Ulta Beauty is up 8%

Earlier this week we added to our position in Ulta Beauty.

The stock will open 8% higher today.

The main reason? Ulta Beauty was too cheap for being such a great company.

Results

Yesterday, Ulta Beauty published its results.

Let’s update you in a few minutes:

Results

Revenue: $2.73 billion vs. $2.72 billion expected

EPS: $6.47 vs. $6.24 expected

Share buybacks (important for Ulta’s investment case):

In Q1, Ulta Beauty bought back 588,004 shares for $285.1 million (average price: $484)

In 2024, Ulta Beauty will buy back shares for $1 billion

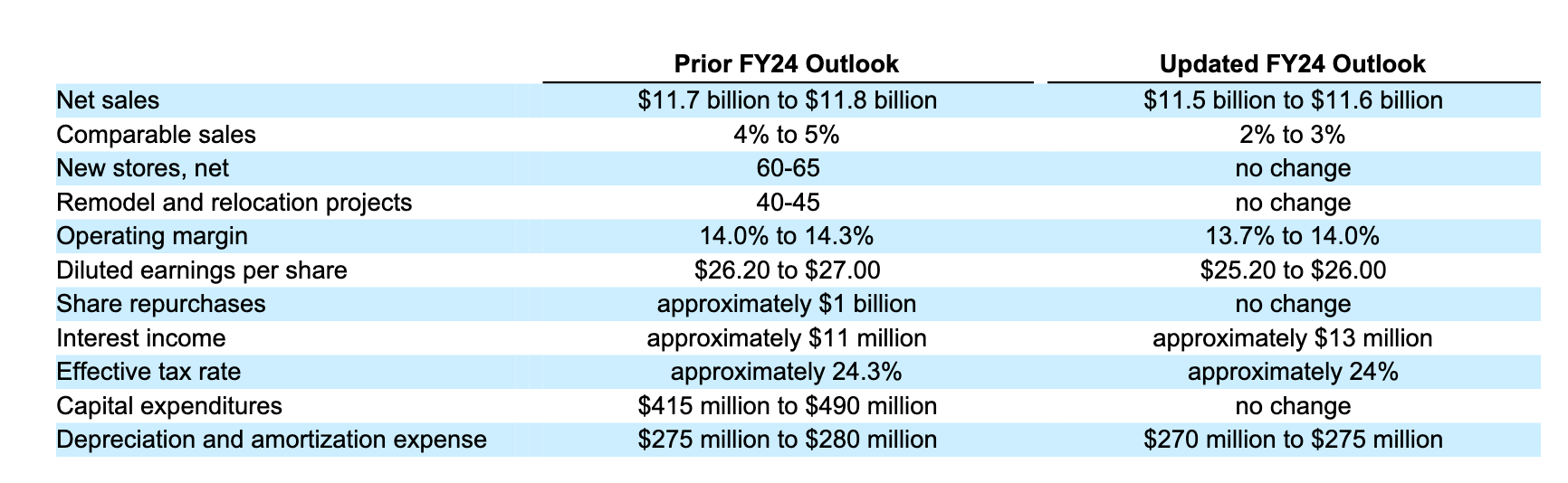

In the update, Ulta Beauty lowered its guidance:

So the company lowered its guidance, but is up +8% today?!

Sounds strange. Doesn’t it?

In the announcement of adding to our position of Ulta Beauty, I wrote the following:

Ulta Beauty will publish its results next Thursday (May 30).

Will Ulta’s result be good or bad? I have no clue at all.

But I know two things:

On Friday, the stock price will be volatile (the stock will probably go up or down significantly)

The current valuation level looks attractive providing us with a margin of safety in the long term

We are long-term investors. Quarterly results are just noise.

What matters is how the company can grow its intrinsic value per share in the long term (> 5 years).

I feel comfortable adding to our position in Ulta Beauty at today’s valuation level.

The reason that Ulta Beauty is going up today can be explained by the fact that the expectations of other investors were VERY low.

In other words: the current valuation level provides us with a margin of safety.

Key takeaways earnings call

Here are some of the key takeaways from Ulta’s earnings call:

Taking market share:

“We are confident in our model and our ability to gain share and drive significant sustainable value over the long term.”

Strong loyalty program

“We've created a world-class loyalty program that engages with more than 43 million active members and provides us with valuable customer and transaction data.”

“We ended the quarter with 43.6 million Ulta Beauty Rewards members, 6% higher than last year, primarily driven by member retention.”

“The fact that we gained 6% in total members, our retention is healthy. We're moving more members up into platinum and diamond. And retention of those guests is very high. And our brand love reached an all-time high.”

Partnership with Doordash

“We recently expanded our partnership with DoorDash with our launch on DoorDash marketplace, which extends our unique assortment to the more than 70 million active users of the DoorDash app.”

E-commerce sales

“In the first quarter, our app accounted for 57% of our e-commerce sales, up more than 450 basis points compared to last year. Our loyalty program is a powerful strategic asset, and we will lean into this platform to drive greater engagement and support top-line growth.”

Long-term growth plans will be shared at the Analyst Day in October

Update investment case

Now let’s update our investment case.