🥂 Compounding Quality: Lessons Learned

Year In Review Part 1

Hi Partner 👋

I’m Pieter and welcome to a 📈 free edition 📈 of Compounding Quality.

In case you missed it:

If you haven’t yet, subscribe to get access to these posts, and every post.

Today, it’s exactly 1 year ago that I quit my job.

What a year it has been since then:

The newsletter grew from 93,000 subscribers to 295,000 subscribers

Compounding Quality has thousands of loyal Partners

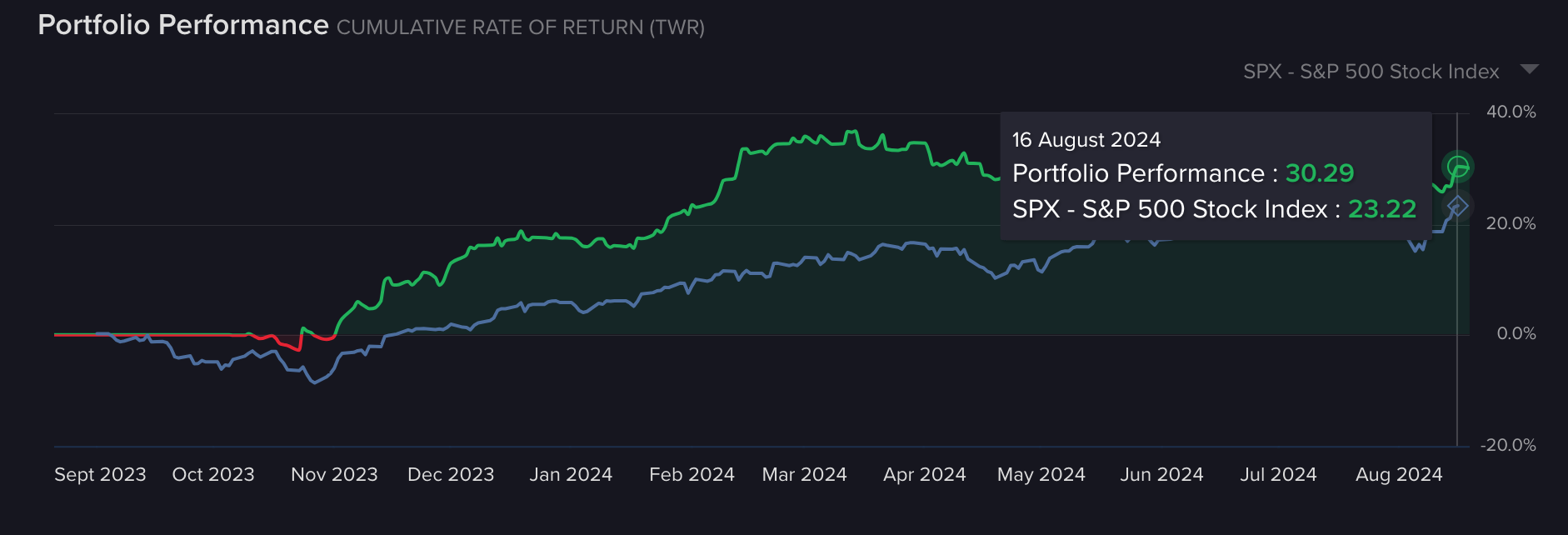

The Portfolio returned 30.3%

You allowed me to turn my hobby into a profession and I’ll forever be grateful for that. ❤️

Let’s put the year in review and share some key lessons.

The screenshot above is the official track record from Interactive Brokers.

I use Interactive Brokers for every transaction. You can explore Interactive Brokers here.

Partnership

Every Paid Subscriber of Compounding Quality is called a Partner.

Why? Because we’re in this together.

I try to genuinely do the right thing and to help you along your investment journey.

Honesty and integrity is a serious problem in the investment industry.

There are Fund Managers managing billions of dollars who don’t want to invest a single dollar in the Fund they manage.

Charlie Munger once said: Show me the incentive and I’ll show you the outcome.

It’s a rule I want to live by.

That’s why ALL my investable assets are invested in the Portfolio.

If you do well, I do well, and the other way around.

The best articles I wrote in the past year? The ones Partners asked to write about in the Community. The Wisdom of Crowds is amazing.

Why we invest

Do you know why we invest?

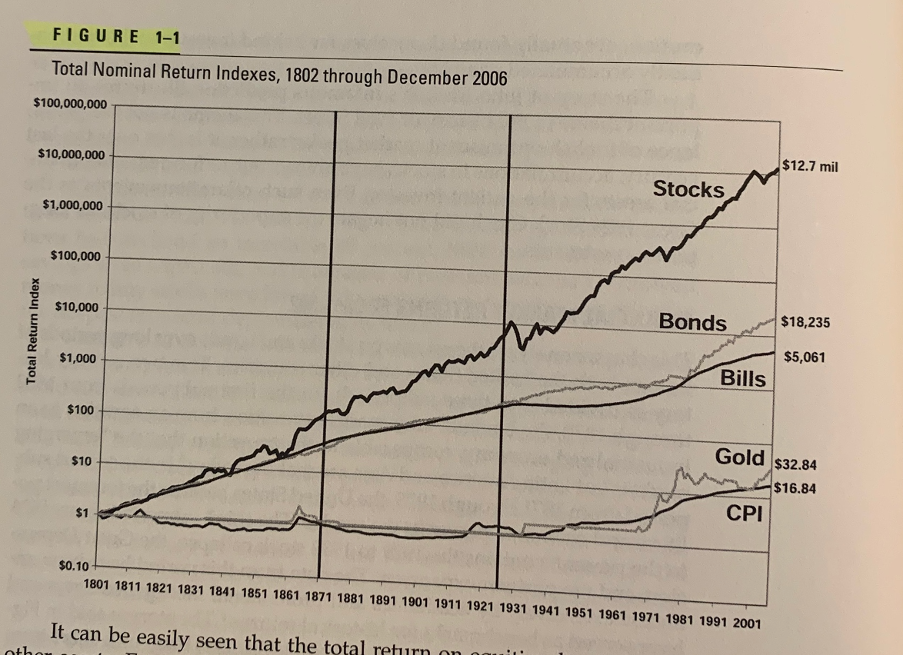

Investing is the best way to become wealthy as stocks always go up in the long term.

Here are the chances you’ll make money in the stock market:

https://t.co/wwMzytoFGe\" / X")

Since 1802, an investment of $1 in stocks turned into $12.7 million:

Source: Stocks For The Long Run - Jeremy Siegel

How we invest

The essence of the portfolio is very simple:

Buy wonderful companies

Led by outstanding managers

Trading at fair valuation levels

We want to invest in the best companies in the world.

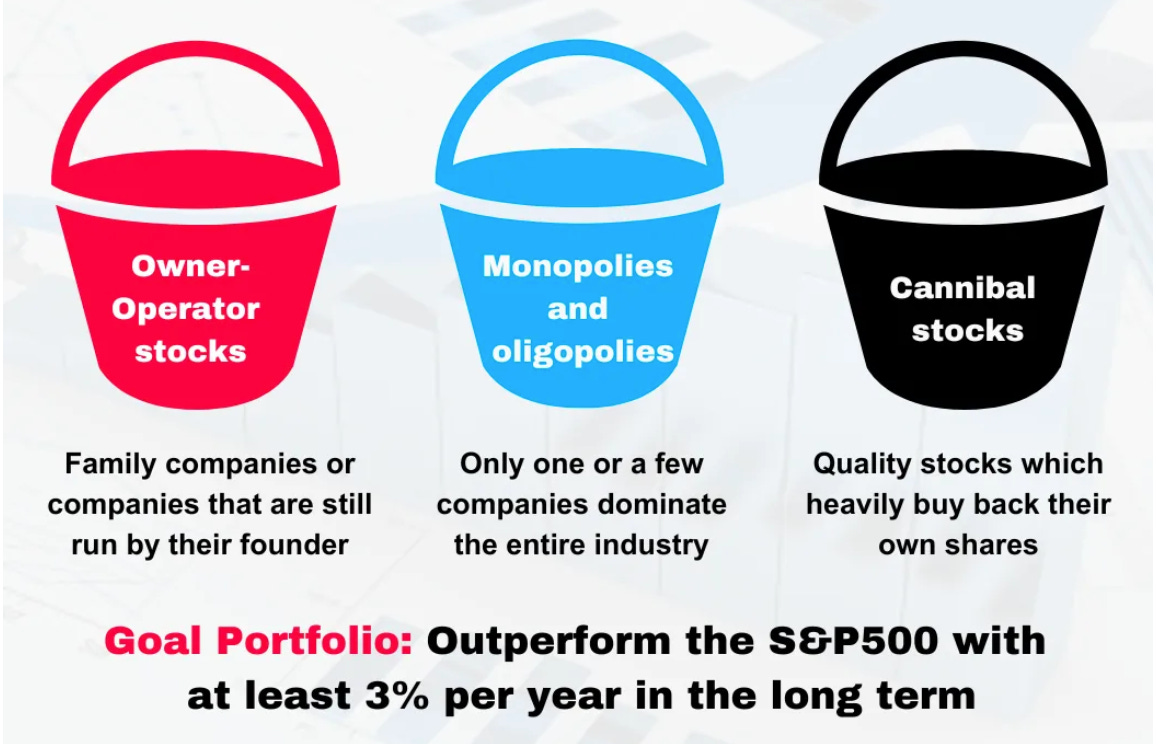

The portfolio will consist of 3 buckets, as you can see here:

Owner-Operator stocks:

Owner-Operator stocks are companies that are still run by their founder

Academic studies found that family companies and founder-led companies outperform the S&P500 by 3.7% per year and 3.9% per year respectively

“Some of our key managers are independently wealthy. They work because they love what they do and relish the thrill of outstanding performance. They unfailingly think like owners. They are the best kind of managers we can wish for.” - Warren Buffett

Monopolies and oligopolies

Only one or a few companies dominate the entire industry

Monopolies and oligopolies are usually great investments because they can operate at attractive conditions due to the lack of competition

“Over the years, Buffett followed his philosophy of buying into industries with little competition. If he can’t buy a monopoly, he’ll buy a duopoly. And if he can’t buy a duopoly, he’ll settle for an oligopoly.” - The Myth of Capitalism (Book)

Cannibal stocks

Quality stocks that heavily buy back their own shares

When outstanding shares decrease, your stake in the company increases

“Pay close attention to the cannibals.” - Charlie Munger

Portfolio Characteristics

✅ The portfolio will invest worldwide (developed countries only)

✅ We’ll own 15-20 stocks

✅ The portfolio aims to invest in the best companies in the world

✅ We won’t trade a lot. Activity and costs harm our results

✅ We won’t try to time the market (I’m way too dumb for that)

✅ The characteristics of companies in the portfolio:

Sustainable competitive advantage

Integer management with skin in the game

Healthy balance sheet

Low capital intensity

Good capital allocation

High profitability

Plenty of reinvestment opportunities

Trading at fair valuation levels

“It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” - Warren Buffett.

Portfolio goal

Let’s be honest with each other. We won’t outperform the market every single year.

There are only 2 kinds of people who can do this:

Cheaters

Liars

That’s why we’ll focus solely on the long term.

While Wall Street likes to think in quarters, we like thinking in quarter decades.

Here’s what Jeff Bezos has to say about this topic:

The goal of the portfolio?

Outperform the S&P500 by more than 3% in the long term (> 5 years).

It’s important to highlight that I will never aim for the highest return. I aim for consistency and doing above average for very long periods.

It’s great to see that Our Portfolio returned 30.3% versus 23.2% for the S&P 500:

But always remember…

Investing is a marathon, not a sprint.

“The goal is not to have the longest train, but to arrive at the station first using the least fuel.” - Tom Murphy

Flavor of the day

The flavor of the day is a specific investment theme that looks overvalued today.

For this year, it’s Nvidia.

170%. That’s how much Nvidia’s stock price has risen in 2024 so far.

Today, the company is worth $3.2 trillion.

In our Not So Deep Dive, we concluded that Nvidia should generate $350 billion (!) in Free Cash Flow 10 years from now to justify the current stock price. That’s as much as the Free Cash Flow of all Big Tech companies combined!

There is no question that Artificial Intelligence will change our lives but I’m not sure whether this justifies Nvidia’s current stock price.

Let’s see how the stock price evolves over the next 5 years.

Major Mistakes

In this section, I’ll highlight my 3 major investment mistakes in the recent past.

🥉 Not taking a full position in Brown & Brown

On the 26th of November, we bought Brown & Brown for 3% of the Portfolio.

I wrote the following:

Next Monday, we’ll buy Brown & Brown for 3% of the Portfolio at the opening.

Why only for 3%? Brown & Brown is a beautiful business trading near its all-time high. We hope to add to our position at somewhat more attractive valuation levels.

Since then, the stock is up 36.5%.

In hindsight, it was a mistake not to take a full position in this great company.

Great companies with plenty of reinvestment opportunities will always keep compounding at very attractive rates.

🥈 Buying Text SA

Warren Buffett said the first rule of investing is never to lose money. Rule number 2? Never forget rule number 1.

I did break this rule with Text SA.

When I announced buying the company, a lot of Partners were very skeptical of Text SA’s moat.

In hindsight, they were 100% right.

I have no idea what the business will look like in 10 years from now.

When you notice you’ve made a mistake, you should act as fast as possible.

Only 5 months after buying the company, I sold it with a loss of 20%.

When we bought Brown & Brown instead of Text SA, the difference in return would be more than 50%.

🥇 Not buying Constellation Software

During the COVID crisis in 2020, many great companies were trading at attractive valuation levels.

One of them was Constellation Software. I was seriously looking into buying the company.

Constellation Software is an excellent serial acquirer led by Owner-Operator Mark Leonard.

In March 2020, Constellation Software traded at a forward PE of 21.5x (currently 38.6x) and I knew it was an excellent business.

I decided not to buy Constellation (yet) because I thought the valuation was ‘still too expensive’.

Since March 2020, Constellation Software is up 260%.

Conclusion

Here’s what you need to remember from today’s article.

Since the start, our Portfolio returned 30.3% (7.1% better than the S&P 500)

We invest in 3 buckets:

Owner-Operator Stocks

Monopolies and Oligopolies

Cannibal Stocks

Flavor of the day: Nvidia. The valuation looks expensive

Major mistakes:

Brown & Brown: not buying a full position

Text SA: buying the company in the first place

Constellation Software: Not buying it in 2020

On Thursday, we’ll review the key happenings within our Portfolio over the past year.

Make sure you become a Partner and don’t miss out:

Book

Order your copy of The Art of Quality Investing here

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Finchat: Financial data