👑 What you need to know about free cash flow

In the end, Free Cash Flow is all what matters.

But what is Free Cash Flow and how can you calculate it?

It’s one of the most important metrics in the world of finance.

I’ll teach you everything you need to know together with concrete examples.

What is Free Cash Flow?

In child language, Free Cash Flow is all the cash that enters a company minus all the cash that leaves a company over a certain period.

It shows you how much money a company generates after deducting all costs.

You can calculate it as follows:

Operating Cash flow = Operating Income + Non-Cash Changes - Changes in Working Capital - Taxes

CAPEX = Changed in Property, Plant & Equipment (PPE) + Depreciation

The Operating Cash Flow shows the amount of cash that is generated by a company’s normal business operations.

In other words, the Operating Cash Flow measures all the cash a company generates from selling its products and or services.

Example: When a clothing company called Jeans X generates $10 in cash per sold pair of trousers and they sell 2 million trousers per year, it’s Operating Cash Flow is equal to $20 million.

The Capital Expenditures (CAPEX) show how much money a company has used to maintain or buy physical assets.

Example: When Jeans X invests $5 million in its physical assets such as their factories, its CAPEX is equal to $5 million.

Now you know the Operating Cash Flow and CAPEX of Jeans X, you can calculate the company’s Free Cash Flow:

Free Cash Flow = Cash Flow from Operations - CAPEX

Free Cash Flow Jeans X = $20 million - $5 million = $15 million

You want the Free Cash Flow of a company to grow at very attractive rates.

Here’s an example of a company we own within the portfolio.

This company managed to grow its FCF with more than 10% per year over the past 20 years:

Why is Free Cash Flow important?

Free Cash Flow is important because it shows you whether more cash enters the company than leaves the company

This is useful for investors because you only want to invest in profitable businesses

You want to invest in companies that translate most Revenue and Earnings into Free Cash Flow

"Free cash flow is the ultimate measure of a company's strength and resilience." - Warren Buffett

What can a company do with its FCF?

In general, a company has 5 capital allocation options:

Reinvesting in itself for organic growth

Pay down debt

Acquisitions and takeovers (M&A)

Paying out dividends

Buying back shares

Capital allocation is by far the most important task of management.

You want to invest in companies that manage to allocate capital very efficiently.

In general, reinvesting Free Cash Flow to achieve organic growth is the most preferred capital allocation strategy.

Obviously, the company needs to have enough growth opportunities in order to do this.

It is also important to underline that it only makes sense to invest in organic growth when these organic investments create value (ROIC > WACC).

Free Cash Flow Margin

The best way to look at the profitability of a company, is by taking a look at the Free Cash Flow Margin.

This metric shows you how much cash a company is generating per dollar in sales.

FCF margin = (Free Cash Flow / Sales)

Visa for example has a Free Cash Flow Margin of 54.6%. This means that for every $100 in sales, Visa generates $54.6 in pure cash.

This in stark contrast with Delta Air Lines, which has a FCF margin of only 1.4%.

It goes without saying that it is justified to pay a higher valuation multiple for Visa compared to Delta Air Lines.

Here are 10 companies with a phenomenal Free Cash Flow Margin (> 30%) within the investable universe of Compounding Quality:

Free cash flow is NOT the same as Net Income

Earnings are an opinion, Cash Flow is a fact.

That’s why you should always look at the Free Cash Flow of a company and not at its Earnings.

While Earnings are an accounting metric, Free Cash Flow looks at the money that actually entered and left the firm over a certain period.

In other words: the Net Income of a company contains a lot of non-cash items whereas Free Cash Flow looks at the cash that effectively entered and exited the business.

Net Income = Total Revenue - Total Expenses

Free Cash Flow = Operating Cash Flow - CAPEX

To go from Net Income to Free Cash Flow, you should make the following adaptations:

Free Cash Flow = Net Income + Depreciation / Amortization - Change in Working Capital - Capital Expenditures

In general, Free Cash Flow can be seen as a better metric compared to the Earnings of a company because this metric is more reliable and harder to manipulate.

Free Cash Flow Conversion

Quality companies convert most Earnings into Free Cash Flow.

FCF Conversion = (Free Cash Flow / Net Earnings)

When there is a huge difference between the Free Cash flow and the Earnings of a company, you should be suspicious as an investor.

It gives an indication that the earnings quality of the company is low.

A study of James O’Shaugnessey (What Works on Wall Street) found that companies which translated most earnings into FCF outperformed companies that translated the least earnings into FCF by 5.3% (!) per year.

That’s why focusing on the FCF Conversion of a company can help you a lot to make better investment decisions.

Here are 10 companies within our investable universe which convert more than 100% of their Earnings into Free Cash Flow:

Become a Partner and get access to the investable universe as of the 1st of October:

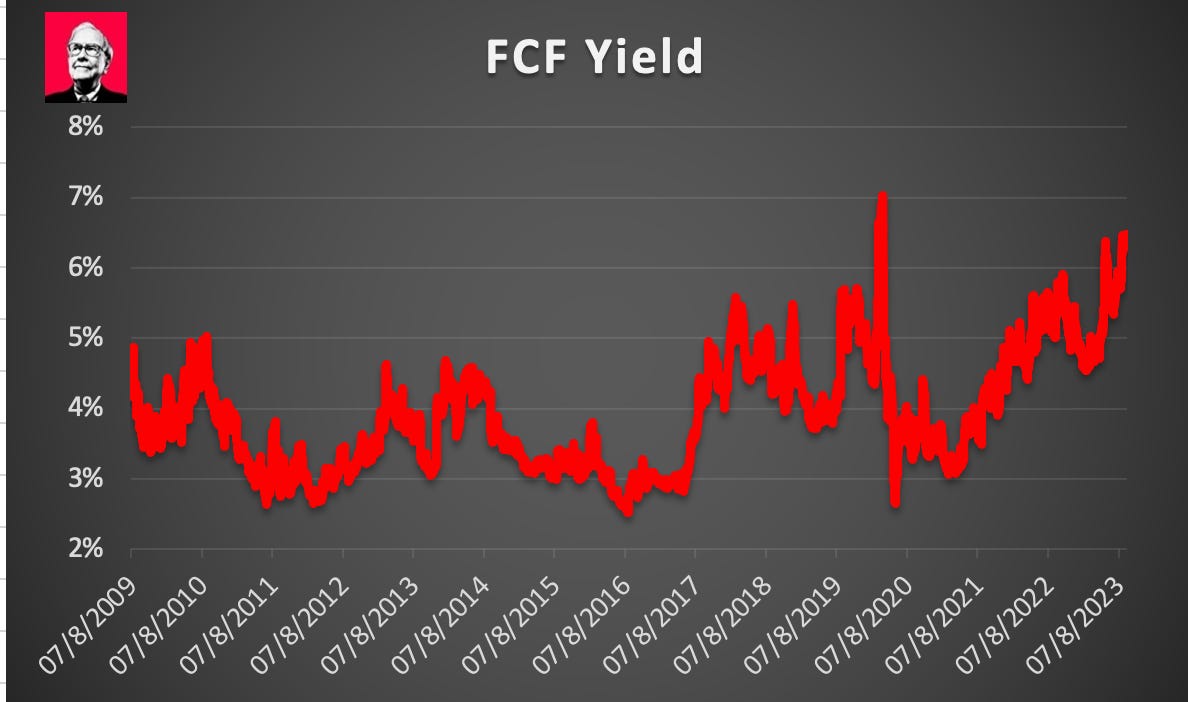

Free Cash Flow Yield

The Free Cash Flow Yield (FCF Yield) of a company is a great way to look at the valuation of a company:

Free Cash Flow Yield = (Free Cash Flow Per Share / Stock Price)

The higher this ratio, the cheaper the stock.

You can compare the FCF Yield of a company with its historical average FCF Yield to get a first grasp about how expensive the company is an historic perspective.

Here’s the evolution of the FCF Yield of the first stock we’ll buy within the Compounding Quality Portfolio:

Watch out for Stock-Based Compensation (SBCs)

A lot of technology companies are giving a lot of Stock-Based Compensation (SBC) benefits to their employees to attract and retain talent.

For investors, SBCs are a cost as it dilutes existing shareholders.

“Stock-based compensation is a cost for investors and it should be treated like that. The name says it all: 'compensation’. If compensation isn't an expense, what is it?” - Warren Buffett

As a result, you should always look at the FCF per share excluding stock-based compensation to get a more reliable and conservative view of the company.

Free Cash Flow = Operating Cash Flow - CAPEX - Stock-Based Compensation

For example, Amazon has a FCF Yield of 1.9%.

However, when you would treat Stock-Based compensation as an expense (you should), the FCF Yield would decrease to 0.3%!

This is a huge difference and underlines why you should exclude Stock-Based Compensation.

Expected return

Last but not least, you can use the following rule of thumb to calculate your expected return as an investor:

Expected Return Per Year = FCF per share growth + Shareholder Yield +/- Multiple Expansion (Multiple Contraction)

Shareholder Yield = Dividend yield + Buyback yield

Let’s use Visa as an example.

We estimate that Visa will be able to grow its Free Cash Flow per share with 13% per year over the next 5 years

The Dividend Yield is equal to 0.7% and we estimate that the outstanding shares of Visa will remain constant in the near future

Furthermore, we think the current FCF Yield of Visa (3.6%) is fair, as a result no multiple expansion nor contraction will take place

Under these assumptions the expected yearly return for Visa is equal to:

Expected Return Per Year Visa = 13% + 0.7% + 0% = 13.7%

Would you be happy with an annual return of 13.7% per year? If so, Visa might be an interesting investment.

If you aren’t happy with this expected return, you should seek for other investment opportunities.

Overview

Here you can find a great overview about Free Cash Flow:

Start of the Community

As already stated, every Premium Subscriber is a Partner of Compounding Quality.

The portfolio and all other services will gradually roll out starting from the 1st of October.

But why not start today already?

We created a Compounding Quality Community where we can chat with each other about investments and the stock market.

You can join via this link: