Hi Partner 👋

I’m Pieter and welcome to a 🔒 free edition 🔒 of Compounding Quality.

In case you missed it:

If you haven’t yet, subscribe to get access to these posts, and every post.

Providing software solutions for the healthcare sector is a very attractive business model.

The end market is expected to grow by 16% (!) per year until 2030.

A clear market leader in this? Equasens.

Equasens Group

👔 Company name: Equasens Group

✍️ ISIN: FR0012882389

🔎 Ticker: EPA:EQS

📚 Type: Owner-Operator Stock

📈 Stock Price: €59

💵 Market cap: €900 Million

📊 Average daily volume: €0.45 million

This investment case was made by pharmacist Jim Slater. Jim is a Partner of Compounding Quality and an active member within the Community.

Please note that we also have investment cases of S&P Global, LVMH, Copart, Mastercard, Fortinet, and Lululemon Athletica available on the website.

High APY Potential, Recurring Income, And Diversification?

Finding all three is like searching for a unicorn - private credit deals on Percent are kind of like a unicorn, except they actually exist.

Private credit? Private credit investments are exclusive assets you won't find on public exchanges.

That means they are less correlated to and could be less volatile than public markets.

What else? Some institutional investors are already allocating 23% of their portfolio1 towards alternatives like private credit, but Percent lets regular accredited investors access the same asset class.

You may even find:

Yield potential: current average of 18.1% (as of Mar 31, 2024).

Shorter-term durations: From 6-36 months.

Diversification: Asset-based lending, SMB loans, trade finance, litigation finance, consumer loans and more across North America and Latin America.

Get Up to A $500 Welcome Bonus With Your First Investment*

Onepager

Here’s a onepager with the essentials of Equasens Group.

You can click on the picture to expand it:

1. Do I understand the business model?

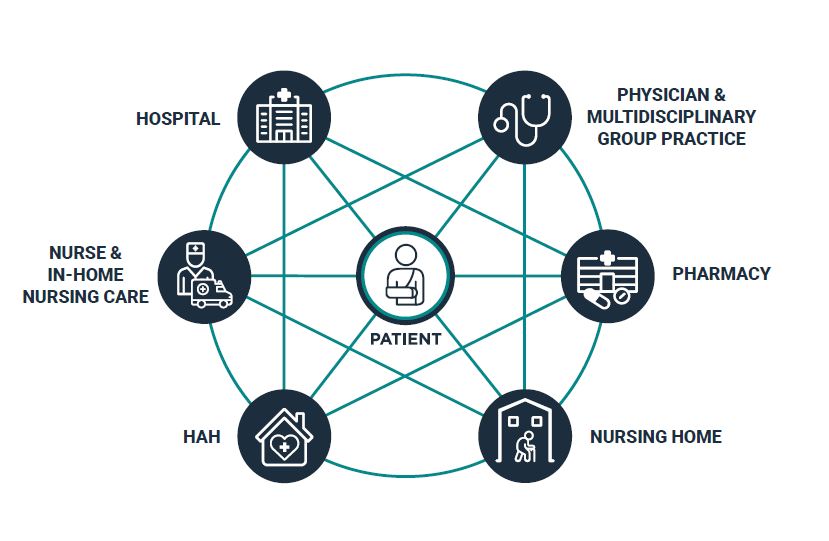

Equasens Group is an expert in professional software solutions for healthcare professionals and establishments. Furthermore, the French company is active in the development of electronic equipment as well as digital and robotic healthcare solutions.

Equasens provides its solutions to retirement homes, hospitals, nursing homes, home hospital care, professional regional healthcare communities, and independent healthcare professionals such as pharmacists, doctors, and nurses.

The systems of Equasens allow 18,000 pharmacies to connect and send orders. Their systems handle over one million transactions per day. The end goal of the company is improved patient care and a more efficient healthcare system.

2. Is management capable?

Equasens was founded in 1996 via the merger of the companies Rousseau and CPI. Thierry Chapusot is the founder and he still serves as the President of the Board today.

Denis Supplisson has been the CEO of Equasens since last year. He has been working for the company since 1991. This underlines the great culture of the company.

The largest shareholder of Equasens is Welcoop. They own 66.7% of the shares.

Thierry Chapusot, the founder of Equasens is the chairman of Welcoop. Welcoop is a community of 3,800 pharmacist cooperative members working to help the profession evolve and grow.

This means we’re talking about an Owner-Operator stock.

3. Does the company have a sustainable competitive advantage?

Equasens is the second largest player in the world when we’re talking about pharmacy management software.

The company can be seen as a market leader in a niche (healthcare IT) with diverse and specialized solutions. They mainly distinguish themselves via continuous adaptation and innovation.

Equasens also enjoys network effects. The more healthcare companies use their services, the more valuable it becomes. Equasens’ solutions become deeply integrated into the user workflows. This creates high switching costs for clients.

The combination of specialized software development, advanced technology integration, and a deep understanding of the European healthcare sector creates a high barrier for (potential) competitors.

4. Is the company active in an attractive end market?

The IT Healthcare sector evolves all the time. Think about artificial intelligence, machine learning, big data analytics, cloud computing, and telemedicine.

These technologies are transforming how healthcare data is managed, how patient care is delivered, and how healthcare operations are streamlined. There’s also a growing consumer preference for personalized, accessible healthcare services.

Equasens should be well-positioned to benefit from this trend.

Another positive? The market should be able to grow at very attractive rates:

“In Europe, the digital health industry is going through a time of rapid expansion and innovation. The market is projected to grow at 16% per year from 2023 to 2030.” - Stephen Viljoen VP of Healthcare & Retail

Some of the competitors include Cerner Corporation and Siemens Healthineers. Cerner Corporation isn’t listed on the stock market. Siemens Healthineers is a spin-off from Siemens. The company IPO’ed in 2017.

Equasens is more profitable and has better capital allocation skills compared to Siemens Healthineers.

5. What are the main risks for the company?

Here are some of the main risks for Equasens:

Regulatory compliance challenges

Data security and privacy concerns

The IT healthcare industry evolves rapidly

Equasens needs to keep investing in R&D to stay ahead of the competition

Dependence on global economic conditions

It’s hard to recruit and retain skilled employees in the industry

Reliance on a few major clients

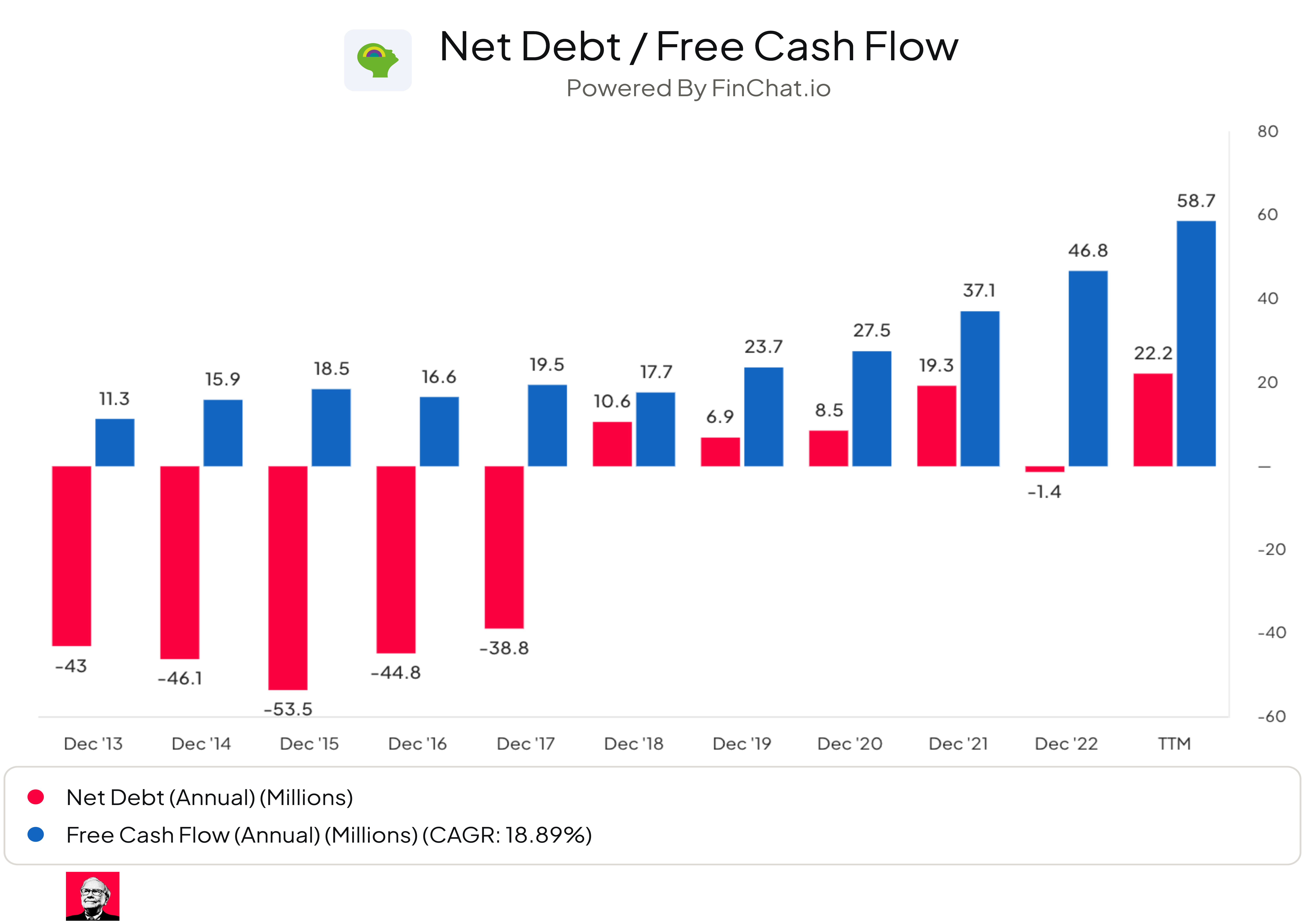

6. Does the company have a healthy balance sheet?

We want to invest in companies that are in good financial shape.

Equasens:

Interest Coverage: 81.1x (Interest Coverage > 15x? ✅)

Net Debt/FCF: 0.4x (Net Debt/FCF < 4x? ✅)

Goodwill/Assets: 23.6% (Goodwill/assets not too large? < 20% ❌)

As you can see, the company’s balance sheet looks healthy.

7. Does the company need a lot of capital to operate?

The less capital a company needs to operate, the better.

Here’s what things look like for Equasens:

CAPEX/Sales: 5.4% (CAPEX/Sales < 5%? ❌)

CAPEX/Operating Cash Flow: 17.0% (CAPEX/Operating CF? < 25% ✅)

On average, around 50% of CAPEX is Growth CAPEX.

8. Is the company a great capital allocator?

Capital allocation is the most important task of management.

Look for companies that put the money of shareholders to work at attractive rates of return.

Here’s what Equasens capital allocation numbers look like:

Return On Equity (ROE): 26.6% (ROE > 20%? ✅)

Return On Invested Capital (ROIC): 15.4% (ROIC > 15%? ✅)

9. How profitable is the company?

The higher the profitability of the company, the better.

Here’s what things look like for Equasens:

Gross Margin: 32.6% (Gross Margin > 40%? ❌)

Profit Margin: 21.8% (Net Profit Margin > 10%? ✅)

FCF/Net Income: 120.6% (FCF/Net Income > 80%? ✅)

These numbers look quite attractive.

It’s also great to see that the company’s profit margin gradually increased from 14.0% in 2013 to 21.8% today.

10. Does the company use a lot of Stock-Based Compensation?

Stock-based compensation is a cost for shareholders and should be treated accordingly.

Preferably we want SBCs as a % of Net Income to be lower than 4%.

SBCs as a % of Net Income higher than 10% are seen as a bad thing.

Equasens uses almost no stock-based compensation to reward managers. This is something we love to see.

11. Did the company grow at attractive rates in the past?

We seek companies that grew their revenue and EPS by at least 5% and 7% per year.

Equasens:

Revenue Growth past 5 years (CAGR): 10.0% (Revenue growth > 5%? ✅)

Revenue Growth past 10 years (CAGR): 7.4% (Revenue growth > 5%? ✅)

EPS Growth past 5 years (CAGR): 14.7% (FCF growth > 7%? ✅)

EPS Growth past 10 years (CAGR): 12.8% (FCF growth > 7%? ✅)

12. Does the future look bright?

You want to invest in companies that manage to grow at attractive rates.

Why? Stock prices tend to follow earnings growth over time.

Equasens:

Expected Revenue Growth next 2 years (CAGR): 5.2% (Revenue growth > 5%? ✅)

Expected EPS Growth next 2 years (CAGR): 4.6% (EPS growth > 7%? ❌)

Expected long-term EPS Growth (CAGR): 17.3% (EPS growth > 7%? ✅)

13. Does the company trade at a fair valuation level?

For Equasens, we use two methods to look at the valuation of a company:

A comparison of the forward PE multiple with its historical average

Earnings Growth Model

A comparison of the multiple with the historical average

The first thing we do is compare the current forward PE with its historical average over the past 5.

Today, Equasens trades at a forward PE of 17.8x versus a historical average of 32.5x over the past 5 years.

Earnings Growth Model

This model shows you the yearly return you can expect as an investor.

In theory, it’s really easy to calculate your expected return:

Expected return = Earnings growth + Shareholder Yield +/- Multiple Expansion (Contraction)

Wherein Shareholder Yield = Dividend Yield + Buyback Yield

Here are the assumptions I use:

Earnings Growth = 8% per year

Shareholder yield = 2.4% (dividend yield)

Forward PE to increase from 17.8x to 17.0x

Expected yearly return = 8% + 2.4% - 0.1* (17.0x-17.8x)/17.8x = 10.0%

14. How did the Owner’s Earnings of the company evolve in the past?

Over time, stock prices tend to follow the Owner’s Earnings of a company (EPS Growth + Dividend Yield).

That’s why we want to invest in companies that managed to grow their Owner’s Earnings at attractive rates in the past.

Equasens:

CAGR Owner’s Earnings (5 years): 16.9% (CAGR Owner’s Earnings > 12%? ✅)

CAGR Owner’s Earnings (10 years): 14.8% (CAGR Owner’s Earnings > 12%? ✅)

15. Did the company create a lot of shareholder value in the past?

We want to invest in companies that managed to compound at attractive rates in the past.

Ideally, the company returned more than 12% per year to shareholders since its IPO.

Here’s what the performance of Equasens looks like:

YTD: -1.0%

5-year CAGR: +0.0%

CAGR since IPO in 2000: +14.0%

Quality Score

Here’s an overview of Equasens based on the 15 Quality Criteria.

Equasens gets a score of 7.5/10:

Do you want more? Check out the investment cases of S&P Global, LVMH, Copart, Mastercard, Fortinet, and Lululemon Athletica?

Whenever you’re ready

That’s it for today. Equasens is a company we don’t own as we see more attractive opportunities in the market today.

If you aren’t yet, become a Partner to get access to the Portfolio:

Email any questions to pieter@compoundingquality.net.

Pieter (Compounding Quality)

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Finchat: Financial data

Special thanks to James Slater

The Community of Compounding Quality is amazing.

Did you like this case? You should thank James Slater, Pharm.D.

James Slater is an invaluable member of the Community and made this investment case about Equasens. James is a shareholder of the company.

Let’s give him a hand!

Do you also want to write an investment case about a company? Let me know and let’s become better investors together.

Nice run down James! Thank you.

Rather than a "one size fits all" in terms of margins, it seems best to make comparisons with similar companies where possible, or at least similar industries.