Why Some Businesses Never Lose

Monopolies & Oligopolies

Do you like Compounding Quality?

See the power of Compounding Quality for yourself—no risk, just results. Try it now.

Some companies are almost untouchable.

Why? They have a strong competitive advantage or moat.

For years, investors have hunted for these companies. The ones with strong brands, powerful patents, and network effects.

Think about companies like Coca-Cola, Google, and Visa. They dominate. They keep growing.

Let’s teach you everything you need to know today.

Quality Investing

Quality Investing is all about investing in the best companies in the world.

You want to buy wonderful companies at a fair price instead of fair companies at a wonderful price.

Quality stocks possess over 6 characteristics:

A strong competitive advantage

Great management

Low capital intensity

Great capital allocation

High Profitability

Attractive growth

And guess what?

Quality investing works!

Since 1994, Quality Stocks outperformed by 4.2% per year.

But why does it work?

It all comes down to the Return On Invested Capital (ROIC).

Great businesses don’t just make money—they make a lot of money on every dollar they invest.

Wall Street misses this. Analysts focus on short-term noise. They don’t see how these companies quietly compound wealth, year after year.

That’s why quality stocks keep winning.

And why the best investors stick with them.

But Pieter… Doesn’t reversion to the mean take place?

High returns attract competitors.

Reversion to the mean states that new competitors will enter the market and returns will go down as a result.

Well…

When a company is really strong, it stays strong. It doesn't go back to average.

The bigger the moat, the longer the above-average returns last.

That’s why a competitive advantage is truly essential.

"A truly great business must have an enduring 'moat' that protects excellent returns on invested capital.“ - Warren Buffett

What is a moat?

A moat or durable competitive advantage is a condition that puts a company in a superior business position. This will allow the business to maintain and increase its profit margin and market share.

“It’s incredibly arrogant for a company to believe that it can deliver the same sort of product than its rivals do and actually do better for very long.” - Warren BuffettWarren Buffett once stated that the company itself can be seen as the equivalent of a castle and the value of the castle will be determined by the strength of the moat.

In other words: the moat protects those inside the castle and prevents outsiders from entering the fortress.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.” - Warren BuffettHow do you know the company has a moat?

A moat is a structural business characteristic that allows a firm to generate excess economic returns for a long period of time.

There are two critical factors to determine whether a company has a moat:

ROIC > WACC

The ROIC has maintained high and constant for a reasonable period of time in the past.

Looking at the evolution of the Gross Margin and ROIC over the past decade can already give you a great indication.

When both metrics are robust and (very) high, this is already a great sign that the company has a moat.

Companies with a moat often have a lot of pricing power too.

Charlie Munger stated once that a few times in your lifetime, you’ll find a company which could raise its return enormously by just raising their prices, and yet they haven’t done it. This gives them a lot of untapped pricing power. These companies are the ultimate no-brainer.

Coca-Cola, S&P Global and See’s Candies are great examples of companies with pricing power.

“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business.” - Warren BuffettA moat in today’s world

Our world is changing more rapidly.

Many investors ask themselves whether they need to adapt to this new situation.

Technological progress is going faster and faster.

While it took Netflix 41 months to reach 1 million users, ChatGPT achieved this in just 1 month. DeepSeek even did it in a few days.

Disruption is the worst enemy for companies with a competitive advantage.

Some disruptions don’t just hurt a company. They reshape entire industries.

Just look at what happened with Nokia for example.

That’s why it’s important a company keeps innovating and reinventing itself.

A great example is Amazon. They evolved from a loss-making online bookstore to the largest e-commerce company in the world.

Monopolies & Oligopolies

Loyal readers know that I love to invest in Monopolies & Oligopolies:

Monopoly: Only one company dominates the entire market

Oligopoly: A few companies dominate the entire market

Warren Buffett likes them too:

Currently, Our Portfolio is invested for 20% in Monopolies & Oligopolies.

The interesting thing?

There is an ETF that allows you to invest in this attractive theme.

Tema Monopolies and Oligopolies ETF (TOLL)

Recently, I recorded a free webinar together with Tema about Monopolies and Oligopolies:

They have built their ETF on three key pillars:

1. Durability

The longer a company’s moat lasts, the longer it can generate returns above its cost of capital.

Instead of focusing on just the moat, you should also focus on the durability of the moat.

How long can the company keep compounding at above-average rates?

2. Tangibility

Focus on tangible moats instead of intangible moats.

Tangible assets: can be touched

Example: buildings, machines and infrastructure

Intangible assets: can’t be touched

Example: a strong brand name and patents

The key reasoning for this?

In a world that is changing rapidly, intangible moats can change rapidly too.

Great examples of companies with a tangible moat are Sherwin-Williams and Canadian Pacific.

3. Dominance

You want to invest in companies that deliver a lot of value to clients.

The client always comes first.

It’s the key idea on which companies like Costco and Amazon became so successful.

This approach also helps filter out competitive industries.

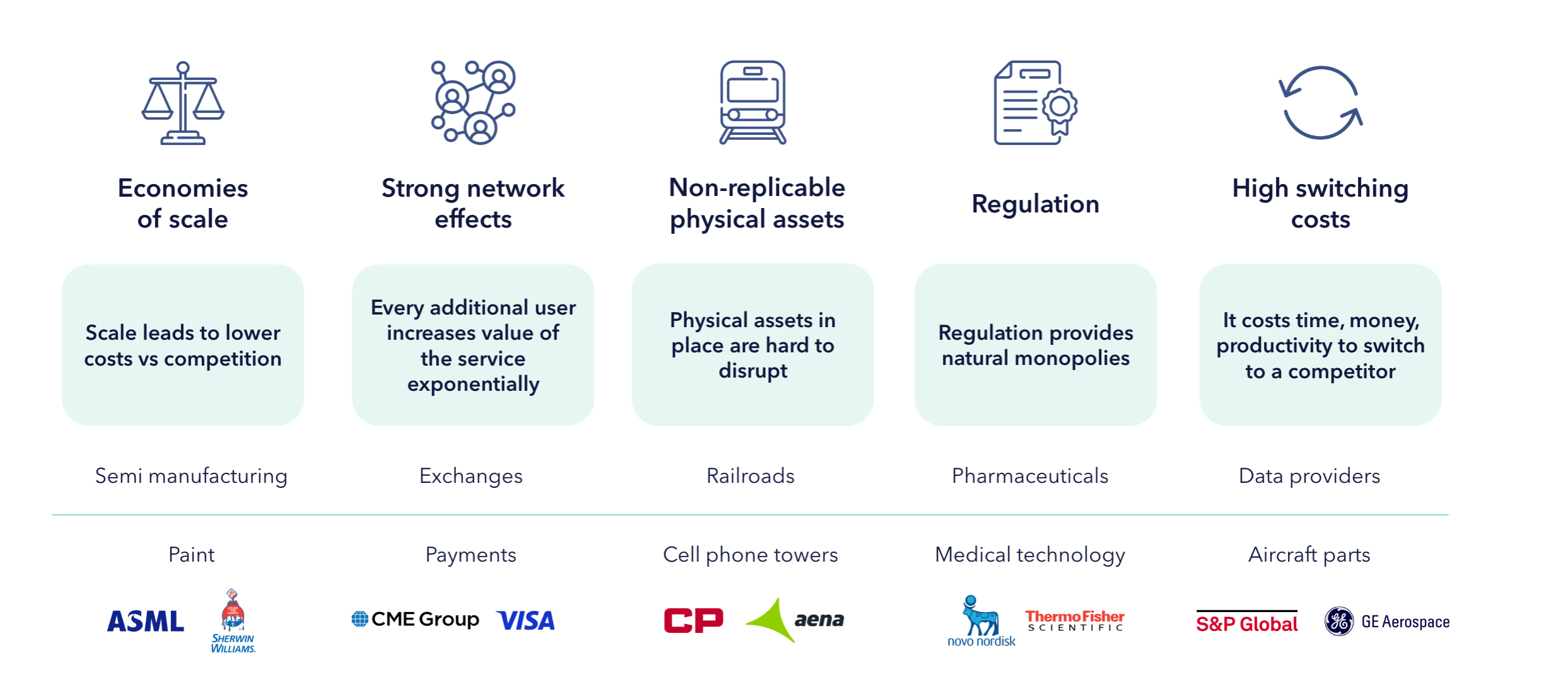

Examples

Here are some examples in the TOLL ETF that match these criteria:

Intercontinental Exchange ($ICE) | Network Effects

Intercontinental Exchange operates stock exchanges. A good trading platform helps users. More people trading means more money flowing. This makes the system stronger. ICE is also the first to offer full mortgage data and software. This brings the power of networks to a new market.

Visa ($V) | Network Effects

Visa is a payment provider. They take a small fee from every transaction. This helps keep the system stable. It is accepted in 140 out of 150 countries. People trust Visa, so it is used everywhere. Along with Mastercard, it controls 84% of the payments market.

Moody’s ($MCO) | Switching Costs

Moody’s is one of two major credit rating companies. It also leads in financial data and analytics. It owns the world’s largest database of company credit decisions. Many financial transactions depend on this data, making it hard and expensive to replace.

Sherwin-Williams ($SHW) | Economies of Scale

Sherwin-Williams is the biggest paint company in North America. Large companies like this save money by producing more at lower costs. They reinvest these savings to improve their business, even during tough times.

Canadian Pacific ($CP) | Unique Assets

After merging with Kansas City Southern, CP became the first railroad to connect all of North America. This makes it a one-of-a-kind industrial asset.

FICO ($FICO) | Switching Costs

FICO is known for credit scores. It also has a fast-growing credit software business. In the U.S., FICO is mentioned in almost every credit document. This makes it difficult to replace.

ASML ($ASML) | Economies of Scale

Making computer chips is all about producing tiny transistors at scale. ASML is the only company that can build EUV machines. These machines make the smallest semiconductors possible.

GE Aerospace ($GE) | Switching Costs

Most commercial planes use GE engines. GE and its partner Safran control 60% of the market for small jet engines. Once installed, jet engines last 30–50 years, bringing long-term profits.

Conclusion

That’s it for today.

Here’s what you should remember:

Quality investing has a strong track record of success

Warren Buffett emphasized investing in "moat" businesses

In a fast-changing world, durable and dominant moats matter most

The Tema Monopolies and Oligopolies ETF (TOLL) focuses on these strong moats

Do you want to learn more?

Everything in life compounds

Pieter (Compounding Quality)

Book

Order your copy of The Art of Quality Investing here

Compounding Dividends

Do you like dividends? Test out Compounding Dividends here

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Finchat: Financial data