Hi Partner 👋

Welcome to this week’s 🔒 paid edition 🔒 of Compounding Quality. Each week we talk about the financial markets and give an update on our Portfolio.

In case you missed it:

Subscribe to get access to these posts, and every post.

Another month, another Best Buy list.

Every month I give an overview of the most interesting Quality Stocks.

Let’s dive into this update and talk about November’s best picks.

September 2024

In October the S&P 500 decreased by 1.8%

The Fear & Greed Index indicates that we are currently in ‘Neutral’ Mode.

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

Worst performers

The cheaper we can buy great companies, the more we like it.

A lot of Partners have asked questions about ASML. Let’s write a Not So Deep Dive about them shortly.

Best Performers

It’s great to see that two companies in Our Portfolio are on the Best Performers List:

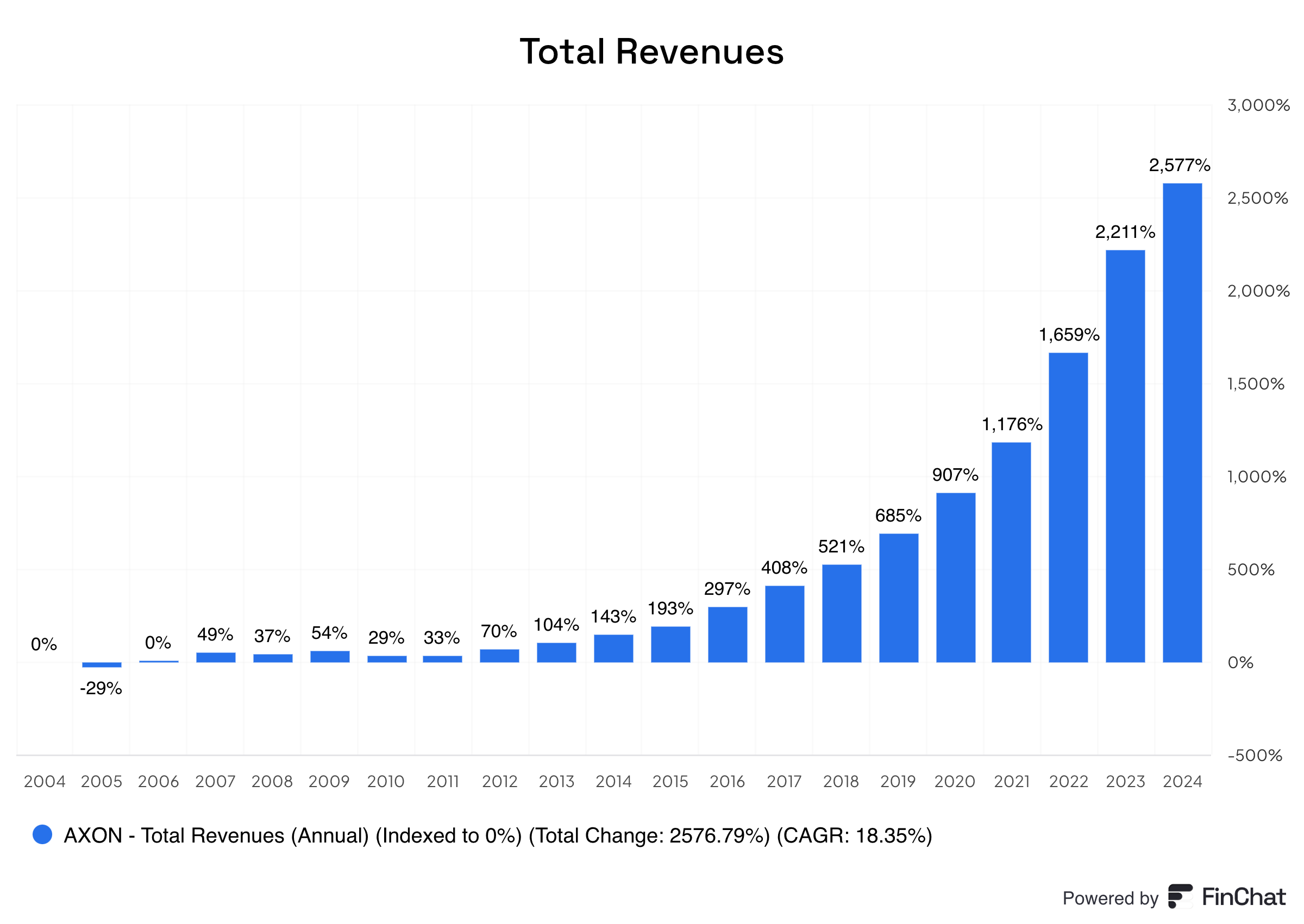

Company Spotlight: Axon

The Company Spotlight this month? Axon.

Axon makes tools to help the police and public safety workers.

They create devices like body cameras and tasers. These tools help keep people safe. Axon also makes software to store videos and data.

The police can use this software to review what happened. Axon’s tools help police get better info quickly to make correct decisions.

Four reasons why it’s an interesting company:

Network effects: As more police use Axon’s software, it gets more valuable

Patrick Smith is the Founder and CEO. He still owns 3.9% of the company

Axon returned 32.9% (!) per year to shareholders since 2001

Revenue growth is 18.4% per year for the past 20 years

We would love to buy Axon at the right price.

Unfortunately, the company is rather expensive right now:

Forward PE: 82.0x (10-year average: 87.7x)

Earnings Growth Model: expected yearly return of 10% per year

Reverse DCF: Axon should grow its FCF by > 20% per year to return 10% per year to shareholders.

Expected long-term growth per year: 19.5%

Once the valuation normalizes, it’s definitely a company we’ll look into.

Best Buys October 2024

Let’s jump into our Best Buys for November 2024.

We won’t cover the companies in our Portfolio.

Why? Because we love them all! You can read the latest Portfolio Update here.

Now, here are our five best buys for the month.

5. Adobe

How does Adobe make money?

Adobe is a high-quality company with a simple mission: to create innovative products that transform the world.

The company makes money by selling software tools for creativity and productivity, like Photoshop and Acrobat, mostly through subscriptions.

94% (!) of Adobe’s revenues are generated via subscriptions.

Adobe is active in 3 segments:

Creative Cloud (75.7% of sales): Creative Cloud offers over 20 apps for design, photography, …

Document Cloud (23.7% of sales): Document Cloud provides tools to create and sign documents.

Experience Cloud (0.6% of sales): Offering marketing and customer experience tools.

Why is Adobe a quality business?

Adobe’s products are the industry standard

The company should be able to benefit from AI in the years to come

Long-term estimated EPS-Growth: 17.3%

Valuation

Forward PE: 27.5x (5-year average: 31.8x)

Earnings Growth Model: expected return of 13.9% per year

Reverse DCF: Adobe needs to grow its FCF by 13.5% per year to return 10% per year to shareholders

Why is Adobe in our Top 5 right now?

Adobe dropped by another 4.6% in the past month. The company now trades 24.4% below its 52-week high.

4. Judges Scientific

How does Judges Scientific make money?

Judges Scientific is the second serial acquirer on our list.

JDG acquires companies that make special science equipment. These tools are used in labs for research and testing.

The beautiful thing about this? The market for scientific instruments is still very fragmented. This provides JDG with plenty of acquisition targets.

I had the privilege to meet David Circurel, the founder and CEO, on my way back from Omaha after the Berkshire AGM. We ended up chatting for two hours about Judges Scientific.

The key takeaway? He said JDG still has plenty of growth potential. According to him, the company could still 20x in the next 20 years.

Why is Judges Scientific a quality business?

JDG is the Constellation Software for science equipment

CEO David Cicurel owns 9.3% of the total shares outstanding

CAGR since IPO in 2005: 27.5%

Valuation

Forward PE: 25.7x (5-year average: 19.9x)

Earnings Growth Model: expected return of 6.7% per year

Reverse DCF: Judges Scientific needs to grow its FCF by 14.0% per year to return 10% per year to shareholders

Why is Judges Scientific in our Top 5 right now?

Judges Scientific is an amazing business. The stock is down 23.8% from its ATH and might offer opportunities.

Now let’s dive into the top 3.

Spoiler alert: our Next Buy is in here.