🤝 What I learned from the Berkshire Meeting

Hi friend 👋

The Berkshire Hathaway weekend was amazing.

It was once again an amazing experience.

The track record of Warren Buffett is truly remarkable.

You could take away 99% of the return of Berkshire Hathaway…

And you would still have outperformed the S&P 500.

$10.000 invested in 1962:

S&P 500: $6 million

Berkshire Hathaway: $3.8 billion

That’s the magic of compounding put to work.

We as humans are not wired to truly understand the power of exponential growth.

If you do, it will pay you tremendously.

During the Berkshire AGM, I learned a lot of new things which I’d like to share with you.

The intense schedule looked as follows:

Let’s dive into the three main lessons I took away.

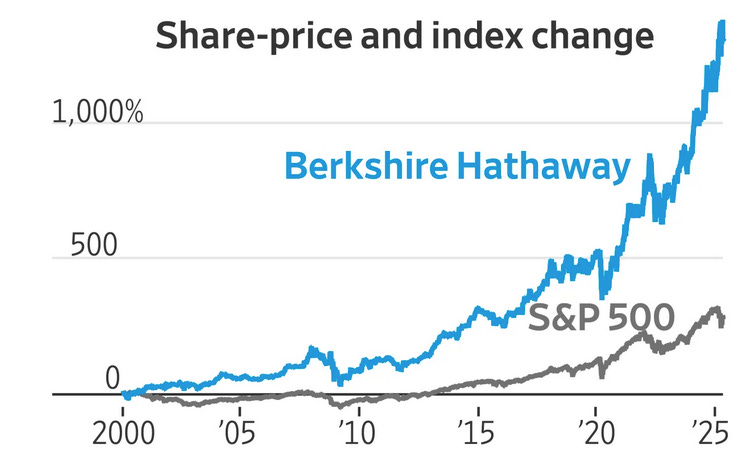

1. Berkshire Hathaway will outperform

Many people have asked whether Berkshire Hathaway will be able to outperform the market in the years ahead.

The short answer?

Yes they will.

While the outperformance will be lower than the decades before due to the law of large numbers…

It’s very logical that Berkshire will continue to outperform.

The secret of sauce of Berkshire Hathaway is its float.

What is float?

Float is the money an insurance company holds between collecting your insurance premium and paying out a claim. Customers pay upfront but claims come later. This means the insurer gets to sit on a big pile of cash in the meantime.

Smart insurers (like Berkshire Hathaway) invest that cash to earn returns. Often, they make more money from investing the float than from the insurance itself.

Berkshire Hathaway uses its float to invest in bonds and stocks.

You are not exactly sure what ‘float’ means?

Let me give you an example.

Just imagine you sign an insurance policy for your car today for $1.500 per year.

Under normal circumstances, you will not have a car accident today.

The average driver has a car accident once every 17-18 years.

The average damage per car accident equals $8,000-$10,000.

This means Berkshire Hathaway will receive $1.500 per year from you, but on average they will only pay out $8,000-$10,000 once every 17-18 years.

Until the car accident takes place, Berkshire Hathaway can invest these premiums in stocks and bonds.

That’s the float and it’s exactly what makes Berkshire so powerful.

Here’s the evolution of Berkshire’s float:

Just think about it for a second…

If you do well as an insurance company and you are profitable…

You receive the float for free.

It’s free money that is not yours you can use to invest.

This accelerates the investment profits from companies like Berkshire.

It also means the following:

If Berkshire Hathaway would use it’s operating profit and float to just copy the S&P 500, by definition it will outperform the index because it’s using ‘free money’ to invest in the index.

That’s exactly why Berkshire will keep outperforming in the years ahead.

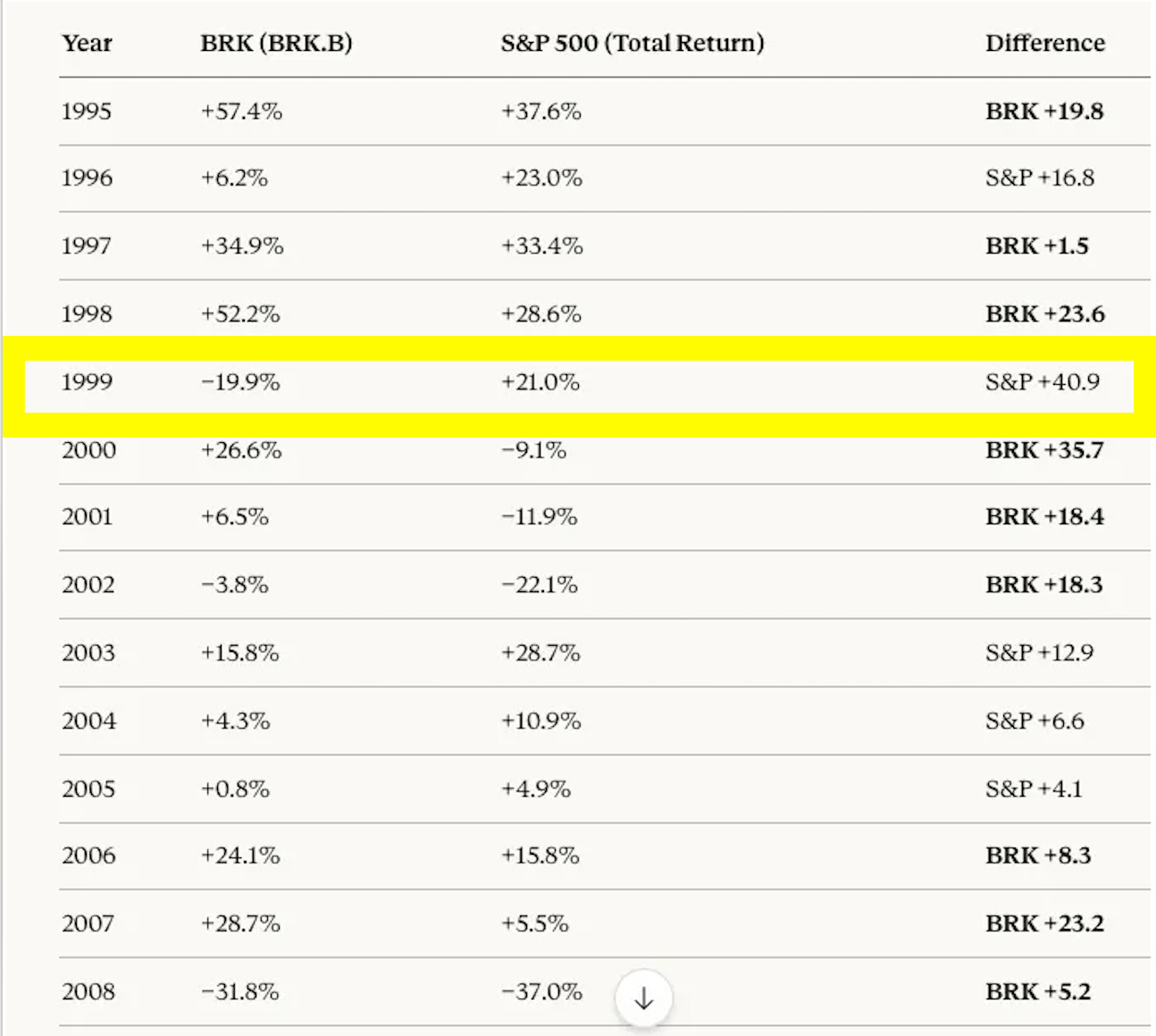

2. This is ridiculous

Berkshire Hathaway has underperformed the index by 40% since it was announced that Greg Abel would become its CEO.

This has nothing to do with Greg Abel.

It has everything to do with Mr. Market who is a Manic-Depressive.

The last time Berkshire underperformed this much? 1999.

In the years thereafter, Berkshire massively outperformed the market.

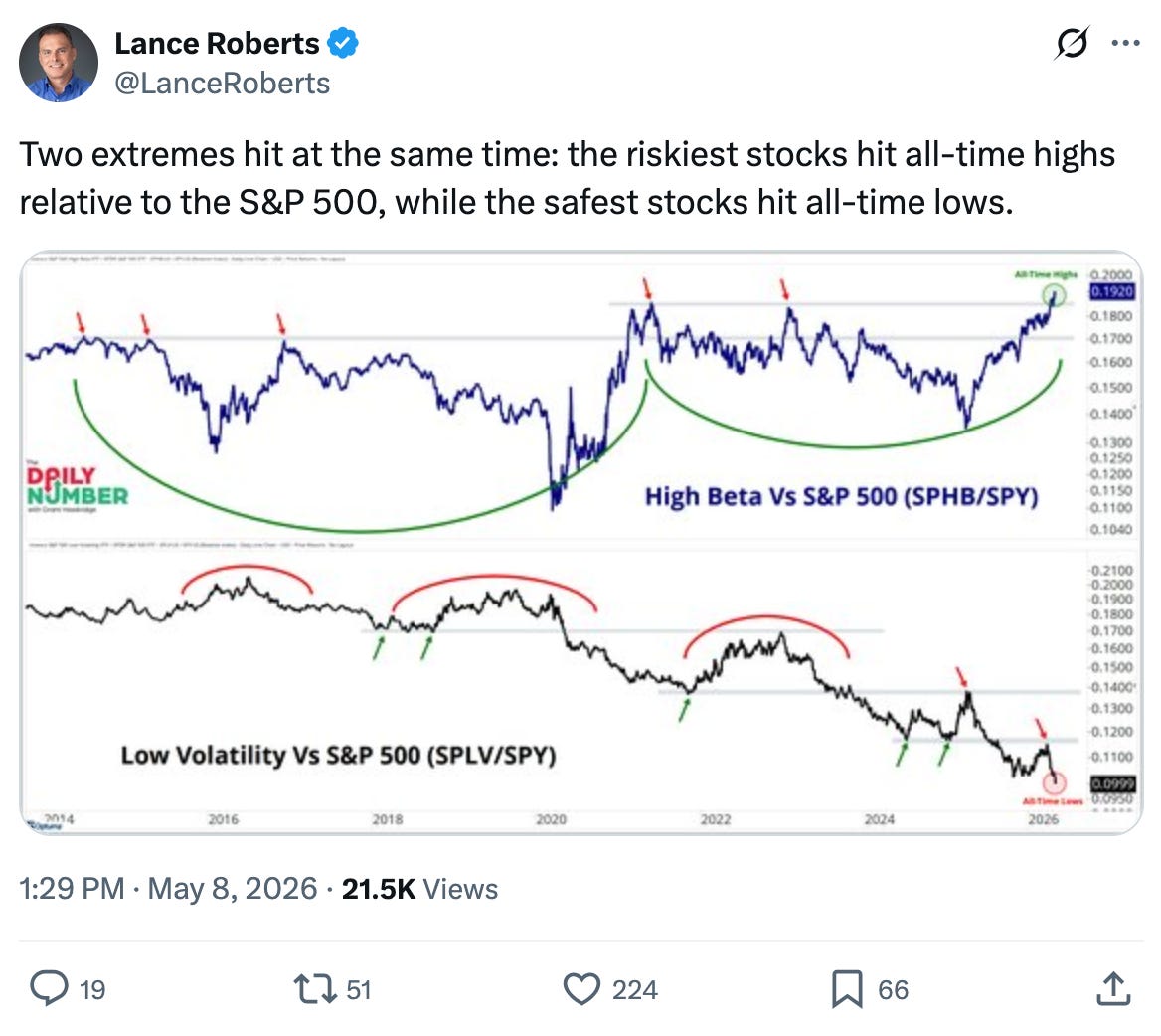

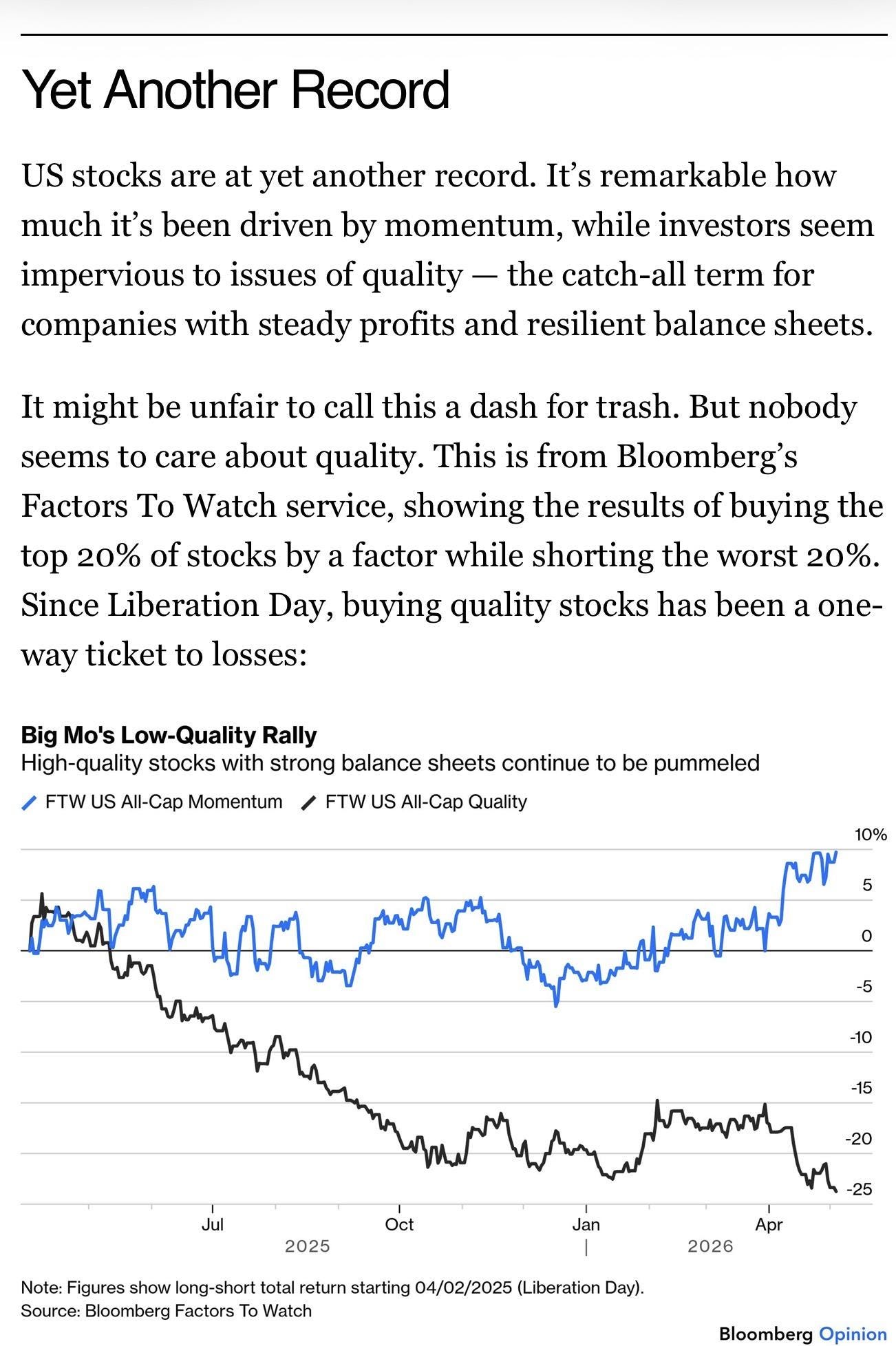

We start seeing more and more weird signals in the market.

Take this one:

Or this one:

It shows you we are in very strange times.

Let me give you one extra example to make my point.

Here’s what things look like for Our Portfolio.

Our Portfolio in 2025

Intrinsic value: +8.6%

Stock price: -6.6%

As a result, Our Portfolio became 15.2% cheaper.

Our Portfolio in 2026

Intrinsic value: +8.3% (expectations)

Stock price: -17.2%

As a result, Our Portfolio became 25.5% cheaper.

Our Portfolio since the beginning of 2026

If you combine 2025 and 2026, Our Portfolio became 40.7% cheaper (!)

Over the same period, the valuation of the S&P 500 increased by 5%.

This means that since 2025, Our Portfolio’s relative valuation declined by almost 50% compared to the index.

That’s just ridiculous.

Just look what the fundamentals look like:

While the market will remain irrational in the short term, it will be a weighing machine in the long term.

I wrote an extensive summary about this.

Partners of Compounding Quality can read it here:

3. Buy Berkshire instead of the index

Passive investing is very popular.

But today, I think it’s a way safer bet to buy Berkshire Hathaway instead of the index.

There are a few reasons for this:

Berkshire is better diversified (they have no large exposure to AI such as the S&P 500)

They have a huge cash pile (one third of the portfolio = cash)

They can use their float to invest

Berkshire is one of the best capital allocators in the world

The valuation is way cheaper than the one of the S&P 500

Berkshire Hathaway is a structural winner that will keep winning if you ask me.

If you invested $10.000 in 1962, here’s what you would have:

S&P 500: $6 million

Berkshire Hathaway: $3.8 billion

This means you could takeaway 99% of the returns of Berkshire Hathaway and you would still have outperformed the market.

That’s ridiculous.

It’s exactly why I keep going back to the Berkshire AGM year after year.

It’s like a yearly pilgrimage for me.

More resources

Finally, let’s end this article with some more resources.

💼 Investment case: The Next Berkshire Hathaway

🗣️ Investment case 2: The Company I pitched in Omaha

📄 Exclusive Berkshire Weekend PDF + Extensive Market Update

You can find them here: