Our Shopping List

Companies we might add

Hi Partner 👋

Last week, you got an extensive Portfolio Update.

In case you missed it:

For every company in the Portfolio, you found out about our conviction levels.

Investing is an intellectual game that never stops.

And it’s also a game of opportunity costs.

What do I mean by this?

If you are invested in a company where you believe the future expected return equals 8% per year…

… And you find another one with an expected return of 13% per year…

You should consider making the switch.

That’s exactly why we’ll dive in some companies we’re considering adding to the portfolio this week.

Ready. Set. Go!

Companies we’re considering adding

Let’s now go over a list of companies we’re considering for the Portfolio.

3i Group ($LON:III)

How does the company make money?

3i Group is a Private Equity company/holding. They make money by buying stakes in private companies, growing their value, and selling them for a profit.

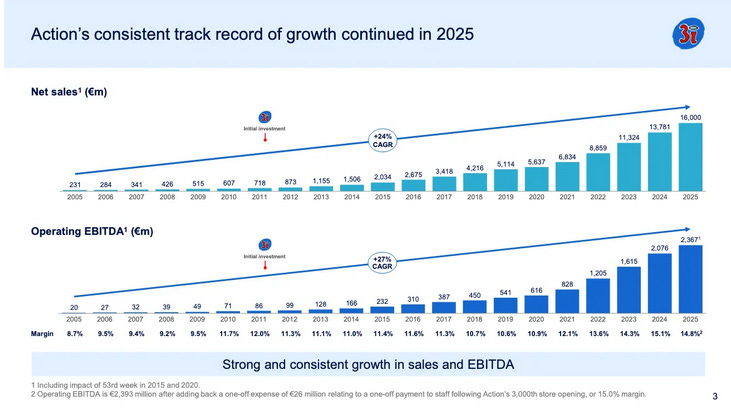

Their largest stake? Action.

Action is an European discount retailers that is growing at very attractive rates:

Why is it an interesting company?

Here’s why 3i Group is interesting in 5 bullet points:

Action exposure: ~90% of 3i’s private equity returns come from Action. Action is the fastest-growing non-food discount retailer in Europe (Revenue CAGR since 2011: 26%)

Exceptional unit economics: Action earns back the ~€500k it spends to open a store in less than a year. This helps them pay for new stores on its own, opening about one new store every day.

Massive runway left: Many places in Europe don’t have many Action stores yet, and some countries (like the UK and Scandinavia) don’t have any at all.

Wide moat: Because Action is so big, it can sell things cheaper than others. People tell their friends about the low prices, so it grows without spending money on ads. This creates a simple cycle where being bigger helps it stay cheap and to keep growing.

Strong management alignment: CEO Simon Borrows owns over £585 million in 3i shares (865× his base salary), keeping incentives firmly aligned with shareholders.

At which price are we interested?

At the end of 2025, the NAV (intrinsic value) of 3i Group equaled 3,017 pence.

The current stock price equals 2,859 pence.

This means the company now trades at a small discount.

Buying 3i Group at a discount compared to its NAV is never a bad idea if you ask me.

Adyen ($ADYEN)

How does the company make money?

Adyen processes payments between merchants, card networks, and banks through a single unified platform, taking a small percentage or fee on every transaction.

Its edge is cutting out intermediaries, offering a one-stop solution globally, which attracts large enterprise clients and drives high-margin volume growth.

As you can see in this chart, Adyen simplifies the electronic payments value chain:

| Seeking Alpha")

Why is it an interesting company?

Here’s why Adyen is interesting in 5 bullet points:

Boring management in the best way: Management doesn’t focus on M&A. The company grows organically and stays focused.

Economies of scale: Every payment teaches Adyen to catch fraud and approve more transactions. More customers → better data → better results → even more customers.

Technological advantage: Rivals are combining old technology together. Adyen built everything clean from day one on one platform.

Way more than just payments: Started as a payment processor, now quietly running companies’ entire financial back office.

Online + in-store in just one system: Big retailers hate juggling separate systems. Adyen handles both, so customers naturally spend more over time.

At which price are we interested?

Adyen now trades at its cheapest valuation level ever (a FWD PE of 25.3x).

At a PE of 20.0x, the company could be a no-brainer.

This means we’re willing to pay €765 for Adyen (current stock price: €970).

Alphabet ($GOOG)

How does the company make money?

Alphabet dominates digital advertising through Google Search and YouTube.

Advertisers bid for placement in an auction model.

Beyond ads, it earns from Google Cloud, the Play Store, and hardware, though advertising remains roughly 75% of revenue.

Why is it an interesting company?

Dominant core business (Search + Ads): Alphabet’s revenue engine is still built around search advertising, where it effectively forms a duopoly with Meta Platforms in digital ads.

Wide economic moat: Its leadership is reinforced by deep structural advantages, strong network effects, a globally trusted brand, unmatched data scale, and meaningful switching costs.

Self-reinforcing ecosystem: More users generate more data, which improves ad targeting and search quality, which in turn attracts more users and advertisers.

Strong capital allocation: Alphabet is a cash flow machine.

Multiple growth engines: Think about AI, YouTube, and “other bets”. They are diversifying beyond search.

At which price are we interested?

Alphabet is an amazing company, but it also did really well recently.

The stock is up +123% in the past year.

As a result, the valuation looks rather expensive. Alphabet now trades at a Forward PE of 28.9x.

I would love to buy Alphabet at a Fwd PE of 18x.

This would mean at a stock price of $210 (current stock price: $336.0)

ASML ($ASML)

How does the company make money?

ASML has a monopoly in producing chip machines (EUV lithography machines).

They are essential for producing the world’s most advanced chips.

Every major chipmaker in the world, from TSMC to Intel, buys its machines from ASML.

Why is it an interesting company?

The only company that makes the machines that make chips: No ASML means no iPhones, no AI, no nothing. They have 90% market share and literally zero real competitors.

Impossible to copy, even for entire countries: One of their machines weighs as much as two blue whales and takes decades of knowledge to build. China has been trying to replicate it for years. They’re nowhere close.

Once you’re a customer, you’re a customer forever: Chip factories can’t just switch suppliers. It would cost billions. So ASML collects service fees for 20–30 years after every single sale.

AI is a money printer for them: More AI → more chips needed → more factories built → more ASML machines ordered. Every dollar spent on AI eventually flows back to ASML.

They bet big and won bigger: ASML spent over a decade losing money on a technology nobody was sure would work. It worked and ASML is now reaping the benefits from this.

At which price are we interested?

ASML is an amazing company. They currently trade at a Forward PE of 36.8x.

This is rather expensive from a historical point of view. The average Forward PE of the past 10 years equals 32.0x.

Personally, I’d consider owning ASML at 25x earnings.

This means we would become interested at a stock price of €745 (current stock price: €1.245).

Now let’s dive into the three final companies.