🎙️ How Drew Cohen Picks Winners

A conversation with Speedwell Research

Hi Partner 👋

Welcome to this week’s free edition of Compounding Quality. Each week we talk about the financial markets and give an update on our Portfolio.

In case you missed it:

Subscribe to get access to these posts, and every post.

Do you know Drew Cohen?

His investment philosophy is very similar to ours.

Let’s dive into how he finds great quality stocks.

This article was brought to you by Interactive Brokers.

Interactive Brokers is the broker I use for all my transactions. Find out more here.

Compounding Quality: Can you tell a bit more about yourself? Who is Drew? And how did Speedwell Research come to life?

Drew Cohen: I’ve been fascinated by investing since I was a kid. I bought my first stock at 14.

The next few years? A masterclass in what not to do. I traded short-term, chased macro trends, and skipped real research. Thought I was smart. I wasn’t.

Then, like so many, I discovered Warren Buffett and Charlie Munger. I started reading everything they ever wrote. That changed everything.

After studying Accounting and Business Administration at USC, I joined Goldman Sachs in New York. I worked in Investment Research, analyzing financial companies. It was a great experience. But also a lesson in how big firms operate.

Next stop: San Francisco. Capital Group. Managing $2 trillion+ in assets, they’re one of the biggest mutual fund managers in the world. I focused on internet companies, late-stage private deals, and got a front-row seat to how real investing works.

But something was missing. I wanted full control over my investment process. No politics. No distractions. Just real research.

That’s why I started Speedwell Research. To write the kind of analysis I wished I had at Goldman or Capital Group. No fluff. No bias. Just straight-up, deep-dive research.

Compounding Quality: Every investor is unique. How would you describe yourself?

Drew Cohen: Value investing used to mean deep company research. You only bought when the stock traded below its intrinsic value.

Buffett always called himself a value investor, even after Munger and Fisher influenced him. Today, that style is often labeled as quality or growth investing.

Meanwhile, ‘value investing’ now mostly means buying cheap stocks. Low book value, low earnings multiple. Business quality? Irrelevant.

That’s not how I invest.

I want to know every assumption behind an investment. Then, I check if the returns make sense.

To do this, I use a Reverse DCF. It shows me the implied returns under different scenarios. I prefer setups where the downside is minimal. If conservative assumptions suggest market-like returns, I’m interested.

Sounds quantitative? It isn’t. The bulk of my process is qualitative.

I start by reading every earnings transcript. I want to understand how the company has evolved over time.

Deep research builds confidence. If you know your investment inside out, price swings won’t shake you.

I focus on predictability. No turnarounds. No companies that still need to figure out their business models. No stocks that require aggressive future growth just to make sense.

Compounding Quality: How would you define your investment process?

Drew Cohen: My investment approach is simple. I look for companies with

A competitive advantage

Excellent management

High predictability

Positive upside

Satisfactory returns under conservative assumptions

I look at businesses the way Warren Buffett does, but everything depends on the assumptions you make—and how you define ‘great.’

For me, the key question is: how hard is it to compete with this company?

I like businesses with interlocking moats. One advantage isn’t enough. The best companies stack multiple strengths on top of each other.

Take RH as an example. Want to build massive Design Galleries like RH? You’ll need a huge furniture collection. But to get that collection, top designers need to trust your brand. And to pull people into those Galleries, you might need restaurants.

RH solves this by having its own designers—no reliance on outsiders. It also gets prime real estate because landlords know RH stores attract crowds.

To copy RH, you don’t just need good furniture. You need expertise in real estate, branding, design, hospitality, and interior services. Miss one? You’re not a real competitor.

That’s the power of an interlocking moat.

Compounding Quality: You dive deep into companies (80-page investment cases). How long does it take you to create such a case? And does it make you more comfortable when making investment decisions?

Drew Cohen: Generally 5-8 weeks.

Good decisions don’t feel like decisions. Big choices, like joining Goldman Sachs or working for myself, felt obvious. I didn’t have to overthink them.

I don’t force decisions when investing. With enough research, the right choice becomes obvious.

Sometimes, that means reading 60 earnings reports before pulling the trigger. But when the research stacks up, buying feels like a no-brainer. And if it doesn’t? That’s fine too. You can pass.

Mistakes will happen, but at least you won’t waste time agonizing. Staring at a wall, trying to “think” your way to the right choice, doesn’t work. If anything, it makes things worse.

Do the work. Trust the process. The answer will come.

Compounding Quality: You wrote Deep Dives on Constellation Software, Copart, Axon, Costar Group, … About which company do you feel the most comfortable today?

Drew Cohen: For me, comfort in an investment comes from confidence in the business model, not just the valuation.

My strongest conviction? Copart.

Copart helps insurance companies decide when a car is totaled. Then, they pick it up and sell it at auction. Simple concept, incredible business.

Their moat is unbeatable. Competing with them? Nearly impossible.

First, you’d need expensive land near cities. Good luck with that—junkyard permits are almost impossible to get. But even if you had the land, you wouldn’t have cars to sell.

Why? Network effects. Buyers won’t come without cars. Suppliers won’t send cars without buyers. Copart dominates both sides.

And that’s just the start. Copart has:

Massive logistics infrastructure

Deep insurance integration

Exclusive data tools to help insurers total cars

A reputation for reliability—even during disasters

To compete, you’d need land, a marketplace, insurance partnerships, logistics, data tools, and disaster readiness—all at once.

That’s not a business model you can copy. And that’s exactly what makes Copart so powerful.

Compounding Quality: What’s the best investment decision you’ve ever made?

Drew Cohen: The best investment decision I’ve ever made is Meta Platforms.

We published our Meta Research Report in January 2023.

The market was extremely pessimistic about the company. I added down to the bottom and made it my largest position.

In January 2023, we ran a Reverse DCF on Meta Platforms. The market priced in 0-3% annual growth. Reality Labs (Meta’s business unit for AR and VR) had a net negative value.

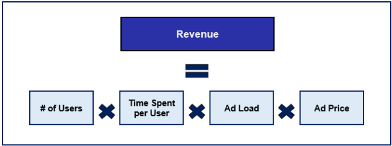

The below image shows the 4 pillars for Meta’s revenue:

When we do the exercise for Meta Platforms:

Despite the noise, the number of users were growing

Time spent per user was growing because of the introduction of short videos

Third is ad load, which is well under Meta’s control as they can always put an ad against any sort of content they host.

The only question mark was the ad price

Meta’s ad prices are set through auctions. They dropped hard after Apple’s App Tracking Transparency (ATT) and the end of the Covid e-commerce boom.

ATT was a game-changer. Meta lost access to key data, making it harder to target ads and measure results. Advertisers saw worse performance, so they spent less.

Meta’s response? Go all-in on AI. They poured $30+ billion into rebuilding their data signals—without needing as much input.

At the same time, they pushed advertisers to use a conversion API on their own servers. The goal? Cut reliance on iOS and regain lost tracking accuracy.

Meta is fighting back. And with AI in the driver’s seat, they might just win.

Compounding Quality: What’s the worst investment decision you’ve ever made?

Drew Cohen: My worst investment has to be Etsy.

My outcome with Etsy wasn’t bad, but my analysis was wrong.

Etsy has a strong competitive position. But they are good in an area (handmade products) that most people don’t care about.

This taught me something important. A company can be the best at something, but if people don’t care, it doesn’t matter. They are focusing on the wrong thing.

Handmade products can’t be stored in warehouses or be mass-produced. This makes them more expensive. These limits are built into their business model.

Etsy can’t match Amazon’s shipping speeds or Temu’s prices without changing what makes them unique.

In other words, Etsy has a competitive advantage in something that few people value.

Compounding Quality: What’s a famous investment rule you disagree with?

Drew Cohen: The idea of staying in your circle of competence is often misunderstood or wrong.

People say it means avoiding areas you don’t know and sticking to what you’re familiar with. This assumes you can’t learn new things. I disagree.

Staying in your circle of competence isn’t about avoiding new industries.

It’s about how well you can predict outcomes.

For example, I might understand Porsche AG as a company. But I can’t confidently predict if they’ll keep selling over 300,000 cars a year far into the future.

On the other hand, I’m confident Floor & Decor will remain a leader in selling Luxury Vinyl Plank (LVP) flooring.

I didn’t know what LVP was five years ago. However, I’ve known about Porsche my whole life.

Your circle of competence isn’t about what’s familiar or simple. It’s about being confident in the assumptions you make.

Compounding Quality: Which key characteristics should a good investor have?

Drew Cohen: Self-awareness. Unfortunately, it’s impossible to be aware of all our biases.

Being self-aware is not going to control your emotions. However, you’ll recognize them and separate them from logic. This is just as helpful, as it stops you from acting on emotions.

Self-awareness helps you notice when you’re falling into those biases. Too often, people think an investment is good for reasons that have nothing to do with the investment itself. They just want it to be good.

Warren Buffett is a good example. He can praise an investment, and then sell it when he thinks the thesis changed, like with Apple.

Compounding Quality: Any book recommendations to share with our audience?

Drew Cohen: It looks like you’ve already mentioned many of the best investing books, but I’ll share a few that are less talked about:

The Big Money by Frederick Kobrick has some interesting insights, particularly around the interplay between research and conviction.

The Investment Checklist by Michael Shearn is a solid and straightforward book on things to look for in an investment.

Secrets of The Temple by William Greider is a great history of the Federal Reserve and focuses a lot on the high inflationary period of the 70s.

Americana by Bhu Srinivasan is an interesting history of American Capitalism by telling the story of a single industry that defined each era.

Men and Rubber by Harvey Firestone is a great business book by an entrepreneur who was contemporary with Henry Ford and Thomas Edison.

Born of This Land by Chung Ju-yung is the story of Hyundai, which became a business conglomerate that spanned many different industries.

Compounding Quality: Thank you. A last one maybe… Can you share which company will be covered in your next deep dive?

Drew Cohen: We just finished Airbnb and are now working on Api Group. Maybe we’ll do LVMH next.

Speedwell Members get access to our whole library of reports, on-going company updates, and our future releases!

Thank you for the opportunity to share with your audience!

Whenever you’re ready

That’s it for today.

Compounding Quality is all about securing your financial future.

Whenever you’re ready, here’s how I can help you:

📈 Access to my Portfolio with 100% transparancy

📚 Access to my ETF Portfolio

🔎 Full investment cases about interesting companies

📊 Access to the Community

✍️ And much more!

Everything in life compounds

Pieter (Compounding Quality)

Book

Order your copy of The Art of Quality Investing here

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Finchat: Financial data

Pieter, many thanks for sharing this engaging and informative interview! I have never met Drew Cohen, but after reading this interview, I am already a big fan of his!

i love copart but i think the EV vehicle market will hurt them a lot , and with the self driving car ...