🛒 Our Shopping List (Part II)

The companies we want to buy

Hi Partner 👋

Over the past few weeks, we’ve been giving you an extensive Portfolio Update.

In case you missed it:

For every company in the Portfolio, you found out about our conviction levels.

And you’ve also found out about opportunity costs.

When you find a company with a higher expected return than one you’re currently invested in, you should consider making the switch.

Let’s dive into the companies we’re considering adding to the portfolio.

Our Shopping List: Part 2

Fairfax Financial Holdings ($FFH)

How does the company make money?

Faifax Financial Holdings is a holding company.

It’s a Canadian company operating a collection of global insurance and reinsurance businesses, collecting premiums upfront and investing the float before claims are paid.

The CEO Prem Watsa takes an opportunistic, value-oriented approach to investing the float, adding a second engine of returns alongside underwriting profit.

The goal of the company is to grow its book value by 15% per year on average in the long term.

In essence, Fairfax copied the business model of Berkshire Hathaway.

I’m currently reading the book The Fairfax Way. It’s a must read.

Why is it an interesting company?

The man who made $3 billion from a single bet: Prem Watsa, Fairfax’s CEO, called the 2008 financial crisis before almost anyone. He runs this company like his personal investment fund; with deep conviction and zero interest in short-term noise.

Two ways to make money at the same time: Fairfax earns on insurance premiums and on its investments simultaneously. When both engines fire together, the returns can be very powerful.

Growing in places most competitors ignore: Around 25% of Fairfax’s business comes from faster-growing markets outside North America (like India). That’s a growth lever most insurance peers simply don’t have.

A great business at a cheap price: Fairfax has compounded book value at 12% per year for over a decade. The stock trades at just 8x earnings. You’re not paying much for something that has consistently delivered.

The CEO hasn’t given himself a raise in 25 years: Watsa has kept his salary at CAD 600,000 since 2000. He’s not here for the paycheck. He owns the stock. His interests and yours are exactly the same.

At which price are we interested?

Fairfax is an amazing business.

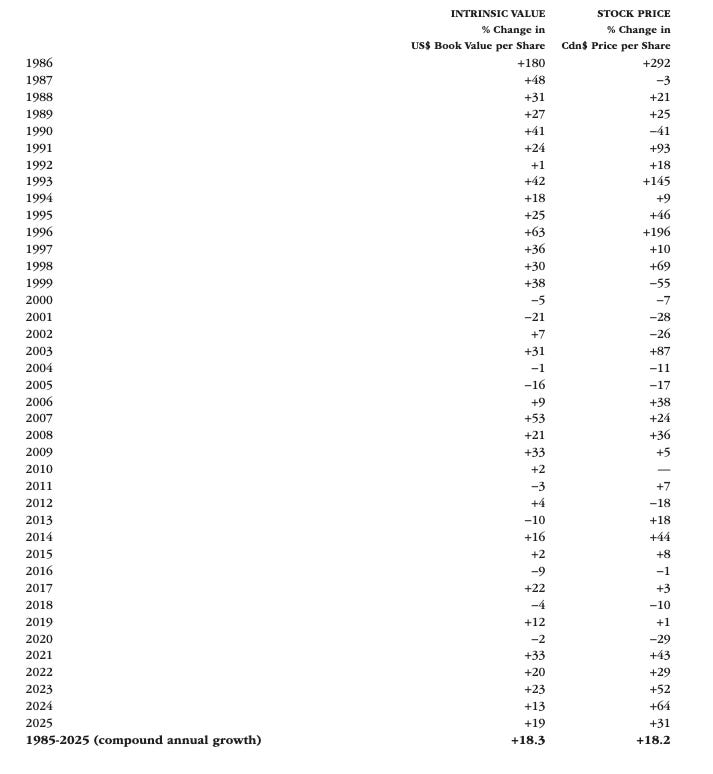

Just look at how the intrinsic value evolved over the years (the stock price followed):

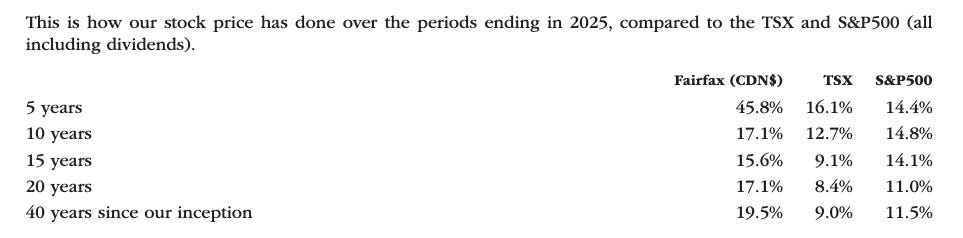

The company massively outperformed over the past 40 years:

In general, it’s quite hard to value Fairfax Holdings.

You should make an estimate of its intrinsic value.

I would be interested in owning Fairfax at 1.2x book value.

This implies a stock price of 1,777.5 CAD (current stock price: 2.472 CAD).

Fortinet ($FTNT)

How does the company make money?

Fortinet is a cybersecurity company.

They sell network security hardware (firewalls) as an entry point. Afterwards, they make high-margin recurring revenue through software subscriptions and support contracts.

Fortinet has a strong vertically integrated model. This gives them a clear cost and performance advantage.

Why is it an interesting company?

Cybersecurity spending only goes up: Hackers get smarter every year. Fines get bigger. Fortinet’s products stop being a nice-to-have and become a must-have.

Once you’re in, you don’t leave: Switching means retraining your team, ripping out systems, and leaving yourself wide open to attacks in the process. As a result customers stay.

The more customers they have, the better the product gets: Fortinet collects live threat data from 800,000+ customers. More data means faster detection. Faster detection attracts more customers. The flywheel keeps spinning.

Two new growth engines are just getting started: SASE and SecOps now make up 38% of billings and are growing by 40% per year. They are sold directly to existing customers at almost no extra cost.

The business gets more profitable every single year: More software, less hardware. Operating margins are expected to climb from 30% today to 36% by 2030. Same revenue base, more profit flowing through.

At which price are we interested?

Fortinet currently trades at a Forward PE of 29.2x.

Stock Based Compensation equals 15% of Fortinet’s Net Income.

If we adjust for this, the adjusted Forward PE equals 33.6x.

We would love to own Fortinet at 25x their adjusted Forward PE.

This implies a target price of $65.7 (current stock price: $85.1).

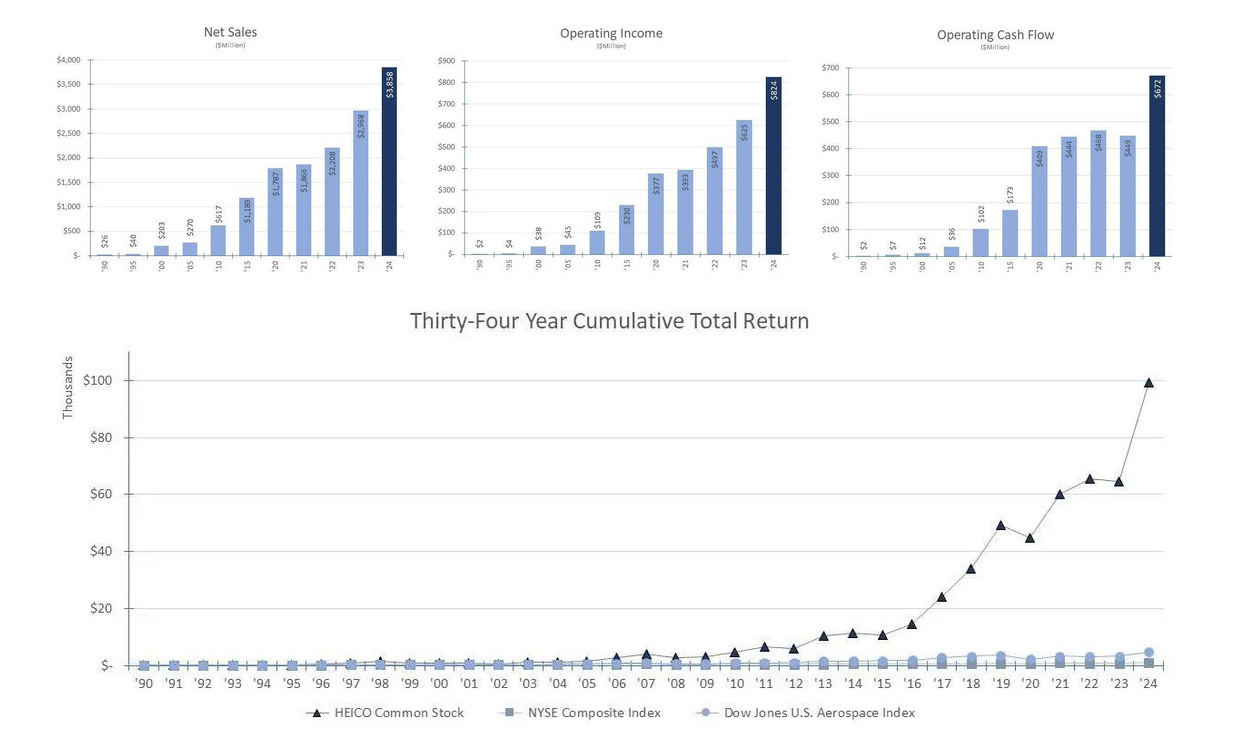

Heico ($HEI)

How does the company make money?

Heico produces FAA-approved aircraft replacement parts at meaningfully lower prices than original equipment manufacturers.

This saves airlines and MRO shops significant cost.

It also runs a repair and overhaul segment, and grows steadily through disciplined bolt-on acquisitions of niche aerospace businesses.

Why is it an interesting company?

They sell the exact same airplane parts for 30-40% less: Airlines have to maintain their planes no matter what. Heico reverse-engineers the exact same parts, gets approval, and undercuts the original manufacturers on price.

Getting in the industry is nearly impossible: Years of regulatory approvals, millions in R&D, hundreds of certified parts just to be a viable alternative. Heico already has all of that. New competitors start from zero.

Once Heico is in, nobody switches: Airlines can’t gamble on untested parts. Heico has a 30-year record of zero in-flight part failures. That track record is priceless and nearly impossible to replicate.

Defense is a whole second business: Heico’s components sit inside targeting systems, satellites, and missile guidance systems. When you’re that deeply embedded in critical defense hardware, nobody swaps you out for a cheaper option.

The numbers keep getting better: 14% revenue growth and 15% operating profit growth last quarter. Older planes are flying more than ever, and original manufacturers keep raising prices, which only makes Heico’s discount more attractive every year.

At which price are we interested?

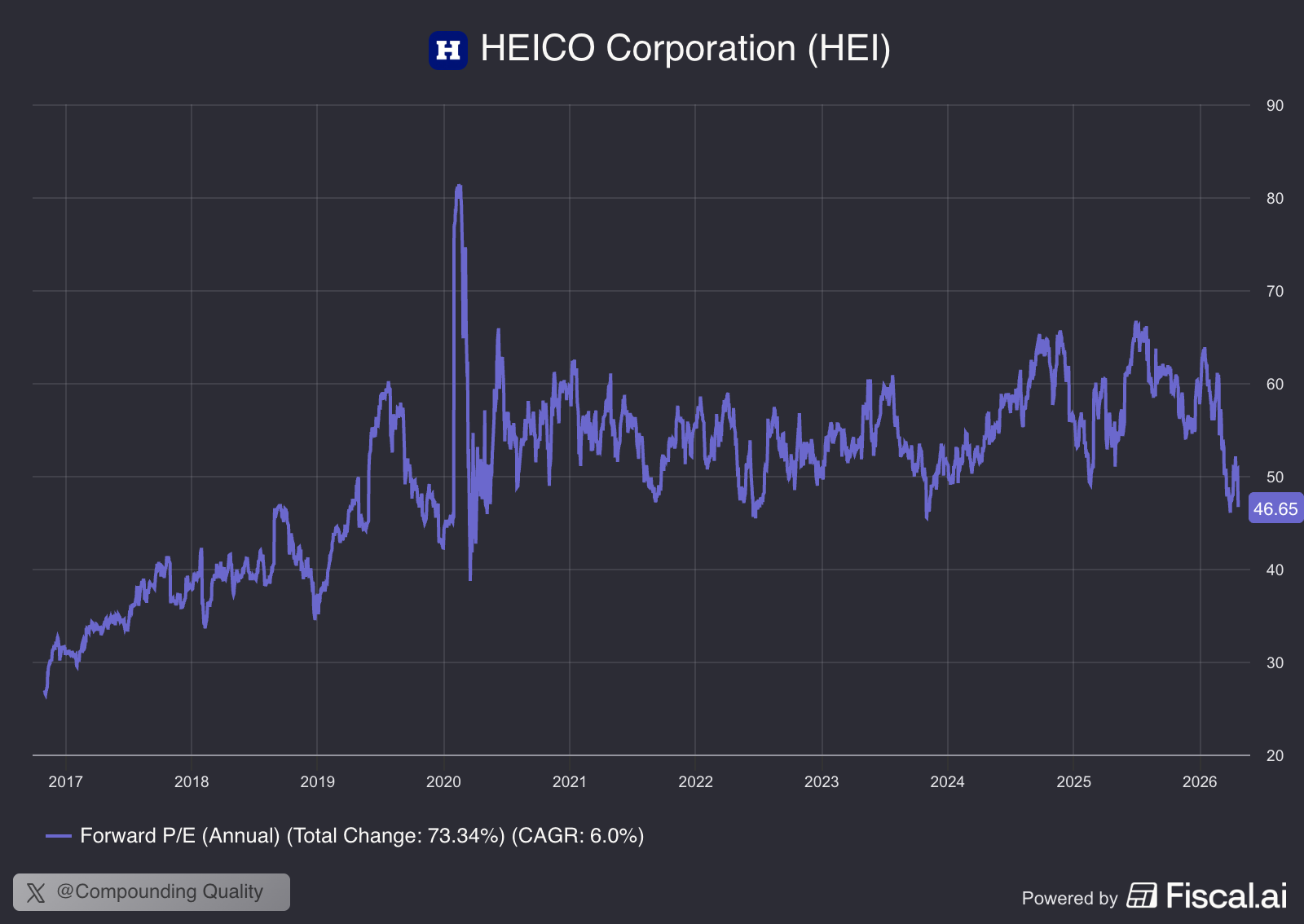

Heico is an amazing company that has always been expensive/

They currently trade at a Forward PE of 46.7x.

I would only be willing to pay 30x earnings for Heico.

This means we’re interested at a price of $178 (current stock price: $270).

Now let’s dive into the final 4 companies.