🍴The Ultimate Cannibal

Hi Partner 👋

I’m Pieter and welcome to a 🔒 subscriber-only edition 🔒 of Compounding Quality.

In case you missed it:

If you haven’t yet, subscribe to get access to these posts, and every post.

Tomorrow at the opening, we will buy a new stock.

It’s a Cannibal Stock that will buy back roughly 9% (!) of its outstanding shares per year.

The company trades at only 10x times earnings providing us with a very attractive expected return.

Cannibal Stock

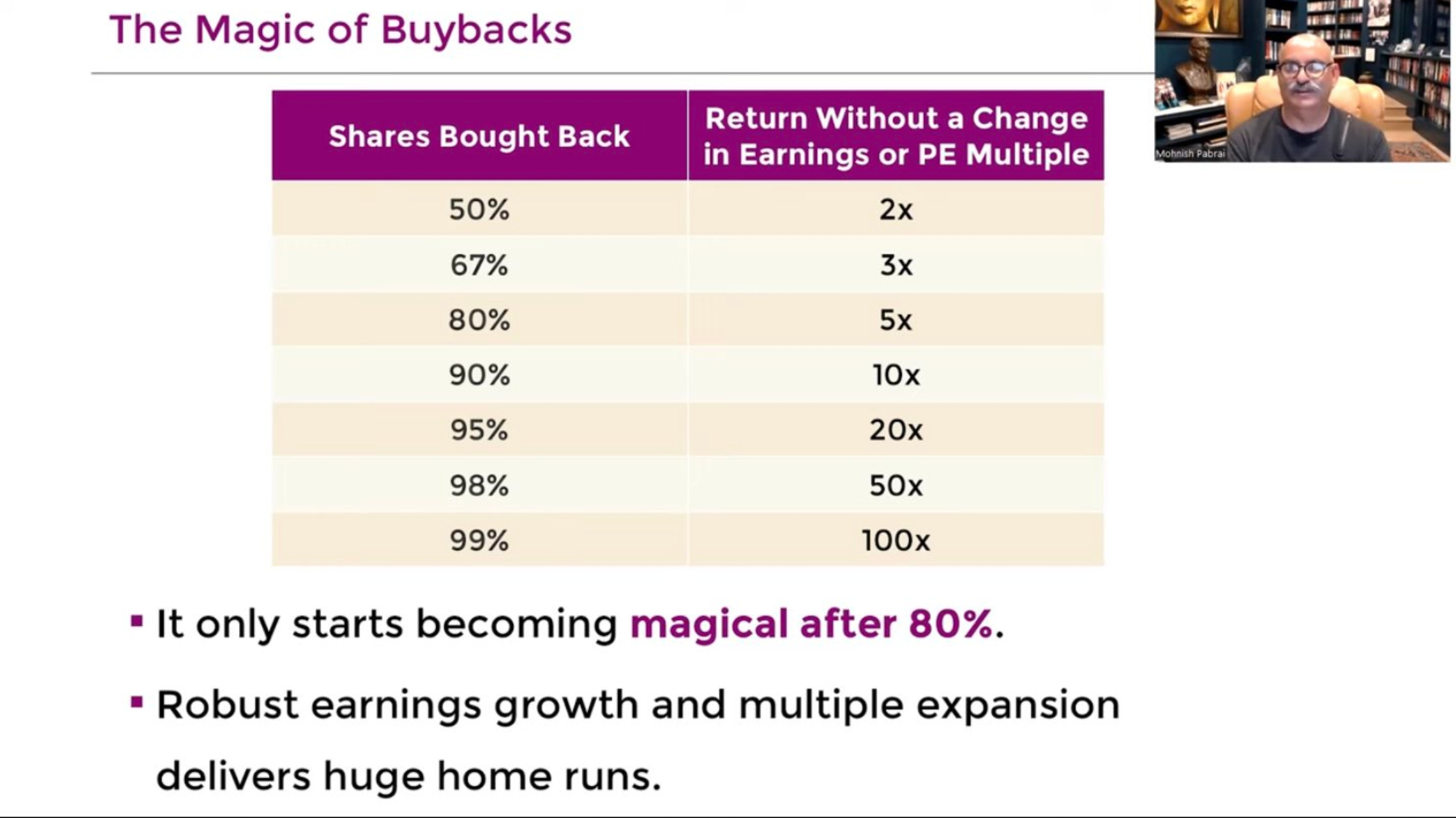

Cannibal stocks are companies that are heavily buying back their own shares.

If you own a business that earns $10 per share and the company buys back 50% of its outstanding shares, EPS will increase from $10 to $20. As a result, the stock price should also double.

Here’s an overview of the magic of buybacks by Mohnish Pabrai:

It is important to highlight that share buybacks only create value when the stock is undervalued.

This makes sense as buying back your shares can be seen as an investment in your own company.

As an investor, you also only want to buy stocks when they are undervalued.

Conclusion investment case

Our Next Buy is a leading diversified financial services firm with $1.2 trillion in assets under management and administration.

Through their extensive wealth management and asset management capabilities, they advise, manage, and protect the assets and income of more than 2 million individual, small business, and institutional clients.

The CEO and CFO have been working for the company for 40 and 55 (!) years respectively. Insiders own over 200,000 shares (value: $63 million).

Our Next Buy has a clear competitive advantage. The world of wealth management is characterized by enduring client-advisor relationships built on trust. Clients often remain with their financial advisors for a decade or more. While the costs to change from a financial advisor might not be that high, the potential benefits of switching are usually uncertain. Client retention is equal to over 90%. The company also benefits from economies of scale, having one of the industry's largest agent networks.

The company has a healthy balance sheet as 10% of its market cap is pure cash. Their capital intensity is also very low.

And guess what makes the business unique? It’s one of the best Cannibal Stocks I have seen. They use 90-100% of their free cash flow to distribute to shareholders via share buybacks and dividends. When you know the company trades at an Earnings yield of 9.2%, you know that the shareholder yield (buyback yield + dividend yield) equals 8.3%-9.2%. This is already quite an attractive return!

The company is also very profitable. They have a Gross Margin of 58.6% and a Net Income Margin of 18.9%.

At the end of last year, this business had $1.2 trillion in assets under management and administration. To put this number into perspective, Blackrock has $8.6 trillion in AUM.

The beautiful thing about these companies is that they are exposed to the stock market:

When the stock market increases → AUM increase —> the company earns more

Over the past decade, Our Next Buy has grown its revenue at a CAGR of 3.7% and its EPS at a CAGR of 15.7%. The company’s revenue growth is roughly equal to GDP growth in the very long term. The fact that the company’s EPS continued to grow at attractive rates can be explained by heavy share buybacks. In the future, I expect this trend to continue. I expect the company to grow its revenue by 3-4% in the very long term, its Net Income by around 5% per year, and its EPS by roughly 10% per year.

The key reason for buying this company is the combination of two things:

Heavy share buybacks

At very cheap valuation levels

Currently, the company trades at a forward PE of 10.9x. Our Earnings Growth Model expects a yearly return of 12.7% per year. Our Reverse DCF indicates that the company’s FCF is allowed to DECREASE by 0.4% per year over the next decade to return 10% per year to shareholders.

In the past, the company managed to create a lot of shareholder value. Since their IPO in 2005, the company compounded by 15.7% per year.

Now let’s tell you which company we are talking about, prepare our transaction for tomorrow, and share the full investment case of 40 (!) pages with you.