👜 Should you buy Hermès?

Investment case Hermès

Hermès is the definition of luxury and exclusivity.

The company even has a multi-year waitlist for its handbags.

Is Hermès stock as finely crafted as its luxury goods? Let’s find out.

Hermès - General Information

👔 Company name: Hermès

✍️ ISIN: FR0000052292

🔎 Ticker: RMS

📚 Type: Owner-Operator Stock

📈 Stock Price: € 2,200

💵 Market cap: €233.4 billion

📊 Average daily volume: €130 million

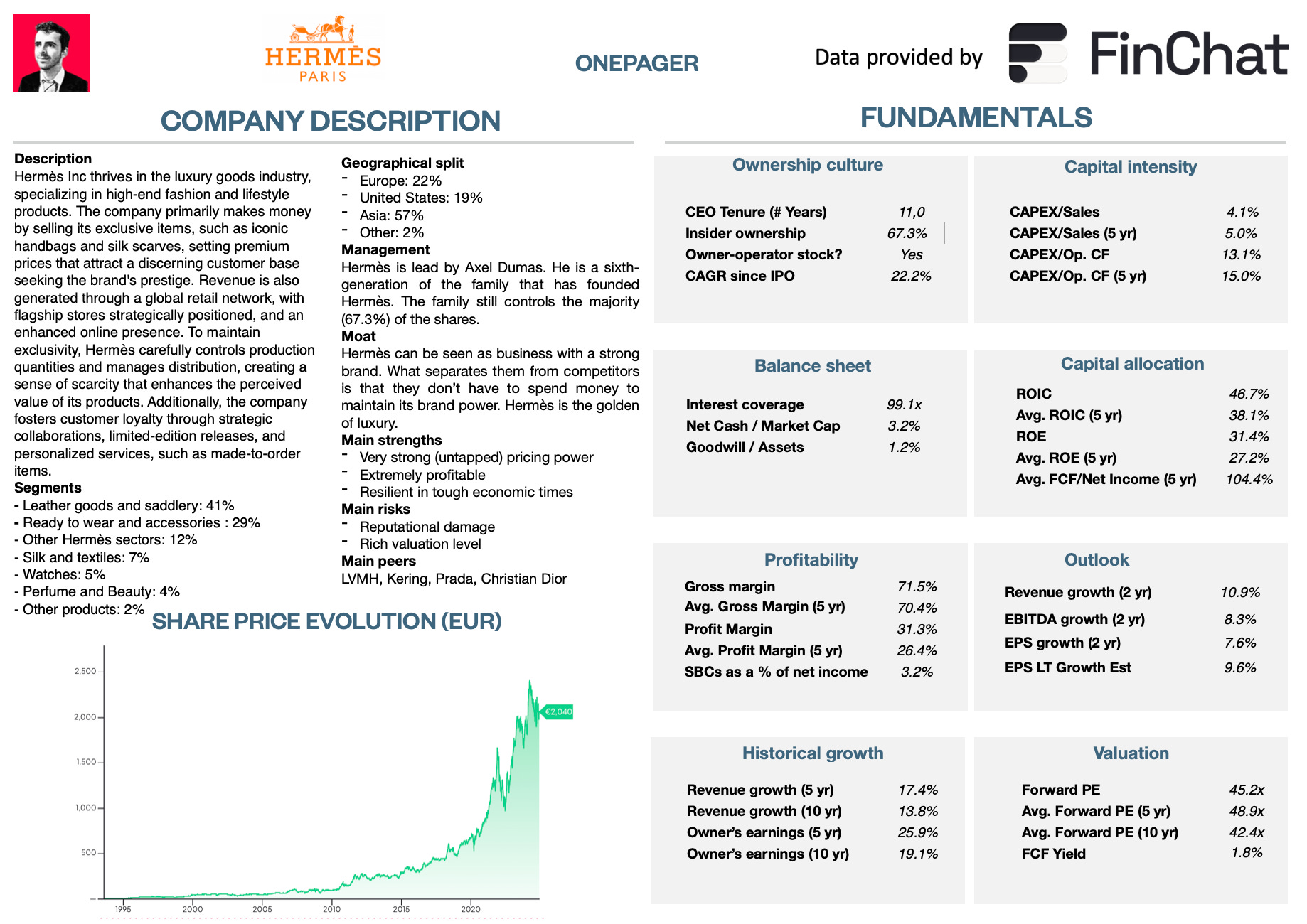

Onepager

Here’s a onepager with the essentials of Hermès (click on the picture to expand):

15-Step Approach

Now let’s use our 15-step approach to analyze the company.

At the end of this article, we’ll give Hermès a score on each of these 15 metrics.

This results in a Total Quality Score.

1. Do I understand the business model?

Hermès is the golden standard when you talk about luxury.

The French company is a global producer and distributor of luxury goods.

Hermès was founded in 1837 in Paris. It started by making saddles (hence the horse in the logo) and grew into a full luxury brand.

Hermès’ main value is its real craftsmanship. It takes longer to produce a Birkin bag (40 hours) than to manufacture a car (20-35 hours). Quality is everything.

If the bag isn’t perfect, it has to be burned.

It’s also great to see that this quality brand goes back 187 (!) years.

As Winston Churchill once said:

“The further back you can look, the further forward you are likely to see.”

In other words, the longer the company's track record, the more likely the company will keep doing well.

Here is the revenue split of Hermès:

Leather goods and saddlery (41%): Iconic bags like the Kelly, Birkin, and Constance, which are known for their high quality and style

Ready to wear and accessories (29%): Fashionable clothing and accessories, like Hermès gloves and the Kelly Belt, that people love for their luxury feel

Other Hermès sectors (12%): Home goods like the Concerto and Avalon collections and beautiful decorative trays

Silk and textiles (7%): Silk scarves, especially the carré, which people collect for their unique designs

Watches (5%): Stylish, high-end watches like the Arceau, known for its special asymmetrical look

Perfume and beauty (4%): Popular perfumes like Terre d’Hermès and Twilly d’Hermès

Other products (2%): Custom luxury work, like refitting high-end cars such as Bugattis with Hermès designs

2. Is management capable?

Axel Dumas has been the CEO of Hermès since 2013 and joined the company 20 years ago. He is the great-grandson of Émile Hermès, who founded Hermès in 1837.

The Hermès family still owns 67.3% of the business. It’s one of the richest families in the world.

Pierre-Alexis Dumas, another sixth-generation member of the Hermès family, is the company's artistic director.

Another positive is that roughly 80% of employees are shareholders of Hermès. This is a sign of a strong shareholder-orientated corporate culture.

3. Does the company have a sustainable competitive advantage?

Hermès’ moat comes from its strong brand. It can be seen as the golden standard in the luxury industry.

The company’s products are very exclusive. This is interesting because the prices of luxury goods are inelastic. It means that customers won’t stop buying the product when prices increase.

Hèrmes goes even further than being a luxury brand. Just like Rolex and Ferrari, you can’t just walk into a Hermès store and buy the most exclusive bag.

You must buy other less exclusive goods first, to buy the most iconic items. Afterward, you’ll be put on a waitlist. Once it’s your turn, you likely cannot even choose your colors.

The key conclusion from this?

Hermès dominates its customers, which makes them crave its products even more. The business still has a lot of untapped pricing power.

“Pricing power is one of the most desirable characteristics of a business. It enables managers to raise prices to not only keep up with inflation of input costs, but it also enables managers to drive revenue and profit increases above inflation.”

– Charlie Munger

Unlike most of its competitors, Hermès:

Doesn’t promote its products heavily

Doesn’t increase supply to meet demand (hence the waitlist)

Doesn’t have celebrity endorsements

Doesn’t even have a marketing department!

Hermès is all about quiet luxury. And yet everyone knows who they are and what they represent.

Companies with a sustainable competitive advantage are often characterized by the following:

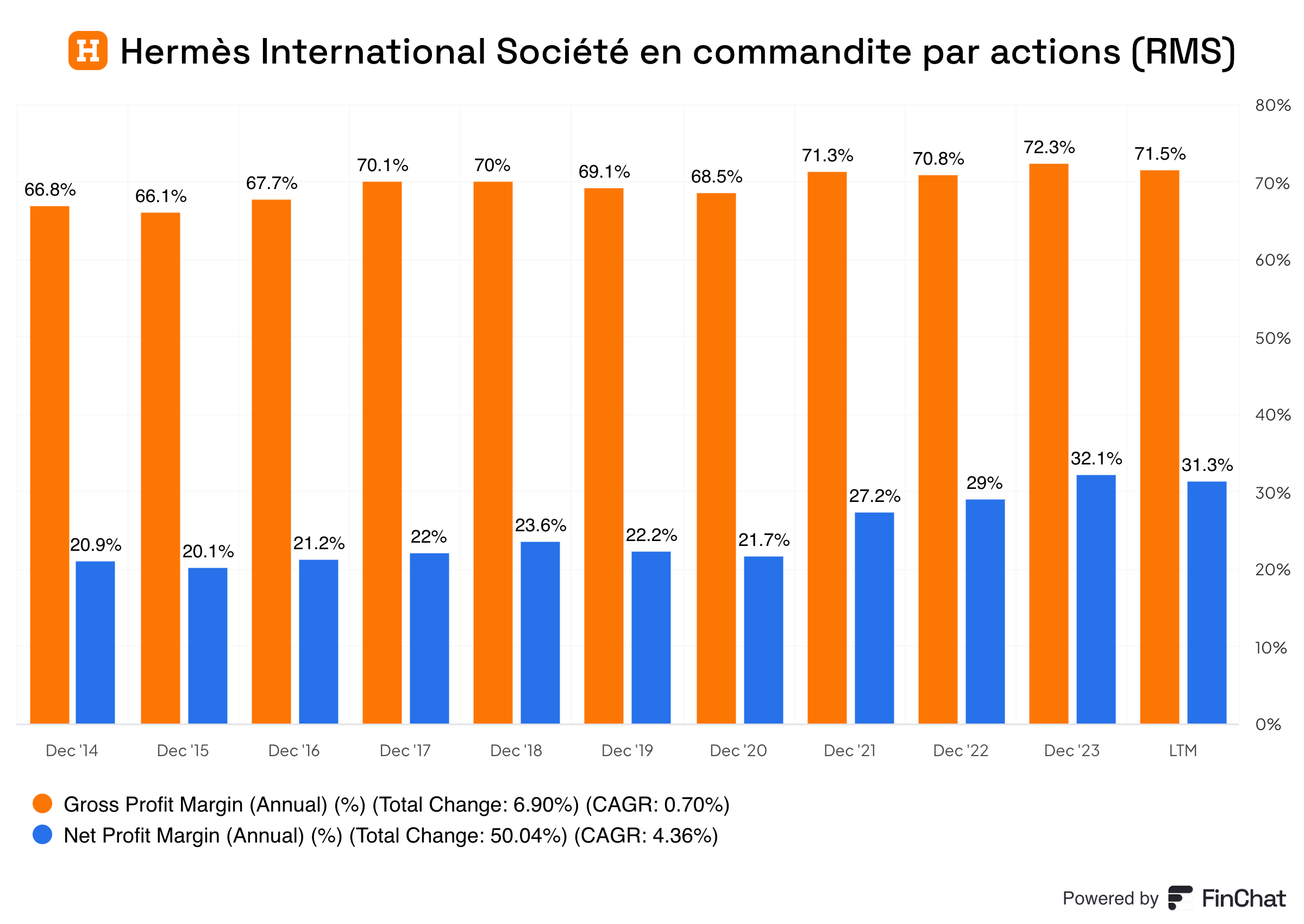

Gross Margin: 71.5% (Gross Margin > 40%? ✅)

Return On Invested Capital (ROIC) 46.7% (ROIC > 15%? ✅)

"We don't want to grow for the sake of growth. We want to preserve the things that make us different." – Axel Dumas, CEO of Hermès

4. Is the company active in an attractive end market?

Hermès is active in an attractive end market.

According to Bain & Company, the global luxury goods market is expected to double between 2020 and 2030.

The main reason for this? The growing middle class in Asia.

Here are a few of Hermès’ main competitors:

LVMH sells luxury goods like Louis Vuitton bags

Kering owns high-end brands like Gucci, Saint Laurent, and Balenciaga

Richemont is known for brands like Cartier, Montblanc, and Van Cleef & Arpels

Prada offers luxury fashion through its Prada and Miu Miu labels

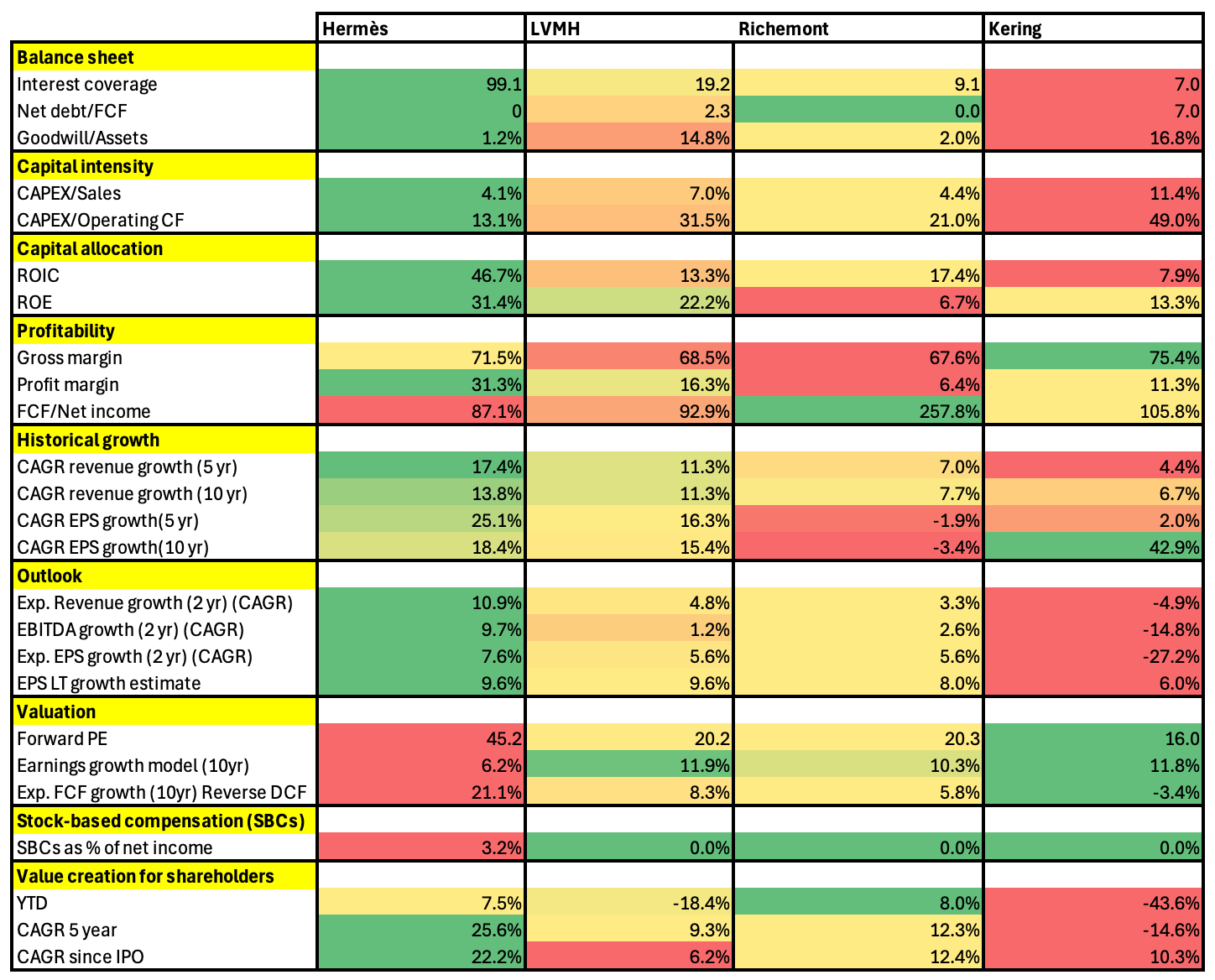

Here’s a comparison between Hermès and its most important competitors:

As you can see, Hermès is fundamentally better than its competitors. That’s why the stock is more expensive than LVMH, Richemont, and Kering.

5. What are the main risks for the company?

Some of the main risks for Hermès.

Gen Z may prioritize sustainable and affordable brands over luxury goods

Too dependent on one brand: Hermès’ revenue comes from just one brand

Birkin and Kelly handbags account for 25% to 30% of total revenue

Reputational risk: In the past, there was some drama about Hermès being cruel to crocodiles on a farm. People said the crocodiles were being raised and killed for their skin. Later, this news was found to be false, but it still hurt Hermès’ reputation. Bad rumors like this can make a brand less attractive.

The law of large numbers: the bigger a business gets, the more difficult it becomes to grow

High dependence on Asia for future growth

Rich valuation level (See later)

6. Does the company have a healthy balance sheet?

I look at 3 ratios to determine the healthiness of Hermès’ balance sheet:

Interest Coverage: 99.1x (interest coverage > 15x? ✅)

Net Debt/FCF: Net cash position equal to 3.2% of market cap (Net Debt/FCF < 4x? ✅)

Goodwill/Assets: 1.2% (Goodwill to assets < 20%? ✅)

Hermès has a very healthy balance sheet.

We love to see great companies with a healthy net cash position.

7. Does the company need a lot of capital to operate?

I prefer to invest in companies with a CAPEX/Sales lower than 5% and CAPEX/Operating Cash Flow lower than 25%.

Here’s what things look like for Hermès:

CAPEX/Sales: 4.1% (CAPEX/Sales? < 5%? ✅)

CAPEX/Operating cash flow: 13.1% (CAPEX/Operating CF? < 25%? ✅)

Hermès doesn’t need a lot of capital to operate.

8. Is the company a great capital allocator?

Capital allocation is the most important task of management.

We are looking for businesses that are capable of allocating the resources of shareholders effectively.

Hermès:

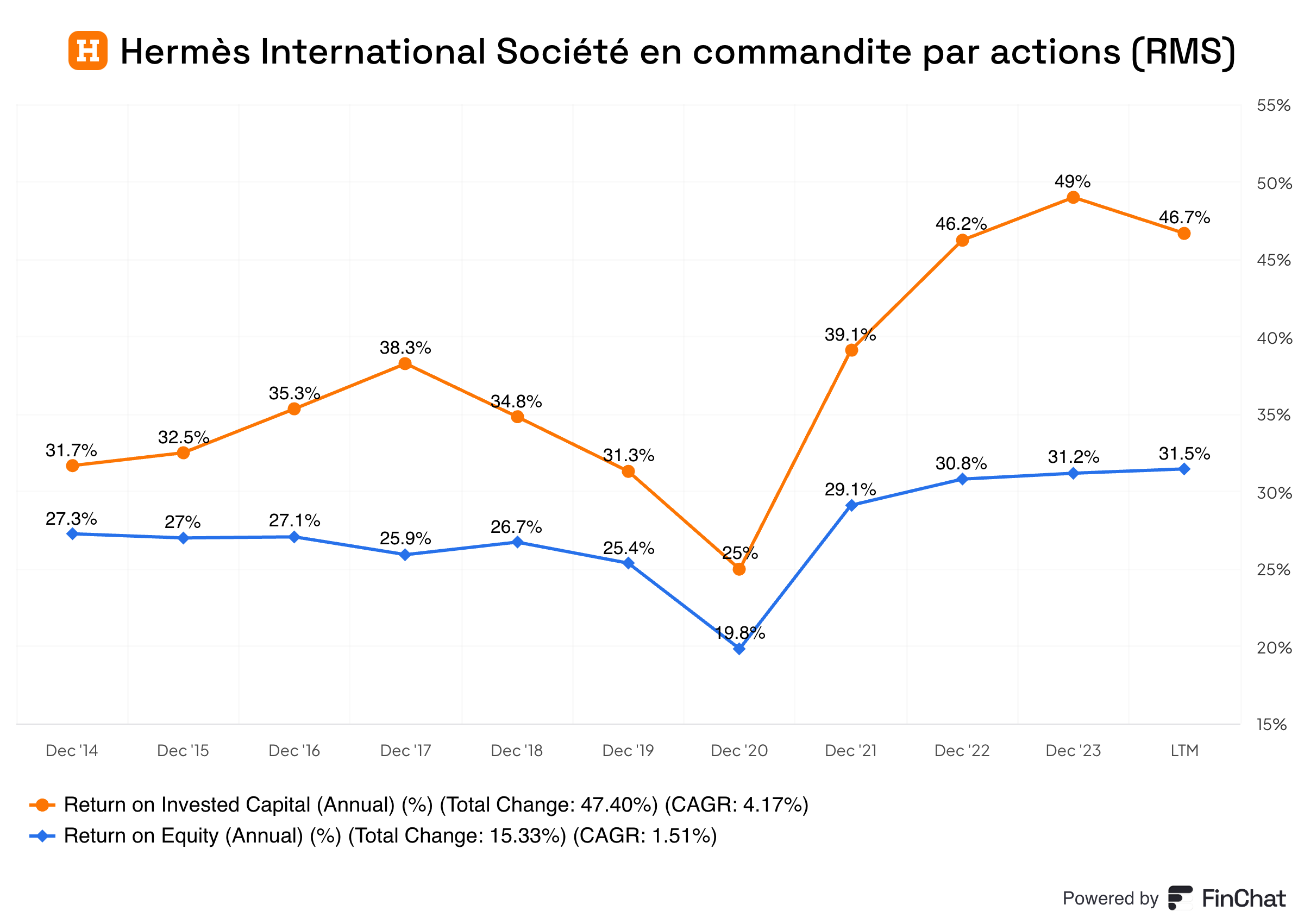

Return on equity (ROE): 31.4% (ROE > 20%? ✅)

Return on Capital (ROIC): 46.7% (ROIC > 15%? ✅)

Here’s an evolution of Hermès’ ROE and ROIC:

9. How profitable is the company?

The higher the profitability of the company, the better.

Here’s what thing looks like for Hermès:

Gross margin: 71.5% (Gross margin > 40%? ✅)

Net Profit Margin: 31.3% (Net Profit Margin > 10%? ✅)

FCF/Net income: 87.1% (FCF/Net income > 80%? ✅)

Hermès is a very profitable company.

10. Does the company use a lot of Stock-Based Compensation?

Stocks-based compensation is a cost for shareholders and should be treated accordingly.

Preferably we want SBCs as a % of Net Income to be lower than 4%.

Hermès:

SBCs of a % of Net Income: 3.2% (SBSs/Net income < 10%? ✅)

Avg. SBC as a % of Net Income past 5 years: 3.6% (SBCs/Net income < 10%? ✅)

It’s good to see Hermès does not use a lot of Stock-Based Compensation.

11. Did the company grow at attractive rates in the past?

I look for companies that grew their revenue and EPS by at least 5% and 7% per year in the past.

Let’s look at what the recent history tells us:

Revenue growth past 5 years (CAGR): 17.4% (revenue growth > 5%? ✅)

Revenue growth past 10 years (CAGR): 13.8% (revenue growth > 5%? ✅)

EPS growth past 5 years (CAGR): 25.1% (EPS growth > 7%? ✅)

EPS growth past 10 years (CAGR): 18.4% (EPS growth > 7%? ✅)

The luxury producer has grown at attractive rates in the past.

12. Does the future look bright?

You want to invest in companies that can grow at attractive rates as stock prices tend to follow EPS growth over time.

Hermès:

Exp. Revenue growth next 2 years (CAGR): 10.9% (revenue growth > 5%? ✅)

Exp. EPS growth next 2 years (CAGR): 7.6% (revenue growth > 7%? ✅)

Long-term growth estimate EPS (CAGR): 9.6% (EPS growth > 7%? ✅)

This outlook looks attractive.

13. Does the company trade at a fair valuation level?

I always use 3 methods to look at the valuation of a company:

A comparison of the forward PE multiple with its historical average

Earnings Growth Model

Reverse Discounted-Cash Flow

A comparison of the multiple with the historical average

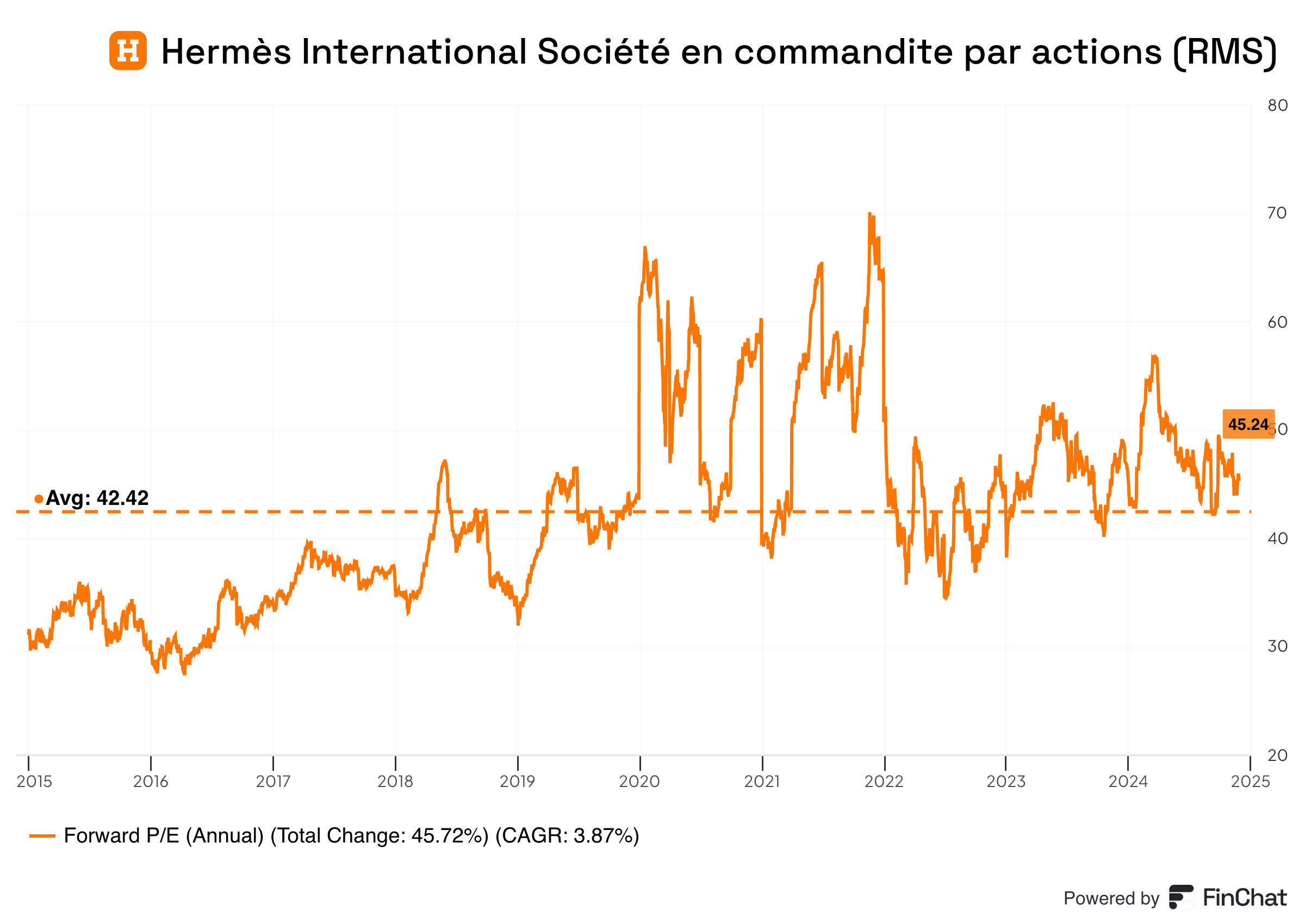

The first thing I do is compare the current forward PE with its historical average over the past 10 years.

Today, Hermès trades at a forward PE of 45.2x compared to a historical average of 42.4x.

This indicates Hermès trades at a (very) high valuation level.

Earnings Growth Model

This model shows you the yearly return you can expect as an investor.

In theory, it’s easy to calculate your expected return:

Expected return = EPS Growth + Dividend Yield +/- Multiple Expansion (Contraction)

Here are the assumptions I use:

EPS Growth: 10% per year over the next 10 years

Dividend Yield: 0.7%

Forward PE to decline from 45.2X to 30.0x

Expected yearly return = 10% + 0.7% + 0.1((30.0x – 45.2x)/45.2x)) = 7.3%

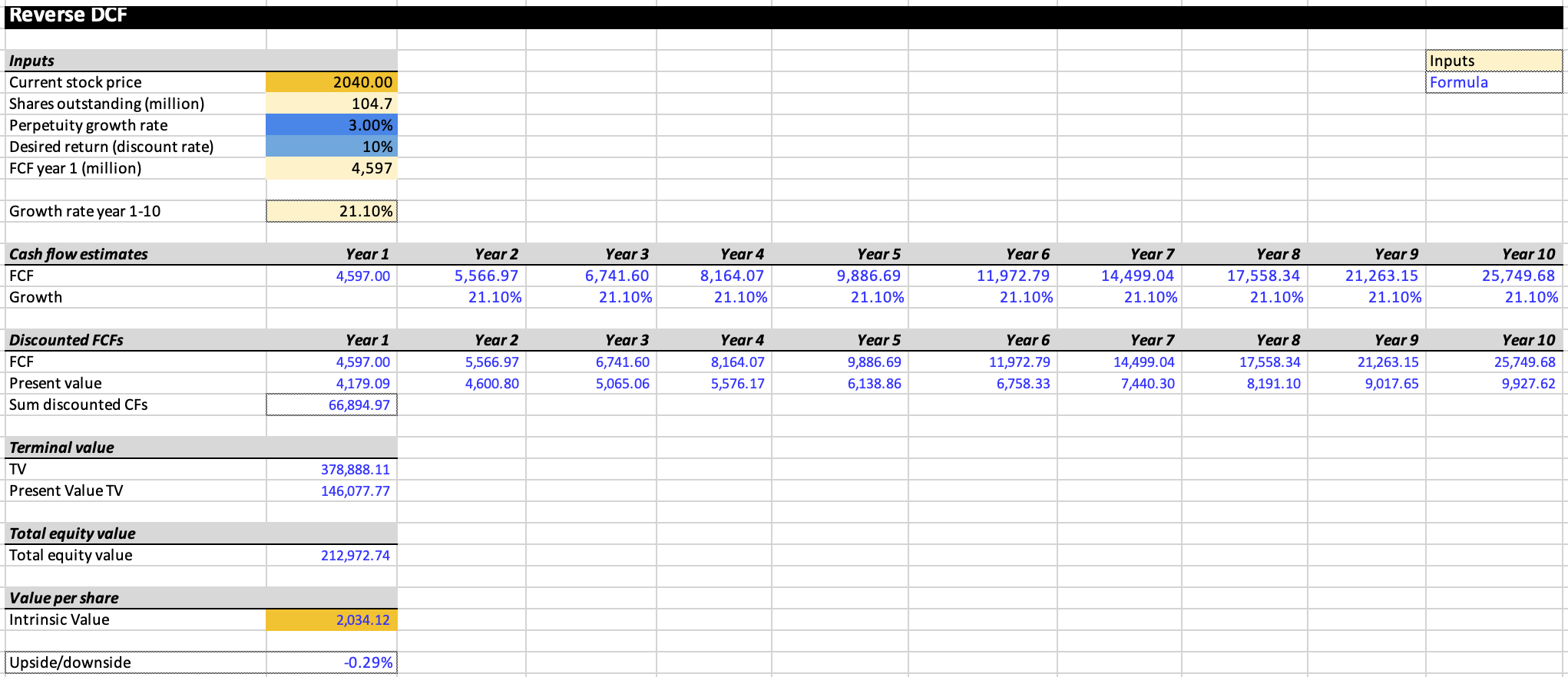

Reverse DCF

Charlie Munger once said that if you want to find the solution to a complex problem, you should invert. Always invert. Turn the problem upside down.

A reverse DCF shows you the expectations that are implied in the current stock price.

You try to determine for yourself whether these expectations are realistic or not.

You can learn more about a reverse DCF here: Reverse DCF 101.

The consensus states that Hermès’ Free Cash Flow over the next 12 months will be equal to €4.72 billion.

We subtract the Stock-Based Compensation (€143 million) and add Growth CAPEX (€18 million) to arrive at FCF in year 1 of €4.6 billion.

Under these assumptions, our Reverse DCF indicates Hermès should grow its Free Cash Flow by 21.1% per year to return 10% per year to shareholders.

Hermès is priced to perfection.

Hermès:

Forward PE: 45.2x (lower than its 10-year average? < 42.4x? ❌)

Earnings Growth Model: 7.3% (Yearly return? < 10%? ❌)

FCF-Growth Reverse DCF: 21.1% (Realistic growth expectations? ❌)

14. How did the Owner’s Earnings of the company evolve in the past?

Over time, stock prices tend to follow the Owner’s Earnings of a company (EPS Growth + Dividend Yield).

That’s why I want to invest in companies that have grown their Owner’s Earnings at attractive rates in the past. This is the case for Hermès.

Hermès:

CAGR Owner’s Earnings (5 years): 25.9% (CAGR Owner’s Earnings > 12%? ✅)

CAGR Owner’s Earnings (10 years): 19.1% (CAGR Owner’s Earnings > 12%? ✅)

15. Did the company create a lot of shareholder value in the past?

I want to invest in companies that can compound at attractive rates in the past.

Ideally, the company returned more than 12% per year to shareholders since its IPO.

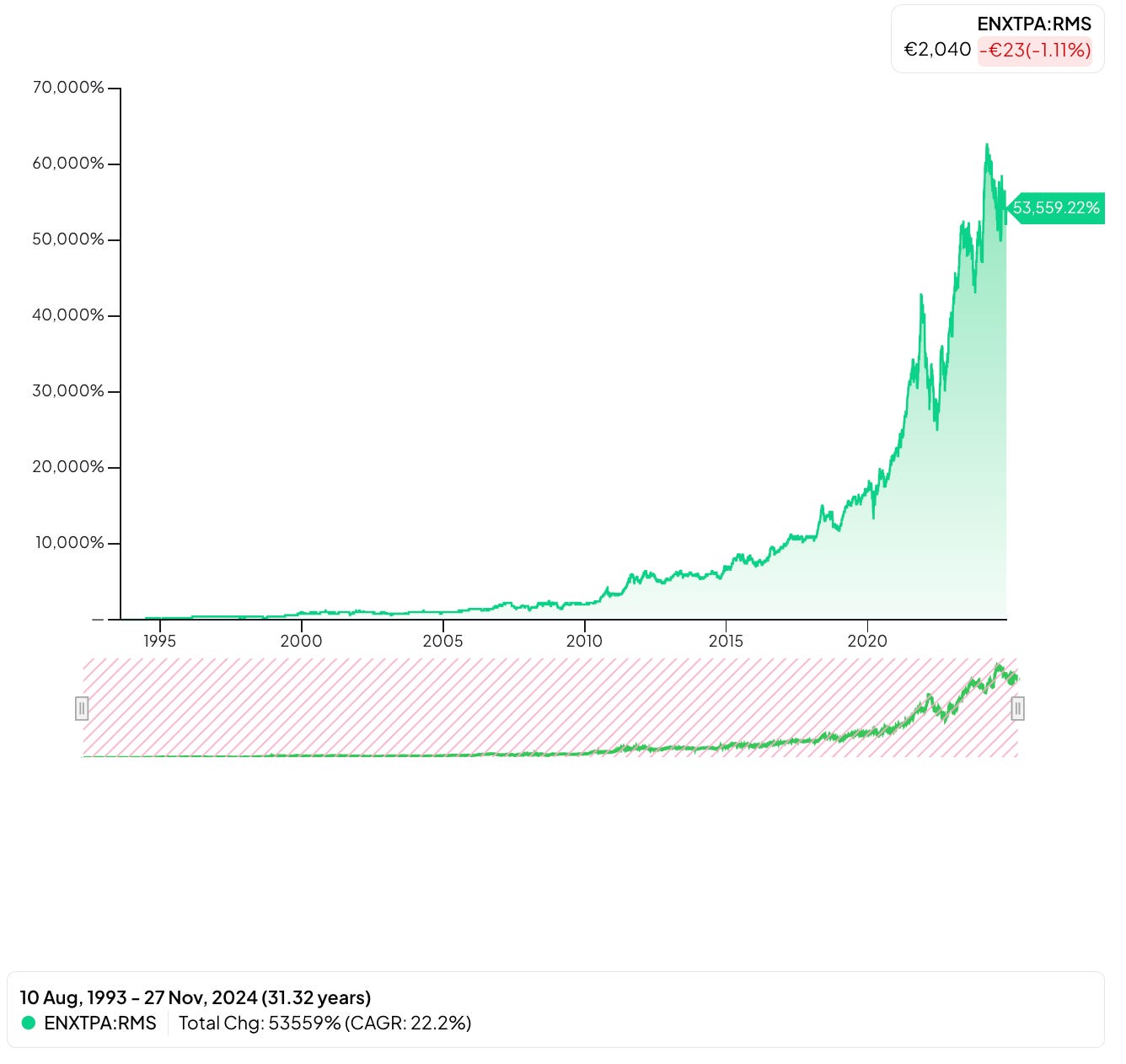

Here’s what the performance of Hermès looks like:

YTD: +7.6%

5-year CAGR: 25.6%

CAGR since IPO in 1993: 22.2% (CAGR since IPO > 12%? ✅)

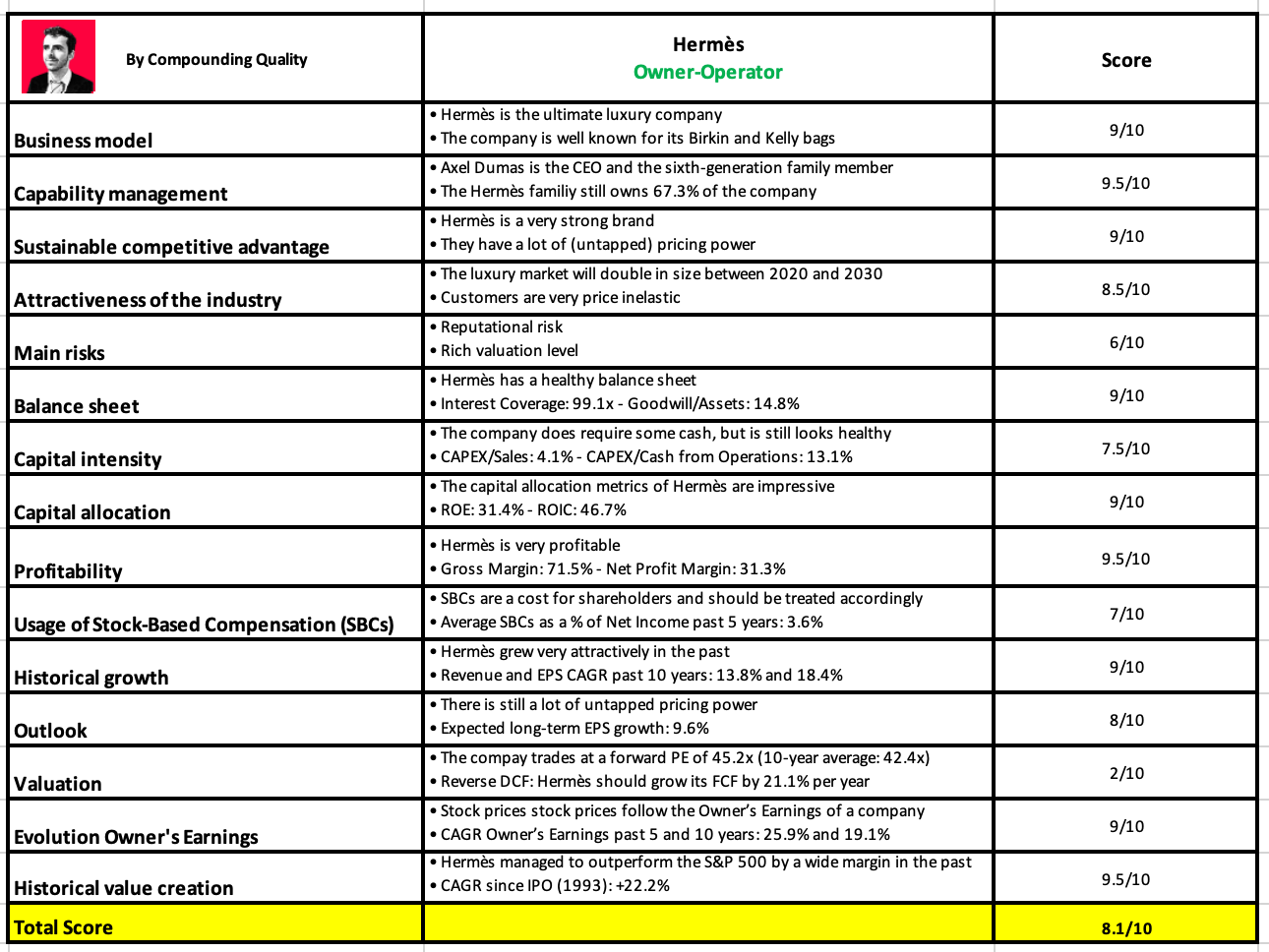

Quality Score

Finally, let’s bring everything together and give the company a Total Quality Score.

As you can see in the table below, Hermès gets a Total Quality Score of 8.1/10:

Hermès in one sentence: you pay a lot and get a lot. Howard Marks once famously said:

“Good investing doesn’t come from buying good things, it comes from buying things well.”

We don’t consider buying Hermès right now, but we would love to own it at the right valuation level.

That’s it for today. Here is what you are missing as a free subscriber:

More than 60 Investment Cases like this one of Hermès

Access to my Personal Stock Portfolio

Access to my ETF Portfolio

A Community where we discuss stock ideas every single month

Courses (How to find good stocks, how to analyze a company, …)

And much more

Everything In Life Compounds

Pieter

PS The best investment is always one in yourself. Partners can read 60 more investment cases like this one of Hermès.

Book

Order your copy of The Art of Quality Investing here

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Finchat: Financial data