Hi Friend 👋

I’m Pieter and welcome to a 🔒 subscriber-only edition 🔒 of Compounding Quality.

In case you missed it:

If you haven’t yet, subscribe to get access to these posts, and every post.

A new month, a new Best Buys List.

Each month, I’ll give an overview of my favorite stocks of the month.

Let’s dive into this update and show you my favorite stocks.

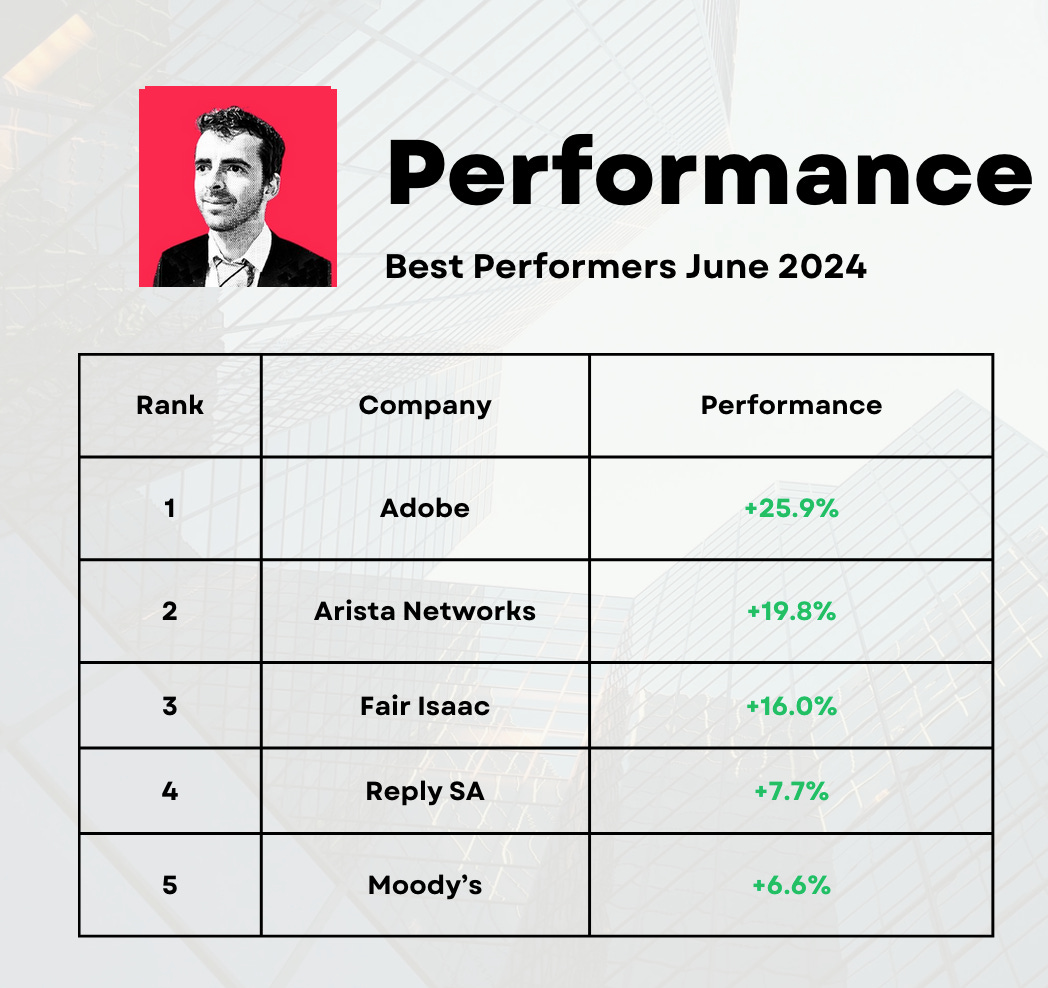

June 2024

In June, the S&P 500 increased by 3.5%.

The Fear & Greed Index indicates that we are currently in ‘Neutral’ Mode.

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

The cheaper we can buy great companies, the more we like it.

Worst performers

Best Performers

Best Buys July 2024

Now let’s dive into our favorite stocks for July 2024.

I only mention companies that can’t be found within the Portfolio today.

I love the companies within our Portfolio and I think most are still (significantly) undervalued.

5. Paycom

Paycom provides data analytical software products to manage the employment life cycle from recruitment to retirement.

Their software features talent acquisition, time and labor management, payroll, talent management, and HR management. Paycom was founded in 1998 by Chad Richison. Today, Chad is still the CEO and owns 11.6% of the business. In total, insiders own 12.6% of Paycom.

The company is down 55% over the past year and declined more than 70% from its all-time high.

The main reason for this decline?

Paycom's Beti, which lets employees handle their own payroll and minimizes errors, is a double-edged sword for the company.

Although it provides great value to customers, it has also decreased demand for some of Paycom's other services.

Here’s what is interesting about Paycom:

The founder is still the CEO. Chad Richison has built a strong track record over the years

Paycom is a very healthy business

Balance sheet: Net Cash Position

Profitability: Gross Margin: 86.6% - Net Income: 26.9%

Capital allocation: ROCE: 28.3%

Paycom trades at its cheapest valuation level ever. The Forward PE is equal to 17.7x (5-year historical average: 49.9x)

Source: Finchat

What I don’t like about the company? The high level of stock-based compensation.

Stock-based compensation as a % of Net Income is equal to 29.1% (!).

Many SaaS companies pay out a lot of SBC, but as you know this is a cost for shareholders. When you exclude SBCs, Paycom’s forward PE would increase from 17.7x to 24.4x.

I am not considering investing in Paycom today due to the high level of Stock-Based Compensation and the high risk associated with the company.

The current stock price might offer opportunities for investors with a higher risk appetite.

4. Nike

Just Do It. Right?

Everyone knows Nike and its famous products.

It’s a great business for sure:

Healthy balance sheet

More than 50% of all revenue is translated into pure cash

Great capital allocation skills

They will benefit from the rising middle class in Asia

Nike returned 20.8% per year to shareholders since 2008

In June, Nike lost 20% in value after management stated that it expects sales to decline next year. It was the worst stock market decline for Nike ever.

But does this decline offer opportunities for long-term investors?

Nike currently trades at a forward PE of 23.6x. This in line with its historical average.

Our Earnings Growth Model gives an expected yearly return of 13.9% and our Reverse DCF states that Nike should grow its Free Cash Flow by 11.8% in order to return 10% per year to shareholders.

Even after the 20% decline, Nike doesn’t look (extremely) cheap. I would start to get seriously interested at a stock price of $65 (current stock price: $75).

Now let’s dive into the top 3.

Spoiler alert: Our Next Buy might be in there.