Text SA: Where's the moat?

Investment case Text SA

Last week, you learned that Text SA makes money from selling B2B subscriptions for managing online business communications.

A positive thing? Almost all its revenue is recurring in nature.

Today, you’ll learn more about the company’s management team, moat, and its key risks.

Investment Case Text SA

👔 Company name: Text SA

✍️ ISIN: PLLVTSF00010

🔎 Ticker: $LCHTF

📚 Type: Owner-Operator Stock

📈 Stock Price: 110.4 PLN ($27.9)

💵 Market cap: 2.84 billion PLN ($718 million)

📊 Average daily volume: 3.6 million PLN ($900k)

You don’t want to read the entire case?

Scroll down to the bottom of this analysis and find out whether we’re buying Text SA or not.

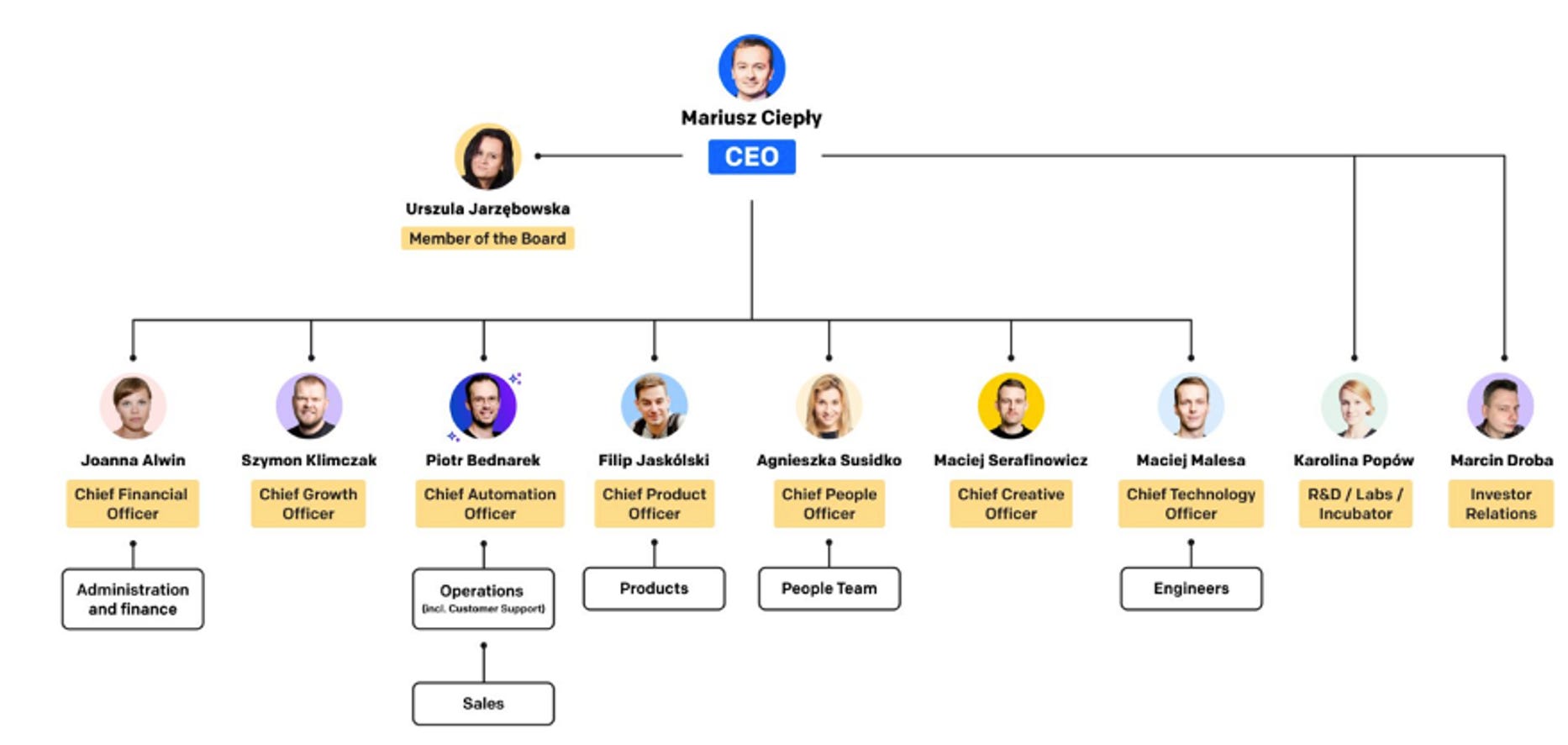

Is management capable?

Text SA was founded in 2002 by Jakub Sitarz, Mariusz Ciepły, and Maciej Jarzębowski.

Today, Mariusz Cieply is still the CEO and President of the Board and one of the main shareholders of the company.

Jakub Sitarz and Maciej Jarzębowski are also still active within Text SA. Maciej serves as Chairman of the Supervisory Board while Jakub serves as Vice-Chairman of the Supervisory Board.

Urszula Jarzębowska has been working for the company since 2002 and serves as an important Partner for Mariusz Cieply. She’s also a member of the board.

It’s great to see that both Urszula as Mariusz are working for the company since Text SA was founded in 2002.

Here’s how the organizational structure of Text SA looks like:

In total, insiders own 41.6% of the company, indicating that we’re talking about an owner-operator stock.

Jakub Sitarz: owns 11.7% of Text SA

Mariusz Ciepły: owns 13.1% of Text SA

Maciej Jarzębowski: owns 9.2% of Text SA

Urszula Jarzębowska: owns 4.7% of Text SA

Other insiders: own 2.9% of Text SA

Currently, the company focuses a lot on AI and automation. They want to automate the work they do on a daily basis.

To give an example, Text SA no longer has a Chief Operating Officer and Piotr Bednarek, who was the COO, now holds the position of Chief Automation Officer.

Employees of the company give Text SA a score of 4/5. This is a good score.

Quality Score - Capability Management: 9/10

The 3 founders are still involved in the company and insiders own more than 40% of Text SA. Under current management, the company has built a strong track record in creating shareholder value.

That’s why the company gets a score of 9/10 for its management.

Does the company have a sustainable competitive advantage?

Text SA targets companies of all sizes representing all industries. One of their significant competitive advantages is a very effective, automated sales process for small and medium-sized companies.

In the future, the company wants to maintain this advantage while focusing on medium-sized companies. Maintaining a strong position in the small business segment will help them to generate new leads.

Increasing the number of corporate clients will translate into increased predictability of their business and even greater stability.

Over the past 21 years, the company has gained a lot of knowledge and expertise. The company focuses mainly on the US market, which is the largest for Text SA in terms of sales value and future growth potential, but also sets trends for the entire industry.

Furthermore, the company also benefits from economies of scale. Their solutions are used by thousands of companies and millions of end users. This gives the company data and experience that they use for further growth development of its current products and designing new ones The company focuses on implementing projects with the highest potential.

Another benefit of Text’s products is that its products are open and easy to integrate with other solutions provided by external suppliers. Even its API (Application Programming Interface) has become a product in itself.

According to Datanyze, Text SA has over 200 live chat technologies on the market. They have several patents, but they must rather rely on constant development and close contact with its customers. On the bright side, they have a very flexible product, an open API, and management tries to encourage third parties to build add-ons on its marketplace. The company want to remain its competitive edge by being in constant contact with its customers. Text SA is a very large user of its own solutions.

This is what Text SA considers as its sweet spot:

“And our niche, our sweet spot, I would say, we are very good in giving a lot of value to the small or medium companies, which are able to pay for premium solution, but are not big enough to use and pay and be charged for some enterprise level solution and maybe to take solution and just not good for them because they have our own limitation.”

I also asked management about its pricing power:

“Our pricing power would seem low at the first glance. There are a lot of solutions offered in the free or freemium model on our market. However, in November 2022 we increased the prices of LiveChat effectively by an average of 25% (the first increase since 8+ years). Customer churn increased to 4% (the long-term average is 3% per month), but then decreased every next month.”

It’s also noteworthy to state that Zendesk followed Text SA and also announced price increases in May 2023.

Since November 2022, the Average Revenue Per User (ARPU) remained constant (after Text SA increased its prices by 25%).

From January 2019 to today, the ARPU has increased from less than $100 to a bit below $160.

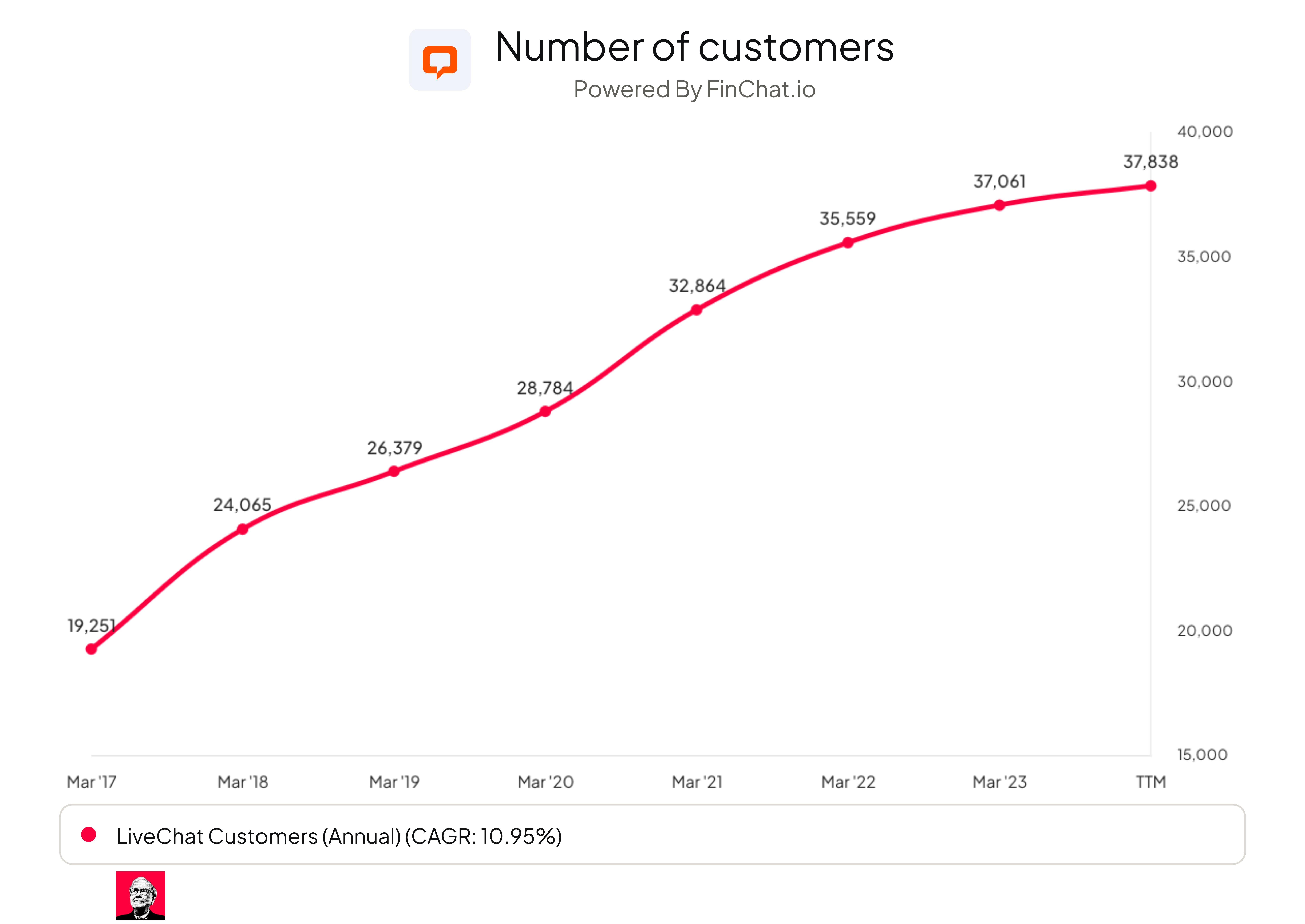

Here’s what the evolution of the number of customers looks like:

To conclude, Text SA has a proven business model with a marginal, close to zero customer acquisition cost. The relatively low level of recurring expenses and the marginal ultimate variable cost of new clients coupled with the absence of the need for additional CAPEX, gives the company a high degree of scalability of its business while retaining strong profit margins.

Companies with a sustainable competitive advantage are often characterized by a high and consistent gross margin as well as ROIC.

Here’s what the situation looks like for Text SA:

As you can see, Text SA has phenomenal margins (more on this later).

Over the past 10 years, its ROIC has never been lower than 180% and its Gross Margin has consistently been higher than 80%.

This indicates that the company has pricing power as well as a sustainable competitive advantage.

Quality Score - Competitive advantage: 7/10

Text SA has a proven business model with a marginal, close to zero customer acquisition cost.

They benefit from economies of scale and have a very high Gross Margin and ROIC. This indicates the company has a competitive advantage as well as pricing power.

As a result, Text SA gets a score of 7/10 for its competitive advantage.

Now let’s dive into competitive environment, the risks the company faces and determine whether we’ll buy Text SA.