TransDigm: Mini-Monopolies at 30,000 Feet

Which companies come to mind when you think about the most successful serial acquirers?

Perhaps Constellation Software, Berkshire Hathaway, …

But a company often forgotten on that list is TransDigm.

In fact, here’s what a $1,000 investment 10 years ago would be worth today:

Berkshire Hathaway: $1,000 → $3,400

Constellation Software: $1,000 → $5,300

TransDigm: $1,000 → $8,500

Is Transdigm the perfect addition to Our Portfolio? Or did we miss the flight?

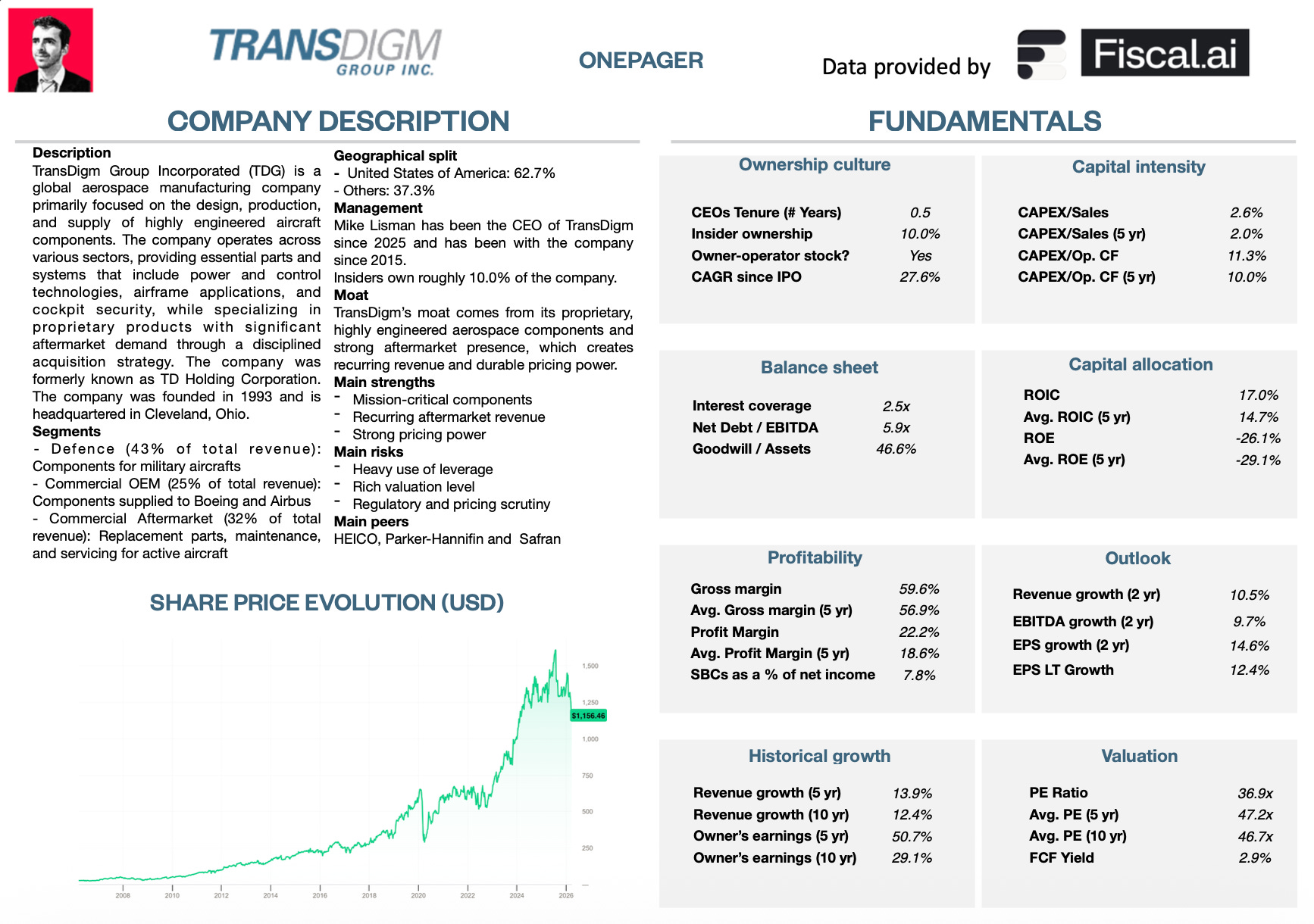

TransDigm - General Information

👔 Company name: TransDigm

✍️ ISIN: US8936411003

🔎 Ticker: TDG

📚 Type: Owner-Operator/Serial Acquirer/Collection of Monopolies

📈 Stock Price: $1,156.5

💵 Market cap: $65.3 billion

📊 Average daily volume: $430 million

Onepager

Here’s a onepager with the essentials of TransDigm:

15-Step Approach

Now let’s use our 15-step approach to analyze the company.

At the end of this article, we’ll give TransDigm a score on each of these 15 metrics.

This results in a Total Quality Score.

1. Do I understand the business model?

Have you ever noticed that on every flight you have been on, the seatbelts are always the same?

It doesn’t matter if you’re flying in America, Europe, or Asia

It doesn’t matter if it’s first class or economy

It doesn’t matter if Boeing or Airbus made the plane

It doesn’t matter if the carrier is Ryanair, Emirates, or American Airlines

It’s always the same seatbelt.

The reason for this?

There is one company that completely dominates the entire airplane seatbelt market: Amsafe.

And Amsafe is a subsidiary of TransDigm.

TransDigm paid $750 million for the company.

On first sight, this looks completely crazy, right? $750 million for a product that isn’t more than some steel and a strap.

Yet TransDigm has achieved returns of over 20% per year on this acquisition.

Here’s why:

Producing a typical commercial jet costs between $30 and $50 million

The average commercial aircraft carries about 200 passengers

Even if we’re generous and assume an airplane seatbelt costs $100, the total cost for all seatbelts on the plane would be $20,000 ($100 × 200).

Seatbelts are an essential component of an aircraft. You can’t take off without them.

Their total cost represents less than 0.1% of the aircraft’s overall cost.

Given that, do you think companies like Boeing, Airbus, or the airlines really care whether Amsafe charges $50 or $100 per seatbelt?

In addition, Amsafe has a market share of over 95%, approaching a near monopoly.

TransDigm benefits from 3 things:

Seatbelts are mission-critical

There is almost no competition

Seatbelts make up only a tiny portion of the total costs of an airplane

This gives them tremendous pricing power.

If you look inside TransDigm’s history, you’ll find plenty of stories like Amsafe.

TransDigm is a collection of mini-monopolies.

They own over 100 of these niche aviation subsidiaries: from seatbelts and soap dispensers to engine parts.

To some regard, you can compare niche aviation companies like TransDigm to Constellation’s Vertical Market Software (VMS).

These companies are mission-critical, only represent a tiny portion of total costs, and have little to no competition.

It’s the principle of ‘a tiny thing going into big things’.

Besides owning great businesses with strong pricing power, much of TransDigm’s success comes from its operating playbook.

The operating playbook

1. Price increases

TransDigm uses a value-based pricing system.

As co-founder Nick Howley explains:

“We don’t price products based on cost, but on the value we deliver to customers, which depends on the product itself and the switching costs.”

TransDigm raises its prices by 5–6% per year on average.

They do this every single year.

An interesting anecdote from Airbus says a lot.

When a part costs under $800 and doesn’t work on arrival, Airbus often doesn’t bother requesting a refund. Instead, they simply order a replacement.

The average price across TransDigm’s product portfolio is around $1,000.

See where this is going? Because its customers are very price insensitive, Transdigm can increase its prices year after year.

2. Cut costs

Cost-cutting measures are mostly related to people.

Since TransDigm’s IPO in 2006, sales have gone up 15x while headcount has only grown 13x.

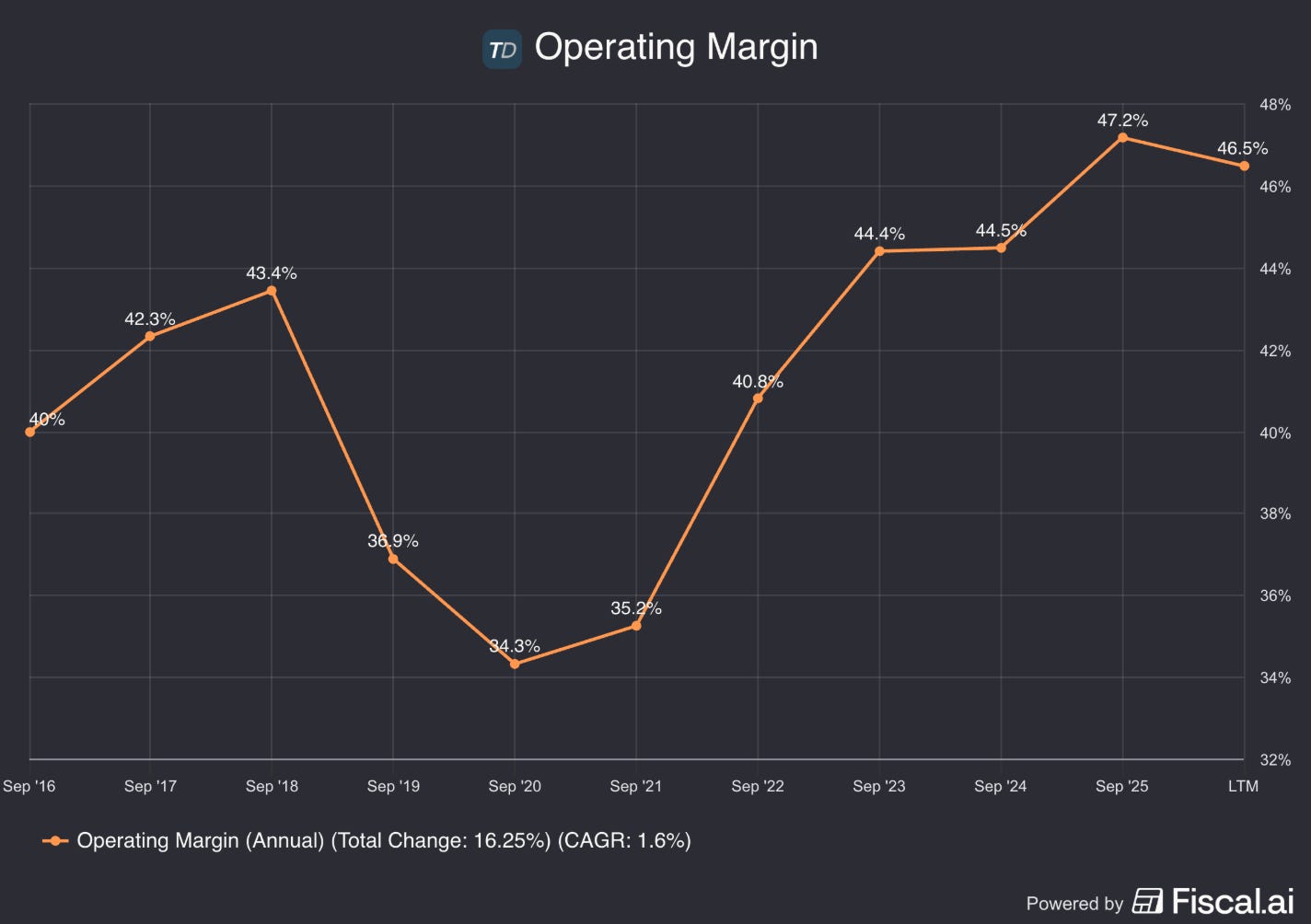

This extreme cost focus, in combination with pricing power, has translated into healthy operating margin expansion:

3. Profitable new business

Many aviation subsidiaries spend money on R&D projects where:

The probability of winning is low

Even if they win, the potential profit is limited

TransDigm aims to avoid wasting resources this way.

Instead of pursuing new business to increase sales, it focuses only on opportunities that drive earnings growth.

The results

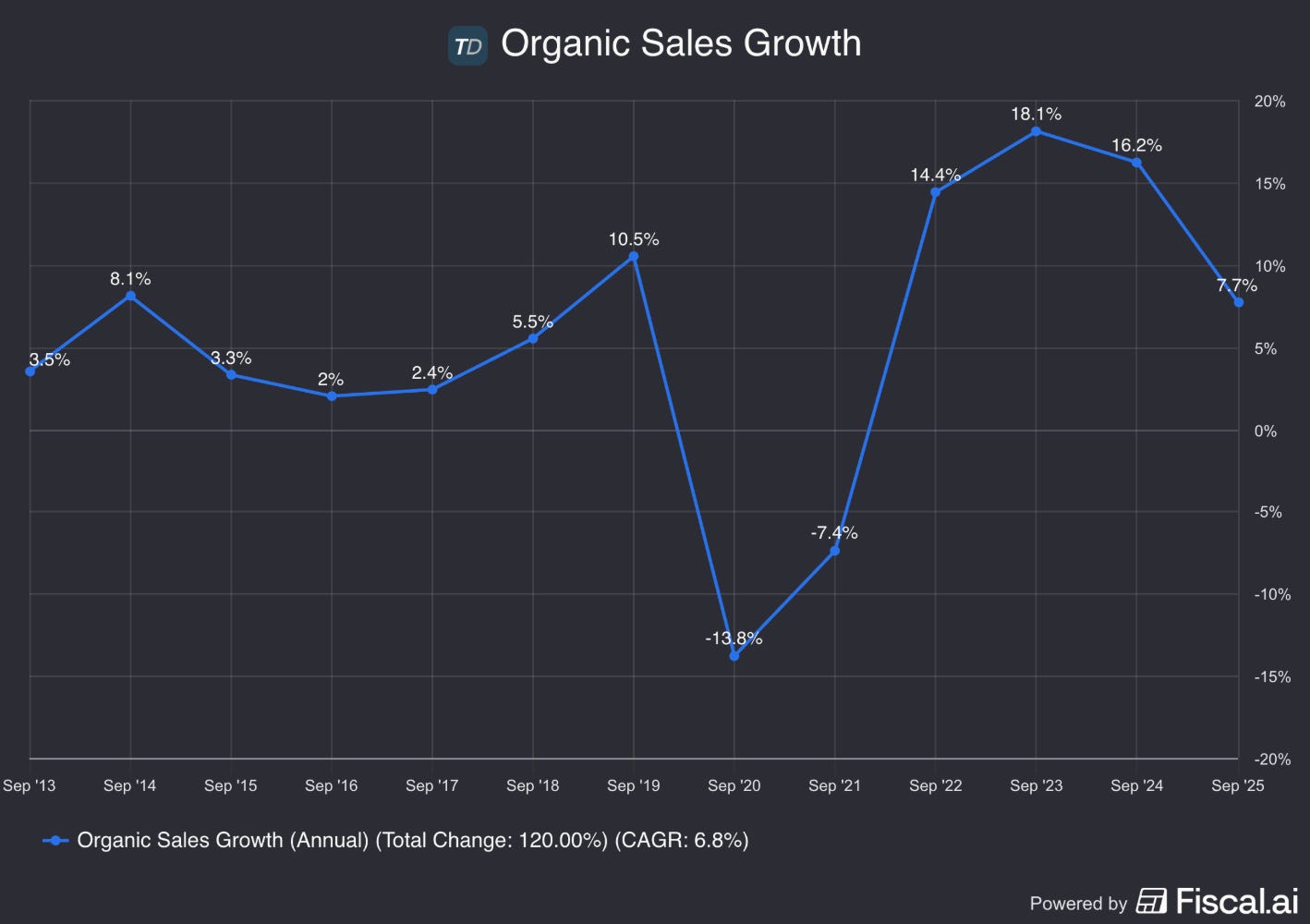

Implementing this playbook, TransDigm has achieved exceptional organic growth rates.

They grow well above the rate serial acquirers typically grow.

This chart highlights organic revenue growth.

Organic profit growth has been even stronger, driven by margin expansion within acquired businesses.

The reason for the drop in 2020? During the COVID-period, the aviation market was going through a rough time.

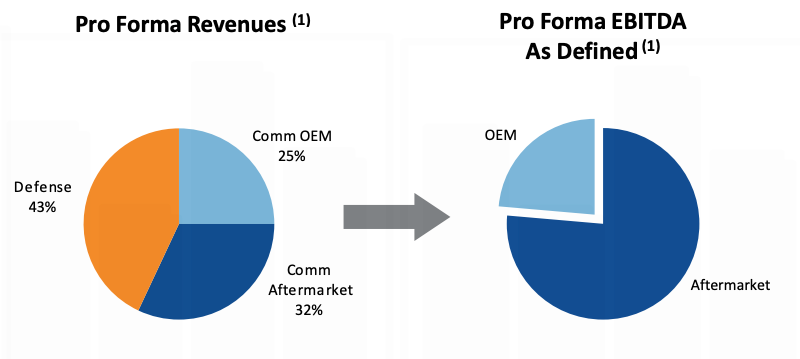

Revenue Split

TransDigm makes money in three ways:

Defense (43% of revenues): Next to commercial airlines, you can also find TransDigm’s parts on military aircrafts

Commercial Original Equipment Manufacturer (25% of revenues): These are products that TransDigm sells to Boeing and Airbus

Commercial Aftermarket (32% of revenues): Airplanes are typically 30-50 years in the sky. Across this lifetime, some parts need replacement. This is what they call “the aftermarket”. It can be seen as recurring revenue. It’s a stable segment during downturns

As you can see in the chart above, margins in the Aftermarket are much higher compared to the OEM market.

The explanation? TransDigm uses a razor-razorblade model.

In a razor-razorblade model, the initial product (the “razor”) is sold at very low margins, sometimes even at a loss, while the replacement parts or aftermarket products (the “razorblades”) are sold at much higher margins.

The higher margins on replacement parts come from stronger pricing power.

In older, shrinking aircraft fleets, new competitors have little incentive to enter the market. There is already an established manufacturer, demand is gradually declining, …

This makes the required investment to enter unattractive.

This lets established makers like TransDigm act like a monopoly and push prices higher.

Summary

This slide summarizes the business model quite well:

2. Is management capable?

The strong success of TransDigm’s model has attracted competitors.

One of them was a company called McKechnie Aeroscace, a TransDigm 2.0.

TransDigm eventually bought McKechnie for $1.3 billion.

During the first months after the acquisition, the former McKechnie CEO continued to work at the company alongside the TransDigm team to lead the transition.

After working with TransDigm, he said this:

“These guys are so much better than I ever imagined. I totally underestimated how they do what they do ... It’s crazy because every day we were trying to copy them.” - Former McKechnie CEO on TransDigm

The key person from the TransDigm team? Nick Howley.

Howley is the co-founder and a former CEO of TransDigm.

It’s fair to put Howley on the same level as Mark Leonard or even Warren Buffett.

Here’s why:

1. Winning the Singleton Prize

Cary and Will Singleton (two children of the legendary Henry Singleton) founded the Singleton Foundation.

Every year, the Foundation gives a prize to an exceptional CEO with a tremendous track record of creating per-share value.

On its jury are Will Thorndike (The Outsiders), Todd Combs (ex-Berkshire), and Mark Leonard (Constellation Software).

In 2022, Nick Howley won the Singleton prize.

You can click here to find more information about this and watch a great video on Howley’s thinking.

2. A flawless track record

During his tenure as a CEO, Howley made 50 to 82 acquisitions. It depends on how you look at it.

They acquired 50 companies, but some were holding companies consisting of multiple operating companies, hence 82.

According to Howley and the math of Will Thorndike, all these acquisitions created private equity-like returns (>15%).

Studies have found that close to 70% of acquisitions destroy shareholder value.

The probability of a 0% loss rate when doing 82 acquisitions is 0,0000000000000000000000000000000000000000133% (=0.3^82).

Let alone getting +15% on each acquisition.

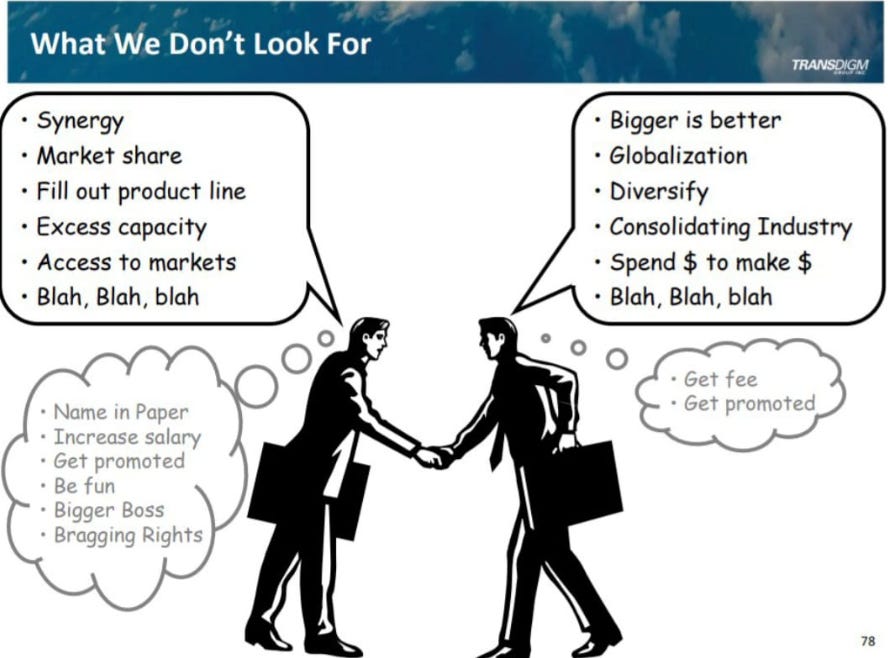

TransDigm has an iconic slide on what not to look for in M&A:

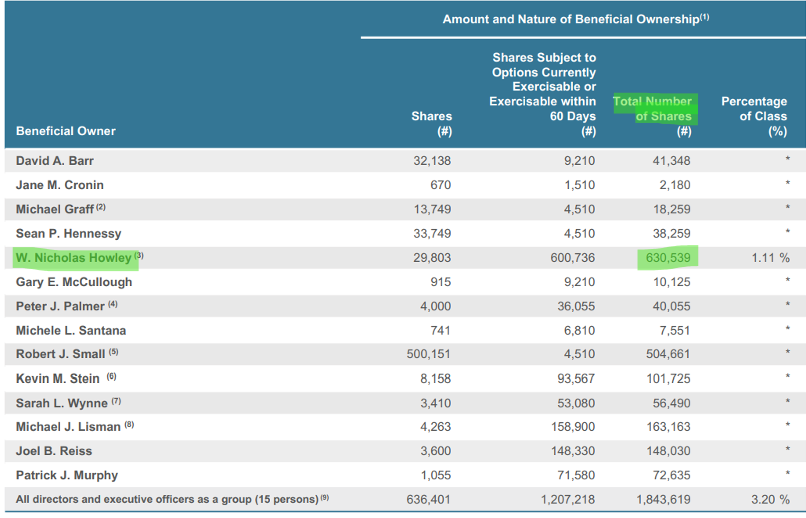

Unfortunately, Howley is no longer CEO, but he remains Chairman of the Board, where he oversees major capital allocation decisions. Think about special dividends, share repurchases, or acquisitions.

Howley still owns 630,000 TransDigm shares worth around $750 million, which is probably the vast majority of his net worth.

Total insider ownership (Board + Executive Team) is around 10%.

This is high insider ownership for a company as large as TransDigm (Enterprise Value is close to $100B).

Skin in the game is an important concept for TransDigm:

“The more you can make people feel like owners, pay them like owners, and treat them like owners, the more they will act like owners” - Nick Howley

A perfect Tiny Titan?

What’s interesting? Howley and his team are now applying the TransDigm playbook in a small-cap together with a former Buffett lieutenant.

The company we are talking about has a Board of Directors of 9 people:

5 of them have a TransDigm history

1 of them is Will Thorndike

And another is called “a Buffett protege”

It’s basically a sector-agnostic TransDigm with a massive runway.

If you want to learn more about this company, I would highly encourage you to leave your email address here:

You’ll receive the investment thesis in your mailbox shortly.

Current TransDigm CEO

The current CEO is Mike Lisman.

Lisman has plenty of experience within TransDigm. He previously served as:

Chief Operating Officer

Chief Financial Officer

Vice President of M&A

Business Unit Manager of a TransDigm subsidiary

He has experience in capital allocation and in operations. A combination that not many CEOs have.

Lisman has also been buying shares recently on the public market.

3. Does the company have a sustainable competitive advantage?

It’s hard to think of a more regulated market than airplane parts.

A funny example of this? Even the soap dispensers on planes need approval from the Federial Aviation Administration (FAA).

Getting FAA approval is a very expensive and time-consuming thing, which creates a high barrier to entry.

An interesting statistic: most of the airplane parts manufacturers have been in business for over 70 years.

It’s almost impossible to disrupt these companies.

If you look at TransDigm’s portfolio, you’ll notice that it largely consists of the more “boring” components of an aircraft. These companies are even more resilient.

As the saying goes in the industry:

“Airlines buy new planes for fuel efficiency, not seatbelts.”

According to Morningstar, TransDigm has a wide moat.

“We assign TransDigm as a wide moat company based on switching costs that arise from the lack of alternatives to its products with very long regulated maintenance cycles,” - Morningstar

Morningstar also mentions the lack of alternatives.

According to TransDigm, 80% of its revenue comes from products for which it is the only provider.

4. Is the company active in an attractive end market?

Bain & Company has an excellent report on the future of air travel.

They share some very interesting insights:

“Over the long run, the fundamentals for air travel remain strong. More efficient aircraft, falling real ticket prices, and rising demand in developing markets will keep air travel on a growth trajectory.” - Bain & Company

And on top of that, Boeing and Airbus can’t keep up with the demand, which results in huge aircraft backlogs.

This is especially interesting for a manufacturing company like TransDigm:

“Aircraft production and maintenance continue to lag far behind demand. Legacy fleets are operating years past their intended retirement as new aircraft deliveries fall short of targets (see Figure 3). Adding to the squeeze, record numbers of aircraft are grounded, waiting for overdue maintenance. Aircraft backlogs are huge. Manufacturers are making substantial efforts to support their supply chains, but are unable to close the gap. Disruptions and parts shortages persist, limiting the number of new aircraft built. In 2024, Boeing and Airbus grew their fleets by only 4.7%, well short of the 6.8% growth needed to meet demand and enable normal retirement rates, according to Bain analysis.” Bain & Company

Another direct effect of the aircraft backlog? The global aircraft fleet is meaningfully older than it was a couple of years ago, as fewer new planes are being built.

Older aircraft require more replacement parts, driving TransDigm’s aftermarket sales up.

Next to the airline industry, TransDigm also has exposure to the defense market (43% of Total Sales), another structurally growing end market.

Recently, Trump raised the defense budget from $1.5 trillion to $2.0 trillion annually.

Overall, TransDigm clearly operates in structurally growing end markets.

5. What are the main risks for the company?

Here are the key risks for TransDigm:

Potential parts failure: TransDigm operates in a “cannot fail” environment. If a TransDigm part were to fail in the air, it could be catastrophic for the company

Bad reputation: Bears often describe TransDigm like this: “TransDigm acquires airplane parts, fires people, and egregiously raises prices.” Especially the price increases make many investors skeptical

Charlie Munger once said this after studying the company:

“I don’t like that way of making money... It’s too brutal. They figure out something that has a little monopoly due to the defense department regulations, and they raise the price 10 times. And they’re famous for it. I regard that as immoral.” - Munger

It’s interesting to read this, given how much Munger emphasized the importance of pricing power in quality companies.

Competition from HEICO: HEICO makes aircraft replacement parts.

It reverse-engineers existing components and sells them under the FAA’s Parts Manufacturer Approval (PMA) program. PMA lets companies other than the original maker produce approved spare parts. This reduces the risk of monopolies in the aftermarket. The use of PMA parts has increased in recent years.

Keep in mind that most of TransDigm’s profits come from the aftermarket.

Heavy use of leverage: TransDigm runs with an aggressive balance sheet, leveraging up to 6× EBITDA.

Rich valuation level: We’ll talk about this later

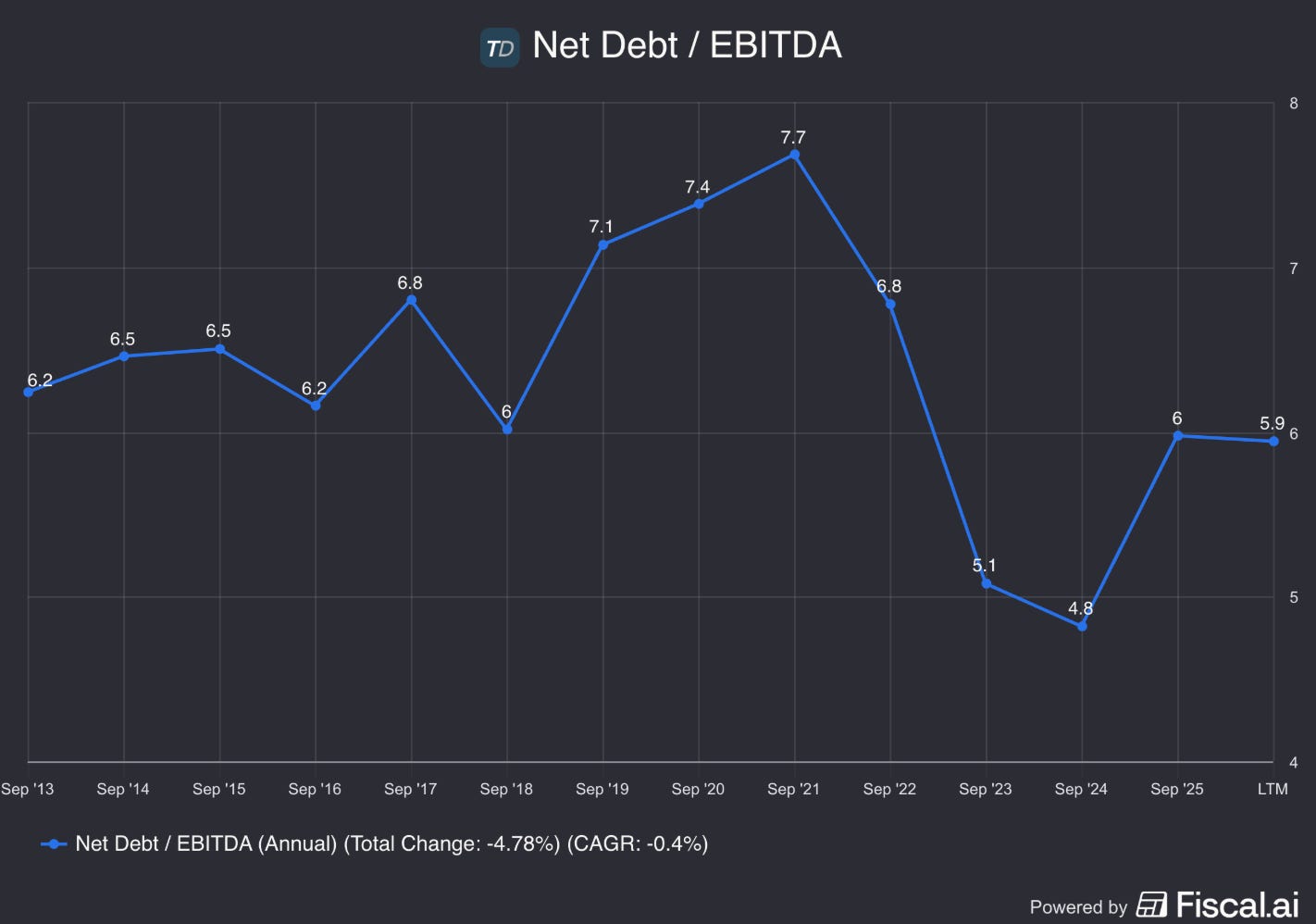

6. Does the company have a healthy balance sheet?

We look at three ratios to determine the healthiness of TransDigm’s balance sheet:

Interest Coverage: 2.5x (Interest Coverage > 15x? ❌)

Net Debt/EBITDA: 5.9x (Net Debt/EBITDA < 4x? ❌)

Goodwill/Assets: 46.6% (Goodwill/assets not too large? < 20% ❌)

TransDigm does have a serious amount of debt on its Balance Sheet.

However, it’s not unusual in TransDigm’s history:

There are two reasons why this is less concerning than initially thought:

While the Balance Sheet is clearly aggressive, TransDigm is very conservative in its M&A, often even underwriting multiple contractions

The aftermarket provides steady, recurring revenue

Nevertheless, we still prefer companies with less debt.

Last year, TransDigm also raised debt to fund a special dividend. This doesn’t make much sense in our opinion.

7. Does the company need a lot of capital to operate?

We prefer companies that don’t need a lot of capital to operate.

Here’s how TransDigm looks:

CAPEX/Sales: 2.6% (CAPEX/Sales < 5%? ✅)

CAPEX/Operating Cash Flow: 11.3% (CAPEX/Operating CF? < 25% ✅)

TransDigm is a capital-light business.

8. Is the company a great capital allocator?

Capital allocation is the most important task of management.

We like to invest in companies that put shareholders’ money to use at attractive rates of return.

TransDigm:

Return On Equity (ROE): -26.1% (ROE > 20%? ❌)

Return On Equity = Net Income/Equity

TransDigm is very profitable, but it’s Equity is negative for two reasons:

Their capital structure relies on Debt instead of Equity

They just paid a big Special Dividend. As a result, retained earnings are low.

In short, TransDigm is very profitable, so a negative ROE is not a bad sign here

Return On Invested Capital (ROIC): 17.0% (ROIC > 15%? ✅)

TransDigm’s capital allocation policy is centered around Special Dividends, M&A, and occasional Buybacks.

TransDigm’s 10-year historical Shareholder Yield (Dividend Yield + Buyback Yield) has been close to 3%.

It’s also important to look at the runway.

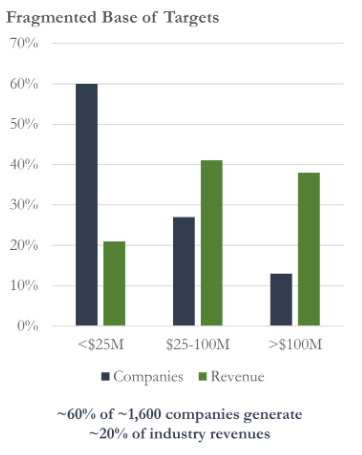

TransDigm estimates that there are still over 1,000 potential acquisition targets in the aerospace business.

In its latest quarter, TransDigm acquired three businesses, proving they can still find good deals.

9. How profitable is the company?

The higher the profitability of the company, the better.

Here’s what things look like for TransDigm:

Gross Margin: 59.6% (Gross Margin > 40%? ✅)

Net Profit Margin: 22.2% (Net Profit Margin > 10%? ✅)

Average FCF/Net Income past 5 years: 100.0% (FCF/Net Income > 80%? ✅)

Keep in mind that FCF is not a clear number in TransDigm’s case, given the Stock-Based Compensation expenses (more on this later).

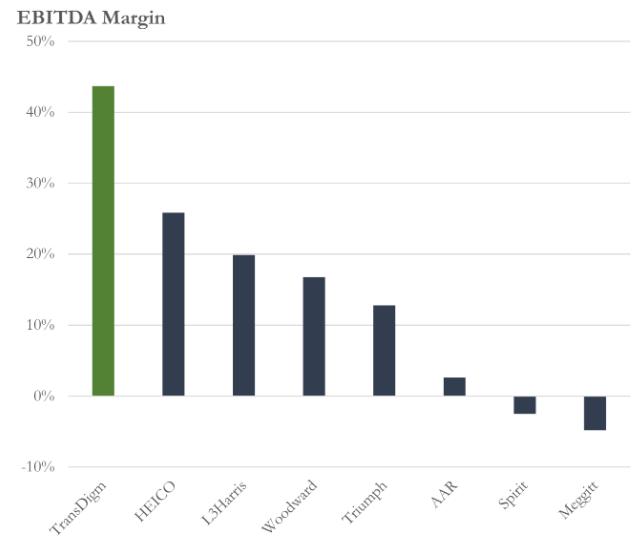

These are very healthy margins.

And what’s even more interesting? TransDigm’s margins are miles above its competitors:

10. Does the company use a lot of Stock-Based Compensation?

Stock-based compensation is a cost for shareholders and should be treated accordingly.

TransDigm:

SBCs as a % of Net Income: 7.8% (SBCs/Net Income < 10%? ✅)

Avg SBC as a % of Net Income past five years: 11.0% (SBCs/Net Income < 10%? ❌)

TransDigm uses quite some Stock-Based Compensation.

We will take this into account in our valuation model later.

11. Did the company grow at attractive rates in the past?

We seek companies that managed to grow their revenue and EPS by at least 5% and 7% per year.

TransDigm:

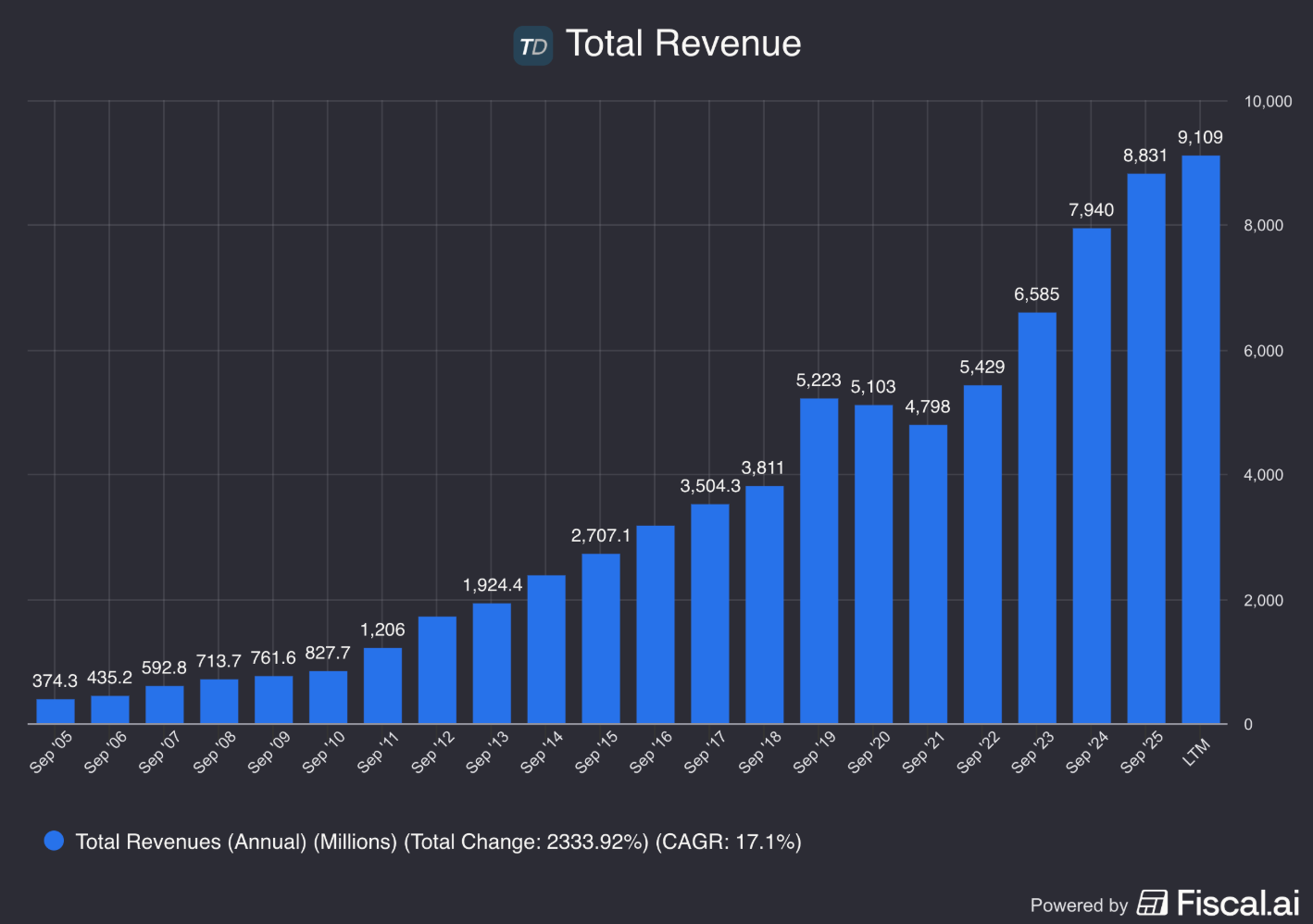

Revenue Growth past 5 years (CAGR): 13.9% (Revenue growth > 5%? ✅)

Revenue Growth past 10 years (CAGR): 12.4% (Revenue growth > 5%? ✅)

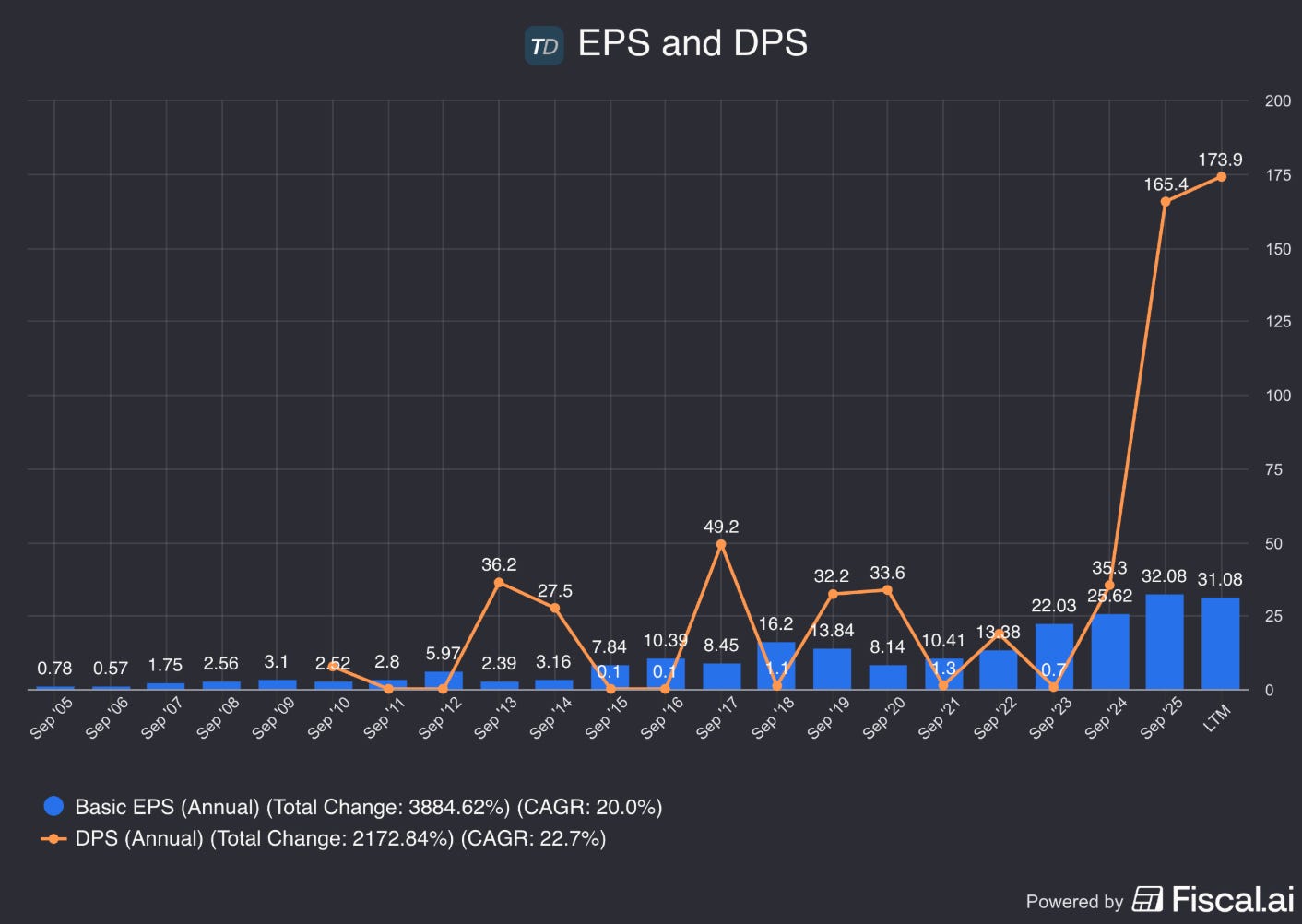

EPS Growth past 5 years (CAGR): 35.5% (EPS growth > 7%? ✅)

EPS Growth past 10 years (CAGR): 13.9% (EPS growth > 7%? ✅)

These are numbers that only a few incredible compounders can show.

And the business keeps delivering.

In the most recent quarterly numbers, sales were up 13.9% (of which 7.4% organic) once again.

12. Does the future look bright?

We want to invest in companies that can keep growing attractively.

First, we look at analyst’s expectations.

TransDigm:

Exp. Revenue Growth next two years (CAGR): 10.5% (Revenue growth > 5%? ✅)

Exp. EPS Growth next two years (CAGR): 14.6% (EPS growth > 7%? ✅)

EPS Long-Term Growth Estimate: 12.4% (EPS growth > 7%? ✅)

Let’s also look at TransDigm’s own outlook for 2026:

13. Does the company trade at a fair valuation level?

We always use 3 methods to look at the valuation of a company:

A comparison of the forward PE multiple with its historical average

Earnings Growth Model

Reverse Discounted-Cash Flow

Forward PE

The first thing we do is compare the current forward PE with its historical average over the past 10 years.

This is a shortsighted method, but it already gives a quick indication.

Think about it as checking the temperature of the water with your feet before diving into it.

The graph looks as follows:

Earnings Growth Model

This model shows you the yearly return you can expect as an investor.

In theory, it’s easy to calculate your expected return:

Expected return = EPS growth + Dividend Yield +/- Multiple Expansion (Contraction)

Here are the assumptions I use:

EPS Growth = 12.5% per year over the next 10 years

Dividend Yield = 2.5%

TransDigm’s Dividend Yield is currently above 6%. However, this is related to a Special Dividend (=not sustainable)

We use 2.5% as a more conservative estimate

Forward PE to decline from 28.2x to 26.0x over the next 10 years

Expected yearly return = 12.5% + 2.5% - 0.1* ((20.0x-28.2x)/28.2x)= 12.1%

A 12.1% return looks attractive.

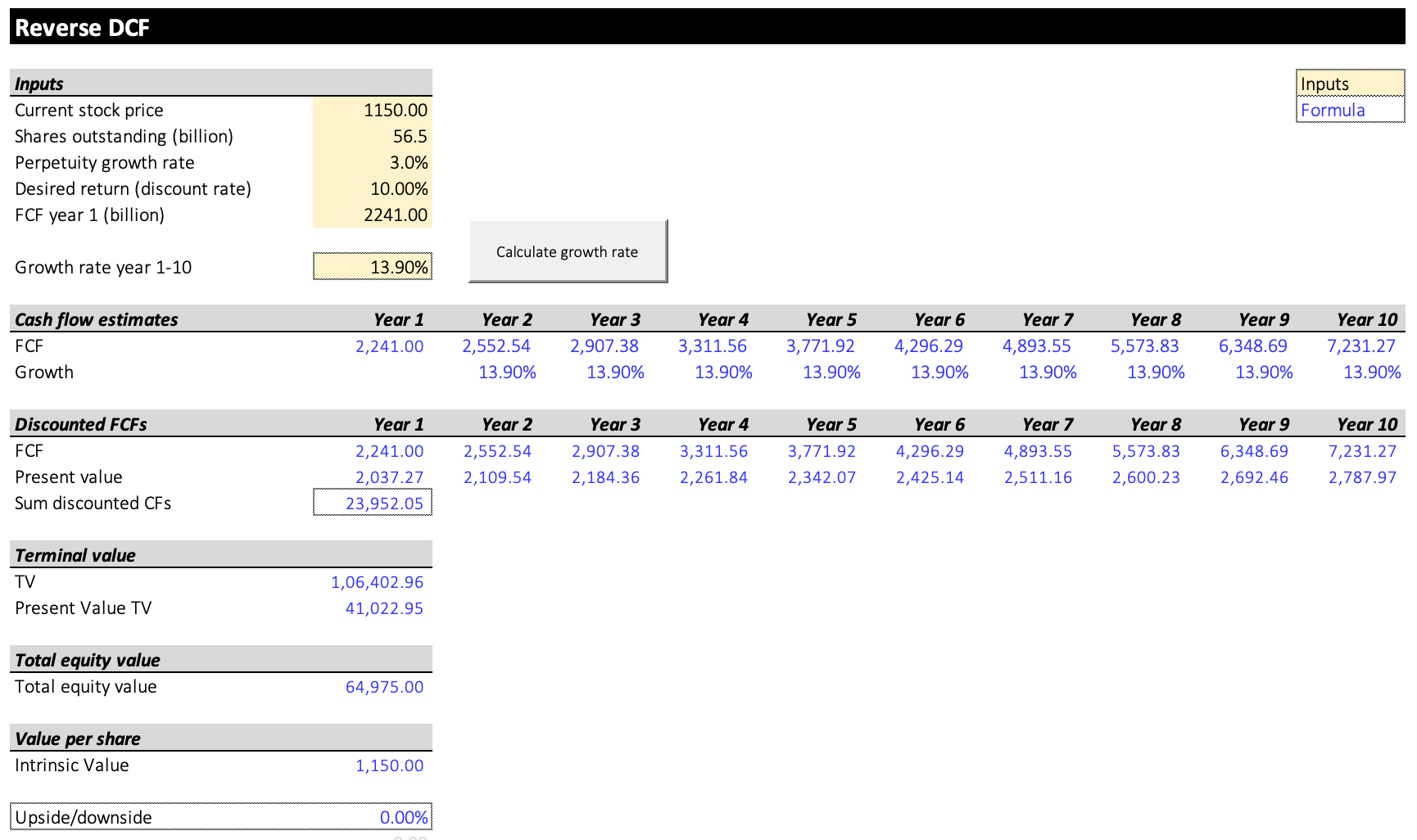

Reverse DCF

Charlie Munger once said that if you want to find a solution to a complex problem, you should invert. Always invert. Turn the problem upside down.

This is exactly what a reverse DCF does. As an investor, we don’t make assumptions.

We look at what assumptions the market has made and see whether they are reasonable.

TransDigm aims to reach $2.4 billion in Free Cash Flow.

We subtract Stock-Based Compensation ($159 million) and add Growth CAPEX ($0 million) to arrive at FCF in year 1 of $2.241 billion.

The reverse DCF indicates that TransDigm’s FCF should grow by 13.9% each year for the next ten years.

This could be possible, but there is no large margin of safety.

TransDigm:

Forward PE: 28.2x (lower than its 5-year average? < 34.9x? ✅)

Earnings Growth Model: 12.1% (Yearly return? > 10%? ✅)

FCF-Growth Reverse DCF: 13.9% (Realistic growth expectations? ❓)

The conclusion here? TransDigm is a wonderful company at a fair price.

But TransDigm is also one of these companies that has always been expensive but kept generating shareholder value.

The high historical Forward PE proves this.

14. How did the Owner’s Earnings of the company evolve in the past?

Over time, stock prices tend to follow a company’s Owner’s Earnings (EPS Growth + Dividend Yield).

That’s why we want to invest in companies that managed to grow their Owner’s Earnings at attractive rates in the past.

TransDigm:

CAGR Owner’s Earnings (5 years): 50.7% (CAGR Owner’s Earnings > 12%? ✅)

CAGR Owner’s Earnings (10 years): 29.1% (CAGR Owner’s Earnings > 12%? ✅)

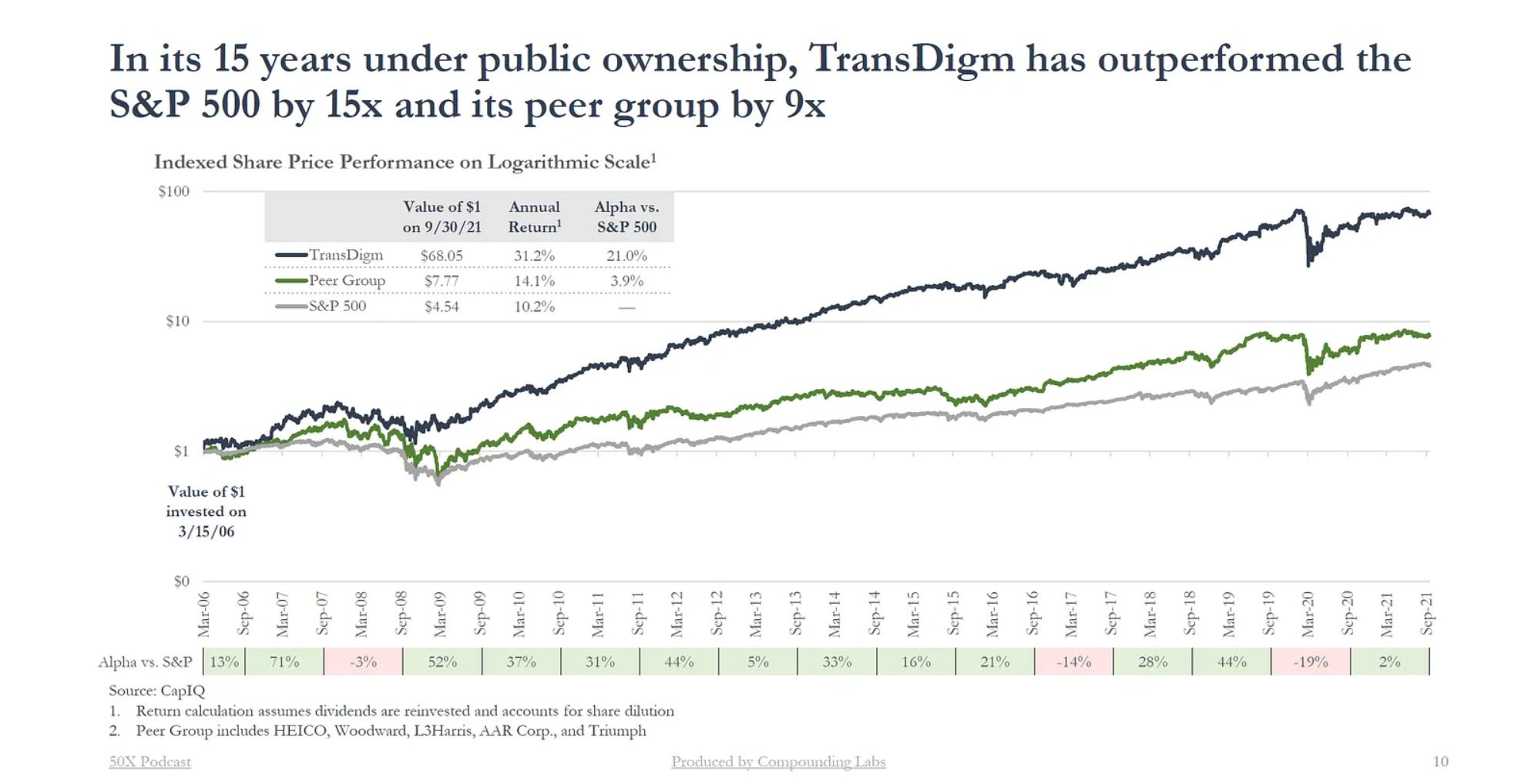

15. Did the company create a lot of shareholder value in the past?

We want to invest in companies that have managed to compound at attractive rates in the past.

Ideally, the company returned more than 12% per year to shareholders since its IPO.

TransDigm:

YTD: -14.9%

5-year CAGR: +18.5%

CAGR since IPO 2006: +27.6% (CAGR since IPO > 12%? ✅)

Looking back to before the IPO makes the story even more impressive.

TransDigm was founded in 1993 with just $25 million of Equity. Over the next 34 years, it compounded at 26.4% per year.

This makes TransDigm a 3,000-bagger (excluding Dividends).

Since 2017, TransDigm has paid out more than $15 billion in (Special) Dividends.

These Special Dividends alone are already a 600x on the initial Equity Investment.

Speaking about compounding.

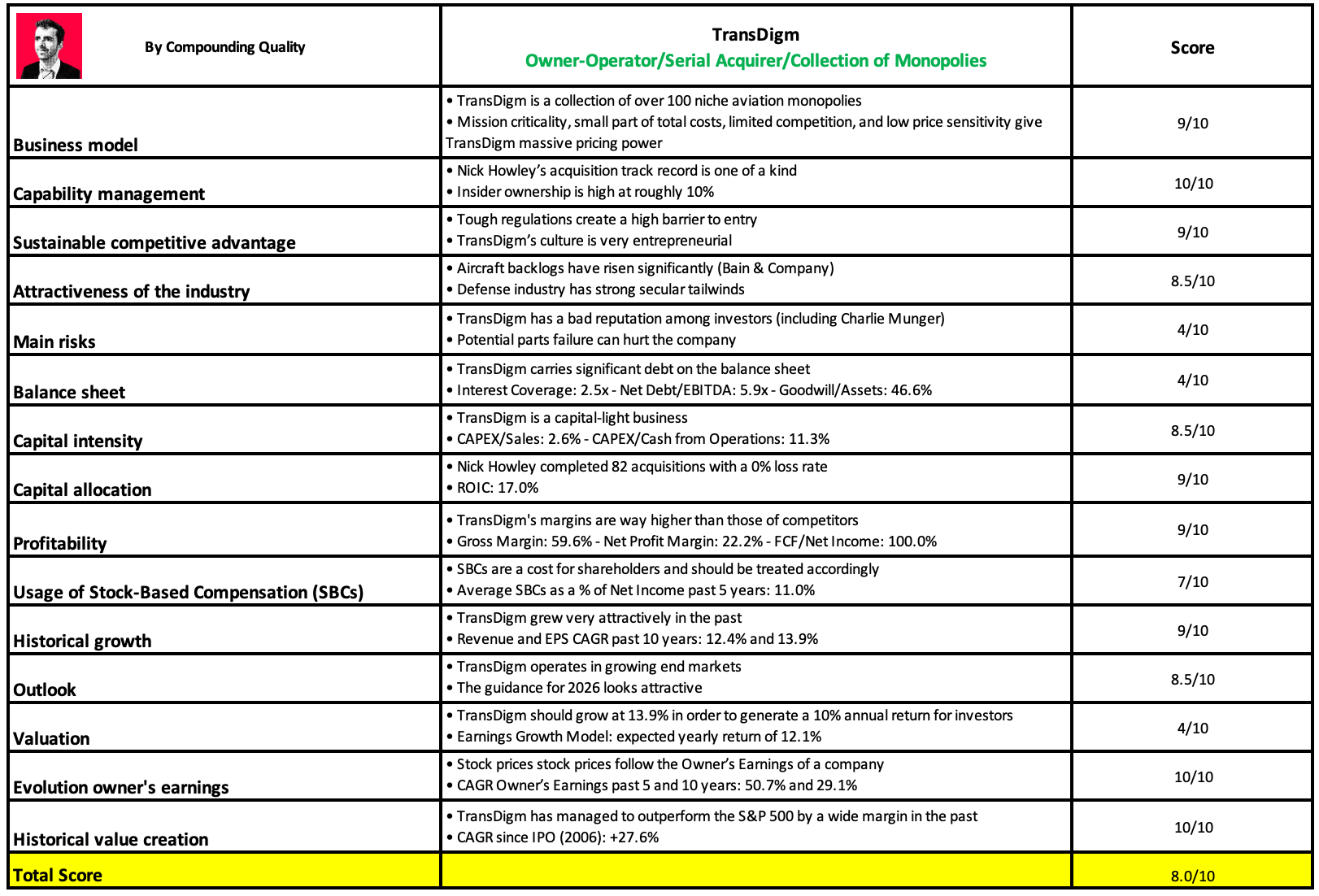

Quality Score

Finally, let’s bring everything together and give TransDigm a Total Quality Score.

As you can see in the table below, TransDigm gets a Total Quality Score of 8.0/10:

TransDigm is a phenomenal business.

Nevertheless, we are not buying for three reasons:

Large size: It’s becoming harder to reinvest all the cash flows into future growth

Heavy gearing: We prefer companies with more conservative balance sheets

We also have question marks related to the large Special Dividend of 2025 that was financed with Debt

Rich valuation levels: TransDigm isn’t cheap

We would start to become interested at a FWD PE of 25x times earnings.

This means we would become interested at a stock price of $1,010. (12.5% below today’s stock price).

Whenever you’re ready

That’s it for today.

Compounding Quality is all about securing your financial future.

Whenever you’re ready, here’s how I can help you:

📈 Access to my Portfolio with 100% transparency

📚 Access to my ETF Portfolio

🔎 Full investment cases about interesting companies

📊 Access to the Community

✍️ And much more!

Everything in life compounds

Pieter (Compounding Quality)

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Finchat: Financial data