📈Strategies that outperform the market

There are a lot of strategies that outperform the market. In his excellent book What Works on Wall Street, James O’Shaugnesey investigated which investment strategies worked the best over the past decade.

Do you want to outperform? Learn which strategies work here.

Size matters

In general, small cap stocks perform better than large cap stocks due to the law of large numbers.

Small cap stocks outperformed large cap stocks on average by 3,56% (!) per year between 1927 and 2009.

Valuation matters too

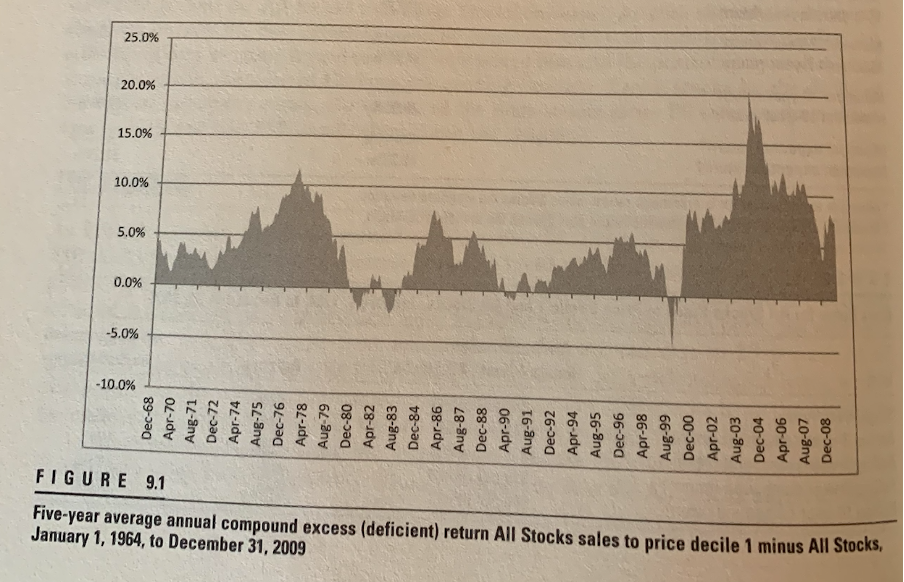

Price-to-sales ratio

The cheaper you can buy a stock, the better.

When you would have bought the cheapest companies based on the price-to-sales ratio, you achieved an annual return of 14.22% compared to 11.22% for the general market. This is an annual outperformance of 3% per year.

Buying the cheapest stocks based on this simple valuation metric seemed to have worked in the past if you executed it consistently.

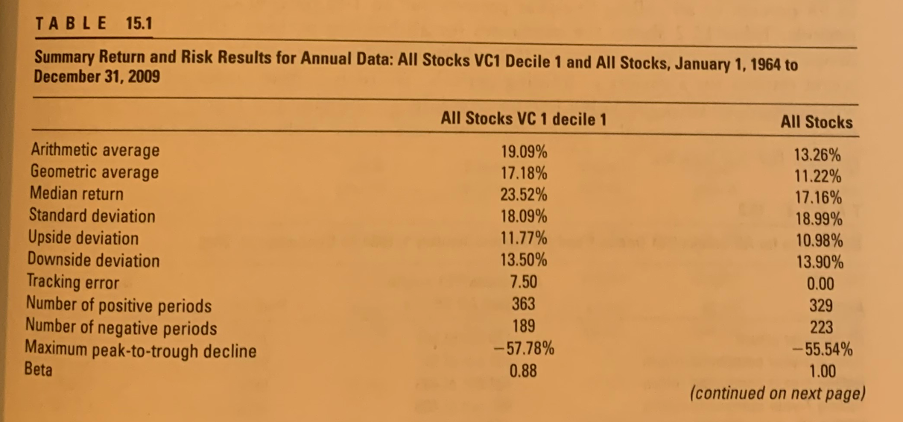

Price-to-earnings ratio

Between 1927 and 2009, it was a better strategy to buy stocks based on the cheapest P/E compared to the P/S ratio.

Investors who used this strategy outperformed the market by more than 5% per year, achieving an annual return of 16.3%.

This strategy outperformed the market in 76% of all the single-year periods and in 99% (!) of all 10-year periods.

The best valuation factors

In the picture below, you can find which valuation factors performed well between 1964 and 2019.

A low EV/EBITDA seemed to have worked the best as your $10.000 would have turned into more than $11.6 million (!) over the studied period:

Combination of value factors

However, if you further want to improve your performance, you should combine different value factors.

When you bought the cheapest stocks based on a combination of the P/E, P/B, EBITDA/EV, P/S and P/CF, you would have achieved a yearly return of 17.2% (!) per year between 1964 and 2009.

This is a yearly outperformance of almost 6%!

High dividend stocks do NOT outperform

Investing in high dividend yield stock does NOT work as it only slightly outperformed the market between 1927 and 2009.

When you want to invest in dividends stocks, don’t focus on dividend yield. Focus on dividend aristocrats (stocks with more than 25 years of consecutive dividend increases) with a durable payout ratio.

Free cash flow is king

Companies with the lowest accruals-to-price (where most earnings are translated into free cash flow) outperformed companies with the highest accruals-to-price (where there was a huge difference between earnings and free cash flow) with 5.3% per year.

Earnings are an opinion. Cash is a fact. Focus on free cash flow.

The healthier balance sheet, the better

Quality investors invest in companies with a healthy balance sheet.

In his book, O’Shaugnessey concludes that companies with the highest cash flow to debt (healthiest balance sheet) outperformed companies with the least healthy balance sheet with 8.0% (!) per year.

Don’t look at profit margins alone

When you would have just bought the companies with the highest profit margin, you would have underperformed the market.

This underlines why the competitive advantage (moat) is so important. When a company has a high profit margin but no moat, rivals will enter the market and reversion to the mean takes place.

Return On Equity (ROE) doesn’t work either

Good capital allocation is very important for investors.

When you would have bought the stocks with the highest Return on Equity (ROE), you would have only slightly outperformed the market by 1.07% per year.

However, in general it is a very good idea to combine good capital allocation metrics with a high profitability.

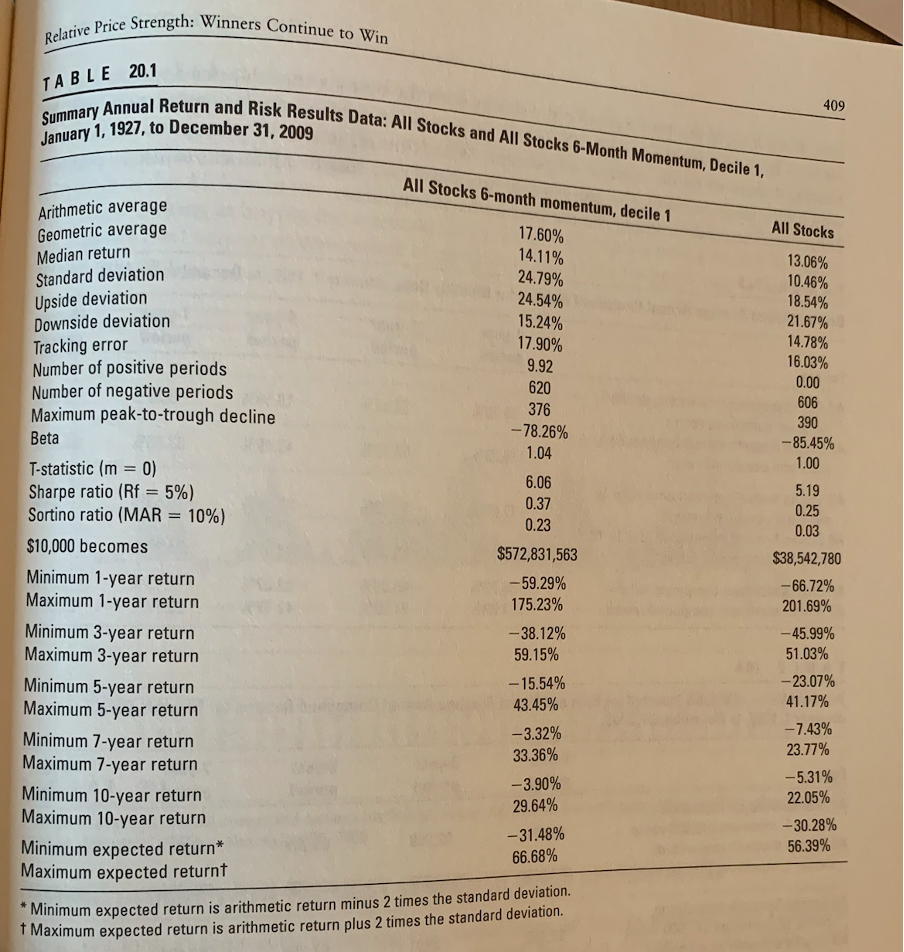

Momentum works great

In the short term, what goes up tends to keep going up and what goes down tends to keep going down.

A momentum-based strategy would have generated a return of 14.11% (!) per year over the studied period. This is an annual performance of 3.6% per year.

Golden egg: momentum + value

Do you want to further increase your returns? Buying the cheapest stocks with the best momentum has worked the best over the studied period.

This strategy (Trending Value) achieved an annual return of 23.04% (!) per year between 1964 and 2009. This is an annual outperformance of 10% (!) per year compared to the market.

Consistency is key

There are a lot of strategies that outperform the market. In general, it is important to note that you should stick to the strategy that suits you as an investor.

By definition, every active strategy will underperform the market from time to time. Discipline and consistency are key. Keep faith to your strategy and you’ll end up fine. Investing is a marathon, not a sprint.

More from us

Do you want to read more from us? Please subscribe to our Substack where we provide investors with investment insights on a weekly basis. You can also follow us on Twitter and Linkedin.

About the author

Compounding Quality is a professional investor which manages a worldwide equity fund with more than $150 million in Assets Under Management. We have read over 500 investment books and spend more than 50 hours per week researching stocks.

Awesome read, thank you for sharing! A question, how do you apply momentum with value in your investments? like above or shorter/longer?

So looking at VALUE trumps looking at profitability and growth???

I had just decided QCOM was a better investment than MU based on the following reasoning:

MU has a lower P/E ratio (forward PE) AND lower P/S ratio. BUT QCOM trumps MU on PEG ratio, Operating margins, ROA, and profit & earnings growth (yoy).

But according to your post, MU would be the better buy?

Similiar situation for GOOG vs MSFT.

GOOG is cheaper on several metrics but MSFT is more profitable and has higher growth. You would still prefer GOOG in this situation?

(on that account AMZN is WAY overpriced)

Thank you for the great post!