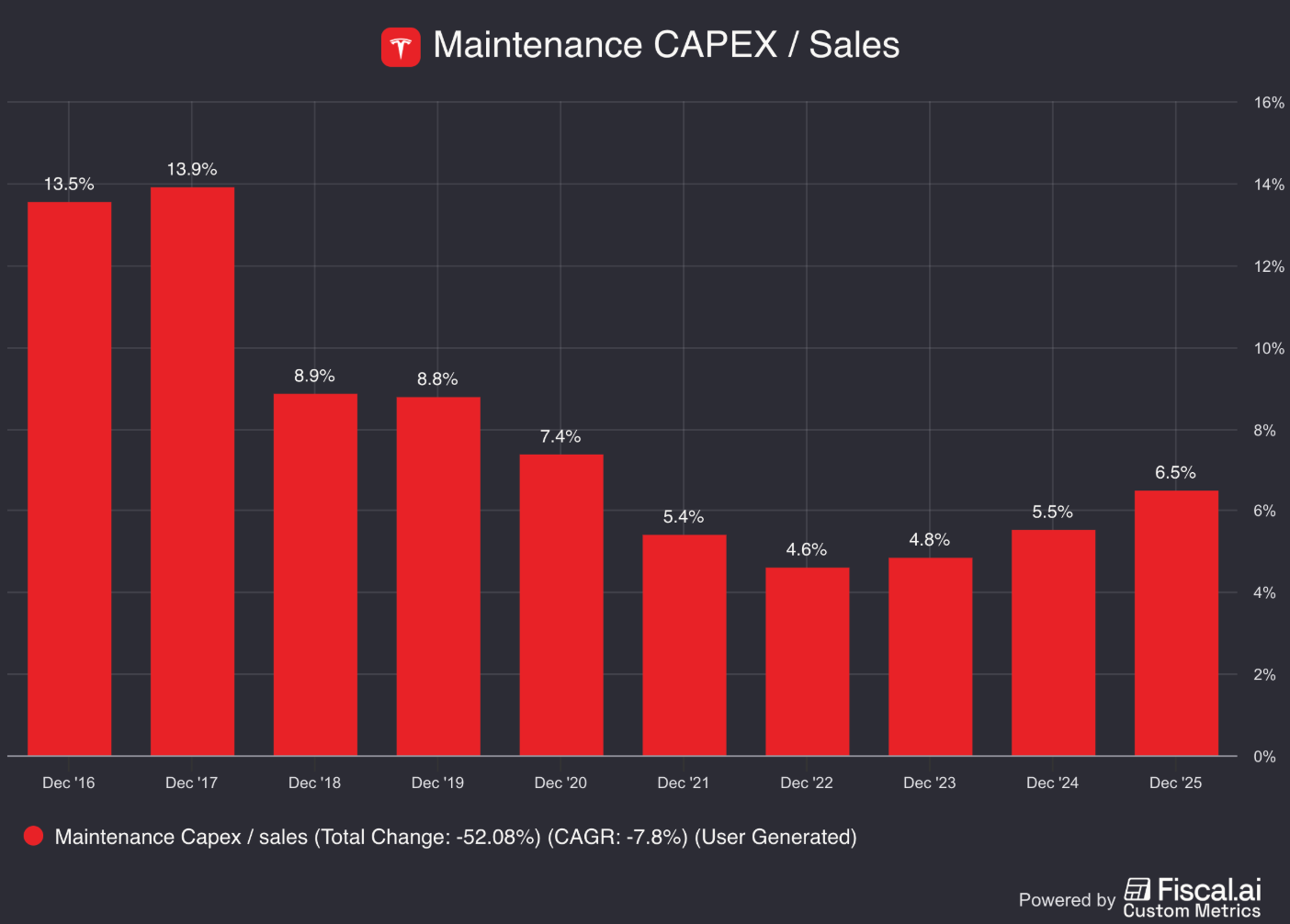

CAPEX/Sales: 9.0% (CAPEX/Sales < 5%? ❌)

CAPEX/Operating Cash Flow: 57.8% (CAPEX/Operating CF? < 25% ❌)

At first glance, Tesla looks capital-heavy.

But remember… there is a difference between Maintenance CAPEX and Growth CAPEX.

Maintenance CAPEX: Investments made in existing assets

Growth CAPEX: Investments made in new assets to grow

When a company invests a lot to grow, its growth CAPEX is very high.

These investments might actually create a lot of value in the long term.

That’s why sometimes (like for Tesla) it might make sense to only take the company’s Maintenance CAPEX into account.

As a rule of thumb, we state that the company’s maintenance CAPEX is equal to the company’s Depreciation & Amortization.

CAPEX = Maintenance CAPEX + Growth CAPEX

Wherein Maintenance CAPEX = Depreciation & Amortization

When we do the calculations for Tesla

Maintenance CAPEX/Sales: 6.5% (CAPEX/Sales < 5%? ❌)

Maintenance CAPEX/Operating Cash Flow: 41.7% (CAPEX/Operating CF? < 25% ❌)

These numbers look more reasonable, but Tesla is still a capital intensive business.

On top of that, they are also investing heavily in future growth.

AI & Computing: Buying thousands of Nvidia chips to train their Self-Driving AI

Gigafactories: Building and expanding huge plants in Texas, Berlin, and Shanghai

New Tech: Developing the Cybercab and the Optimus robot

These future growth investments could yield high returns in the future.

8. Is the company a great capital allocator?

Capital allocation is the most important task of management.

We like to invest in companies that put shareholders’ money to use at attractive rates of return.

Tesla:

Return On Equity (ROE): 4.9% (ROE > 20%? ❌)

Return On Invested Capital (ROIC): 4.9% (ROIC > 15%? ❌)

As we already mentioned, Tesla is heavily investing in projects that aren’t profitable yet. This brings the ratios down.

9. How profitable is the company?

The higher the profitability of the company, the better.

Here’s what things look like for Tesla:

Gross Margin: 18.0% (Gross Margin > 40%? ❌)

Net Profit Margin: 4.1% (Net Profit Margin > 10%? ❌)

The Gross and Net Margins look low, but that’s a purposeful choice by Tesla.

Tesla has intentionally reduced manufacturing for factory upgrades

Reduced the car prices and engaged in a price war with Chinese EV companies

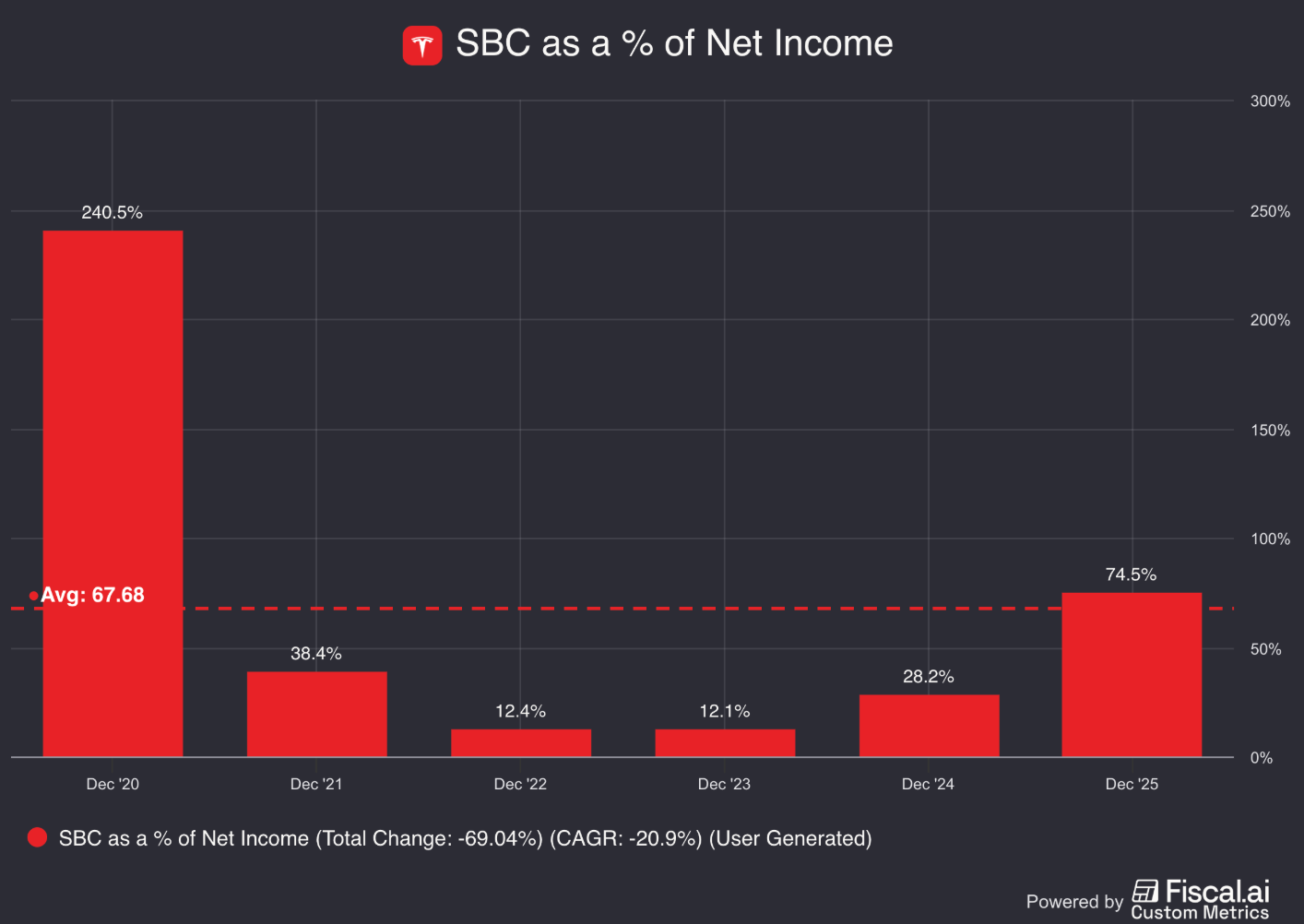

10. Does the company use a lot of Stock-Based Compensation?

Stock-based compensation is a cost for shareholders and should be treated accordingly.

Tesla:

SBCs as a % of Net Income: 74.5% (SBCs/Net Income < 10%? ❌)

Avg SBC as a % of Net Income past five years: 67.7% (SBCs/Net Income < 10%? ❌)

Tesla uses a lot of Stock-Based Compensation.

This is not something you want to see as a quality investor.

We will take this into account in our valuation model later on.

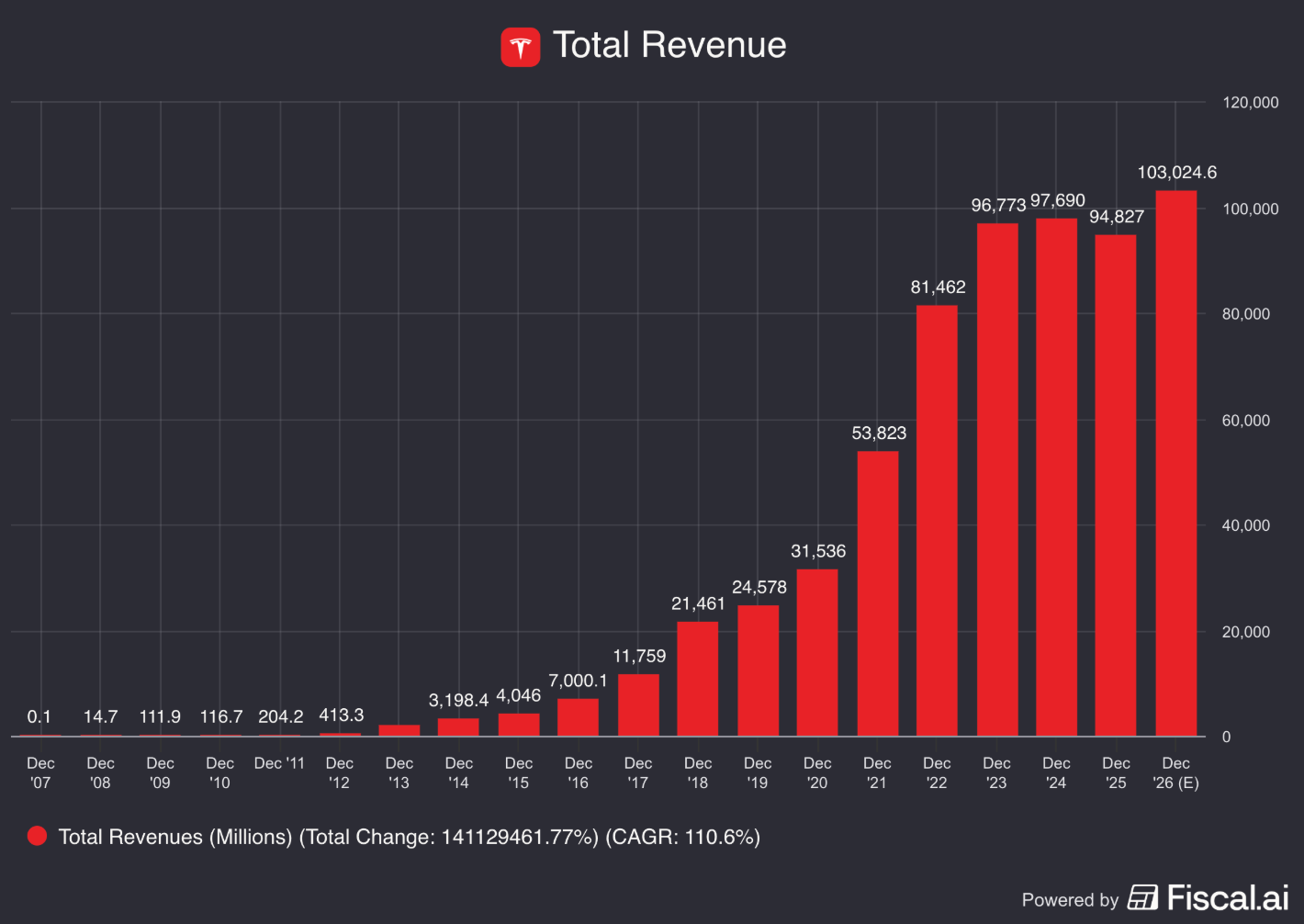

11. Did the company grow at attractive rates in the past?

We seek companies that managed to grow their revenue and EPS by at least 5% and 7% per year, respectively.

Tesla:

Revenue Growth past 5 years (CAGR): 24.6% (Revenue growth > 5%? ✅)

Revenue Growth past 10 years (CAGR): 37.1% (Revenue growth > 5%? ✅)

EPS Growth past 5 years (CAGR): 38.8% (EPS growth > 7%? ✅)

EPS Growth past 10 years (CAGR): 8.9% (EPS growth > 7%? ✅)

Tesla has grown at very attractive rates in the past.

12. Does the future look bright?

We want to invest in businesses that can keep growing attractively.

Tesla:

Exp. Revenue Growth next two years (CAGR): 12.7% (Revenue growth > 5%? ✅)

Exp. EPS Growth next two years (CAGR): 40.7% (EPS growth > 7%? ✅)

EPS Long-Term Growth Estimate: 41.3% (EPS growth > 7%? ✅)

While in the short-term Tesla might face difficulties, the future stills looks bright in terms of growth prospects.