👑 What you need to know about Return On Invested Capital

A high ROIC is key

For quality investors, the Return On Invested Capital (ROIC) is one of the most important financial metrics.

A high ROIC is key for value creation and it’s a great way to look at a company’s competitive advantage.

In this article we’ll teach you everything you need to know about one of the most important metrics in the world of finance.

The power of compounding

Let’s start with an example. Suppose that there are 2 companies:

Company A: ROIC of 5% and reinvests all its profits for 25 years

Company B: ROIC of 20% and reinvests all its profits for 25 years

Can you guess how much company A and B would be worth if you invest $10.000 in both (assumption: valuation remains constant)?

In this example, an investment in company A would be worth $33.860 while an investment in company B would increase to $953.960!

This simple example beautifully shows the importance of ROIC and the power of compounding.

Now you’re convinced of the importance of ROIC, let’s explain this financial metric to you.

What is Return On Invested Capital (ROIC)?

Capital allocation is the most important task of management.

If you want to look at how efficient management allocates capital, you can take a look at the ROIC.

Return On Invested Capital (ROIC) = (NOPAT / Invested Capital)

NOPAT = Net Operating Profit After Tax

Invested Capital = Total assets - non-interest-bearing current liabilities

When a company has a ROIC of 15%, it means that for every $100 in capital the company has on its balance sheet, $15 in NOPAT is generated.

You want to invest in companies with a high ROIC as this means that the company is allocating capital efficiently.

As a rule of thumb, the ROIC should be higher than 10% and preferably higher than 15%.

Why ROIC matters

Did you like the first example in this article? Let’s use a second one.

In this example, we have 2 companies: Quality Inc. and Dividend Inc.

Both companies generate a NOPAT (profit) of $100 million per year and need $500 million to operate (invested capital). Furthermore, both companies have a ROIC of 20%.

Dividend Inc. has no growth opportunities and distributes all earnings as a dividend to shareholders. As a result, Dividend Inc. will distribute $100 million to shareholders each year and will still make $100 million in profits 20 years from now.

On the other hand, Quality Inc. is active in a secular growth market and is able to reinvest all its earnings in organic growth. This means Quality Inc. pays no dividend to shareholders and reinvests everything in itself.

After 1 year, Quality Inc. has $600 million in capital (the starting capital of $500 million + $100 million in reinvestment). On this invested capital of $600 million, Quality Inc. generates a ROIC of 20%. As a result, Quality Inc.’s earnings grew to $120 million (20% * $600 million).

NOPAT = ROIC * Invested Capital

In year 2, Quality Inc. again reinvests it’s earnings of $120 million in organic growth. As a result, Quality Inc.’s invested capital grew to $720 million (the $600 million it already had + $120 million in reinvestment). The earnings of Quality Inc. grew to $144 million (20% * $720 million).

Can you guess how many profit Quality Inc. would make if they would be able to this for 20 consecutive years?

The correct answer is $3.8 billion!

As a result, a high ROIC in combination with plenty of growth opportunities is the golden egg for investors. It will result in exponentially increasing earnings for a company if management makes good capital allocation decisions.

"Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return—even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you'll end up with a fine result." - Charlie Munger

Growth only creates value when ROIC > WACC

It is very important to understand that growth only creates value when the Return On Invested Capital (ROIC) of a company is higher than the Weighted Average Cost of Capital (WACC).

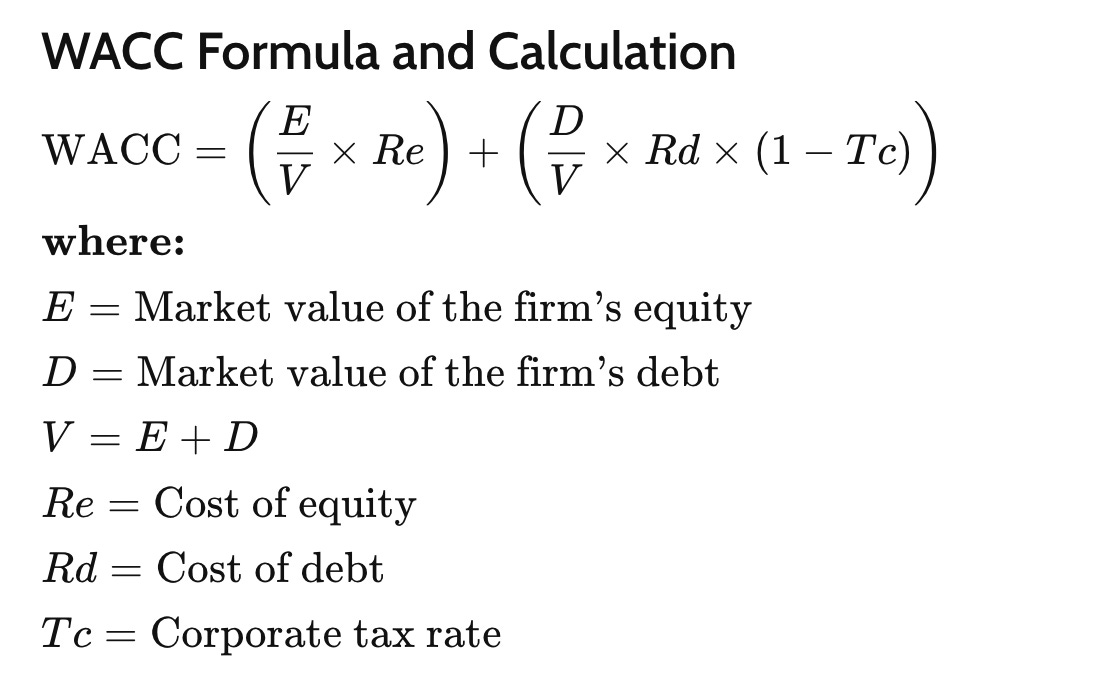

The formula to calculate the WACC of a company can be seen hereunder. Simply put, the Weighted Average Cost of Capital is equal to the firm’s average cost of capital (cost of equity + cost of debt).

Source: Investopedia

It is very intuitive to state that what the company earns on its investments (ROIC) should be higher than what the company needs to pay to finance these investments (WACC).

Let’s give another example to clarify this:

Company A has a ROIC of 5% and a WACC of 10%. The company’s NOPAT is equal to $10 million and they are offered a new project which would generate $1 million in NOPAT.

When company A would accept this project, they will need $20 million in capital to execute this project ($1 million / 5%).

ROIC = NOPAT / Invested Capital

Invested Capital = NOPAT/ROIC

Company A has a WACC of 10% and as a result they will need to pay $2 million ($20 million *10%) to finance this project.

Cost of capital = Capital needed * WACC

As a result, company A should pay $2 million to finance the project while it will only generate $1 million in NOPAT. It goes without saying that company A shouldn’t accept this project because they would lose money on it.

On the other hand, Company B has a ROIC of 20% and a WACC of 10%. The company’s NOPAT is also equal to $10 million and they are offered the identical project as company A which would generate $1 million in NOPAT.

When company B would accept this project, they will need $5 million in capital to execute this project ($1 million / 20%).

Company B has a WACC of 10% and as a result they will need to pay $0.5 million ($5 million *10%) to shareholders and debtors to finance the project.

So company B should pay $0.5 million to finance the project while it would generate $1 million in extra NOPAT. As a result, company B should accept this project.

Excluding goodwill and cash

Some people prefer to exclude goodwill and cash out of the invested capital to calculate the ROIC.

In that case, the formula for ROIC goes as follows:

ROIC = NOPAT / (Invested capital - goodwill - cash and cash equivalents)

When you use this variant of the formula, the ROIC will be higher than in the traditional formula.

This variant is especially relevant to calculate how much a company should reinvest in itself in order to grow at a certain rate.

The underlying reasoning behind this is that you don’t need goodwill or cash in order to grow.

Reinvestment needs

When you want to calculate how much a company should reinvest in itself in order to achieve a certain rate, you can use this formula:

Reinvestment need = (desired growth / ROIC)

Let’s say that a company has a ROIC of 20% and wants to grow its NOPAT with 10% per year.

In that case, the company should reinvest 50% of its NOPAT (10%/20%) in order to grow with 10% next year.

It goes without saying that having a high ROIC is interesting because it results in lower reinvestment needs for the company. The best companies in the world are able to grow attractively (> 10% per year) while reinvestment needs are very low to achieve this growth.

When a company needs to reinvest less, they can use their cash flow for other things like dividends and buying back shares.

ROIC = proxy for a moat

You aren’t convinced yet that the ROIC of a company is important? Well, you can use it to measure a company’s competitive advantage too.

In general, there are 2 crucial conditions for a company to have a moat:

The company is earning profits that are greater than their weighted average cost of capital (WACC)

The level of profitability has maintained high and constant for a reasonable period of time

A consistent and high ROIC is a great indication that the company has a sustainable competitive advantage. By only focusing on companies with a high ROIC when picking stocks, you already exclude a lot of value traps.

A high and consistent ROIC is the result of a sustainable competitive advantage.

Why? Because it indicates that competitors and (potential) new entrants are not able to go into competition with this company. This allows them to stay very profitable and operate at attractive margins.

Conclusion

The ROIC is one of the most important financial metrics for quality investors as it indicates how efficiently management is allocating capital.

You want to invest in companies with a high and consistent ROIC. When a company has a robust ROIC which is higher than their WACC every single year over the past decade, it is a great indication that the company has a competitive advantage.

As a quality investor, you are seeking for compounding machines. These stocks have a high and consistent ROIC with plenty of reinvestment opportunities. This will allow the company to grow its free cash flow exponentially.

Every single article we write right now is completely for free. If you liked this, can you please give this article a like and/or let us know in the comments? In 2023, we would love to engage more with our audience.

Further reading

Do you want to read more? Take a look at these articles:

More from us

Do you want to read more from us? Please subscribe to our Substack where we provide investors with investment insights on a weekly basis. You can also follow us on Twitter, Linkedin, and Instagram.

If you have any suggestions to further improve our posts, or do you want certain topics to be covered? Send us an email:

About the author

Compounding Quality is a professional investor which manages a worldwide equity fund with more than $150 million in Assets Under Management. We have read over 500 investment books and spend more than 50 hours per week researching stocks.

Great article. Thanks!

Couple examples of high ROIC companies?