Kinsale Capital: Niche Mastery, Compounding Success

Investment case Kinsale Capital (Part 2)

Hi Partner 👋

I’m Pieter and welcome to a 🔒 subscriber-only edition 🔒 of Compounding Quality.

In case you missed it:

If you haven’t yet, subscribe to get access to these posts, and every post.

Kinsale Capital is a Compounding Machine for sure.

The founder Michael Kehoe is still the current CEO

Kinsale Capital is a clear market leader in a niche

Their underwriting is far superior compared to peers

Let’s dive in!

Is management capable?

Kinsale Capital is an Owner-Operator stock.

Michael Kehoe founded the company in 2009 and he is still the CEO and President.

Today, Kehoe owns 4.0% of Kinsale Capital.

In total, all executive officers and directors own 5.6% of the business.

Kinsale Capital also benefits from an experienced and cohesive management team. The average manager has over 30 years of relevant experience. What’s also positive is that Michael Kehoe and Brian Haney worked together for over 20 years (since 2002).

As you can see, many employees of Kinsale worked together for decades at other E&S insurance companies:

I believe Kinsale Capital has an excellent culture. The company wants to hire young talent and promote from within.

Employees give Kinsale Capital a good score on Glassdoor:

Does Kinsale Capital have a competitive advantage?

Kinsale Capital is a clear market leader in a niche (insuring excess and surplus lines in the United States).

Kinsale Capital has a moat based on 4 main factors:

Leveraging its technology to generate superior data, insights, and services

Exclusive focus on the E&S market (a more profitable segment within insurance)

Vigilantly controlling expenses (resulting in a lower expense ratio versus competitors)

Focus on small accounts (Kinsale is a market leader in this underserved niche)

Over the years, Kinsale Capital has built a proprietary technology platform that reflects the best practices of its management team and has learned from its extensive prior experience.

Kinsale operates on an integrated digital platform with a data warehouse that collects statistical data.

The platform provides high efficiency, accuracy, and speed across all processes.

Management believes its technology platform will provide them with an enduring competitive advantage. It allows them to respond to market opportunities quickly and will continue to scale as the business grows.

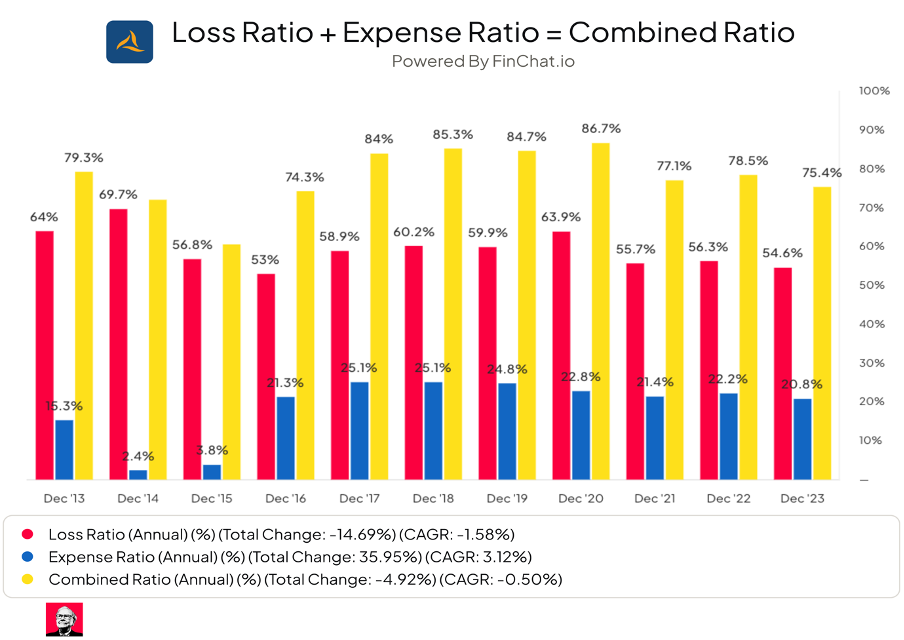

In Part 1, you learned that the most important metric for an insurance company is the Combined Ratio.

The combined ratio is calculated by taking all the expenses and losses an insurance company makes from paying out claims and dividing this number by all the premiums they receive from their insurance policies.

In other words: the combined ratio is the sum of the loss and expense ratio.

Source: Finchat

The lower this ratio, the better.

A combined ratio under 100% indicates that the insurance company is profitable and the other way around.

And guess what makes Kinsale Capital unique…?