Fantastic Fundamentals

Text SA: The Fundamentals

Text SA might have one of the healthiest Fundamentals I’ve ever seen.

💵 The company has more cash than debt

📈 A ROIC of more than 200% (!)

💸 Translating 50% of its revenue in pure cash

Let’s dive right in.

Does the company have a sound balance sheet?

Since 2014, Text SA has had a Net Cash Position every single year.

Today, the company’s Net Cash Position is equal to 135.4 million PLN ($34 million).

As the company’s Market Cap is equal to 3.1 billion PLN ($787 million), 4.3% of Text SA’s market cap is cash.

The company’s EBIT/Interest Expense is equal to 570x.

Text SA uses (almost) no debt to finance its operations. Debt/Equity is equal to 8.5%.

Almost 100% of Text SA’s equity consists of retained earnings. This indicates that the company has been very profitable in the past.

As Text SA doesn’t acquire other companies, the company doesn’t have any goodwill on its balance sheet. This is something I love to see.

Quality Score - Balance sheet: 8/10

Text SA has a healthy balance sheet.

The company has no goodwill and 4.3% of Text SA’s market cap is cash.

How much capital does the company need to operate?

The less capital a company needs, the better.

Text SA’s CAPEX/Sales is equal to 10.4%. Over the past 5 years, this number has averaged 8.5%.

The company increased its CAPEX recently because they are investing heavily in AI solutions.

The company’s CAPEX/Operational CF is equal to 16.8%. Over the past 5 years, this number averaged 16.5%.

These capital intensity numbers look quite high at first sight.

But now let’s look at the company’s CAPEX versus Depreciation:

As you can see, Text SA’s CAPEX is way higher than the company’s Depreciation.

As a rule of thumb, we state that Depreciation is equal to Maintenance CAPEX and that the difference between CAPEX and Depreciation is Growth CAPEX.

In this case, this would mean that 96.0% of Text SA’s CAPEX is growth CAPEX!

When you would only take the company’s maintenance CAPEX into account, the company’s CAPEX/Sales and CAPEX/Operating Cash Flow would be equal to 0.4% and 0.7%.

This is a different story!

Quality Score - Capital Intensity: 7/10

Almost all Text SA’s CAPEX is growth CAPEX. The company will invest heavily in AI solutions in the years to come.

CAPEX/Sales is equal to 10.4% while Maintenance CAPEX/Sales is equal to only 0.4%

Is the company a great capital allocator?

Capital allocation is the most important task of management.

First and foremost, it’s important to highlight that Text SA requires almost no capital to grow.

You can already see this by looking at the company’s ROIC.

Text SA’s ROIC is equal to 228% (!).

A ROIC of 228% means that per dollar you invest in the company, Text SA generates $2.28 in value for you per year.

Here’s an overview of Text SA’s capital allocation metrics:

The company’s capital allocation policy is to pay out as much as possible via dividends.

Currently, the Dividend Per Share (DPS) is equal to 6 PLN, implying a dividend yield of 5.3% at the current stock price.

“The dividend policy envisages allocating the highest possible part of profit for the dividend, unless no investments appear that would provide a higher return rate to shareholders.”

You could ask yourself why Text SA doesn’t invest more in organic growth.

The answer to this is that Text SA needs (almost) no capital to grow.

Quality Score - Capital Allocation: 8/10

Text SA has a phenomenal ROIC of 228%. This means that per dollar you invest in the company, Text SA generates $2.28 in value for you per year.

Most Free Cash Flow is distributed to shareholders via dividends.

How profitable is the company?

The higher the profitability, the better.

The good news? Text SA is very profitable.

Text SA has a FCF margin of 48.7%.

This means that for every $100 in sales, the company generates $48.7 in pure cash.

That’s phenomenal!

Quality Score - Profitability: 9/10

Seldomly do you see a company so profitable as Text SA.

For every $100 in sales, Text SA generates almost $50 in pure cash.

Does the company use a lot of Stock-Based Compensation?

Text SA doesn’t issue shares to reward directors or employees. This is great as stock-based compensation is a cost for shareholders.

A company that doesn’t pay any SBCs at all is quite unusual in today’s world.

Quality Score - Stock-Based Compensation: 10/10

Text SA doesn’t use Stock-Based Compensation to reward management or employees.

Did the company manage to grow attractively in the past?

The best metric to look at Text SA’s results? Its Monthly Recurring Revenue.

Here’s the evolution of the company’s MRR:

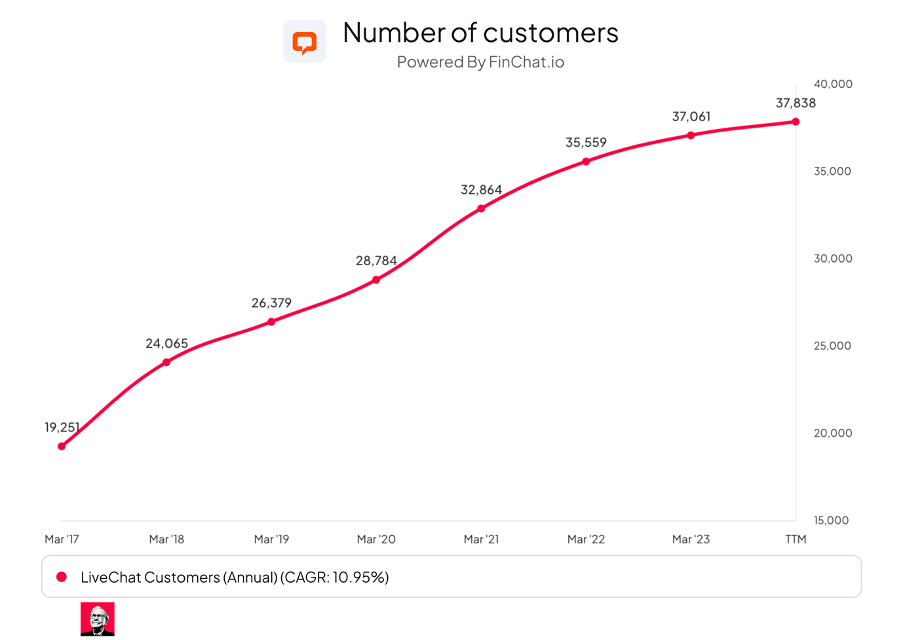

Evolution number of customers:

Since 2017, the company’s customers have grown at a CAGR of almost 11%.

However, you see that growth is slowing down (the company’s growth was ‘only’ 4.2% last year).

The customer base for the primary service, "Livechat," has experienced consistent growth in the preceding years. However, this growth has recently decelerated substantially to approximately 1.5% quarter over quarter.

It’s also important to talk a bit about customer churn here.

Text SA is a SaaS company meaning that their revenues are recurring in nature. When a client doesn’t renew his monthly or yearly subscription, this is called churn.

The monthly churn of Text SA averages 3%. This means that Text SA needs to attract at least 3% of its total customers as new customers every month to keep with the same number of clients. A churn rate of 3% is quite normal for SaaS companies.

Historical growth rates:

These growth figures look very attractive.

Quality Score - Historical Growth: 9.5/10

Text SA has been a strong grower in the past.

Since 2012, the company has grown its revenue from 5.5 million PLN to 315.8 million PLN.

Does the future look bright?

While the future still looks bright for Text SA, we can’t expect the strong historical growth rates (> 20% per year) to persist in the future.

A study of Verified Market Research estimates that the Live Chat Software Market will grow at a CAGR of 8.6% until 2030.

Here’s what the outlook looks like for Text SA:

The outlook above is at the lower end of what is acceptable to us.

Remember that the market for Live Chat Solutions should be able to grow by 8.6% per year until 2030. The above indicates that Text SA will grow slower than the market as a whole.

I think these estimates are too conservative and that Text SA should be able to grow by around 10% per year in the future.

Quality Score - Outlook: 7/10

The end market for Live Chat Solutions will continue to grow at attractive rates in the years to come.

The consensus states that Text SA should be able to grow its Free Cash Flow by 7.5% over the next 3 years.

Is the valuation of the company fair?

As a quality investor, you want to buy wonderful companies at a fair price.

We always look at 3 things when looking at the valuation:

A comparison of the company’s forward PE with the historical PE

Earnings Growth Model - your expected return as an investor is equal to:

Expected yearly return = Earnings Growth + Shareholder Yield +/- Multiple Expansion (Contraction)

Reverse DCF: At what percentage should the company grow its FCF over the next 10 years to generate a return of 10% per year for shareholders?

Here’s how things look like for Text SA:

Forward PE

Text SA trades at a forward PE of 13.9x versus a 5-year average of 22.6x.

This means that Text SA is undervalued by almost 40% compared to its historical average!

Earnings Growth Model

Expected yearly return = Earnings Growth + Shareholder Yield +/- Multiple Expansion (Contraction)

Assumptions:

Earnings Growth = 7% per year

Shareholder yield = 5.3% (dividend yield of 5.3% + 0% buyback yield)

Forward PE to increase from 13.9x to 17.0x over 10 years

Expected yearly return = 7% + 5.3% + (17.0 - 13.9)/13.9 = 14.5%.

An expected yearly return of 14.5% looks attractive.

Reverse DCF

Our Reverse DCF indicates that Text SA should grow its FCF by 7% per year to return 10% per year to shareholders.

This is lower than the expected end-market growth.

It indicates that the company is undervalued today.

Quality Score - Valuation: 9.5/10

Today, Text SA trades at a forward PE of 13.9%. That’s a 40% (!) discount compared to its average valuation of the past 5 years.

My Earnings Growth Model indicates an expected yearly return of 14.5% per year.

Owner’s Earnings

In the long term, stock prices will always follow the Owner’s Earnings of a company.

That’s why I don’t care too much about the stock price performance of a company.

Instead, let’s focus on the evolution of the owner’s earnings.

You can calculate the owner’s earnings yourself using a simple formula:

Owner’s earnings = EPS per share growth + dividend yield

When we do these calculations, you’ll see that Text SA managed to grow its owner’s earnings at very attractive rates on the past:

A company that managed to grow its Owner’s Earnings (intrinsic value per share) by 23.8% per year over the past 5 years looks very attractive.

Quality Score - Owner’s Earnings: 9.5/10

Text SA managed to grow its Owner’s Earnings at very attractive rates in the past.

CAGR over the past 3 and 5 years: 27.8% and 23.8%.

Value creation

As quality investors, we don’t want to invest in The Next Big Thing.

Instead, we want to invest in companies that have already won.

That’s exactly why we prefer to invest in companies with a very strong track record.

Here’s how Text SA performed in the past:

Since 2014, Text SA returned 768% to shareholders (CAGR: 25.1%) versus 203% (CAGR: 12.2%) for the S&P500:

Quality Score - Value Creation: 9.5/10

Since its IPO in 2014, Text SA compounded at 25.1% per year.

This means that Text SA returned 768% to shareholders (CAGR: 25.1%) versus 203% (CAGR: 12.2%) for the S&P500.

Investment case Text SA

That’s it for today.

Did you miss the first 2 parts of Text SA’s investment case? You can find them here: