Our Shopping List: Part 3

Hi Partner 👋

Over the past few weeks, we’ve been giving you an extensive Portfolio Update.

In case you missed it:

Let’s dive in the final part of Our Shopping List today!

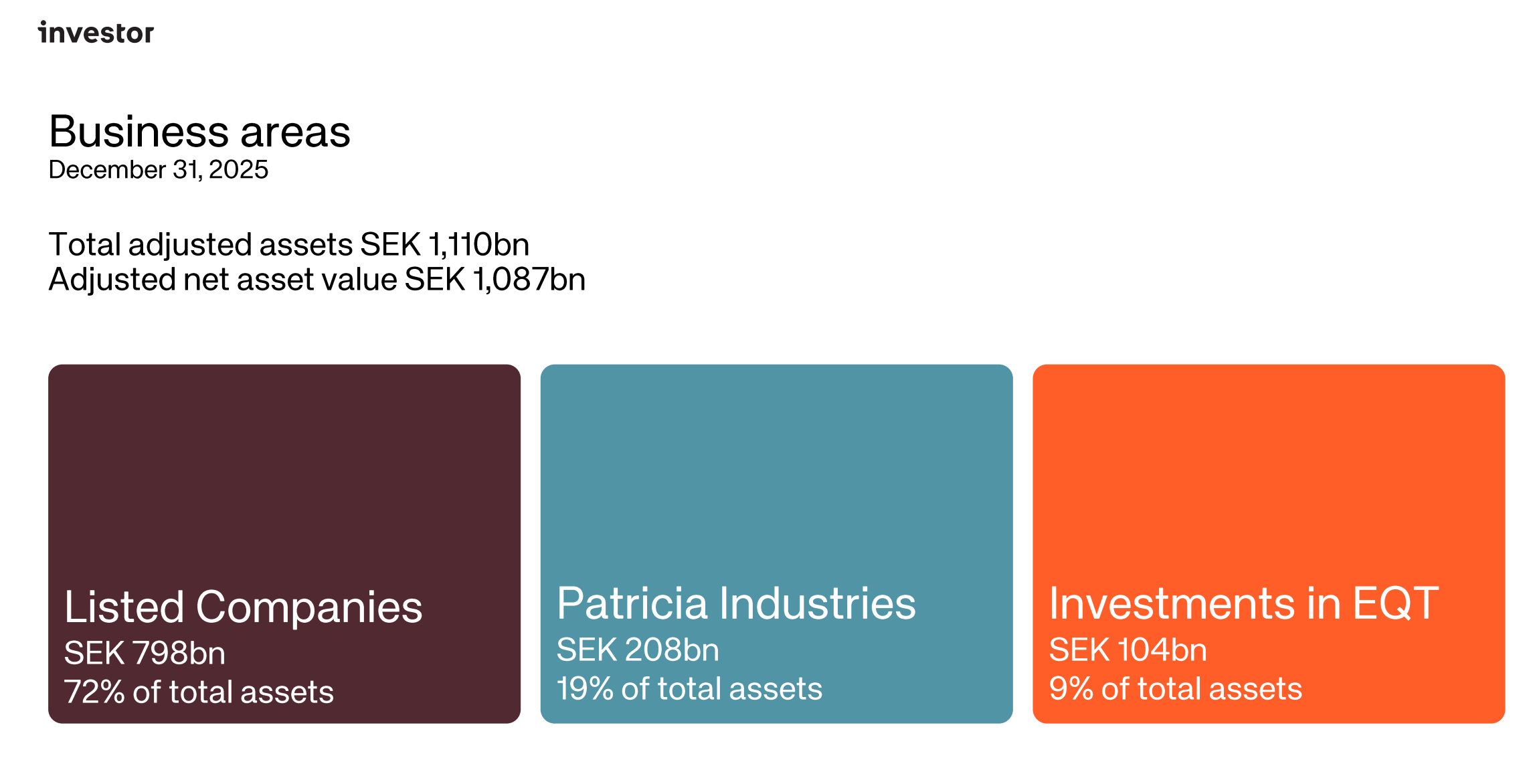

Investor AB ($INVE-B)

How does the company make money?

Investor AB is the Wallenberg family’s listed holding company.

That means it combines two interesting things:

A holding company, a type of asset that often trades at a discount to the assets it owns

A family owned business, meaning there’s a lot of skin in the game

Investor AB owns significant stakes in Sweden’s industrial champions like Atlas Copco, ABB, and AstraZeneca.

They focus on long-term ownership, active board engagement, and capital allocation across listed and unlisted assets, funded by dividends and occasional asset sales.

Why is it an interesting company?

The best of Europe in a single share: Buying Investor AB gives you exposure to a pre-built collection of world-class companies like AstraZeneca (medicine), Atlas Copco (industrial tools), and ABB (robotics). It is effectively a curated fund run by one of the most proven families in European business.

Wonderful companies at a fair price The stock trades near its intrinsic value

An amazing track record: Over the past decade, earnings have grown by nearly 25% per year. The stock has nearly doubled over the past five years. Plus, they pay a growing dividend that has never been cut.

Solid balance sheet: The company has very little debt. That means they aren’t just safe during a market crash, they actually have the cash to go shopping for more companies when prices are low.

The main risk is market exposure: Roughly 70% of the portfolio consists of publicly traded securities. When global markets sell off, Investor AB’s net asset value will decline with them. It’s a great long-term bet, but you should expect some volatility along the way.

At which price are we interested?

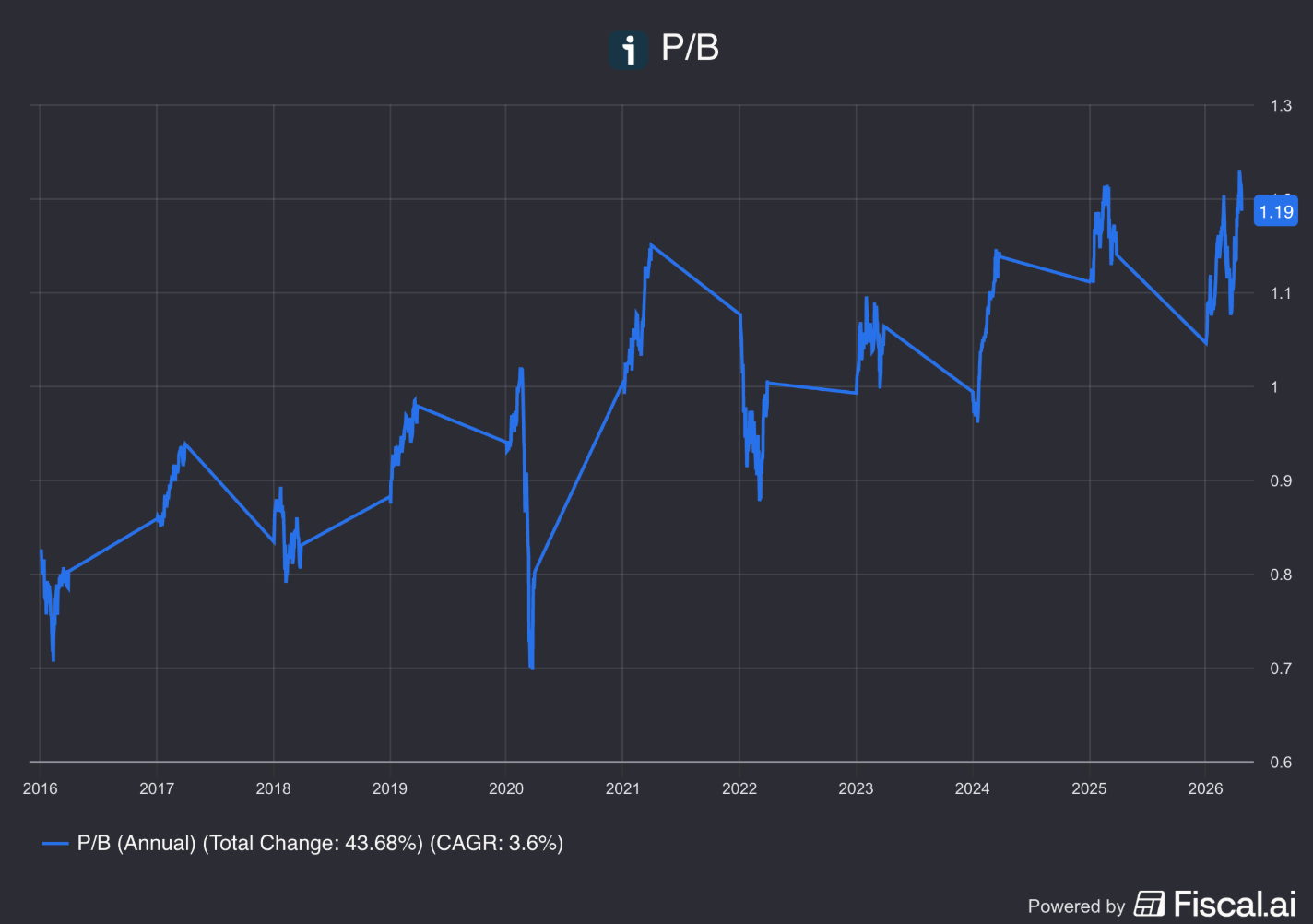

Like most holding companies, Investor AB frequently trades at a discount to the underlying value of its assets.

I think it starts to get interesting at a P/B ratio of 0.9x.

That implies a stock price of around 281 SEK (current stock price: 372 SEK).

KKR ($KKR)

How does the company make money?

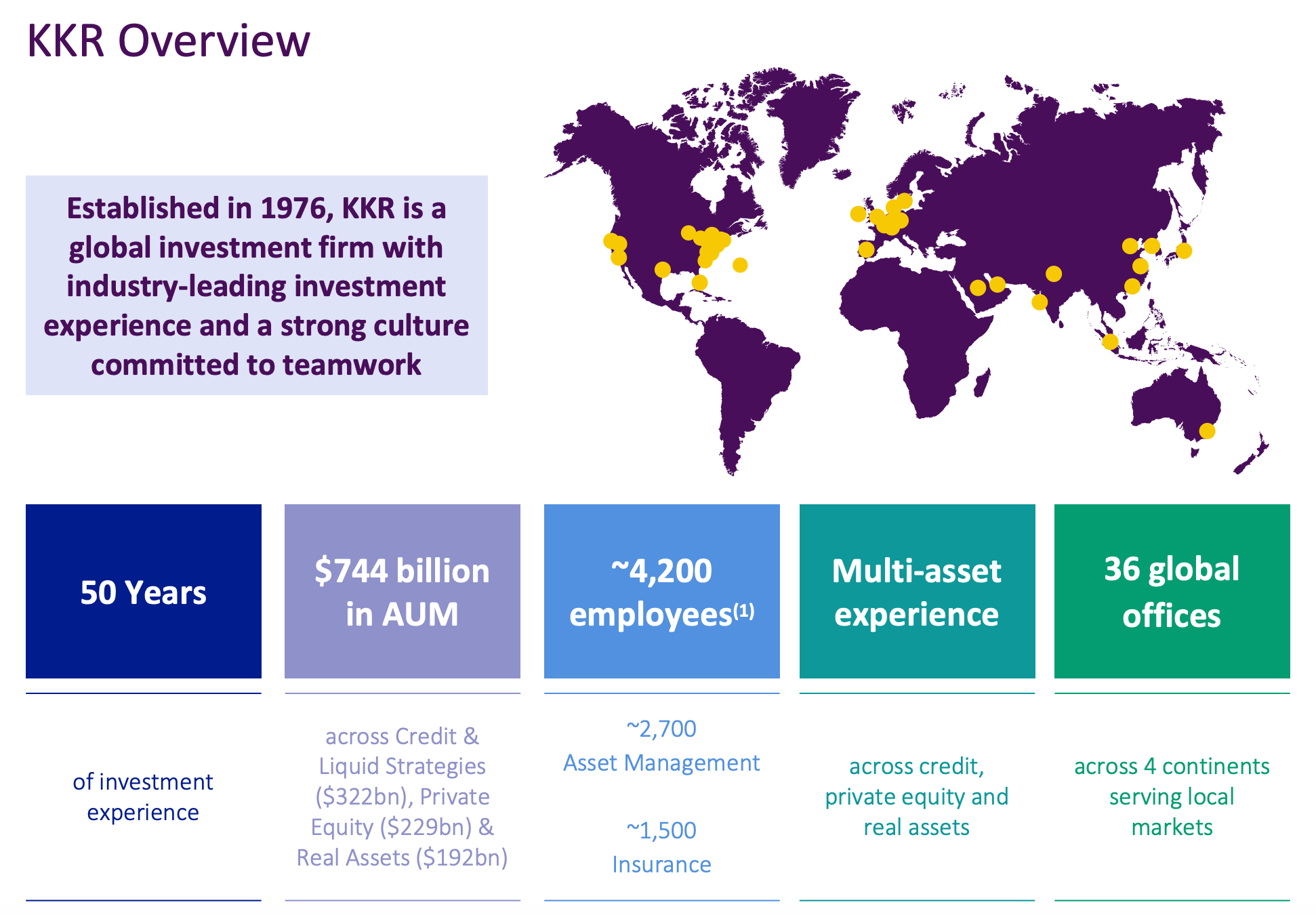

KKR is an American private equity company.

They use money from big clients (like pension funds) to buy and grow other companies, invest in infrastructure and private credit.

They earn recurring fees on the assets they have under management, as well as performance fees (typically around 20%) when they sell an investment for a profit.

Why is it an interesting company?

Strong track record: KKR manages $744 billion across private equity, real estate, infrastructure, and credit. They’ve been doing this since 1976 and are one of the best in the world at it.

Permanent capital: KKR bought Global Atlantic, a life insurer, giving them $321 billion in permanent capital, money that never leaves. They use it to fund their own deals, meaning they can invest without outside money and keep all the profit.

Locked in profits: Most KKR funds have lockup periods of 7-12 years. That means 92% of their AUM is basically locked in. This gives them stable fees and they don’t have to worry about investors panicking and pulling their money out during a market crash.

Massive growth: In 2025, they raised $129 billion in new investment capital. They expect to continue raising over $115 billion every single year, proving that big investors still trust them with their cash.

The stock is on sale: The stock is down nearly 21% this year due to fears around private credit. But KKR’s actual direct lending exposure is just 21% of assets. This looks like an overreaction and a potential opportunity.

At which price are we interested?

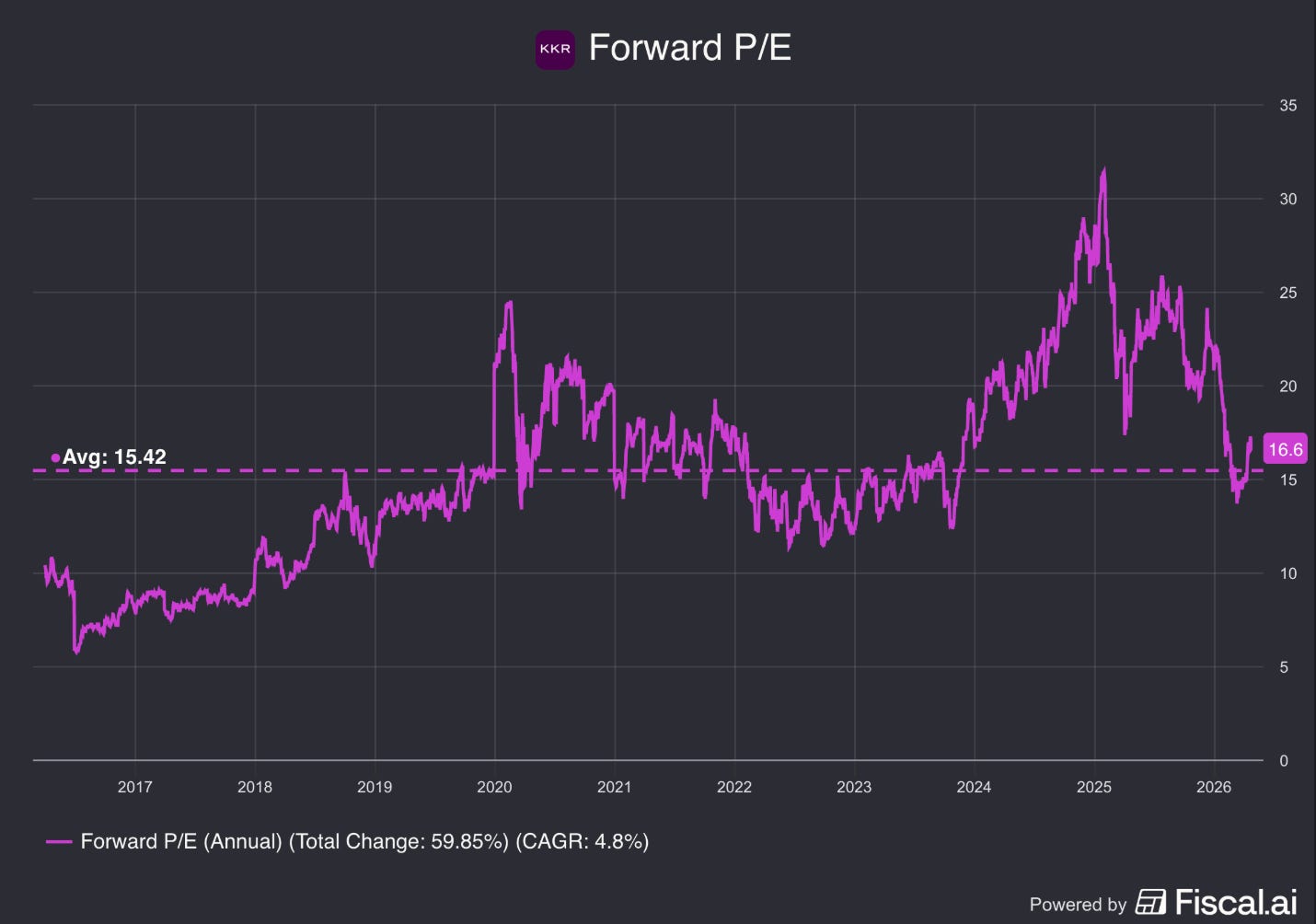

KKR is currently trading near its average Forward P/E over the past decade.

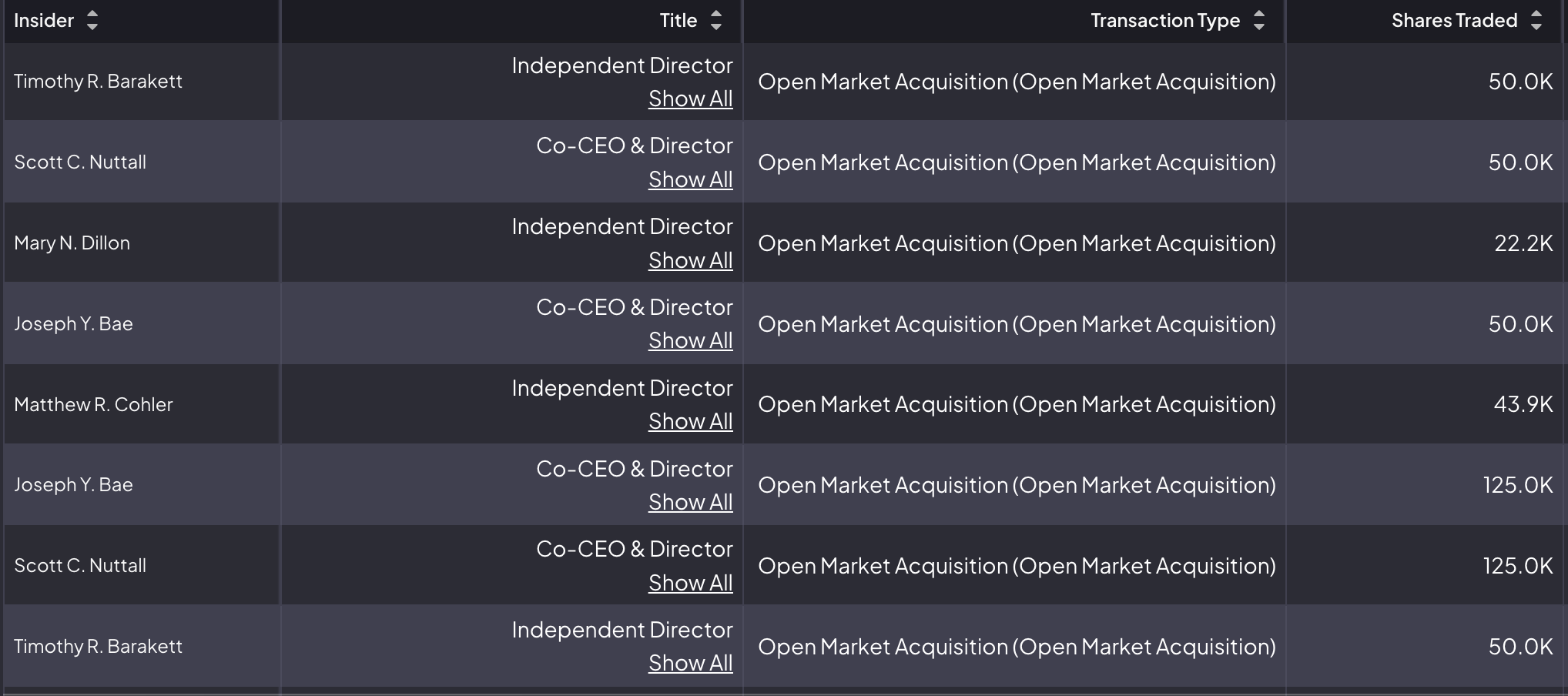

I would say KKR is at or very near an interesting price to buy.

Insiders seem to agree as they have been buying as of late.

Lifco ($LIFCO-B)

How does the company make money?

Lifco is a Swedish serial acquirer focused on small, niche businesses in dental supplies, demolition tools, and systems solutions.

It buys the #1 or #2 company in these small markets, holds them for the long term, and makes them more valuable by improving their operations and buying complimentary companies.

It’s a page right out of Constellation Software’s playbook.

Why is it an interesting company?

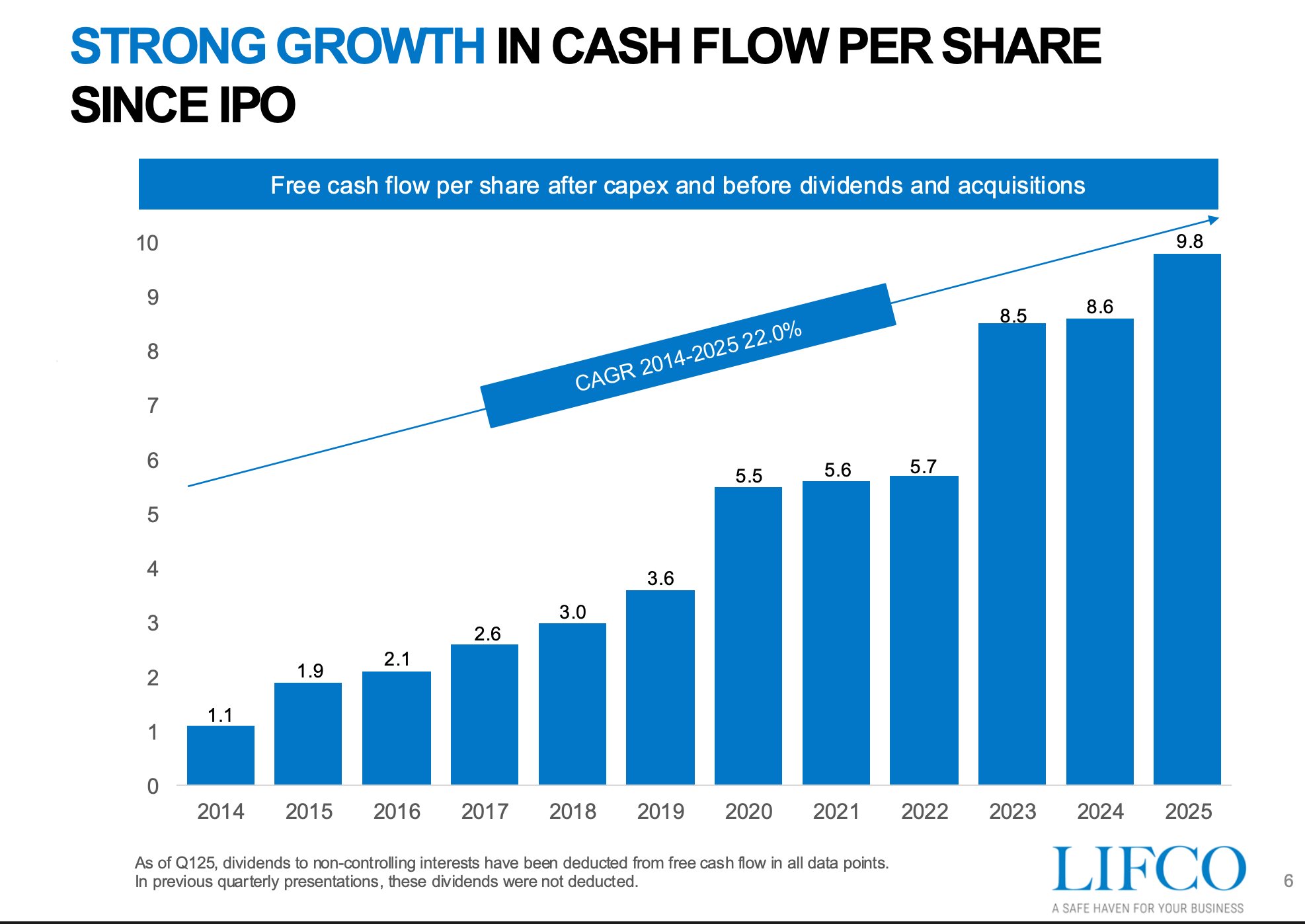

It’s the Swedish Constellation Software: Lifco acquires small, profitable niche businesses and lets them run independently. The decentralized model works. Revenue has grown at more than 13% every year for a decades, and EPS has grown even faster at more than 16% every single year.

It’s got a strong moat: Lifco targets tiny market leaders in specialized niches. Think dental implant systems where switching costs are high, or demolition robots where they set the standard. These companies are too small for larger players to even look at.

The price is getting interesting: Lifco is back to prices we haven’t seen since 2024. It’s not an obvious bargain, but companies of this quality rarely are.

The balance sheet is solid: Interest coverage sits at 10.0x and debt-to-equity at 0.3x. That means they have a solid foundation to keep buying companies.

Serious skin in the game: Carl Bennet owns 50% of the company. The chairman has over half his wealth tied to Lifco’s success. That means the people leading the company are incentivized to make sure you succeed along with them.

At which price are we interested?

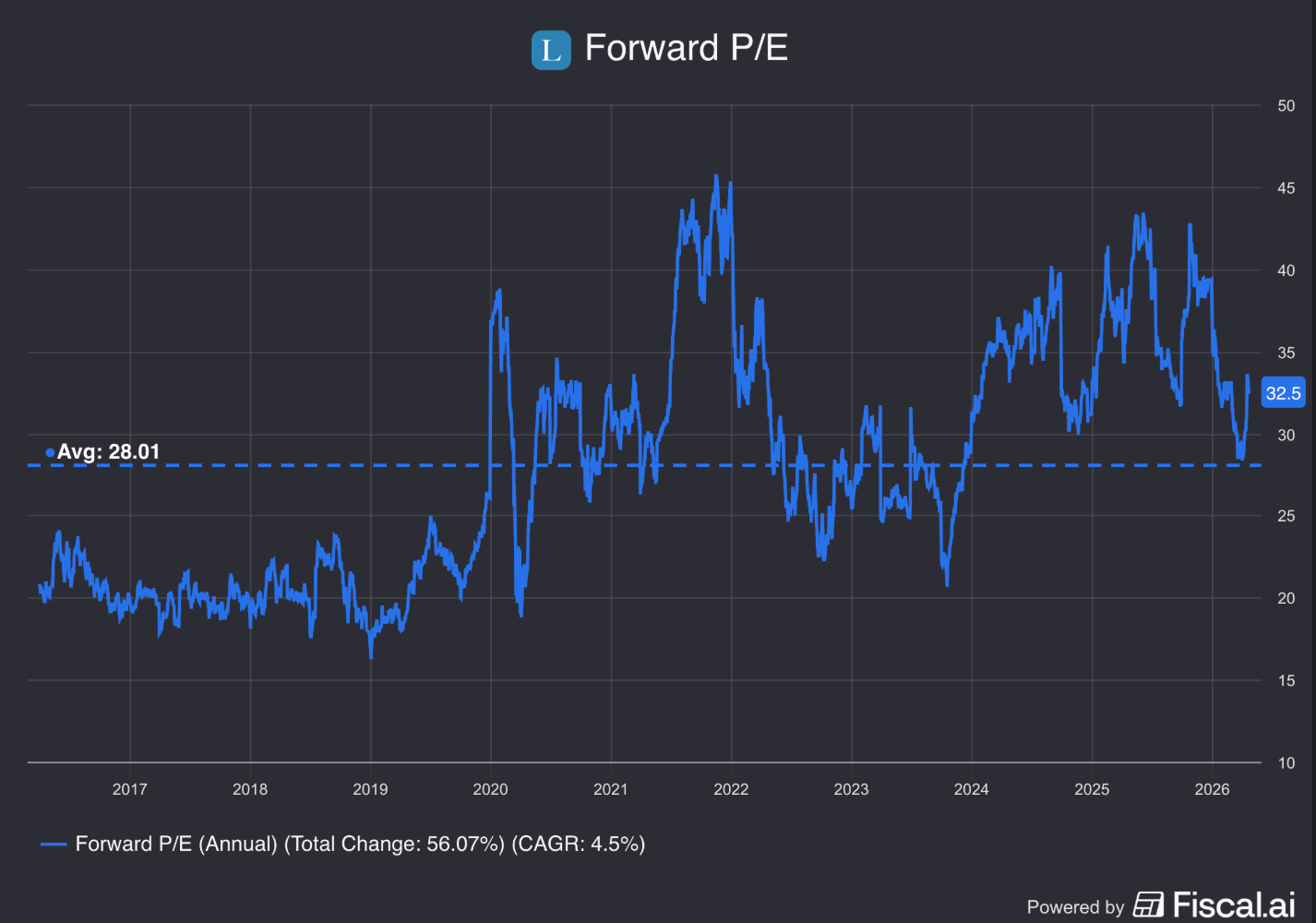

Lifco is never a cheap company.

Since 2020, the cheapest it’s gotten was a Forward P/E of 20x.

We’d love to have another opportunity to buy it at that valuation.

That implies a stock price of 191 SEK (current stock price: 304 SEK).

Now let’s dive into the final companies.