🏆 20 undervalued small cap quality stocks

A few weeks ago we asked you on Twitter about the highest small cap quality stocks you know of. We got more than 200 answers (!) with more than 100 companies mentioned.

In this article, we will give an overview of the 20 best small cap high quality stocks.

If you are reading this and are not subscribed yet, feel free to join the Compounding Quality Family via the button hereunder:

Investment criteria

To filter every response we received, we used a few Quality Criteria. Each company selected has:

A healthy balance sheet

High profitability

Excellent capital allocation

Attractive outlook (expected growth)

Strong compounder (good stock market performance)

Do your own homework

Please note that the information provided in this article is far too insufficient to buy a certain stock. Always do your own homework before buying a company.

“Choosing individual stocks without any idea of what you're looking for is like running through a dynamite factory with a burning match. You may live, but you're still an idiot.” - Joel Greenblatt

Are you ready to learn about great quality stocks? Here we go!

Company 1: SDI Group

Company profile: SDI Group designs and manufactures scientific and technology products like control systems, optics and scientific imaging.

Profit Margin: 15.2%

ROIC: 18.4%

Earnings yield: 6.9%

Expected EPS Growth next 3 years: 16.1%

CAGR since IPO: 20.8% (2008)

Company 2: MIPS

Company profile: MIPS manufactures and sells sports helmets. The Company offers a brain protection system for the helmet market.

Profit Margin: 41.9%

ROIC: 59.6%

Earnings yield: 2.6%

Expected EPS Growth next 3 years: 15.3%

CAGR since IPO: 45.1% (2017)

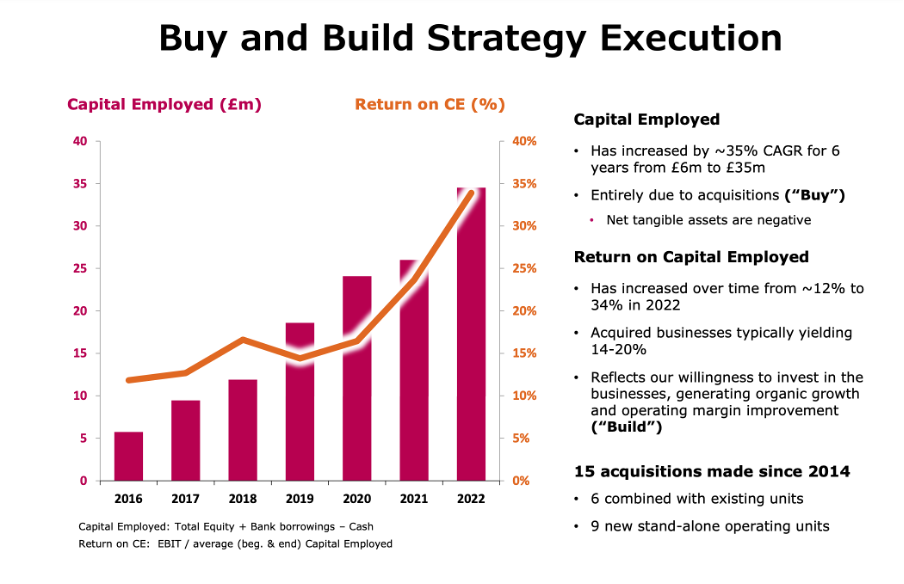

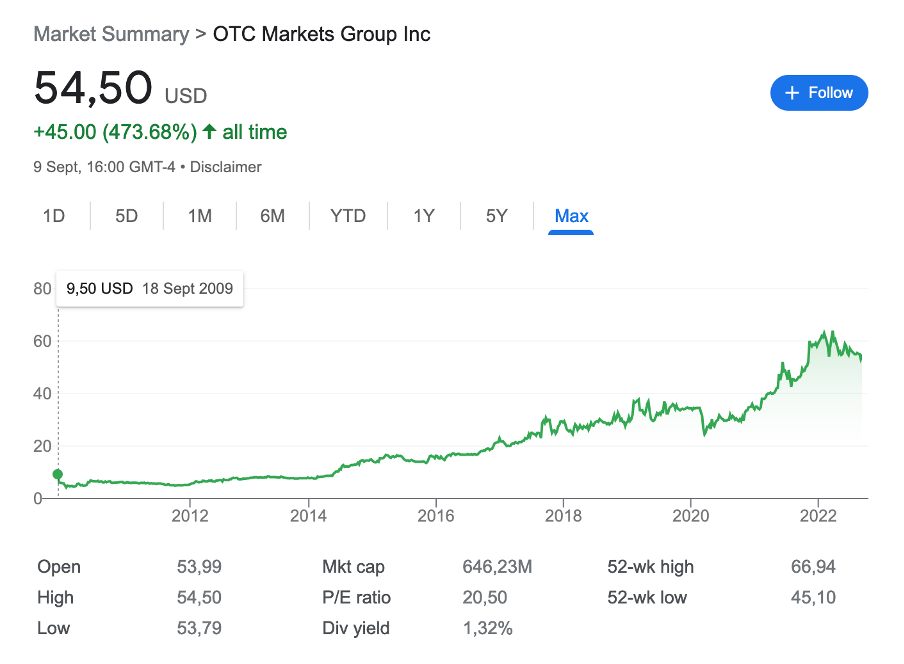

Company 3: OTC Markets

Company profile: OTC Markets regulates the trading systems and connects a diverse network of broker-dealers that provides liquidity and execution services.

Profit Margin: 29.6%

ROIC: 66.2%

Earnings yield: 5.6%

Expected EPS Growth next 3 years: 11.3%

CAGR since IPO: 27.9% (2009)

Company 4: Team17

Company profile: Team17 Group PLC develops game software. The Company publishes games for computer, console, mobile devices, and other digital platforms.

Profit Margin: 26.2%

ROIC: 12.3%

Earnings yield: 6.4%

Expected EPS Growth next 3 years: 18.3%

CAGR since IPO: 21.7% (2018)

Company 5: Kelly Partners Group

Company profile: Kelly Partners Group is a serial acquirer providing accounting and taxation services to private organizations.

Profit Margin: 8.6%

ROIC: 20.0%

Earnings yield: 4.8%

Expected EPS Growth next 3 years: 23.3%

CAGR since IPO: 42.4% (2017)

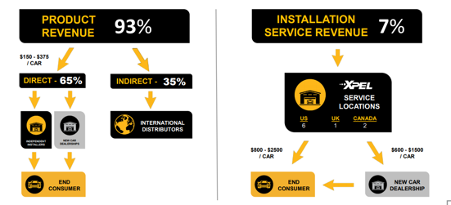

Company 6: Xpel

Company profile: Xpel develops and manufactures automotive protection products offering window and protective film for the painted surfaces of automobiles.

Profit Margin: 12.2%

ROIC: 30.8%

Earnings yield: 2.4%

Expected EPS Growth next 3 years: 31.4%

CAGR since IPO: 25.3% (2006)

Company 7: Livechat

Company profile: LiveChat is a software company that provides communication tools, offering live chat rooms and unique greetings for business.

Profit Margin: 56.0%

ROIC: 86.7%

Earnings yield: 5.1%

Expected EPS Growth next 3 years: 12.8%

CAGR since IPO: 29.2% (2014)

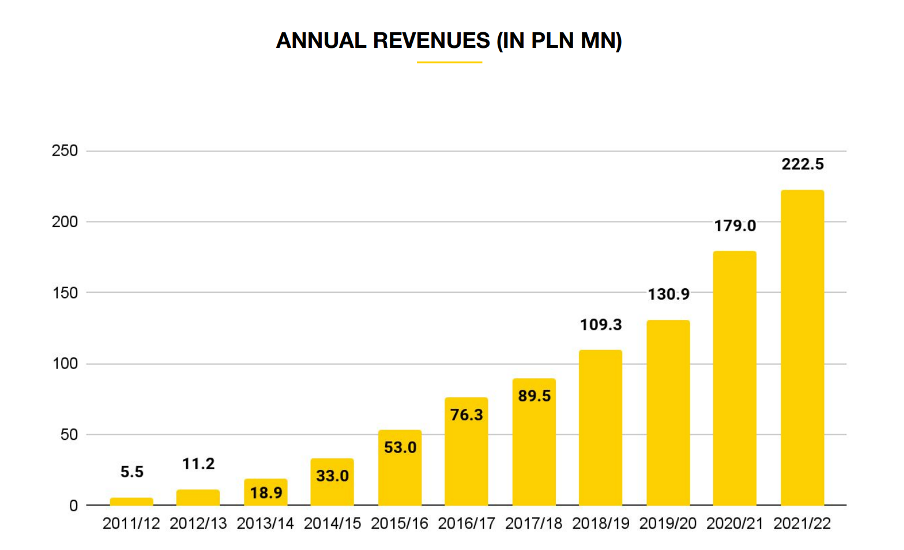

Company 8: InMode

Company profile: InMode develops medical devices, manufacturing platforms that harness novel radio-frequency based technology.

Profit Margin: 46.1%

ROIC: 48.0%

Earnings yield: 6.0%

Expected EPS Growth next 3 years: 14.6%

CAGR since IPO: 64.3% (2019)

Company 9: Games Workshop

Company profile: Games Workshop Group manufactures and retails tabletop war-game systems and associated miniatures.

Profit Margin: 31.0%

ROIC: 51.2%

Earnings yield: 4.5%

Expected EPS Growth next 3 years: 13.2%

CAGR since IPO: 20.6% (1994)

Company 10: Semler Scientific

Company profile: Semler Scientific is a medical risk-assessment company developing markets diagnostic and testing products.

Profit Margin: 32.5%

ROIC: 28.7%

Earnings yield: 3.7%

Expected EPS Growth next 3 years: 15.5%

CAGR since IPO: 23.0% (2014)

Company 11: Talenom

Company profile: Talenom operates as an accounting company offering accounting, bookkeeping, taxation, and other financial management services.

Profit Margin: 13.0%

ROIC: 11.9%

Earnings yield: 3.1%

Expected EPS Growth next 3 years: 17.3%

CAGR since IPO: 38.1% (2015)

Company 12: Qualys

Company profile: Qualys, is a cybersecurity company offering information technology security risk and compliance management solutions.

Profit Margin: 17.3%

ROIC: 23.0%

Earnings yield: 3.1%

Expected EPS Growth next 3 years: 3.1%

CAGR since IPO: 21.2% (2012)

Company 13: Admicom

Company profile: Admicom develops enterprise software. Admicom offers enterprise resource planning and management systems.

Profit Margin: 32.4%

ROIC: 30.0%

Earnings yield: 4.4%

Expected EPS Growth next 3 years: 20.7%

CAGR since IPO: 46.5% (2018)

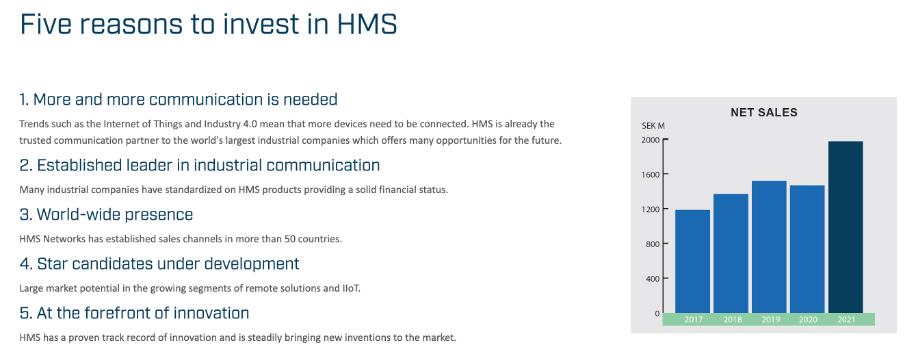

Company 14: HMS Networks

Company profile: HMS Networks AB develops, produces, and markets communication technology for industrial automation. The Company sells worldwide.

Profit Margin: 18.0%

ROIC: 24.2%

Earnings yield: 2.9%

Expected EPS Growth next 3 years: 12.8%

CAGR since IPO: 23.7% (2007)

Company 15: Cerillion

Company profile: Cerillion designs and develops customer management systems offering network asset management, billing operations, and so on.

Profit Margin: 24.7%

ROIC: 36.7%

Earnings yield: 4.4%

Expected EPS Growth next 3 years: 12.8%

CAGR since IPO: 52.4% (2016)

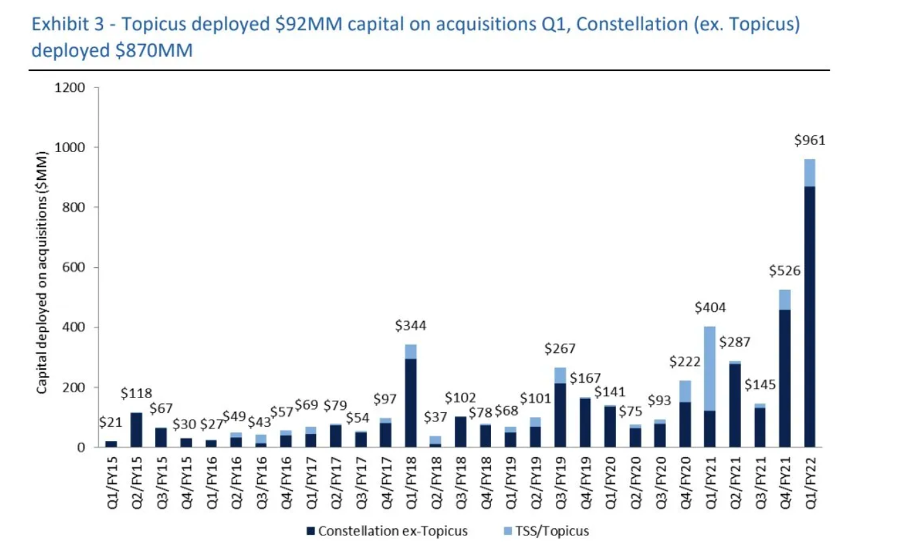

Company 16: Topicus

Company profile: Topicus is a spin-off from Constellation Software. The company is a serial acquirer with a strong focus on Europe.

Profit Margin: 2.2%

ROIC: 19.5%

Earnings yield: 4.6%

Expected EPS Growth next 3 years: 14.4%

CAGR since IPO: /

Company 17: Wingstop

Company profile: Wingstop Inc. owns and operates restaurants, specializing in cooked-to-order, hand-sauced, and tossed chicken wings.

Profit Margin: 15.1%

ROIC: 23.9%

Earnings yield: 0.4% (very expensive)

Expected EPS Growth next 3 years: 20.3%

CAGR since IPO: 37.2% (2015)

Company 18: Chemometec

Company profile: Chemometec manufactures instruments used to analyze particles like mammalian cells, sperm cells, yeast cells, and somatic cells in milk.

Profit Margin: 37.7%

ROIC: 44.1%

Earnings yield: 1.1%

Expected EPS Growth next 3 years: 33.4%

CAGR since IPO: 25.9% (2006)

Company 19: Robertet

Company profile: Robertet produces liquid flavorings, perfumes and associated natural aromatic ingredients.

Profit Margin: 11.8%

ROIC: 11.4%

Earnings yield: 3.3%

Expected EPS Growth next 3 years: 3.5%

CAGR since IPO: 15.7% (1990)

Company 20: PubMatic

Company profile: PubMatic provides integrated inventory, data, and advertising revenue optimization platform for digital publishers.

Profit Margin: 25.0%

ROIC: 18.5%

Earnings yield: 7.1%

Expected EPS Growth next 3 years: 10.4%

CAGR since IPO: /

The end

Now you learned about these 20 great companies, it is time to do your own research.

Let’s see if these companies will outperform the market over the next years!

More from us

Do you want to read more from us? Please subscribe to our Substack where we provide investors with investment insights on a weekly basis. You can also follow us on Twitter and Linkedin.

About the author

Compounding Quality is a professional investor which manages a worldwide equity fund with more than $150 million in Assets Under Management. We have read over 500 investment books and spend more than 50 hours per week researching stocks.

Thanks a lot for this post. I wanted to contribute with my thoughts on Mips, which I know well. It has indeed a lot of quality traits: supportive industry trends, strong economics, strong relationships with helmet brands, end users who value a lot the Mips brand, and a unique position as an ingredient brand (for the same reasons there is only one Gore-Tex in jackets, there is probably only going to be one Mips in helmets)...But recently I am wondering whether the cyclicality of Mips' main end market ("Sports/Cycling" - still >90% of revenue) diminishes the quality, especially after the explosion of bicycle & helmet sales during the pandemic and as we are potentially entering a recession. Since the "Safety" vertical is still ramping up, could Mips be facing a hiatus in growth because of the combination of these two factors (Covid boom fading + weaker macro)? This is why I am still watchful at c.30x P/E. Cheaper valuation or signs of resiliency in this difficult environment is what I am monitoring at the moment.

Hello,

thank you again for all your work.

Would you say that one year after those stocks are still undervalued? Or is it better to focus on your recent list "15 stocks you've never hear of"?